Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Introduction & Market Context

IPG Photonics Corporation (NASDAQ:IPGP) reported its first quarter 2025 financial results on May 6, revealing a 10% year-over-year revenue decline but improved gross margins. The fiber laser manufacturer continues to navigate challenging market conditions in its traditional cutting and welding segments while seeing growth in emerging applications. The company’s stock closed at $63.13 on May 5, down 1.05% ahead of the earnings release, and remains significantly below its 52-week high of $92.21.

Quarterly Performance Highlights

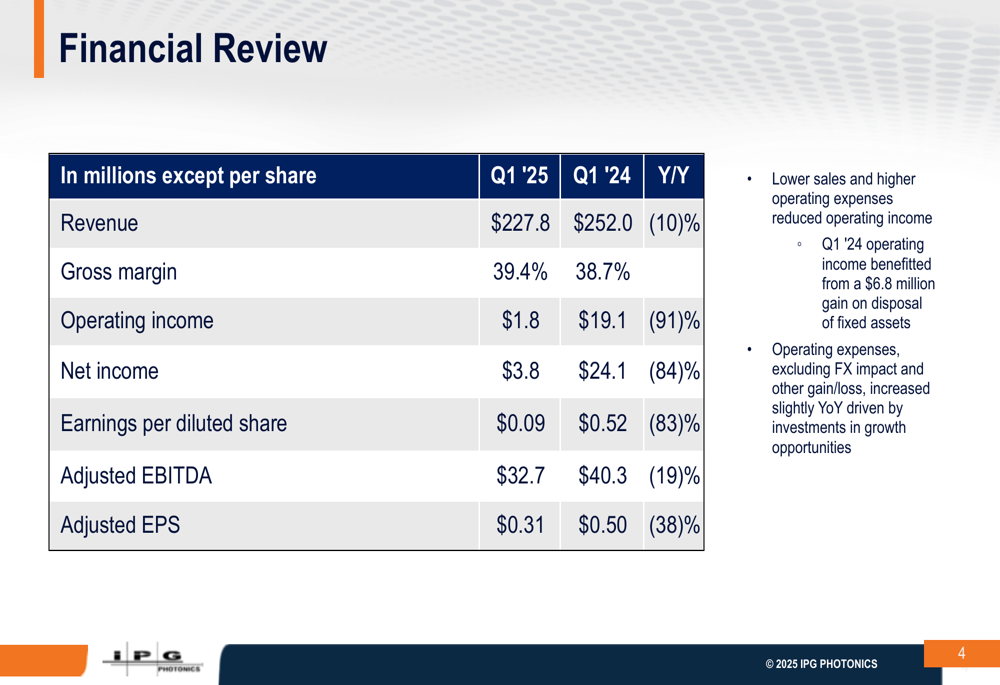

IPG Photonics reported Q1 2025 revenue of $227.8 million, down 10% from $252.0 million in the same period last year. Despite the revenue decline, the company achieved a GAAP gross margin of 39.4%, a 70 basis point improvement year-over-year, which management attributed to reduced inventory provisions and decreased unabsorbed expenses, partially offset by higher product costs.

As shown in the following financial review table, operating income fell sharply to $1.8 million from $19.1 million in Q1 2024, representing a 91% decline:

The steep drop in operating income was partly due to higher operating expenses as the company continued investing in growth opportunities, as well as the absence of a $6.8 million gain on disposal of fixed assets that benefited the prior year’s results. Earnings per diluted share decreased to $0.09 from $0.52 a year earlier, while adjusted EPS came in at $0.31 compared to $0.50 in Q1 2024.

A significant bright spot in the quarterly results was the continued shift toward emerging growth products, which accounted for 51% of total revenue, highlighting the company’s ongoing diversification efforts.

