CME says all CME Group markets open and trading following outage

Introduction & Market Context

ISA Energia Brasil (ISAE4) presented its second quarter 2025 results on July 31, 2025, revealing a 7.5% year-over-year decline in net revenue to R$1,029 million, while simultaneously accelerating investments in transmission infrastructure. The company's stock closed at R$23.99 on October 14, 2025, near the lower end of its 52-week range of R$20.99 to R$25.43, reflecting investor caution about the company's near-term financial performance despite its long-term growth strategy.

The presentation highlighted ISA Energia's efforts to balance current financial challenges with substantial capital expenditures aimed at future revenue growth. The company maintains an investment-grade rating (AAA from Fitch) and continues to emphasize its resilient business model with inflation-protected revenue streams in Brazil's energy transmission sector.

Quarterly Performance Highlights

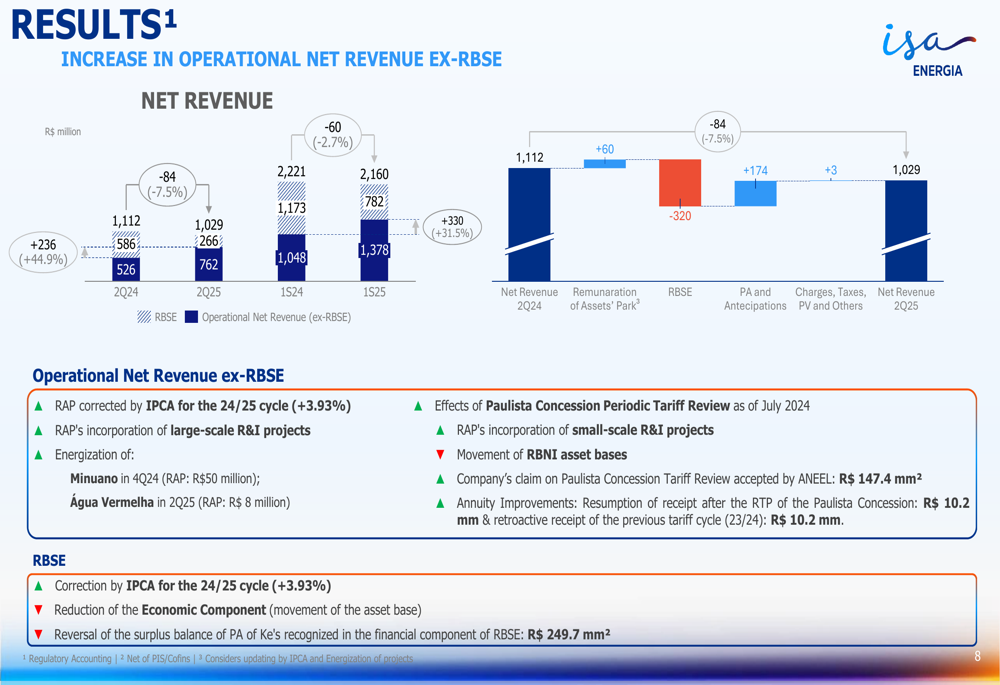

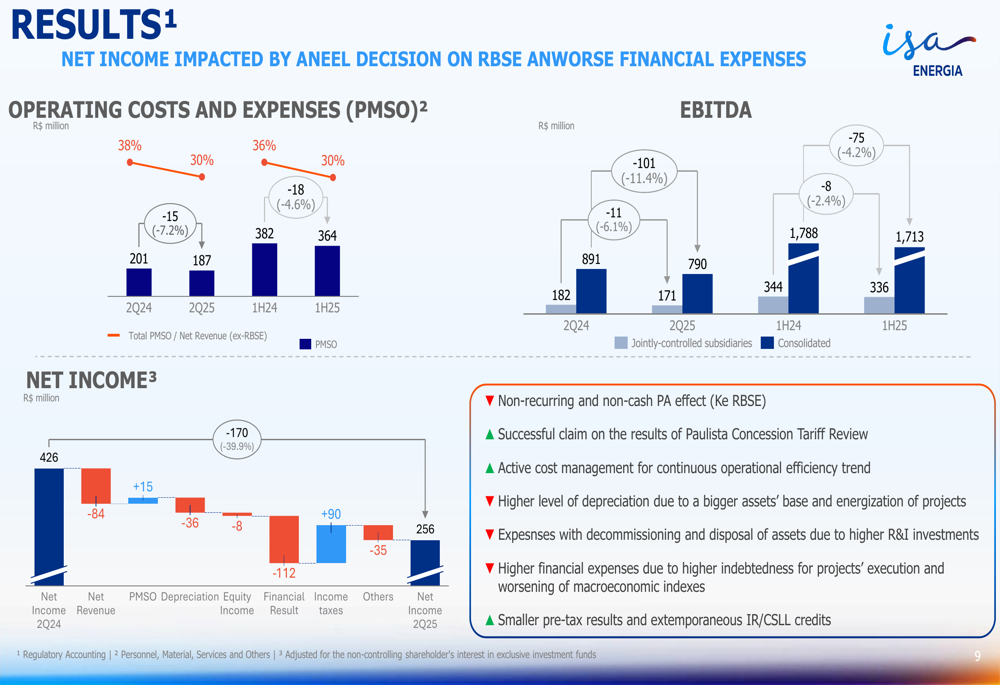

ISA Energia reported a decline in key financial metrics for Q2 2025 compared to the same period last year. Net revenue fell 7.5% year-over-year to R$1,029 million, while EBITDA decreased to R$790 million from R$891 million in Q2 2024. Net income saw a significant drop of approximately 40%, falling to R$256 million from R$426 million in the prior year.

The revenue decline was primarily attributed to the reduction in the RBSE (Rede Básica do Sistema Existente) component, which saw its annual payment decrease from R$1,588 million to R$1,271 million following a final settlement at the administrative level. This was partially offset by a 3.93% IPCA inflation adjustment to the company's RAP (Receita Anual Permitida) for the 2024/2025 cycle.

As shown in the following chart detailing the operational net revenue components:

Despite the overall revenue decline, ISA Energia demonstrated improved operational efficiency, with the ratio of operating costs and expenses (PMSO) to net revenue (excluding RBSE) decreasing from 38% in Q2 2024 to 30% in Q2 2025. This improvement reflects the company's active cost management initiatives amid challenging revenue conditions.

The following chart illustrates the factors affecting net income performance:

