Goldman Sachs expects Nvidia ’beat and raise,’ lifts price target to $240

Introduction & Market Context

ITAB Shop Concept AB (STO:ITAB) presented its third-quarter 2025 results on October 30, showing strong profit development despite currency headwinds. The retail solutions provider’s stock surged 19.54% following the announcement, reaching SEK 21.4 from the previous close of SEK 17.9, reflecting investor confidence in the company’s strategic direction and financial performance.

As a leader in European retail solutions with global reach, ITAB continues to execute its transformation strategy while integrating its significant HMY acquisition, which is expected to deliver substantial synergies by 2027.

Quarterly Performance Highlights

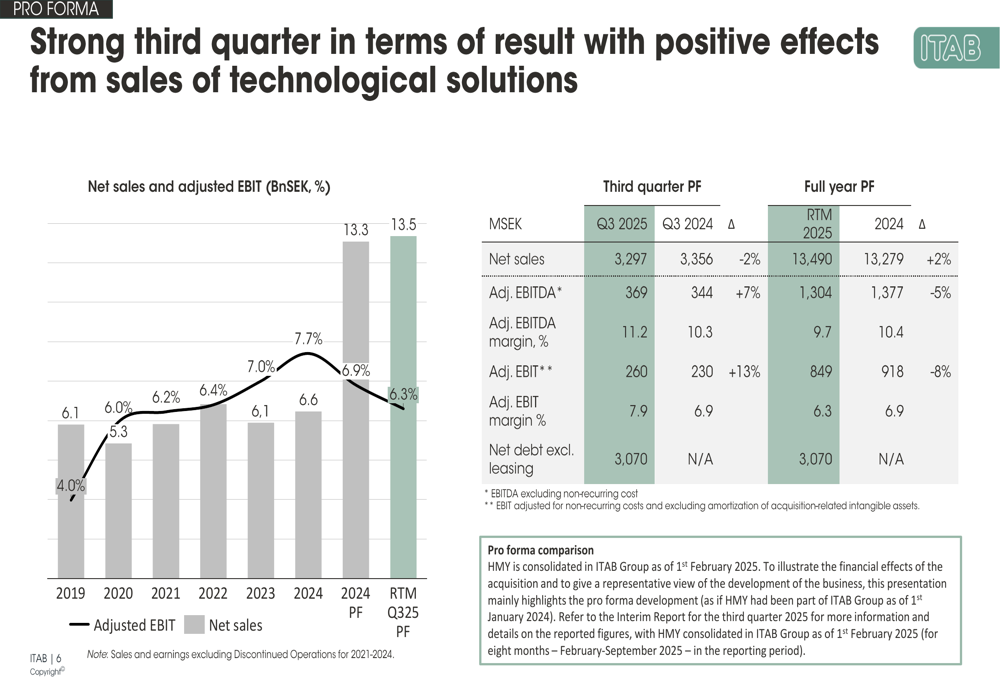

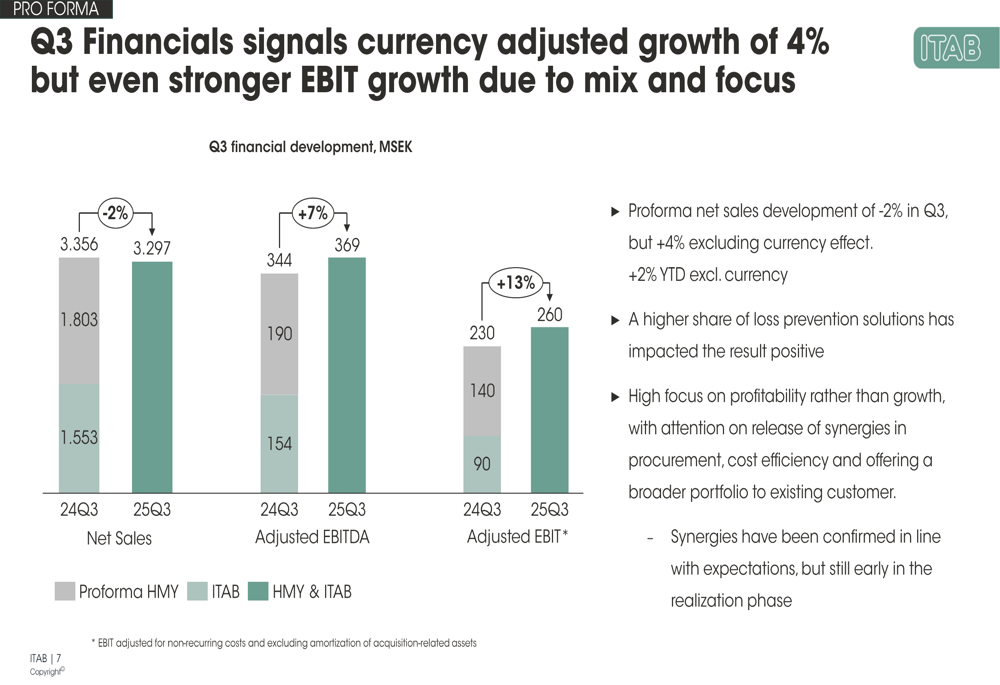

ITAB reported Q3 2025 net sales of 3,297 MSEK, representing a 2% decline in reported terms but a 4% increase when adjusted for currency effects. More impressively, adjusted EBIT rose to 260 MSEK, marking a 13% increase compared to Q3 2024, with the adjusted EBIT margin expanding to 7.9%.

The company attributes this profit growth to a favorable sales mix and increased focus on technological solutions, which carry higher margins than traditional retail fixtures.

