Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

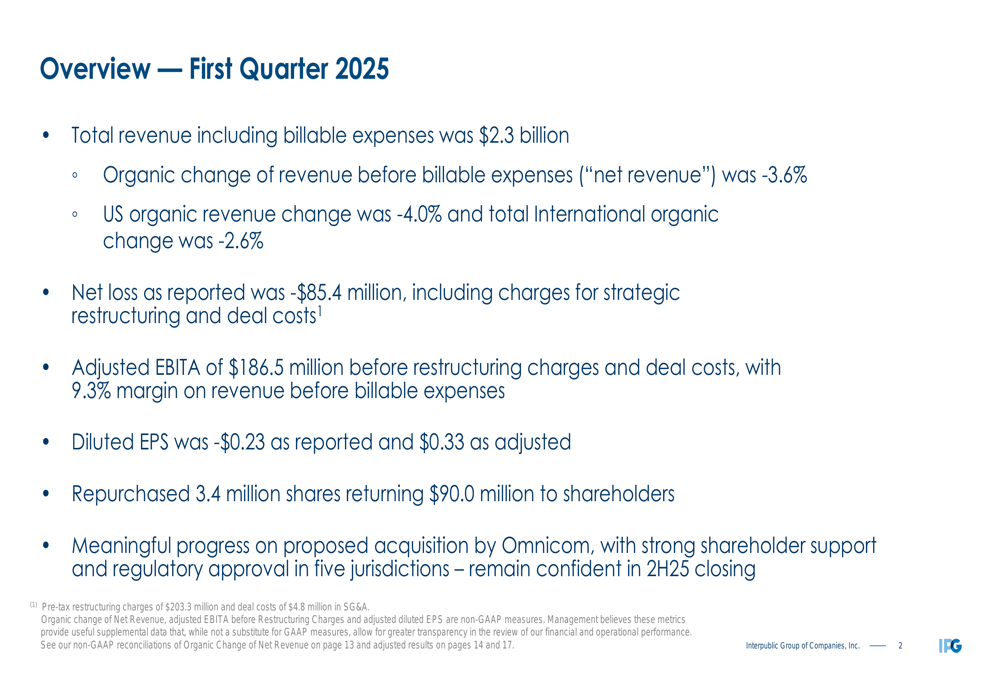

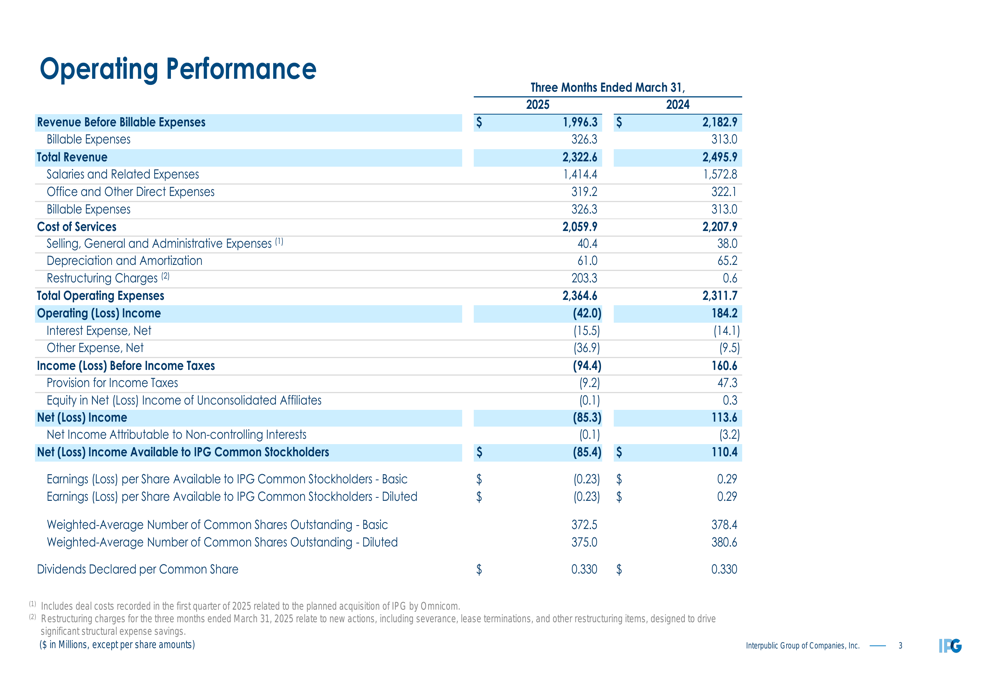

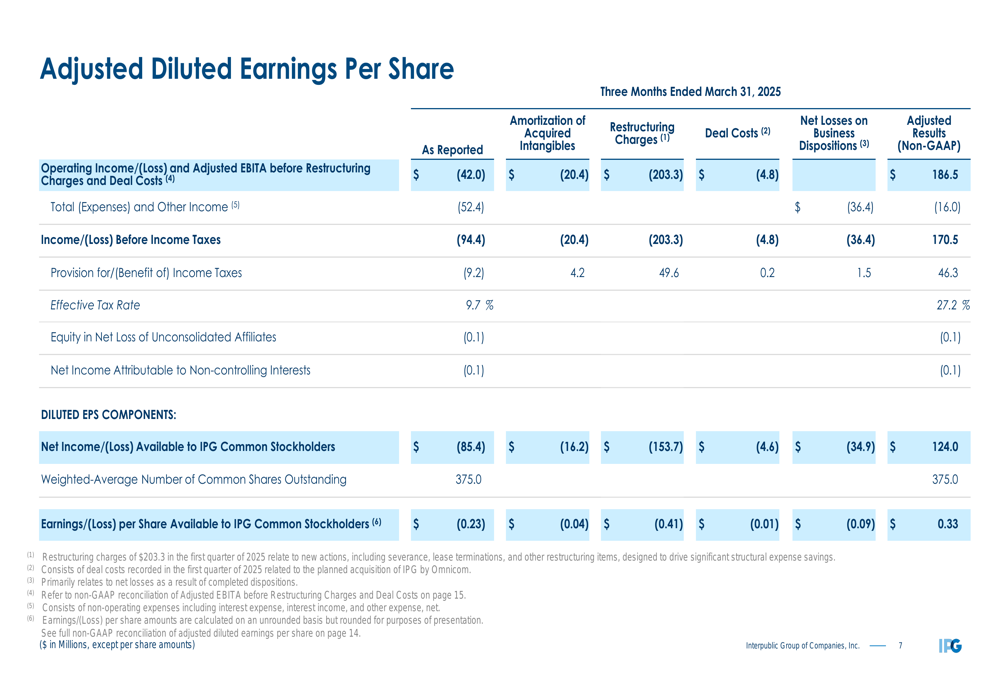

Interpublic Group of Companies Inc (NYSE:IPG) reported a net loss of $85.4 million for the first quarter of 2025, as revealed in its earnings presentation on April 24. The advertising and marketing services giant’s results were significantly impacted by $203.3 million in restructuring charges as the company prepares for its pending merger with Omnicom, expected to close in the second half of 2025.

IPG shares fell 5% in premarket trading to $22.79, approaching the company’s 52-week low of $22.51, as investors reacted to the disappointing results. This follows a challenging Q4 2024, when the company also missed analyst expectations.