Strategic Initiatives and Investments

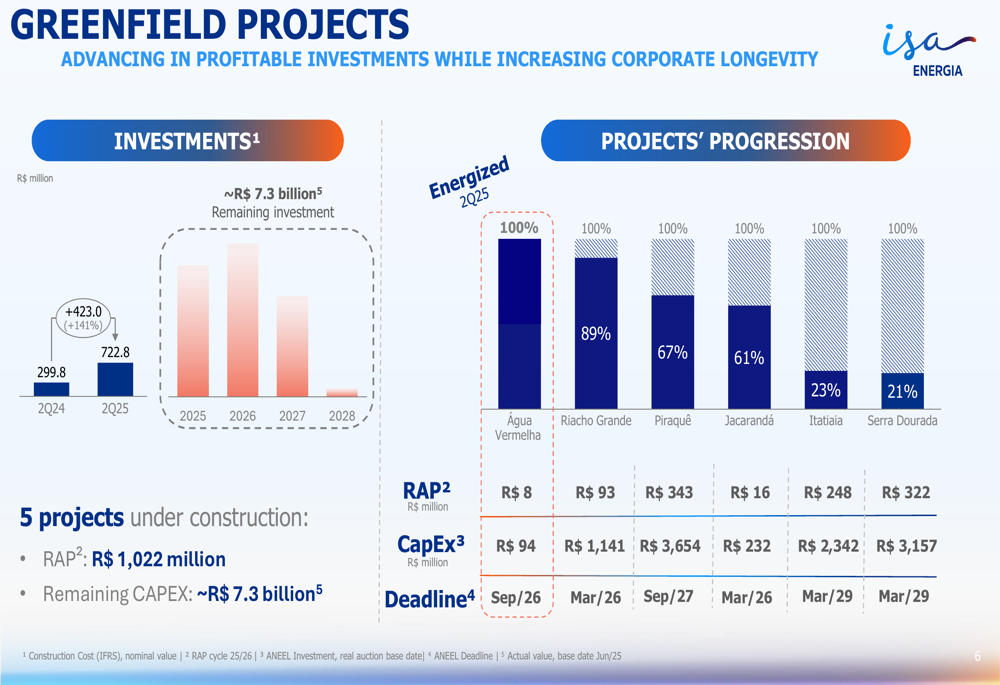

ISA Energia significantly increased its capital investments in Q2 2025, with total investments reaching R$1.1 billion, representing a 72% increase compared to Q2 2024. This acceleration aligns with the company's strategy to expand its transmission infrastructure portfolio through both greenfield projects and improvements to existing assets.

The company highlighted the successful energization of the Água Vermelha Project, completed 16 months ahead of schedule, which will add R$8.5 million to annual permitted revenue (RAP). Currently, ISA Energia has five major projects under construction with a remaining investment of approximately R$7.3 billion, expected to generate significant future revenue streams.

The company's greenfield project portfolio and implementation progress are illustrated in the following chart:

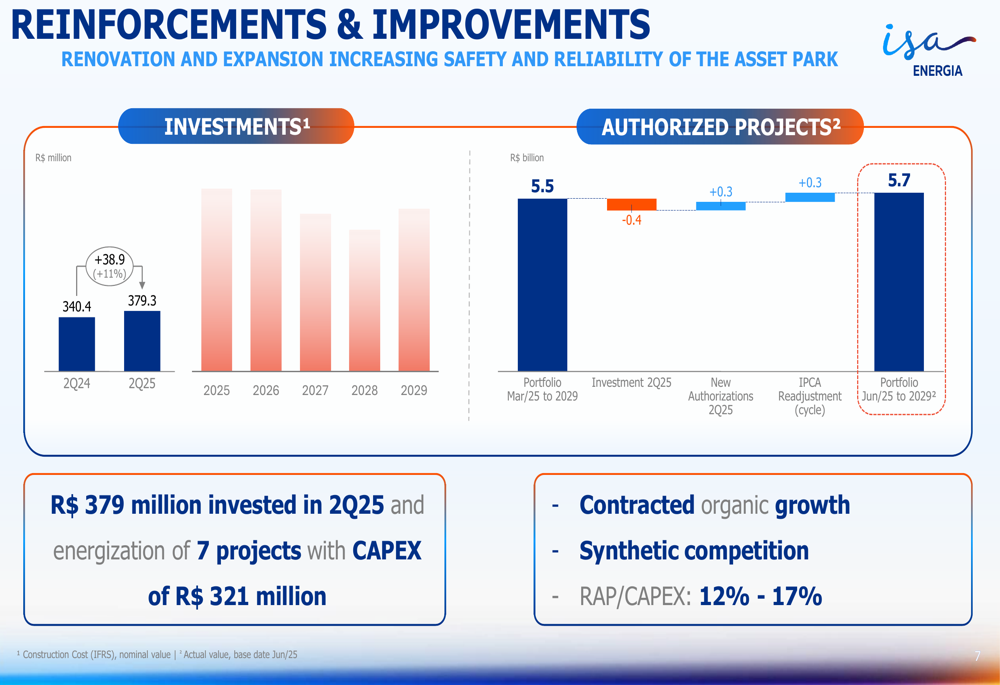

In addition to new projects, ISA Energia invested R$379.3 million in reinforcements and improvements to its existing infrastructure in Q2 2025, an 11% increase from the R$340.4 million invested in Q2 2024. These investments aim to enhance the safety and reliability of the company's transmission assets while generating additional revenue through authorized projects with attractive RAP/CAPEX ratios of 12-17%.

