These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

Ithaca Energy PLC (LSE:LON:ITH) presented its Q1 2025 results on May 21, highlighting record quarterly production and financial performance that enabled the company to upgrade its full-year guidance. The North Sea-focused oil and gas producer has been actively pursuing strategic acquisitions to strengthen its position in the UK Continental Shelf (UKCS) while improving operational efficiency.

The presentation comes as Ithaca’s stock closed at 128.8 on May 20, down 3.45% but trading well above its 52-week low of 93.73, reflecting investor interest in the company’s growth strategy despite recent market volatility.

Quarterly Performance Highlights

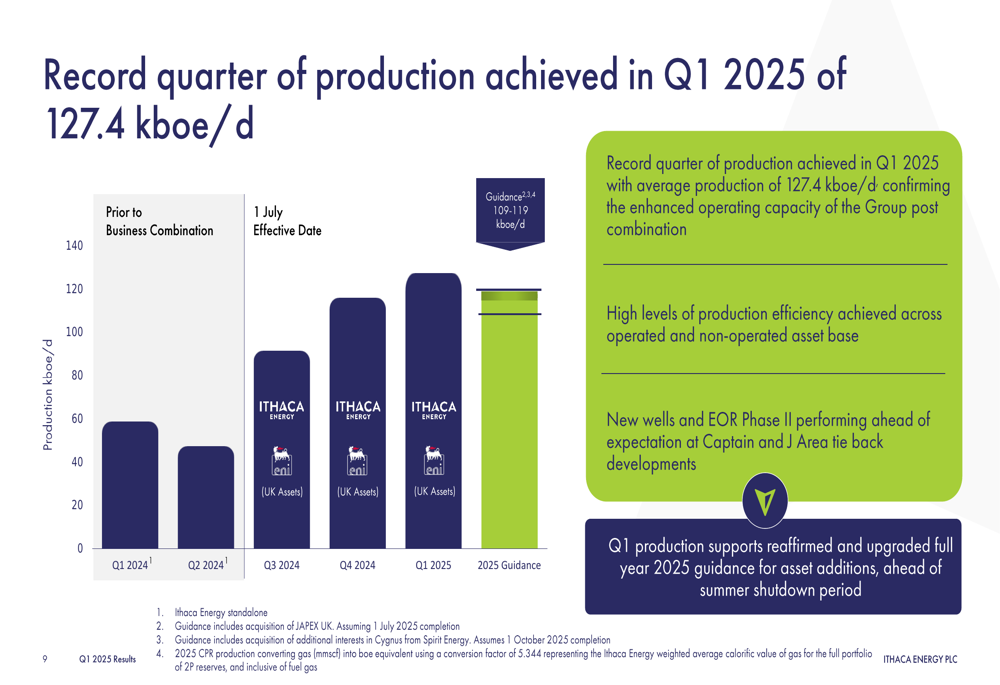

Ithaca achieved record quarterly production of 127.4 kboe/d in Q1 2025, significantly exceeding previous quarters and positioning the company to upgrade its full-year production guidance. The production mix was 59% liquids and 41% gas, providing balanced exposure to both commodity markets.

As shown in the following chart of quarterly production performance:

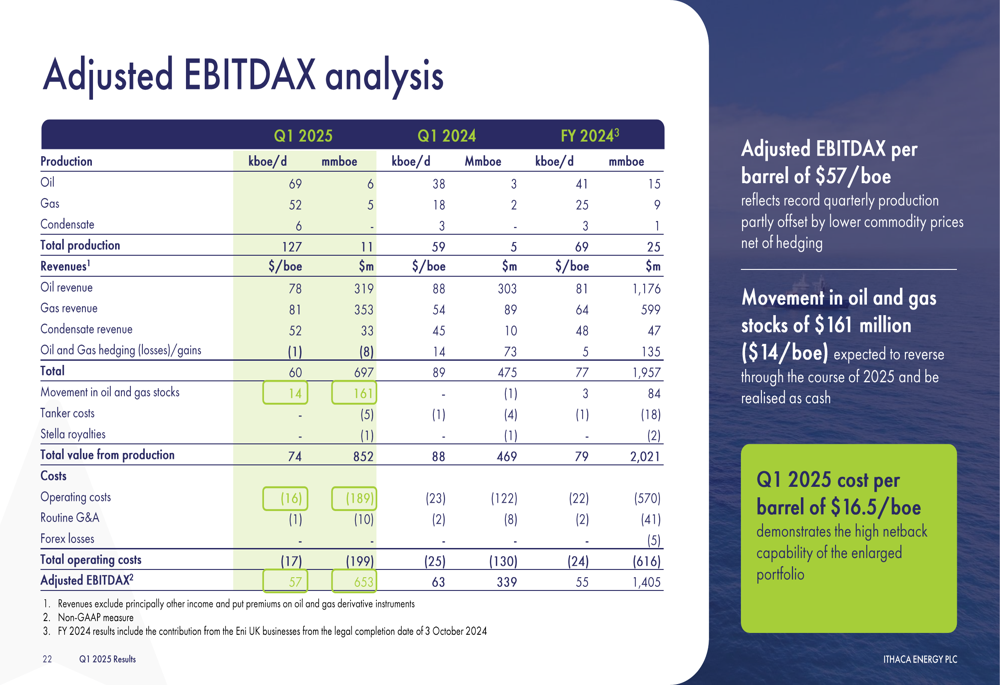

This record production contributed to exceptional financial results, with adjusted EBITDAX reaching $653.2 million for the quarter. Net operating cash flow before working capital movements stood at $625.2 million, while net cash flow from operations was $435.3 million.

The company’s detailed financial breakdown reveals the drivers behind this performance:

Despite these strong operational results, Ithaca reported a net loss of $258.7 million for the period. However, management emphasized that the underlying financial performance remains robust, with available liquidity of $1.1 billion and a pro forma leverage ratio of just 0.38x.

Strategic Acquisitions and Growth Initiatives

Ithaca has been actively pursuing its consolidation strategy in the UKCS market, announcing two significant acquisitions during the quarter that will further increase its production base and reserves.

The company is acquiring Japex UK E&P Limited, which will increase its stake in the high-quality Seagull field from 35% to 50%. This acquisition is expected to add approximately 4-4.5 kboe/d of pro forma net production, with the asset remaining cash generative through the mid-2030s.

As illustrated in the following slide detailing the acquisition strategy:

More significantly, Ithaca is increasing its stake in the Cygnus gas field, the largest producing gas field in the UKCS, by acquiring a 46.25% stake from Spirit Energy. This will raise Ithaca’s operated working interest from 38.75% to 85% and add approximately 12.5-13.5 kboe/d of pro forma net production in 2025.

The company highlighted the attractive investment metrics of this acquisition:

Beyond acquisitions, Ithaca continues to invest in its existing asset base. At the Captain field, the 13th infill well campaign is ongoing with a net production capacity of 2.5 kboe/d. At Cygnus, an infill well campaign has commenced with three wells approved, with the first well due to spud in Q2 2025.

Operational Efficiency and Cost Management

A key focus for Ithaca has been improving operational efficiency and reducing costs. The company’s "Perfect Day" initiative, which drives continuous focus on safety and production targets, has yielded impressive results. In Q1, more than 75% of all days achieved "perfect day" status, with seven out of ten operated assets achieving a "perfect quarter."

