BofA warns Fed risks policy mistake with early rate cuts

Introduction & Market Context

ITT Inc. (NYSE:ITT) presented its first quarter 2025 earnings results on May 1, showcasing a quarter marked by record orders despite flat revenue growth. The industrial manufacturer, which closed at $137.02 on April 30 and traded up 0.73% in premarket activity, reported mixed results that nonetheless demonstrated resilience in challenging market conditions.

The company’s presentation highlighted a record quarterly order intake exceeding $1 billion, resulting in a book-to-bill ratio of 1.15 and a backlog of $1.8 billion—representing 21% year-over-year growth and 10% sequential improvement. This continues the momentum seen in previous quarters, building upon the strong backlog of $1.7 billion reported in Q3 2024.

Quarterly Performance Highlights

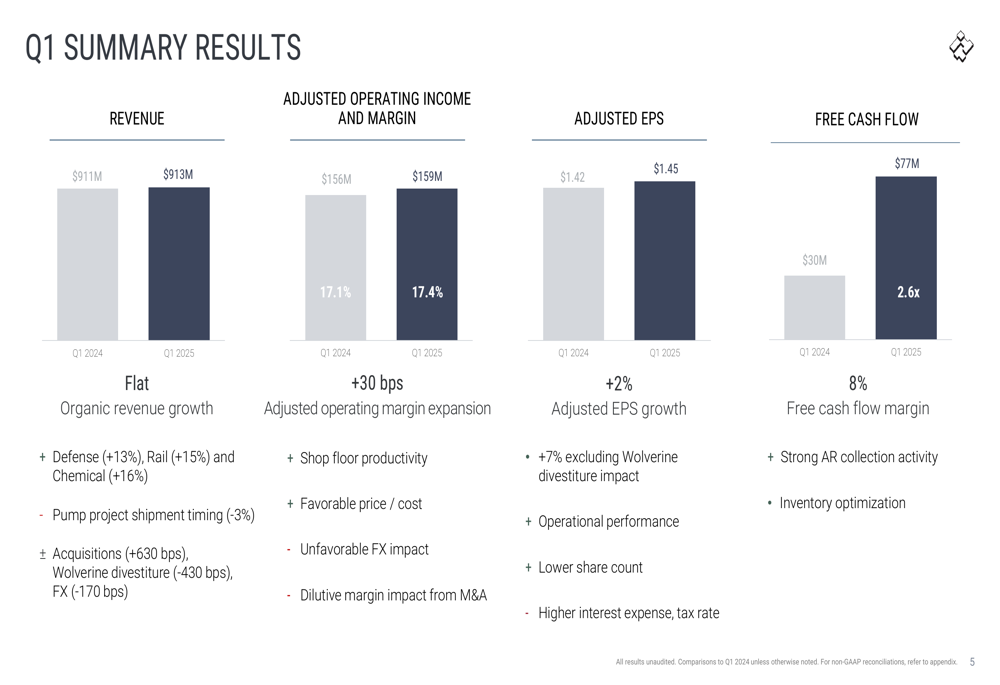

ITT reported Q1 2025 revenue of $913 million, essentially flat compared to $911 million in the same period last year. While organic revenue growth was impacted by pump project shipment timing (-3%), the company saw strong performance in several key areas, including Defense (+13%), Rail (+15%), and Chemical (+16%).

As shown in the following summary of quarterly results:

Adjusted operating income reached $159 million with a margin of 17.4%, representing a 30 basis point improvement over Q1 2024’s 17.1%. This margin expansion occurred despite significant headwinds from foreign exchange and acquisition-related costs.

Adjusted earnings per share increased 2% to $1.45, compared to $1.42 in Q1 2024. Excluding the impact of the Wolverine divestiture, adjusted EPS growth was 7%. Free cash flow showed remarkable improvement, jumping 154% to $77 million from $30 million in the prior year period, reflecting strong accounts receivable collection and inventory optimization.