The company's reinforcement and improvement investments are detailed in this chart:

Financial Position and Debt Management

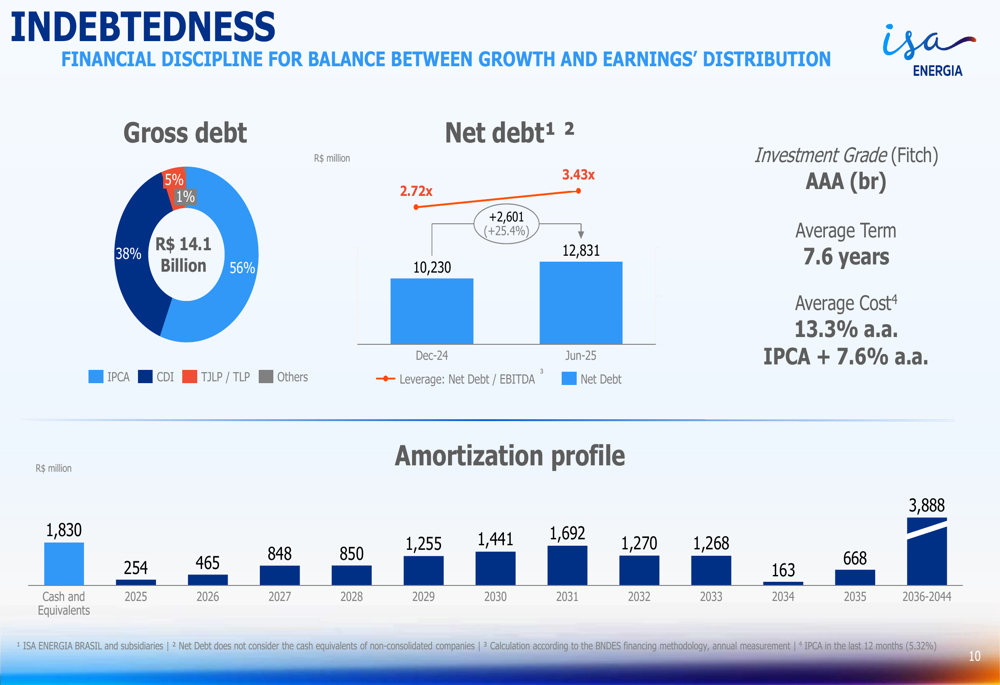

ISA Energia reported gross debt of R$14.1 billion with an average term of 7.6 years and an average cost of 13.3% per annum (IPCA + 7.6% p.a.). The company's leverage ratio, measured as Net Debt/EBITDA, increased to 3.43x as of June 2025, up from 2.72x in December 2024, reflecting the significant capital expenditures for growth projects.

The debt is primarily indexed to IPCA (38%) and other indices (56%), with smaller portions linked to CDI (5%) and TJLP/TLP (1%). The company maintains its investment-grade rating of AAA(br) from Fitch, indicating strong financial credibility despite the increasing leverage.

The following chart details the company's debt structure and amortization profile:

Revenue Outlook and Growth Drivers

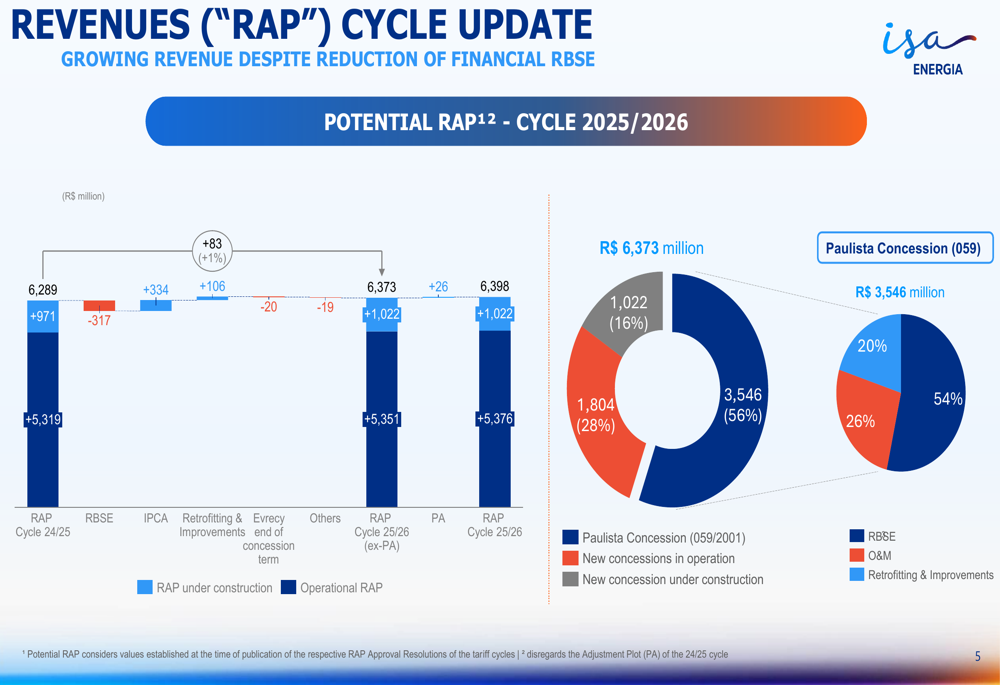

Despite current challenges, ISA Energia's revenue outlook shows potential for growth. The company's RAP for the 2025/2026 cycle is expected to increase by R$84 million (+1.3%) compared to the previous cycle. This growth is driven by a 10.2% increase in the Paulista Concession (excluding RBSE) and a 5.1% increase from new concessions, partially offset by a 9.8% decrease in RBSE.

The company's revenue composition and growth drivers are illustrated in the following chart:

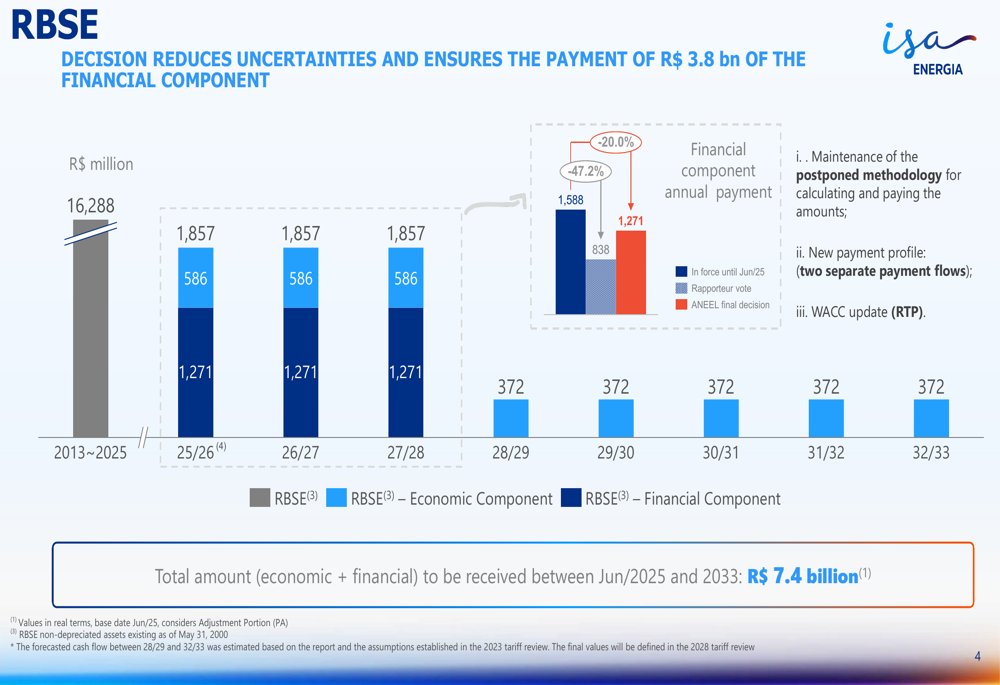

A significant factor affecting ISA Energia's revenue is the RBSE component, which has faced regulatory changes. The company provided details on the new payment profile for RBSE, indicating a total of R$7.4 billion to be received between June 2025 and 2033, with the financial component showing annual payments of R$1,857 million for the next three cycles.

