US stock futures inch higher with Q3 earnings on tap

Introduction & Market Context

Ivanhoe Mines Ltd. (TSX:IVN) released its Q2 2025 financial results on July 31, revealing a quarter marked by operational challenges but demonstrating resilience in its recovery efforts. The mining company reported mixed financial performance, with earnings per share of $0.03, missing forecasts of $0.042 by 28.57%, while revenue slightly exceeded expectations at $96.76 million compared to forecasts of $95.33 million.

The quarter was significantly impacted by seismic activity at the Kakula mine, which affected underground pumping infrastructure and temporarily halted operations. Despite these challenges, Ivanhoe maintained its 2025 production guidance and continued to advance its strategic growth initiatives across its portfolio of mining assets.

Quarterly Performance Highlights

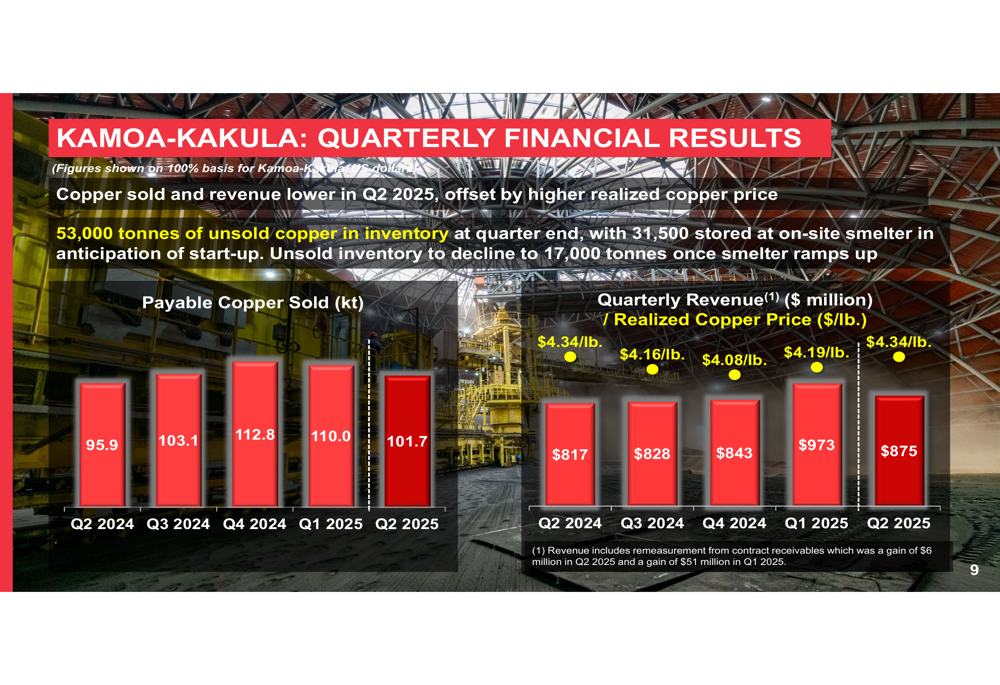

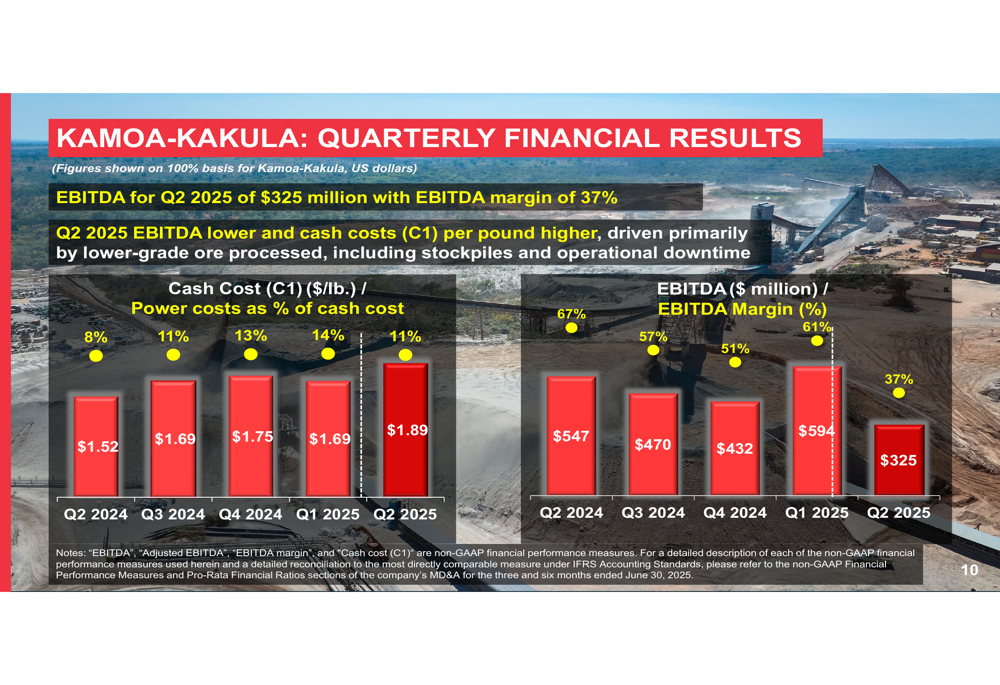

Ivanhoe’s flagship Kamoa-Kakula Copper Complex produced 112,009 tonnes of copper in Q2 2025, down from 133,120 tonnes in the previous quarter. The operation generated revenue of $875 million and EBITDA of $325 million on a 100% project basis, with an EBITDA margin of 37%, significantly lower than the 61% achieved in Q1 2025.