Quarterly Performance Highlights

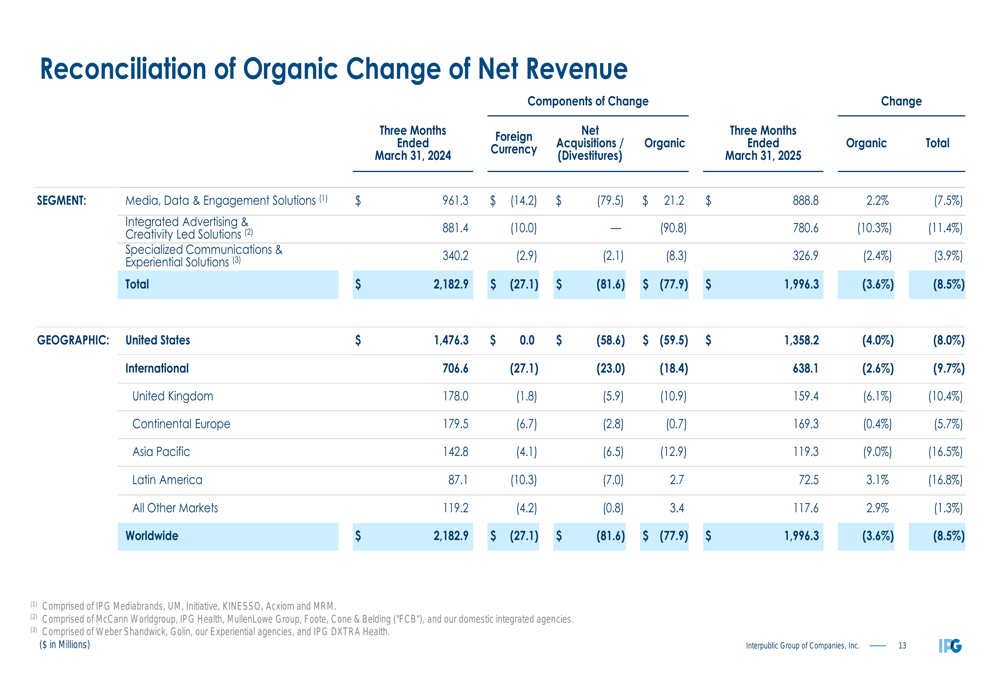

IPG reported total revenue of $2.3 billion for Q1 2025, down from $2.5 billion in the same period last year. The company experienced an organic decline in net revenue of 3.6%, with the US market down 4.0% and international operations declining 2.6%.

As shown in the following overview of first quarter results:

While reported earnings per share came in at -$0.23, adjusted EPS (which excludes restructuring charges and deal costs) was $0.33. The company’s adjusted EBITA reached $186.5 million, representing a 9.3% margin on revenue before billable expenses.

The quarter-over-quarter comparison highlights the significant impact of restructuring charges:

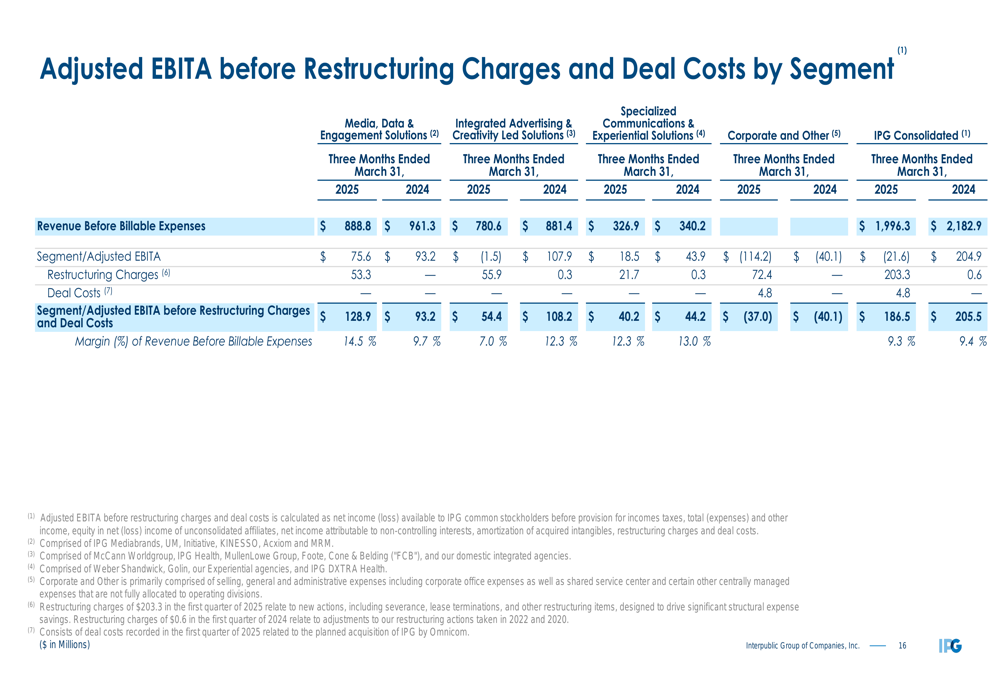

Segment performance varied considerably across IPG’s business units. Media, Data & Engagement Solutions was the only segment showing positive organic growth at 2.2%, while Integrated Advertising & Creativity Led Solutions declined sharply by 10.3%, and Specialized Communications & Experiential Solutions fell by 2.4%.

The following chart provides a detailed breakdown of segment performance:

Regional Performance Analysis

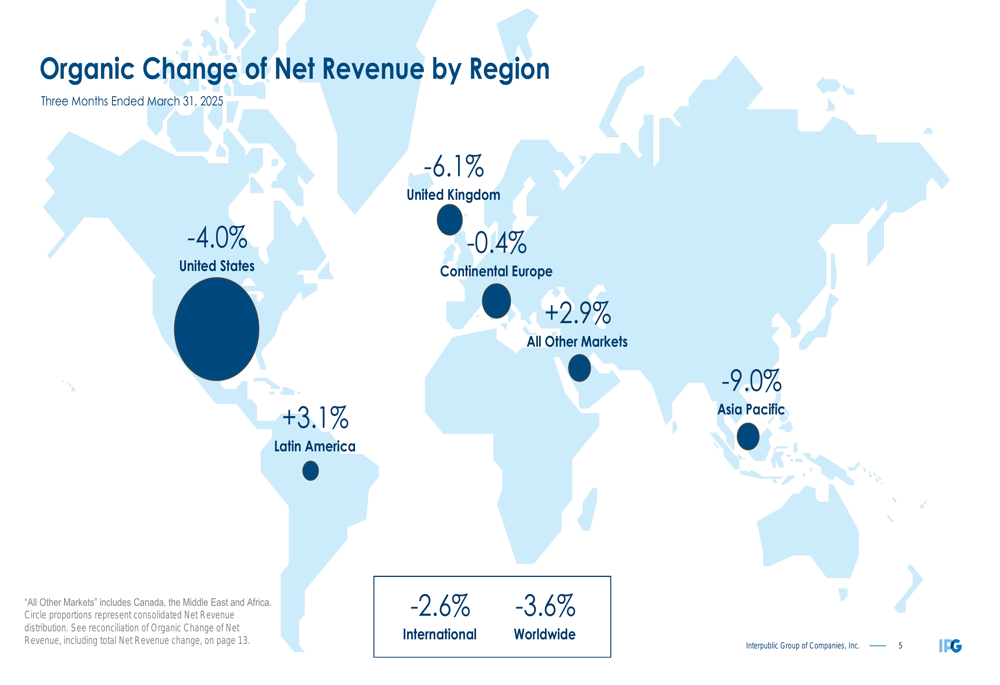

IPG’s regional performance revealed significant geographic disparities. Latin America was a bright spot with 3.1% organic growth, while Asia Pacific suffered the steepest decline at -9.0%. The United Kingdom (TADAWUL:4280) also struggled with a 6.1% drop, while Continental Europe showed more resilience with just a 0.4% decline.

The global map below illustrates these regional variations:

A more detailed reconciliation of organic revenue changes shows how foreign currency effects and acquisition/divestiture activity contributed to the overall revenue picture:

Strategic Initiatives

The substantial restructuring charges of $203.3 million in Q1 2025 (compared to just $0.6 million in Q1 2024) reflect IPG’s strategic preparations for its merger with Omnicom. These charges impacted the company’s bottom line significantly, as shown in the earnings reconciliation:

This restructuring aligns with the company’s previously announced plan in Q4 2024 to implement a $250 million restructuring program. The current quarter’s charges suggest the company is moving quickly to complete these initiatives ahead of the merger.