Detailed Financial Analysis

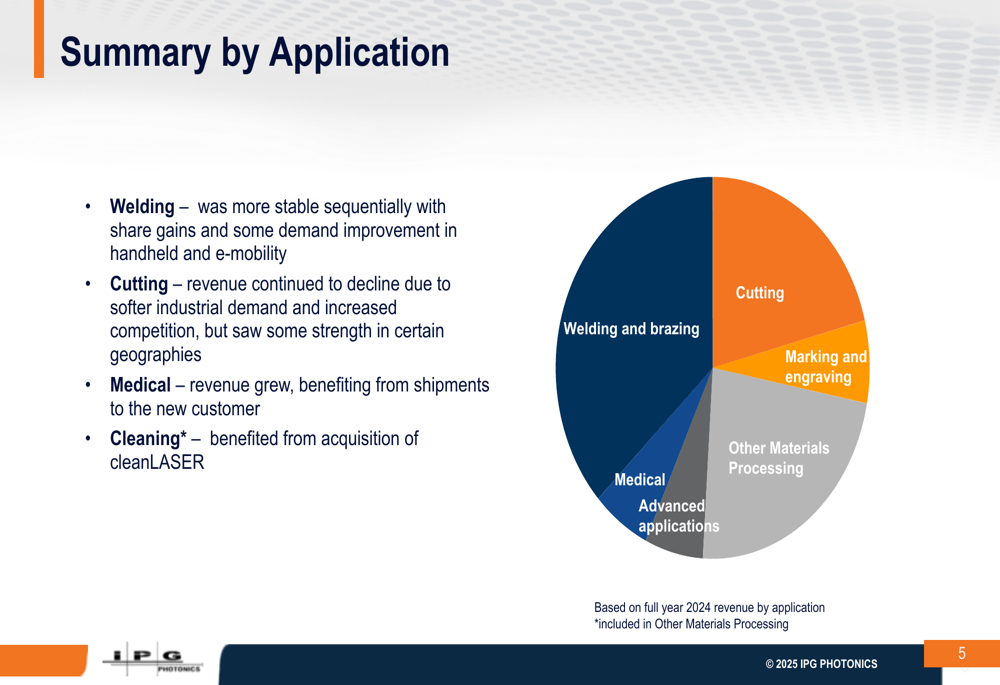

IPG’s revenue performance varied significantly across applications and geographies. The company’s revenue breakdown by application reveals the transition underway in its business mix:

Welding applications showed stability sequentially with share gains in handheld welding and e-mobility applications. However, cutting revenue continued to decline due to softer industrial demand and increased competition, though the company noted some strength in certain geographic markets. Medical (TASE:BLWV) revenue grew, benefiting from shipments to a new customer, while cleaning applications received a boost from the cleanLASER acquisition that was completed following the Q3 2024 results.