Detailed Financial Analysis

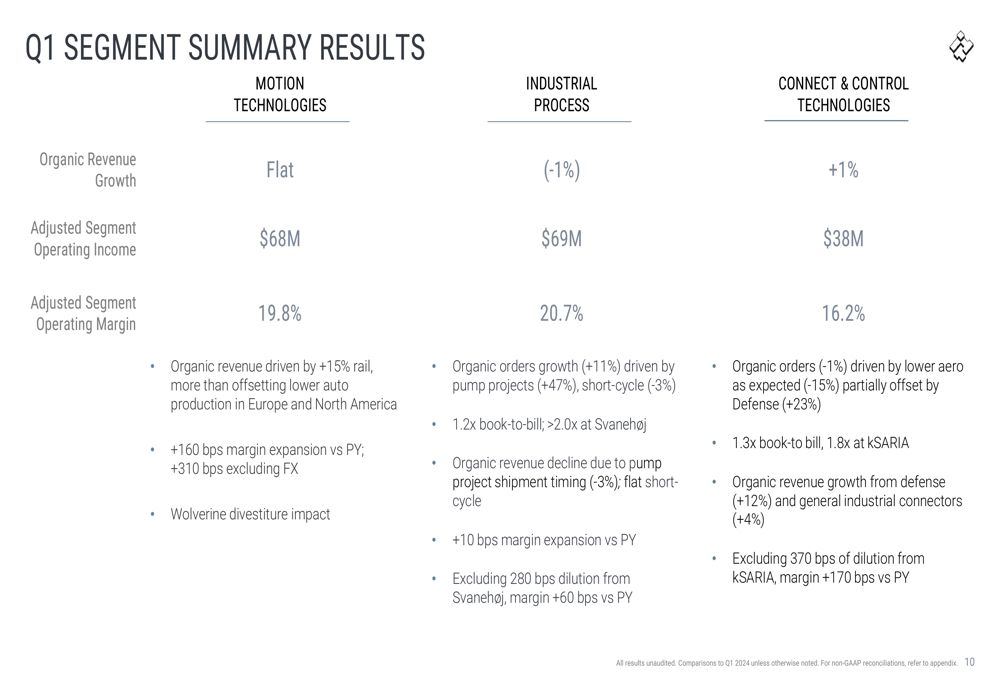

The company’s performance varied across its three business segments. Motion Technologies reported flat organic revenue growth but achieved a 19.8% adjusted segment operating margin, representing a 160 basis point improvement. Industrial Process saw a 1% decline in organic revenue but posted strong order growth of 11% organically (14% total), driven by pump projects. Connect & Control Technologies delivered 1% organic revenue growth with a 16.2% adjusted operating margin.