As shown in the following financial overview:

Year-to-date performance shows net sales of 9,847 MSEK and adjusted EBIT of 648 MSEK. On a rolling twelve-month basis, the company has achieved net sales of 13,490 MSEK, representing a 2% increase over full-year 2024, though adjusted EBIT has declined 8% to 849 MSEK on the same basis.

The detailed quarterly comparison reveals the strength of the company’s profit improvement despite revenue challenges:

However, cash flow performance has weakened, with Q3 operating cash flow at -9 MSEK compared to 160 MSEK in the same period last year. The company’s rolling 12-month cash conversion has declined to 29%, well below its 80% target, primarily due to working capital challenges, particularly in accounts receivable.

Segment Performance Analysis

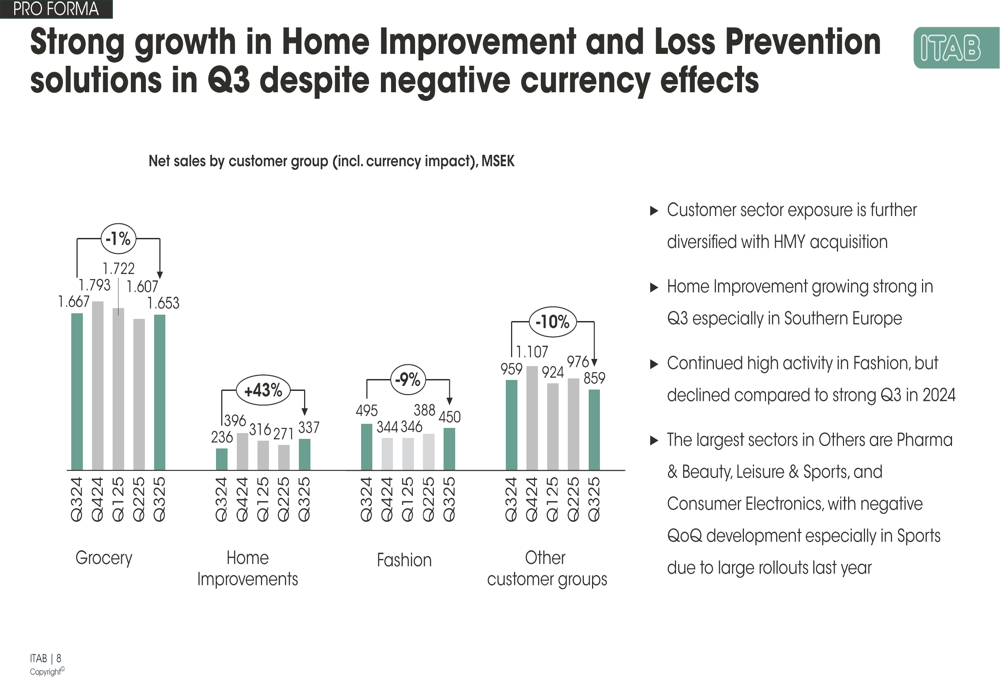

ITAB’s performance varied significantly across customer segments and geographical regions. The Home Improvement sector was the standout performer with 43% growth compared to Q3 2024, while Fashion declined 9% and Other Customer Groups fell 10%. The Grocery segment, which represents 51% of total sales, showed a modest 1% decline.

