Bitcoin price today: struggles at $111k as trade tensions, risk aversion weigh

Introduction & Market Context

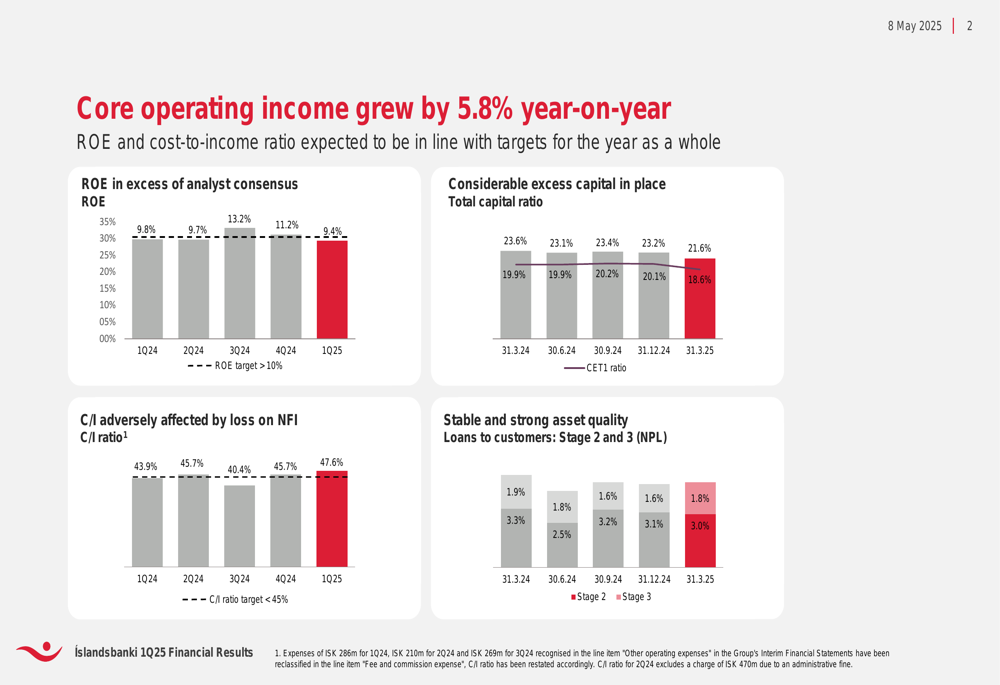

Íslandsbanki (ICE:ISB) presented its first quarter 2025 financial results on May 8, showing core operating income growth of 5.8% year-on-year, though return on equity fell below the bank’s target. The Icelandic lender’s shares closed at ISK 110 on the day of the announcement, up 1.82%.

