Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Illinois Tool Works (NYSE:ITW) reported mixed first-quarter 2025 results, with revenue declining but margins improving, as the industrial manufacturer continues to navigate a challenging economic environment. The company maintained its full-year guidance, emphasizing its operational resilience and strategic positioning.

Quarterly Performance Highlights

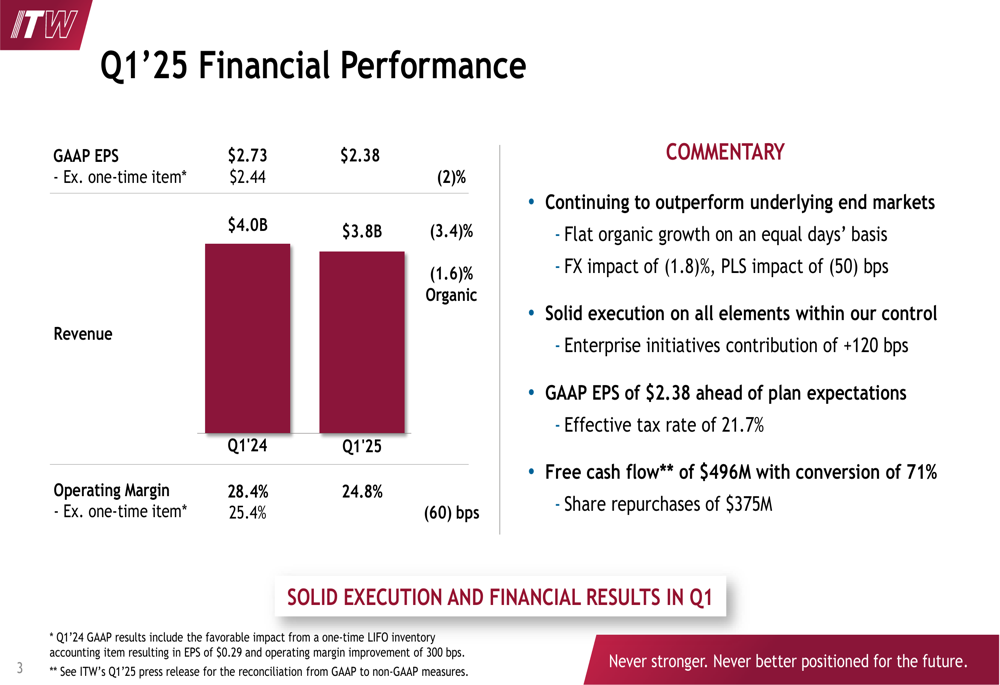

ITW reported first-quarter GAAP earnings per share of $2.73, which includes a one-time item. Excluding this item, EPS was $2.44, representing a 2.5% increase from $2.38 in the same period last year. Revenue came in at $4.0 billion, down 3.4% compared to Q1 2024, with organic revenue declining 1.6%.

Despite the revenue challenges, the company improved its operating margin to 28.4% (or 25.4% excluding a one-time item), up from 24.8% in the prior-year quarter. Enterprise initiatives contributed 120 basis points to the margin improvement.

As shown in the following financial performance summary:

The company generated $496 million in free cash flow with a conversion rate of 71% and spent $375 million on share repurchases during the quarter. Foreign exchange had a negative 1.8% impact on revenue, while product line simplification (PLS) initiatives reduced revenue by 50 basis points.

Segment Performance Analysis

ITW’s seven operating segments showed mixed results, with most experiencing slight revenue declines but several achieving margin improvements.

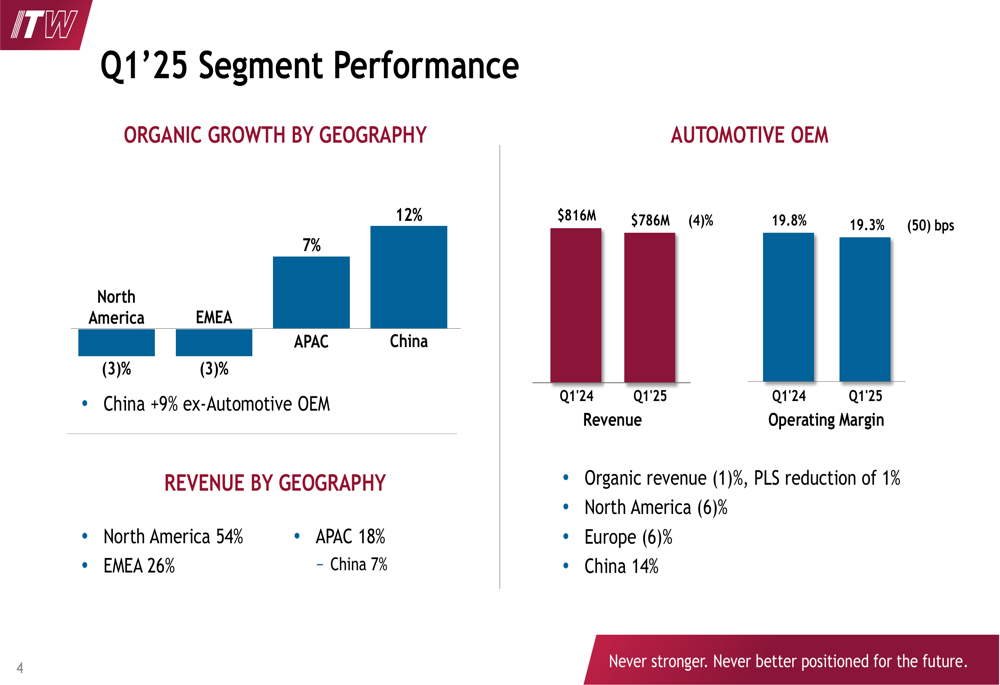

The Automotive OEM segment, which represents a significant portion of ITW’s business, reported revenue of $786 million, down 4% from the previous year. Operating margin decreased by 50 basis points to 19.3%. While North America and Europe both declined by 6%, China showed strong growth of 14%.