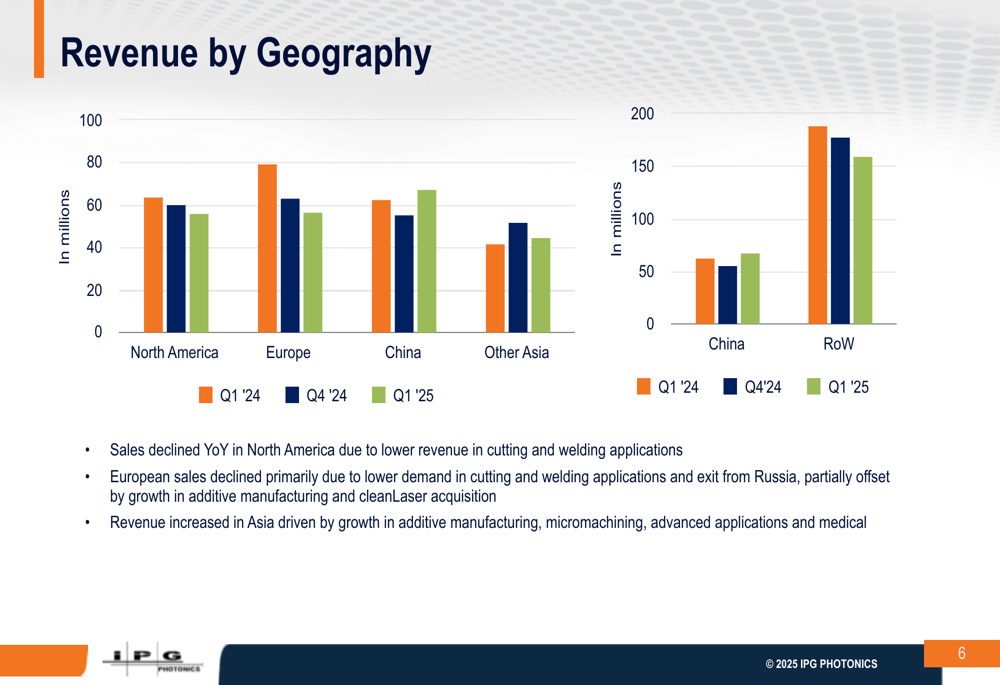

From a geographic perspective, performance was mixed across regions:

Sales declined year-over-year in North America due to lower revenue in cutting and welding applications. European sales also fell, primarily due to reduced demand in cutting and welding applications and the company’s exit from Russia, though this was partially offset by growth in additive manufacturing and the cleanLASER acquisition. In contrast, revenue increased in Asia, driven by growth in additive manufacturing, micromachining, advanced applications, and medical.

Strategic Initiatives

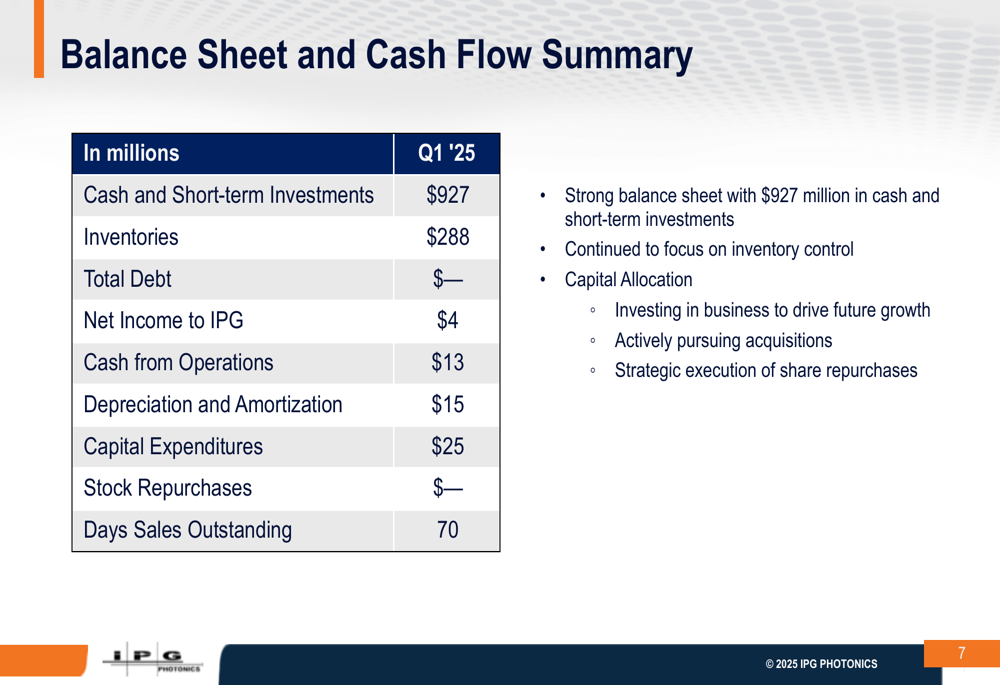

IPG Photonics maintains a strong financial foundation to support its strategic initiatives, as evidenced by its balance sheet and cash flow summary:

The company ended Q1 with $927 million in cash and short-term investments and no debt, though this represents a decrease from the $1 billion reported in Q3 2024. Cash from operations totaled $13 million, while capital expenditures were $25 million. Management emphasized their continued focus on inventory control and strategic capital allocation to drive future growth, including active pursuit of acquisitions.