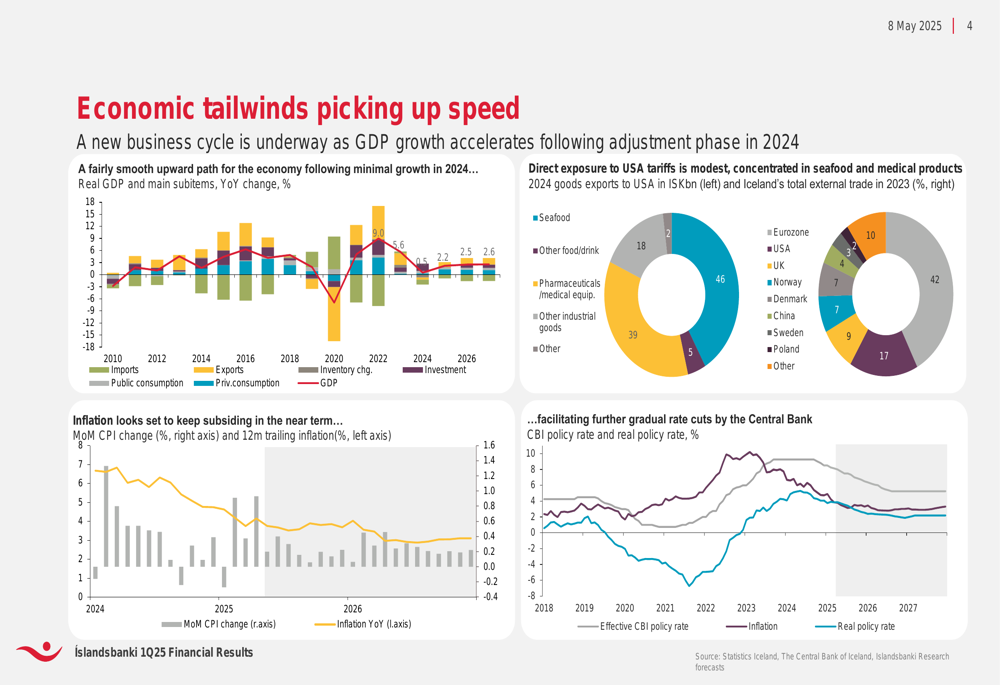

The bank’s presentation highlighted economic tailwinds picking up speed in Iceland, suggesting a new business cycle is underway following minimal growth in 2024. Management noted that direct exposure to U.S. tariffs remains modest, primarily concentrated in seafood and medical products exports.

As shown in the following chart of economic indicators, the bank expects a fairly smooth upward path for the Icelandic economy in the coming years:

Quarterly Performance Highlights

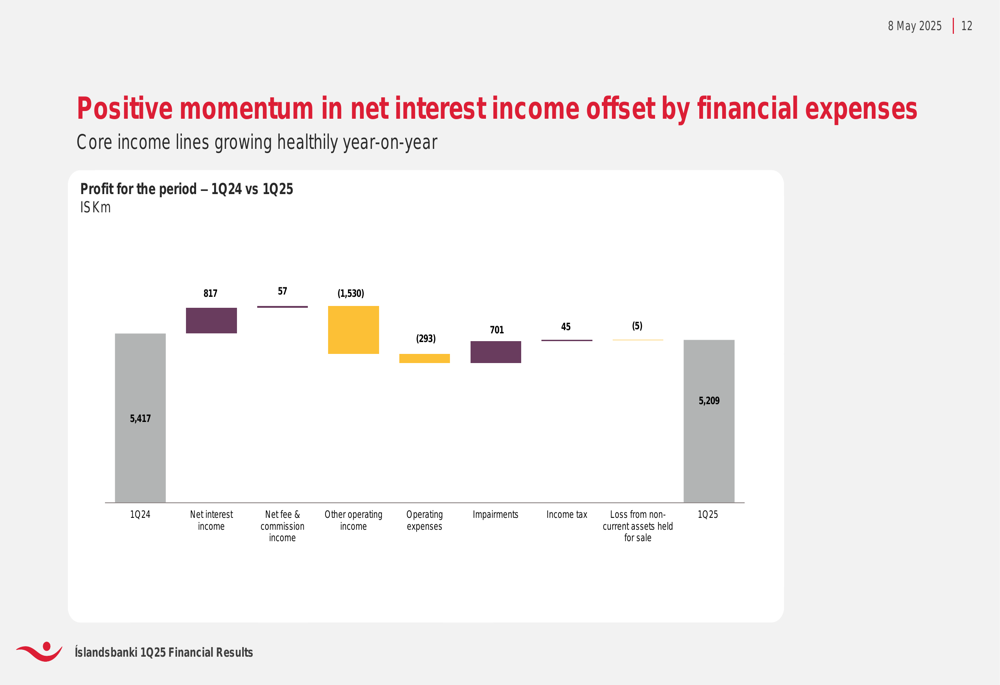

Íslandsbanki reported profit of ISK 5,209 million for Q1 2025, down from ISK 5,417 million in Q1 2024. Return on equity stood at 9.4%, below the bank’s target of 10% and down from 13.2% in the previous quarter. The cost-to-income ratio increased to 47.6%, exceeding the target of 45%.