The initiative’s definition and results are detailed in the following slide:

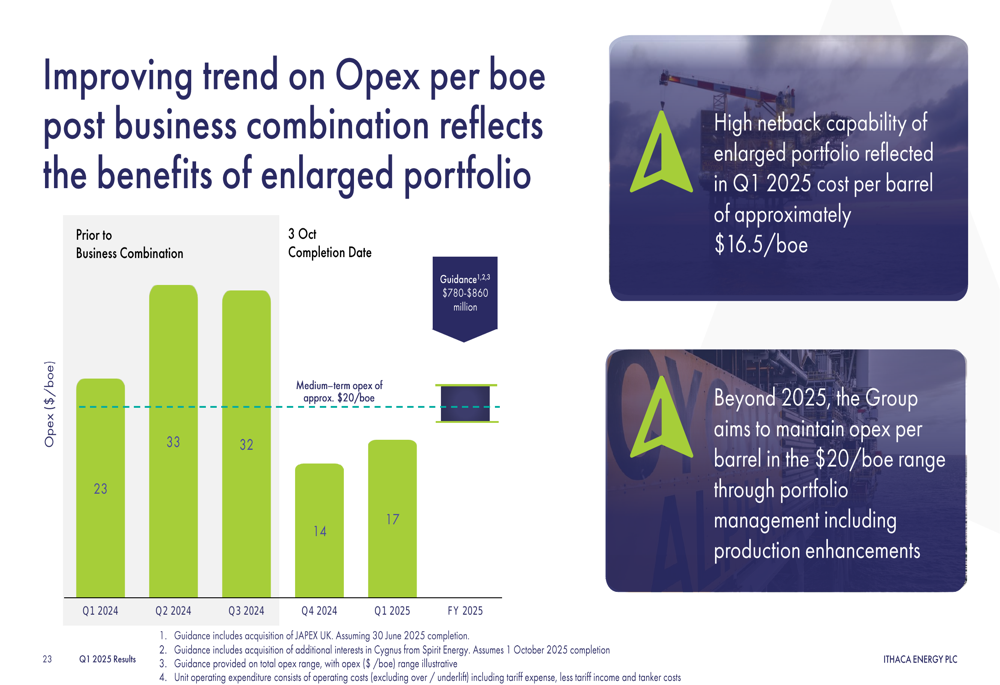

This operational focus has translated into significant cost improvements. Operating expenses per barrel fell to $16.5/boe in Q1 2025, continuing a downward trend since the business combination completed in October 2024.

The following chart illustrates this improving cost trend:

Production efficiency has consistently exceeded the UKCS basin average, with the Cygnus field achieving an impressive 97% efficiency rate. This operational excellence has been achieved while maintaining strong safety performance, with zero Tier 1 and 2 process safety incidents and zero serious injuries during the quarter.