The segment’s performance is illustrated in the following chart:

Food Equipment showed resilience with revenue of $627 million, down just 1% year-over-year, while operating margin improved by 50 basis points to 26.5%. The segment saw organic growth of 1%, with service revenue up 3% and North American operations growing by 1%.

Test & Measurement/Electronics faced more significant challenges, with revenue declining 6% to $652 million and operating margin decreasing by 200 basis points to 21.4%. The Test & Measurement subsegment saw a 9% organic decline, while Electronics grew by 3%.

Welding and Polymers & Fluids segments both experienced modest 1% revenue declines but showed divergent margin performance. Welding’s operating margin decreased slightly to 32.5%, while Polymers & Fluids improved by 70 basis points to 26.5%.

Construction Products continued to face headwinds, with revenue dropping 9% to $443 million and operating margin declining slightly to 29.2%. North American operations were particularly weak, declining 10%.

The Specialty Products segment showed the strongest margin performance, improving by 120 basis points to 30.9% despite a 1% revenue decline to $435 million. This segment achieved 1% organic growth, with North American operations growing by 2%.

2025 Outlook & Guidance

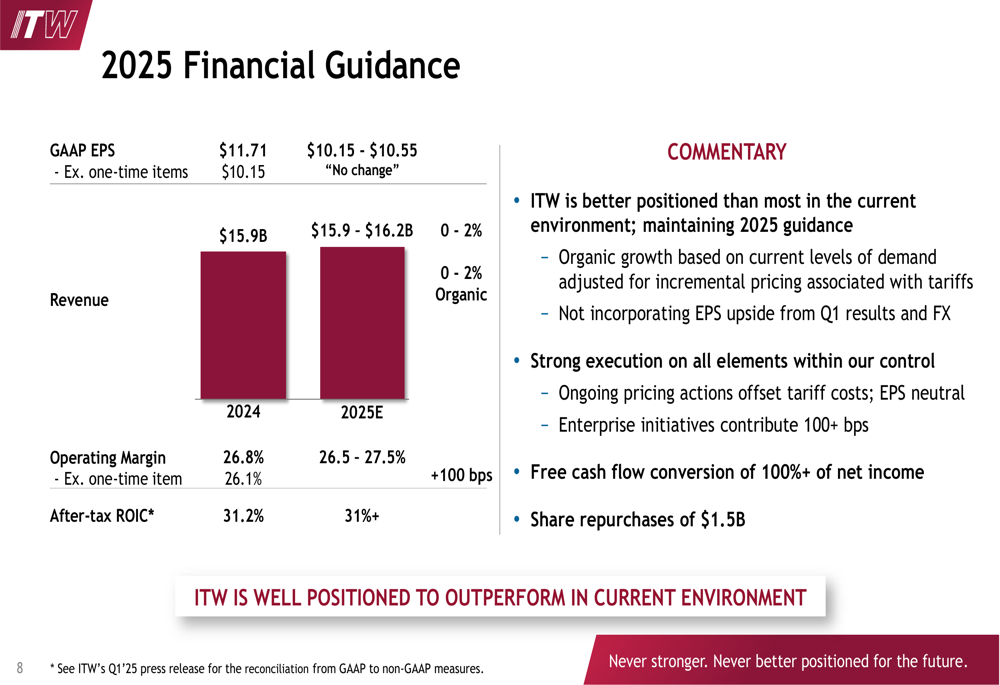

ITW maintained its full-year 2025 guidance, projecting GAAP earnings per share of $10.15-$10.55, compared to $11.71 in 2024 ($10.15 excluding one-time items). Revenue is expected to be $15.9-$16.2 billion, representing 0-2% organic growth.

The company forecasts operating margin improvement of 100 basis points to 26.5-27.5%, with after-tax return on invested capital exceeding 31%. Management plans to continue its share repurchase program, targeting $1.5 billion for the full year.

As shown in the following guidance summary:

The guidance incorporates pricing actions to offset tariff costs, which are expected to be EPS neutral. Enterprise initiatives are projected to contribute more than 100 basis points to margin improvement, and free cash flow conversion is targeted at over 100% of net income.

Strategic Positioning

ITW emphasized its strong positioning in the current economic environment, maintaining that it is "well positioned to outperform" despite market challenges. The company continues to focus on operational excellence and strategic growth initiatives.

Management noted that the guidance does not incorporate EPS upside from Q1 results and foreign exchange impacts, suggesting potential room for improvement if current trends continue. The company’s approach to pricing in response to tariffs reflects its strategic focus on maintaining profitability while navigating external pressures.

ITW’s stock closed at $241.75 on April 29, 2025, and was trading up 0.52% in pre-market activity following the earnings release. The stock remains near its 52-week high of $279.13, indicating continued investor confidence in the company’s strategy and execution.

The company’s tagline "Never stronger. Never better positioned for the future" reflects management’s confidence in ITW’s ability to navigate the current market environment while positioning for long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.