Despite these challenges, the bank’s core operating income grew by 5.8% year-on-year, with net interest income increasing by ISK 817 million compared to Q1 2024. This positive momentum in interest income was partially offset by a significant decrease in other operating income.

The following chart illustrates key financial metrics across recent quarters:

The bank’s profit bridge for Q1 2025 compared to Q1 2024 shows the components driving the slight decline in overall profit:

Detailed Financial Analysis

Capital ratios showed a decline compared to previous quarters, with the CET1 ratio at 18.6% (down from 20.1% in Q4 2024) and the total capital ratio at 21.6% (down from 23.2%). Despite the decrease, the bank maintains considerable excess capital, with CET1 excess at 320 basis points above requirements.

Asset quality remained relatively stable, with a slight increase in Stage 3 loans (non-performing loans) to 1.8% from 1.6% in the previous quarter. Stage 2 loans decreased marginally to 3.0% from 3.1%.

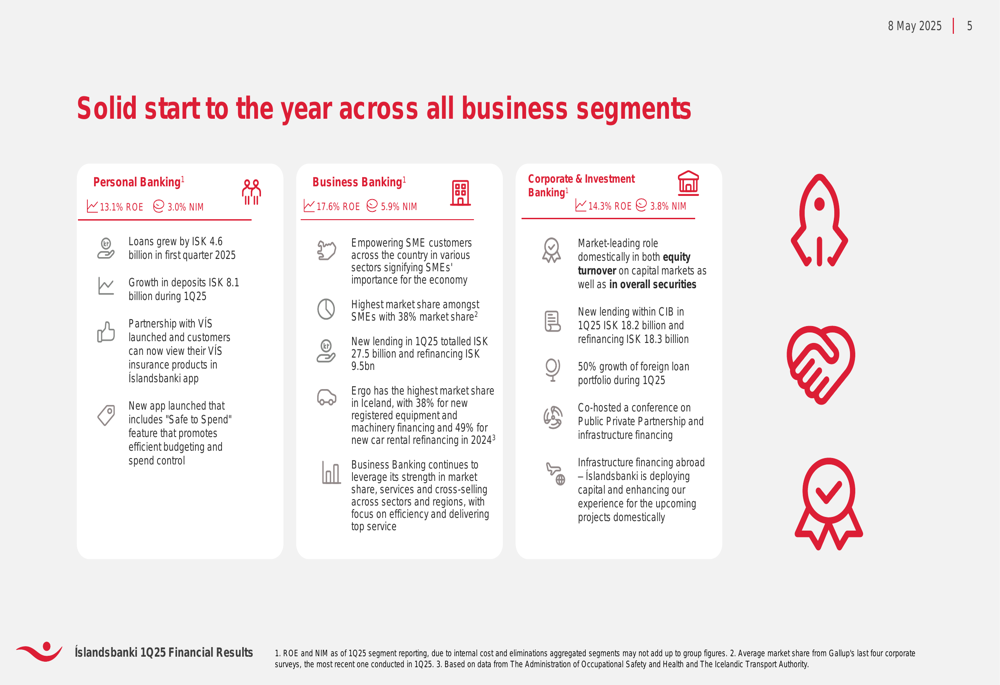

All business segments delivered solid performance in Q1 2025:

- Personal Banking: 13.1% ROE, 3.0% NIM, with loans growing by ISK 4.6 billion

- Business Banking: 17.6% ROE, 5.9% NIM, with new lending of ISK 27.5 billion

- Corporate & Investment Banking: 14.3% ROE, 3.8% NIM, with 50% growth in foreign loan portfolio

The segment performance is summarized in the following slide:

Strategic Initiatives

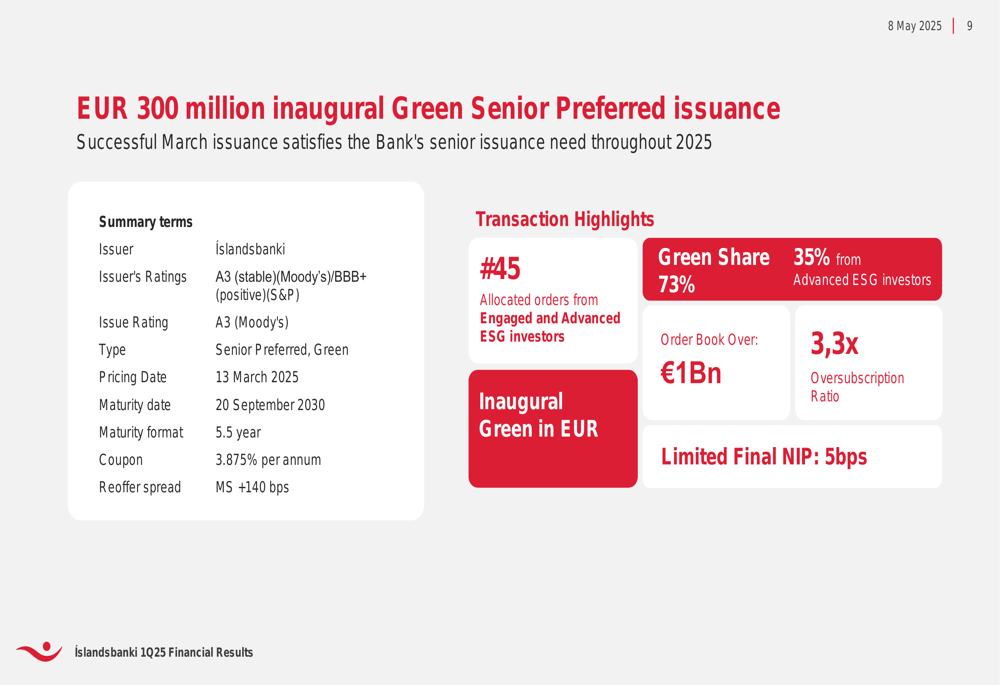

Íslandsbanki successfully issued its inaugural EUR 300 million Green Senior Preferred bond in March 2025, satisfying the bank’s senior issuance needs for the year. The transaction attracted significant interest, with an order book exceeding EUR 1 billion and an oversubscription ratio of 3.3x. Notably, 73% of allocated orders came from ESG investors.

The details of this green bond issuance are presented below:

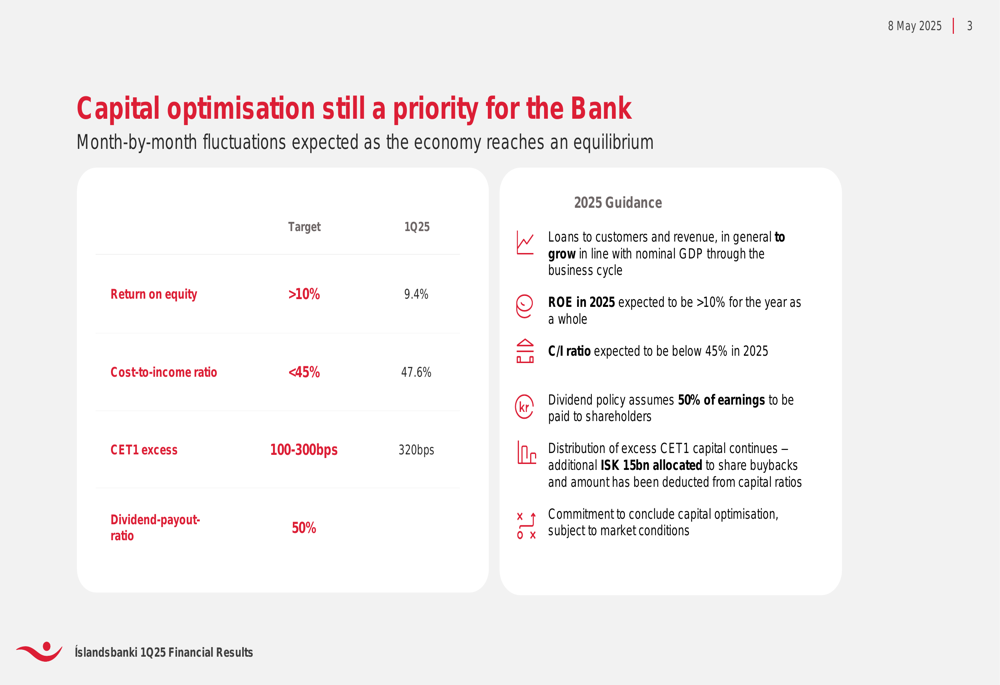

The bank continues to prioritize capital optimization, with an additional ISK 15 billion allocated to share buybacks. The dividend policy assumes 50% of earnings will be paid to shareholders. The government of Iceland remains the largest shareholder with a 45.4% stake and has indicated its intention to continue selling down its position in 2025.

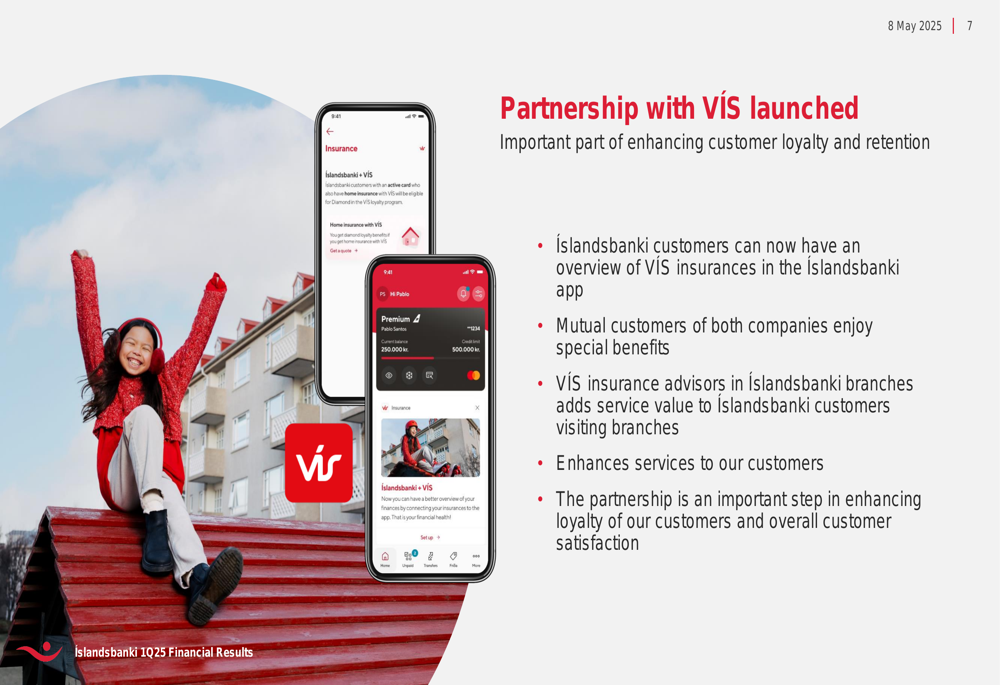

Íslandsbanki also highlighted its partnership with VÍS insurance company, which allows customers to view their VÍS insurances directly in the Íslandsbanki app. This strategic alliance aims to enhance customer loyalty and retention.

The bank showcased its financing of the Samherji Salmon Garden project, with total funding of EUR 235 million, demonstrating its commitment to supporting sustainable aquaculture:

Forward-Looking Statements

For 2025, Íslandsbanki provided guidance that loans to customers and revenue are expected to grow in line with nominal GDP. The bank anticipates achieving its ROE target of above 10% for the full year, despite falling short in Q1. Similarly, the cost-to-income ratio is expected to improve to below 45% for the year.

The bank’s capital optimization priorities and 2025 guidance are summarized in the following slide:

Management emphasized that month-by-month fluctuations in capital metrics are expected as the economy reaches equilibrium. The bank remains committed to concluding its capital optimization program, subject to market conditions, while maintaining its focus on digital innovation to enhance customer experience and operational efficiency.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.