Financial Position and Outlook

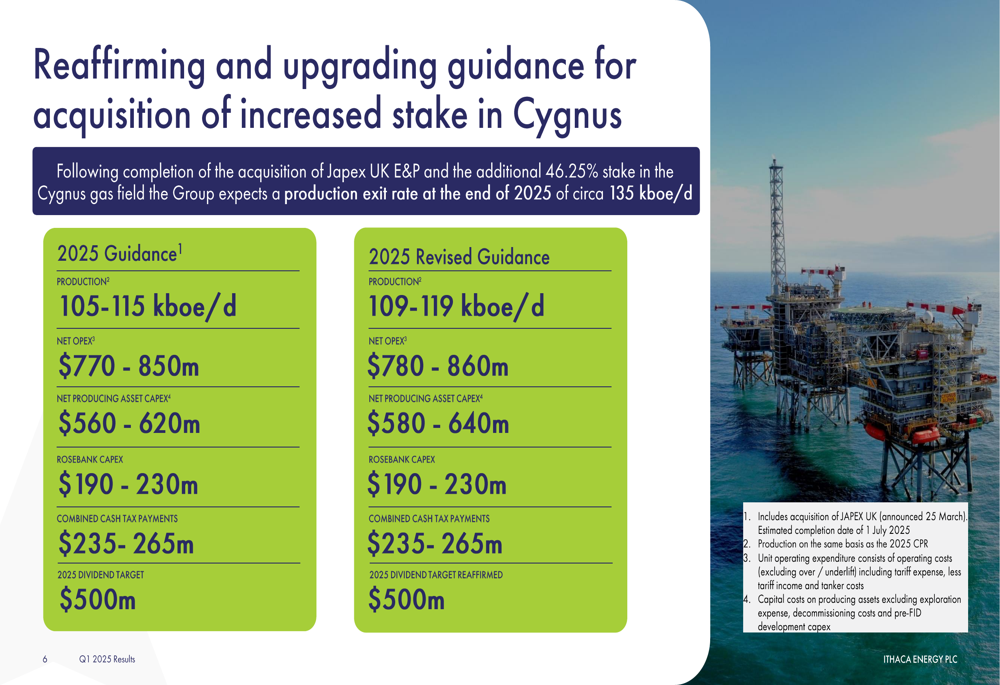

Based on Q1 performance, Ithaca has upgraded its 2025 guidance. Production expectations have been raised from 105-115 kboe/d to 109-119 kboe/d, with a projected exit rate of approximately 135 kboe/d by the end of 2025.

The revised guidance details are presented in the following slide:

The company maintains a strong financial framework underpinned by robust cash flows and a low leverage ratio. Adjusted net debt decreased to $792 million during the quarter, supporting the strong liquidity position of over $1.1 billion.

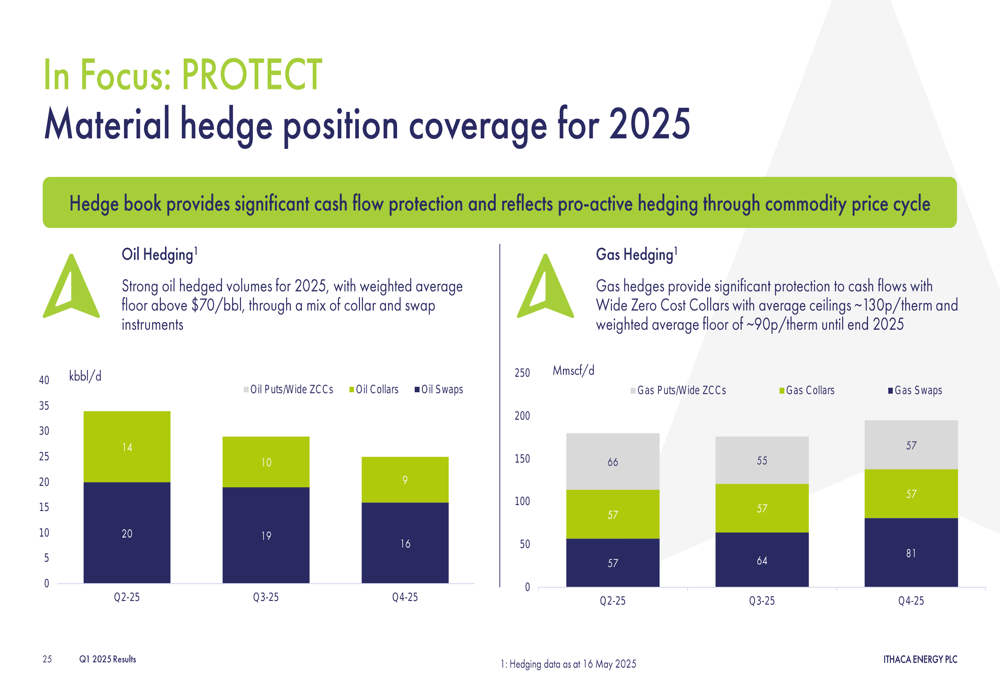

Ithaca has also implemented a comprehensive hedging strategy to protect revenue while maintaining upside exposure. For 2025, the company has secured strong oil hedged volumes with a weighted average floor above $70/bbl, providing significant cash flow protection through commodity price cycles.

The hedging position is detailed in the following slide:

The company reaffirmed its 2025 dividend target of $500 million, highlighting its commitment to returning value to shareholders while pursuing growth opportunities. Management expressed confidence that the combination of operational excellence, strategic acquisitions, and disciplined capital allocation will continue to drive long-term value creation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.