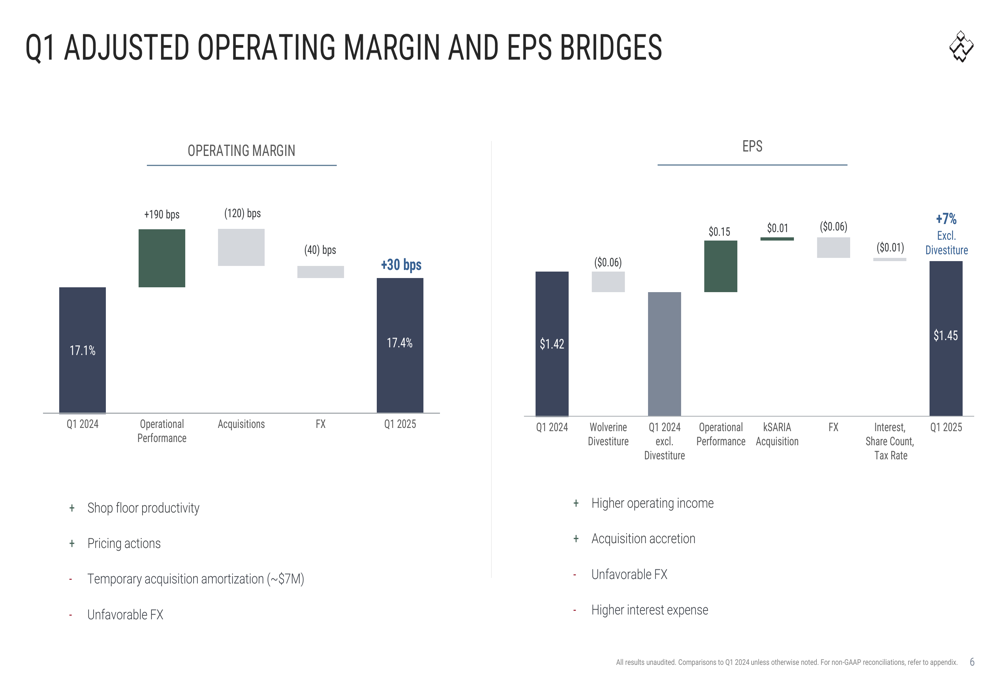

The following bridge chart illustrates the factors contributing to ITT’s adjusted operating margin and EPS performance:

Operational performance contributed 190 basis points to margin expansion, which was partially offset by a 120 basis point dilution from acquisitions and a 40 basis point negative impact from foreign exchange. Similarly, EPS growth was driven by operational performance (+$0.15) but tempered by the Wolverine divestiture (-$0.06) and foreign exchange headwinds (-$0.06).

Strategic Initiatives

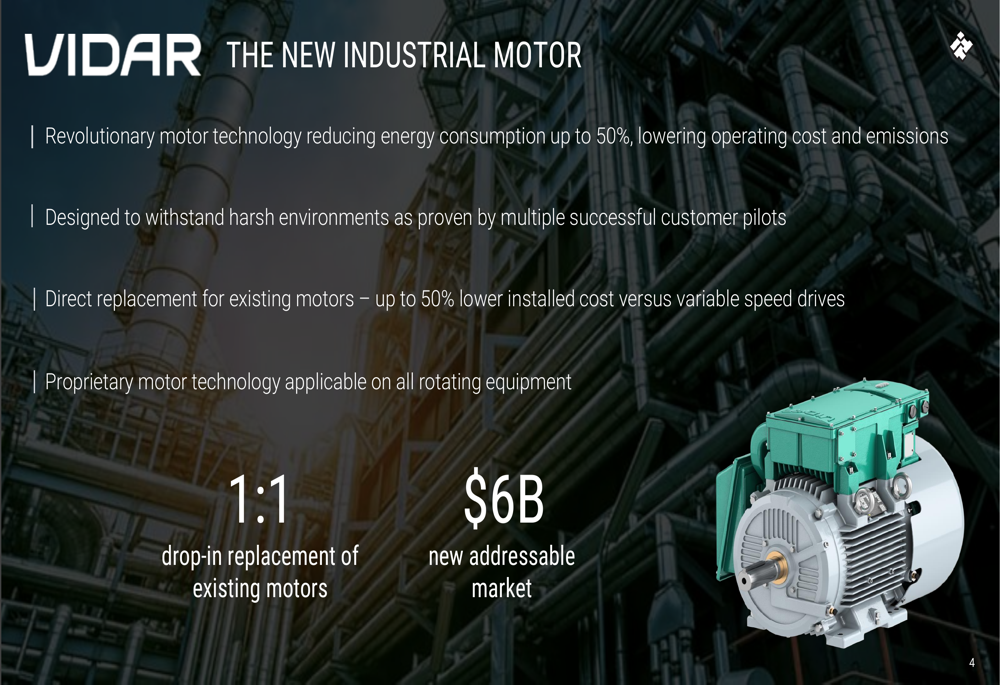

A significant highlight of the presentation was the introduction of VIDAR, ITT’s new industrial motor technology. This innovation represents a major strategic initiative for the company, opening access to a $6 billion new addressable market.

The VIDAR motor offers revolutionary technology that reduces energy consumption by up to 50% while being designed for harsh environments. As a direct replacement for existing motors with up to 50% lower installed cost, the proprietary technology has applications across all rotating equipment.