The RBSE payment structure is detailed in this chart:

Sustainability Initiatives

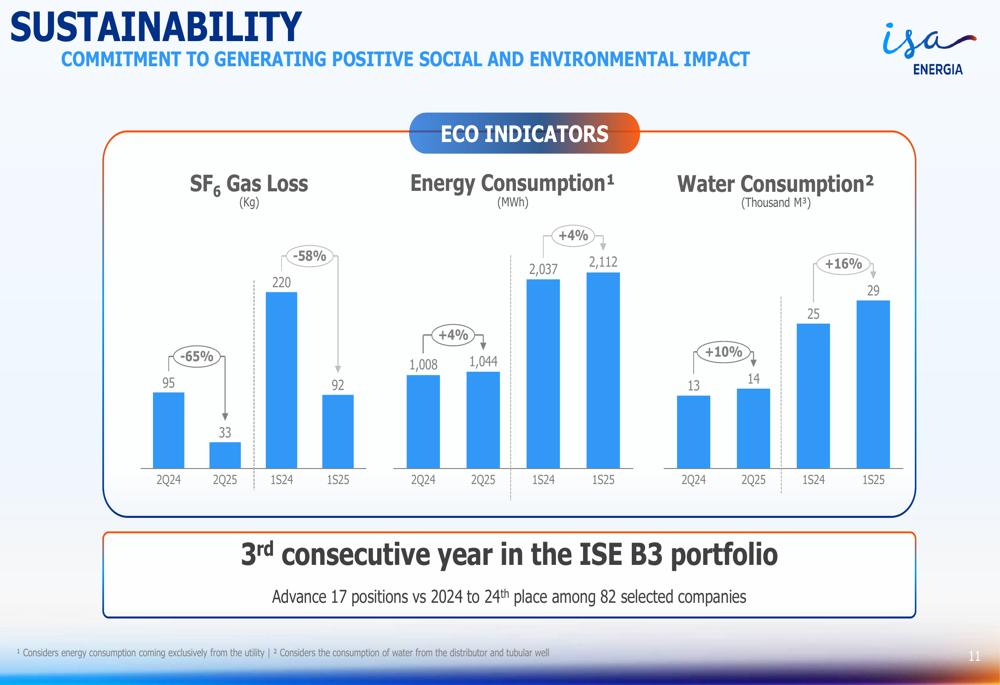

ISA Energia highlighted its commitment to sustainability, noting its third consecutive year in the ISE B3 portfolio and an advancement of 17 positions to 24th place among 82 selected companies. The company reported improvements in key environmental indicators, including a significant reduction in SF6 gas loss from 95kg in Q2 2024 to 33kg in Q2 2025, representing a 65% decrease.

The company's sustainability performance is illustrated in the following chart:

Forward-Looking Statements

Looking ahead, ISA Energia emphasized its focus on balancing growth investments with earnings distribution. The company highlighted five key reasons for investment: a resilient business model with predictable and inflation-proof revenues, opportunities driven by energy transition and network reinforcements, competitive advantages demonstrated by its track record, financial discipline supporting growth with earnings distribution, and a long-term vision creating positive social and environmental impacts.

Management remains confident in the company's ability to navigate current challenges while positioning for future growth through its substantial investment program. The five projects currently under construction are expected to contribute significantly to revenue growth once operational, potentially improving the company's leverage metrics in the medium term.

While the company faces near-term pressure on revenue and profitability, its strategic investments in transmission infrastructure align with Brazil's growing energy needs and the ongoing transition to renewable energy sources, potentially providing long-term value for investors willing to tolerate short-term financial fluctuations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.