The Omnicom acquisition, announced earlier this year, is progressing as planned, with the company anticipating a closing in the second half of 2025. This merger represents a significant consolidation in the advertising and marketing services industry.

Financial Position & Outlook

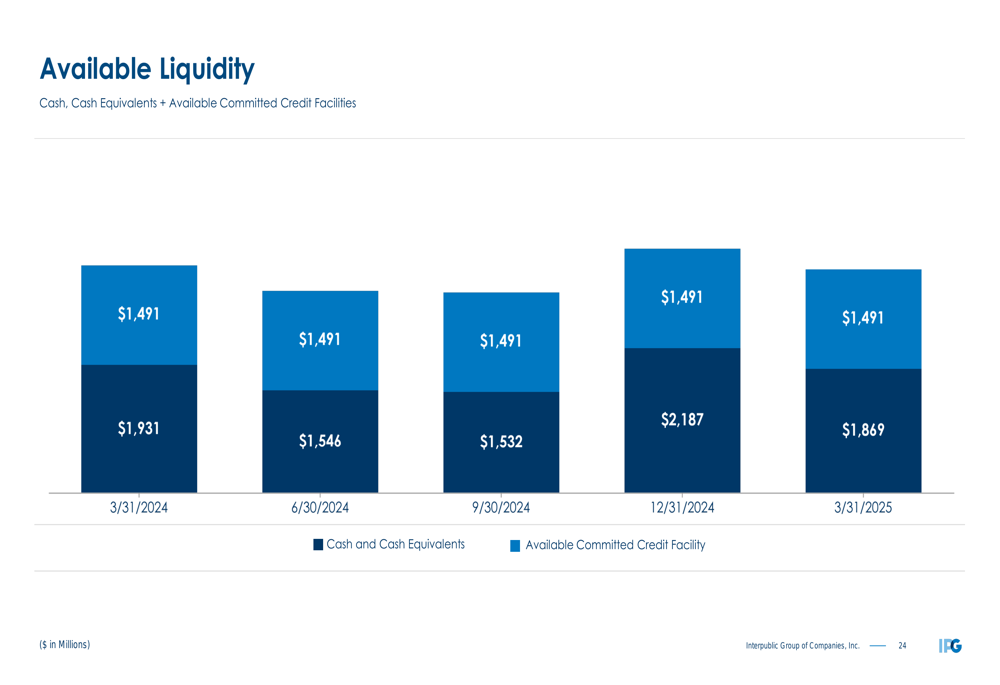

Despite the quarterly loss, IPG maintains a solid liquidity position with $1.87 billion in cash and cash equivalents as of March 31, 2025, plus an additional $1.49 billion in available credit facilities:

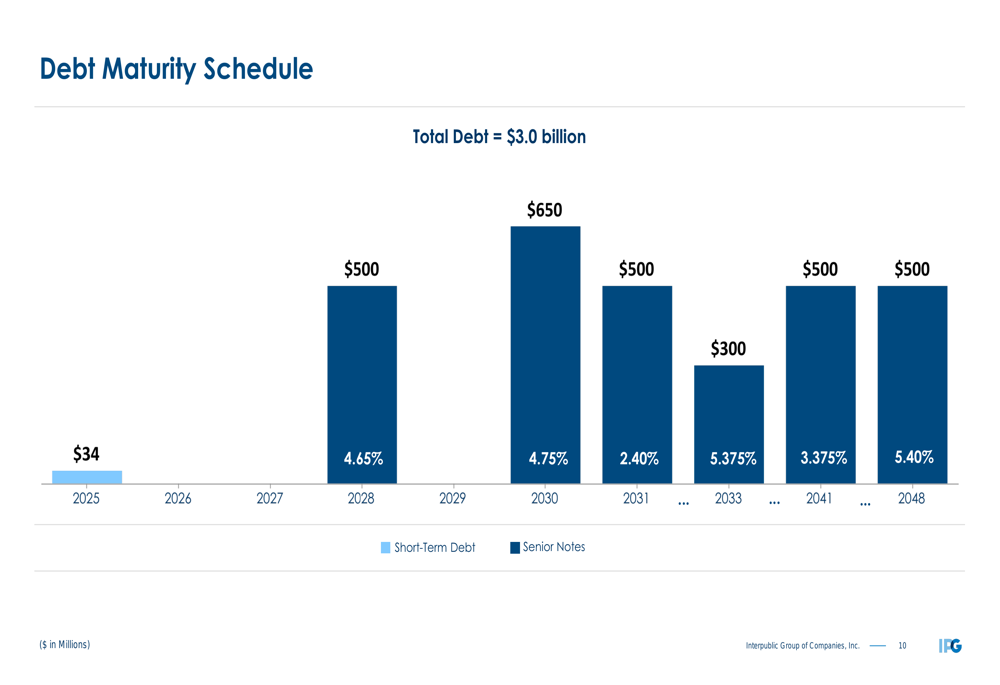

The company’s debt maturity schedule remains well-structured, with minimal near-term obligations. Total (EPA:TTEF) debt stands at $3.0 billion, with only $34 million due in 2025 and no further maturities until 2028:

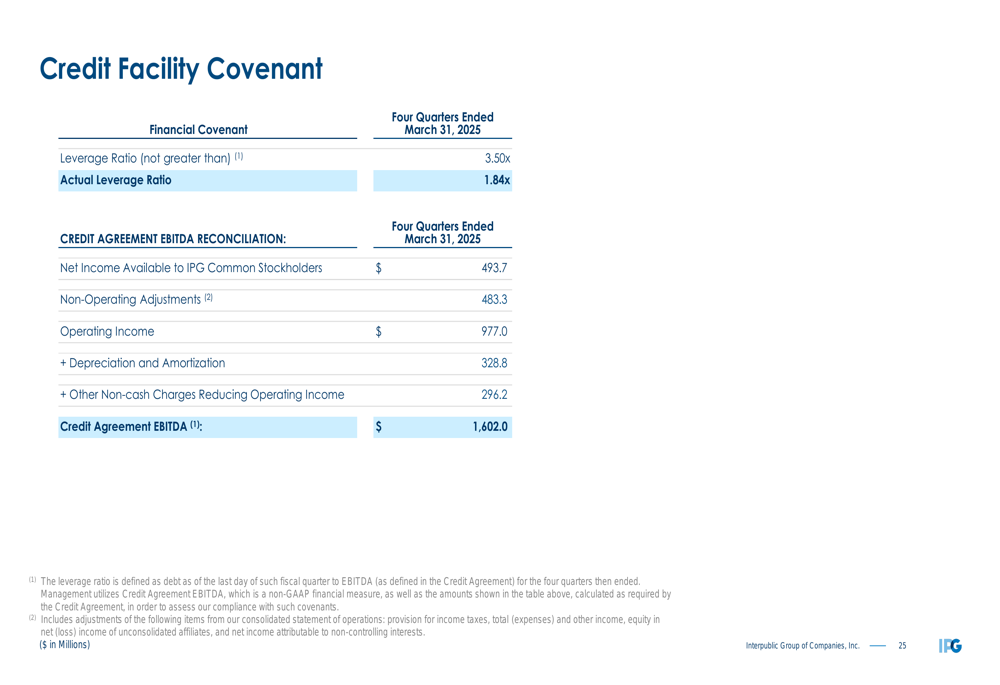

IPG’s leverage ratio of 1.84x remains well below its covenant limit of 3.50x, providing financial flexibility as the company navigates through its restructuring and merger process:

Looking ahead, the company faces continued challenges in 2025. In its previous earnings call, management had targeted an organic revenue decrease of 1-2% for 2025, but the Q1 results (-3.6%) suggest the company may be experiencing more significant headwinds than initially anticipated. The first half of 2025 is expected to be particularly challenging, with potential improvement in the latter part of the year.

As IPG continues its transformation ahead of the Omnicom merger, investors will be closely watching whether the substantial restructuring investments will translate into improved operational efficiency and competitive positioning in the evolving advertising and marketing landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.