In addition to product innovation, ITT has been actively deploying capital, with approximately $400 million in share repurchases through April 2025, reducing share count by 4%. The company emphasized that mergers and acquisitions remain a strategic priority, suggesting potential future deals to complement organic growth.

Forward-Looking Statements

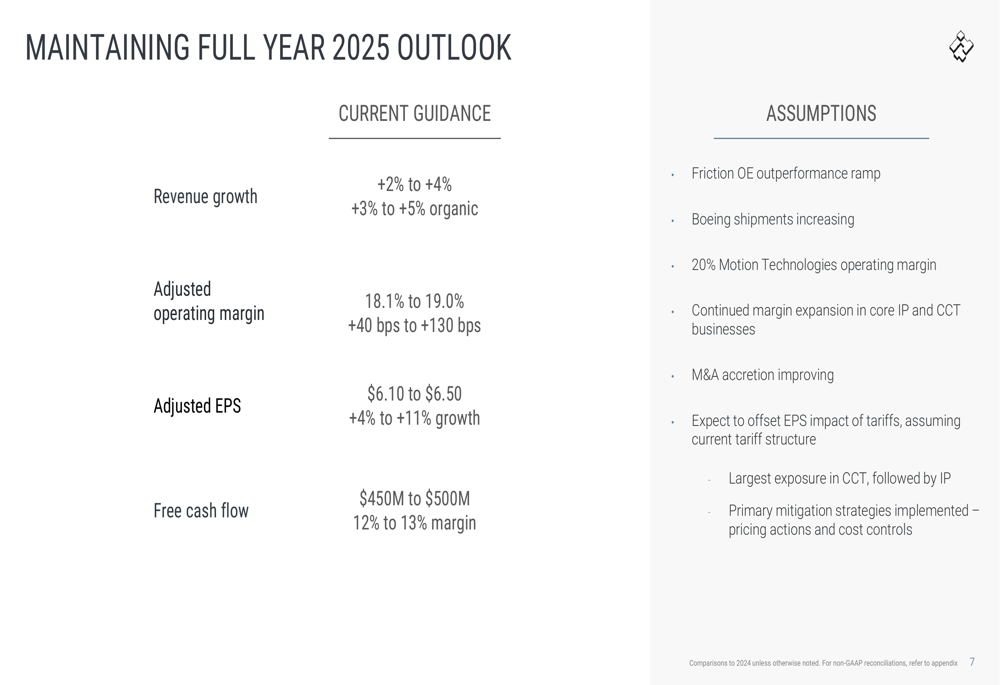

Despite mixed Q1 results, ITT maintained its full-year 2025 guidance, expressing confidence in a stronger second quarter. The outlook includes:

The company expects revenue growth of 2% to 4% (3% to 5% organic), adjusted operating margin of 18.1% to 19.0% (representing 40 to 130 basis point improvement), and adjusted EPS of $6.10 to $6.50 (4% to 11% growth). Free cash flow is projected to reach $450 million to $500 million, representing a 12% to 13% margin.

Key assumptions underlying this guidance include Friction OE outperformance ramp, increasing Boeing (NYSE:BA) shipments, achieving 20% operating margin in Motion Technologies, continued margin expansion, and improved M&A accretion while managing current tariff structures.

ITT also announced an upcoming Capital Markets Day on May 15, 2025, where management will likely provide more details on long-term strategic initiatives and financial targets.

Segment Performance

A closer look at ITT’s segment performance reveals varying dynamics across the business:

Motion Technologies benefited from 15% growth in rail, which offset lower automotive production. Industrial Process saw strong order growth of 11% driven by pump projects, despite a slight revenue decline. Connect & Control Technologies achieved modest organic growth with a solid adjusted operating margin of 16.2%.

The company’s ability to maintain or expand margins across segments despite revenue challenges demonstrates effective cost management and pricing strategies, positioning ITT well for the anticipated stronger performance in Q2 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.