The company’s investment strategy centers on several key competitive advantages, as illustrated in their investment highlights:

IPG continues to leverage its vertical integration as a competitive edge while enabling greater automation for customers. The company’s high electrical efficiency lasers provide lower energy costs for customers, an increasingly important selling point in many markets. Management’s strategy involves both expanding existing laser applications and displacing non-laser technologies in various industries.

Forward-Looking Statements

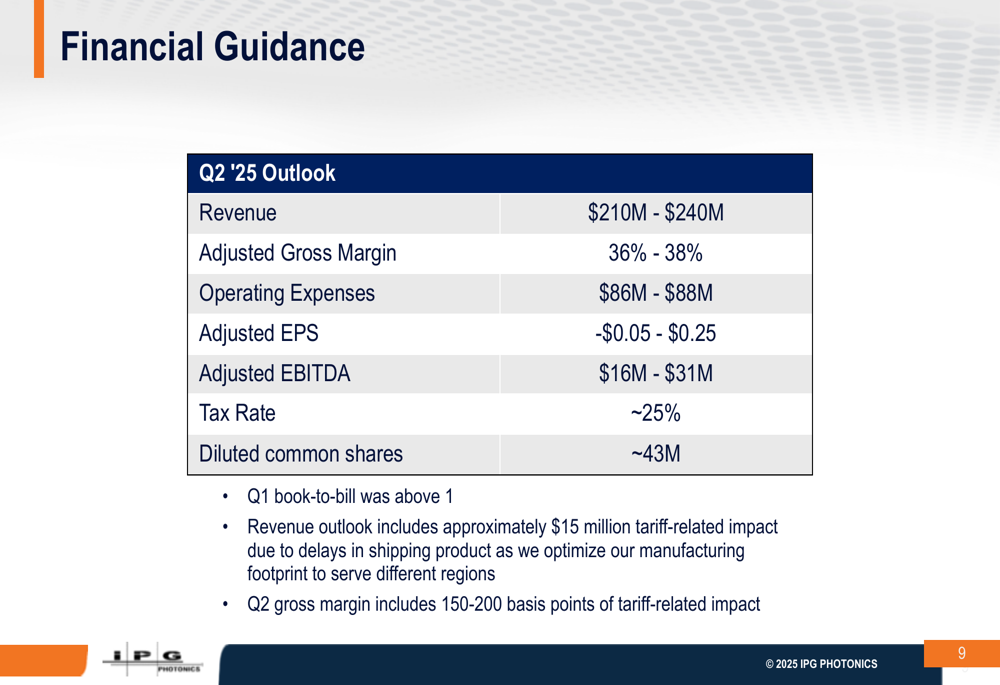

Looking ahead to Q2 2025, IPG Photonics provided the following guidance:

The Q2 outlook includes revenue between $210 million and $240 million, with adjusted gross margin of 36-38% and adjusted EPS ranging from -$0.05 to $0.25. Management noted that the Q1 book-to-bill ratio was above 1, suggesting potential improvement in order trends.

However, the company faces near-term headwinds from tariffs, with approximately $15 million of tariff-related impact expected in Q2 due to delays in shipping products as the company optimizes its manufacturing footprint to serve different regions. The Q2 gross margin guidance includes a 150-200 basis point negative impact from these tariff issues.

The guidance reflects continued challenges in IPG’s traditional markets while the company works to expand its presence in higher-growth applications. Following several quarters of revenue declines, including the 23% year-over-year drop reported in Q3 2024, the company’s Q1 2025 results and Q2 outlook suggest the pace of decline may be moderating, though significant headwinds remain.

As IPG Photonics navigates this transition period, its strong balance sheet provides flexibility to pursue both organic growth initiatives and strategic acquisitions, while the increasing contribution from emerging growth products offers a potential path to returning to overall growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.