The following chart illustrates these segment trends:

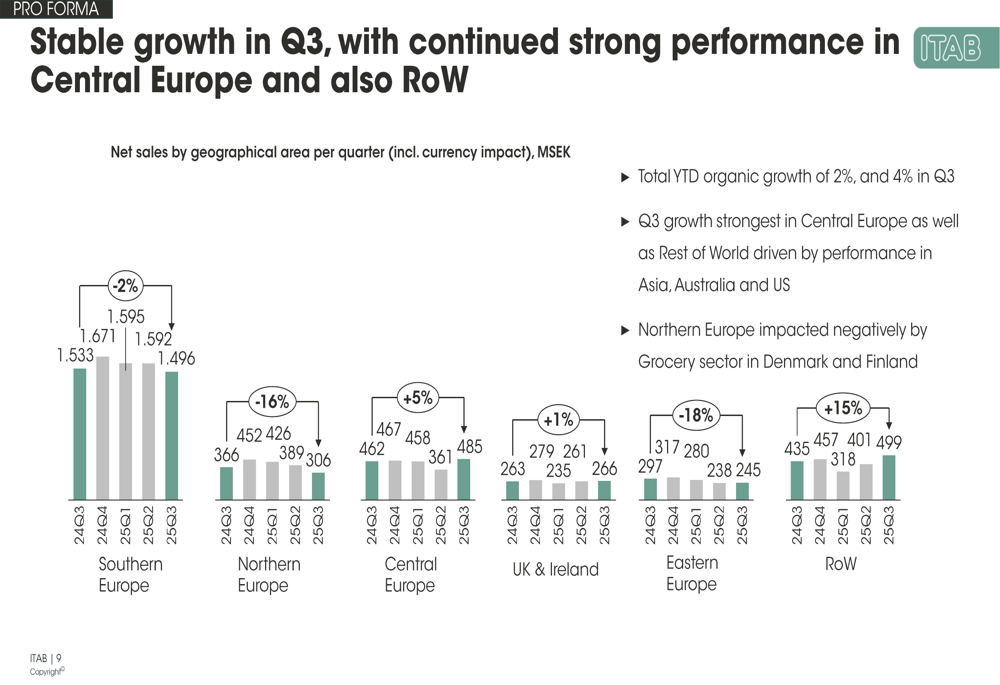

Geographically, Central Europe (+5%) and Rest of World (+15%) delivered strong growth, while Northern Europe (-16%) and Eastern Europe (-18%) experienced significant declines. The company noted that Northern Europe was particularly impacted by weakness in the Grocery sector in Denmark and Finland.

The geographic breakdown highlights these regional variations:

Strategic Initiatives & Acquisition Integration

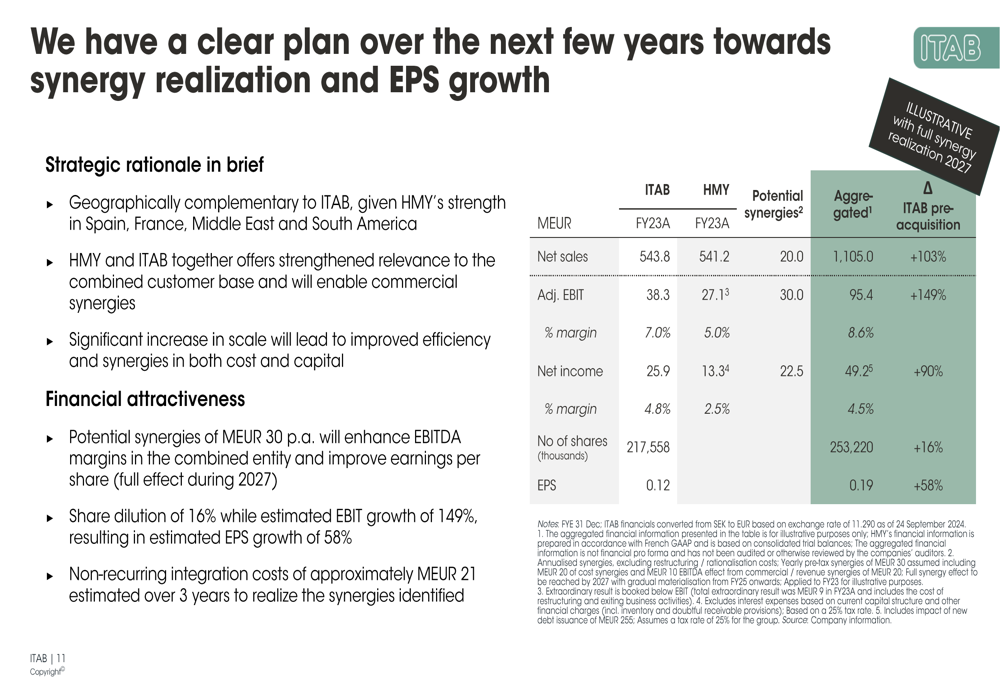

ITAB’s acquisition of HMY represents a cornerstone of its expansion strategy. The company has outlined a clear plan for synergy realization, targeting 30 million euros in annual synergies with full effect expected by late 2027. This integration is projected to significantly enhance EBITDA margins and earnings per share.

The financial impact of the acquisition and expected synergies are detailed below:

The company’s strategic evolution has progressed through several phases, with ITAB now entering the "Expand" phase after successfully completing the "Stabilise" and "Build & Invest" phases. This current phase focuses on sustainable profitable growth by leveraging strengths, increasing cross-selling, and extending technology and services offerings.

ITAB’s value proposition centers on helping retailers address changing consumer expectations through outcome-based solutions. The company positions itself as a partner that helps retailers deliver measurable results by understanding evolving consumer needs and coupling this understanding with retail challenges and investment priorities.

Forward-Looking Statements

Looking ahead, ITAB remains focused on realizing synergies from the HMY acquisition while continuing to transform its business model toward more integrated retail solutions. The company expects working capital seasonality to normalize in Q4 and is working on improving tax efficiency.

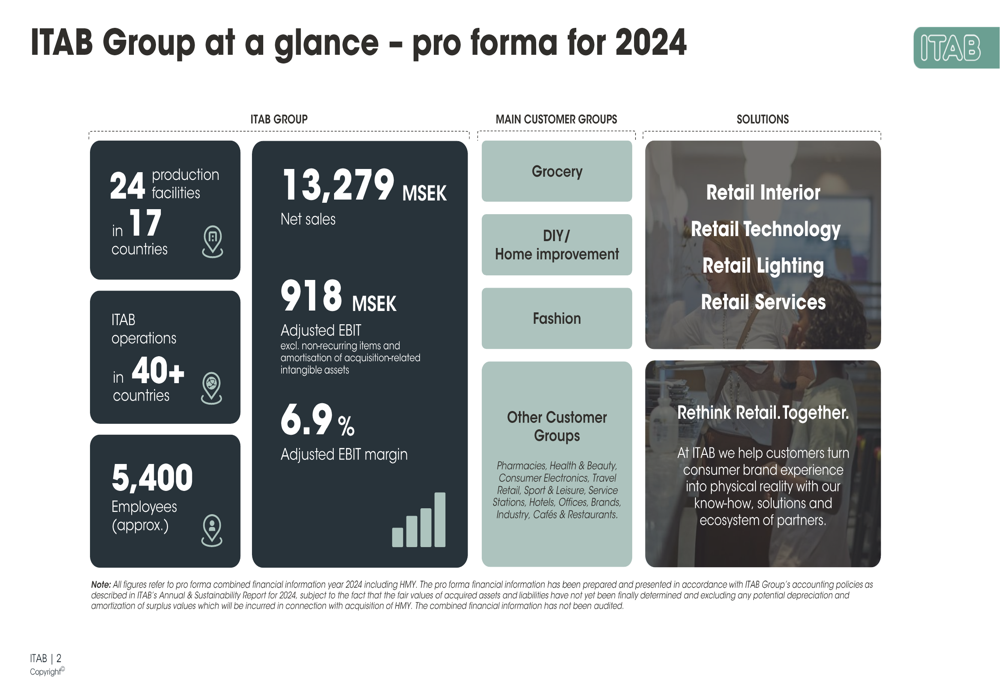

The company’s pro forma overview provides a comprehensive picture of its scale and ambitions following the HMY acquisition:

ITAB’s strategic focus on "Rethink Retail, Together" reflects its commitment to helping retailers navigate changing consumer expectations while improving operational efficiency. The company is particularly focused on expanding its technological solutions, which have been a key driver of margin improvement in recent quarters.

While challenges remain, including integration costs of approximately 21 million euros related to the HMY acquisition and ongoing restructuring efforts in France and Turkey, ITAB’s strong Q3 profit performance and clear strategic direction have resonated positively with investors, as evidenced by the significant stock price increase following the earnings announcement.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.