As shown in the following chart of quarterly financial results, copper sales and revenue were lower in Q2 2025 but partially offset by higher realized copper prices:

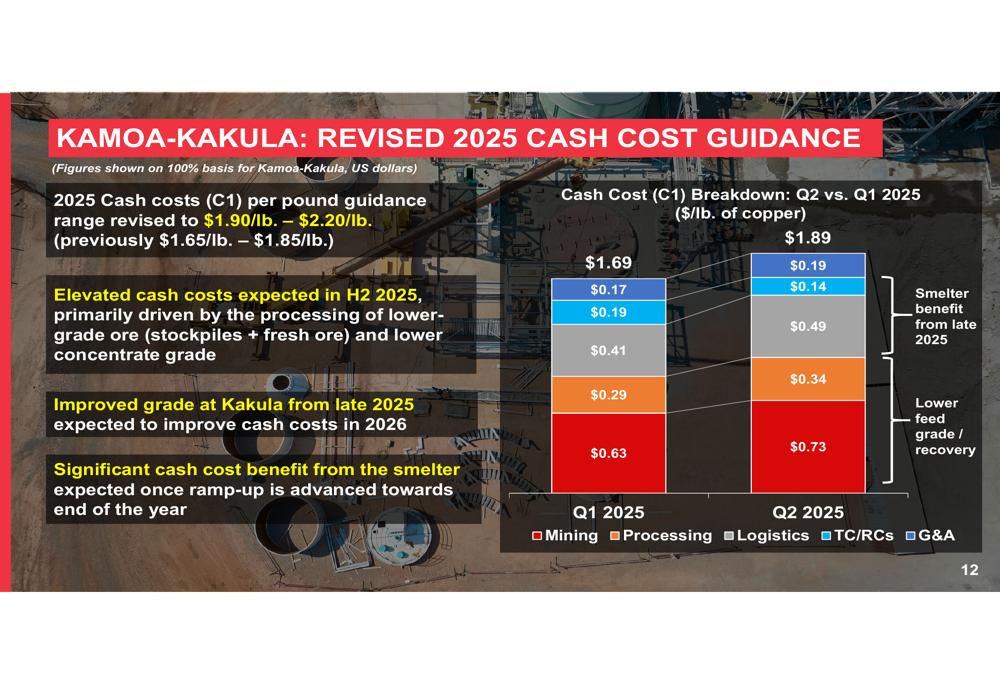

The decline in EBITDA and increase in cash costs were primarily driven by lower-grade ore processed (3.58% compared to 4.10% in Q1), including stockpiles, and operational downtime following the seismic event. C1 cash costs rose to $1.89 per pound from $1.69 in the previous quarter.

The following chart illustrates the quarterly trend in EBITDA and cash costs:

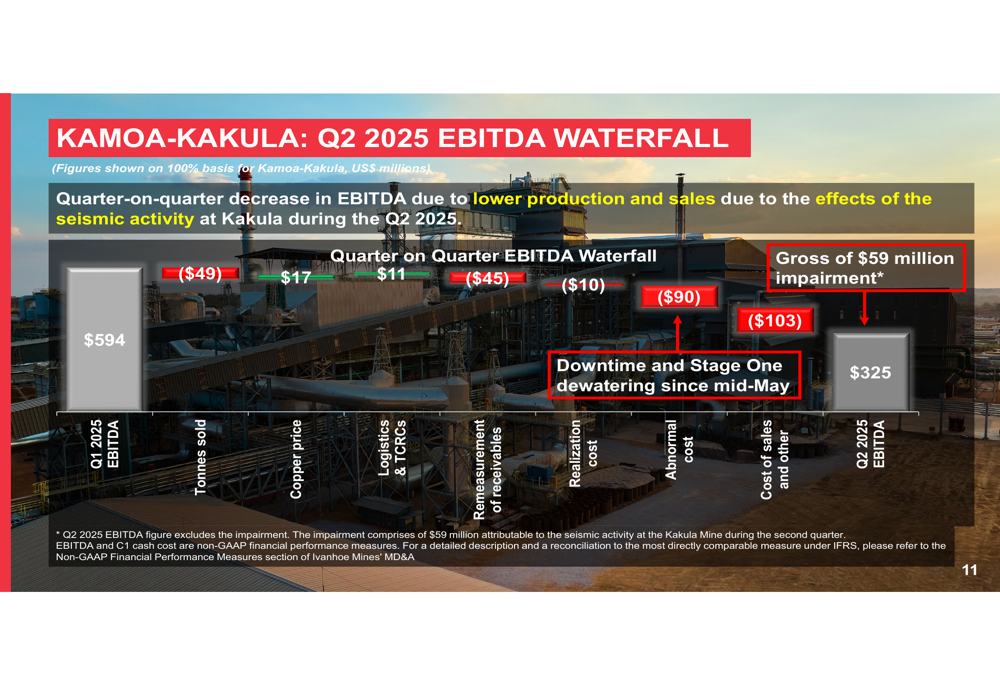

A detailed breakdown of the factors affecting EBITDA reveals the significant impact of the seismic event, with abnormal costs of $90 million and other operational challenges contributing to the quarter-on-quarter decrease:

At the corporate level, Ivanhoe Mines (OTC:IVPAF) reported a net profit of $35 million for Q2 2025, with adjusted EBITDA of $123 million, down from $226 million in Q1 2025. The company maintained a strong balance sheet with $672 million in cash and cash equivalents at the end of the quarter.

Operational Challenges and Recovery Plan

The seismic activity at Kakula in May 2025 caused damage to underground pumping infrastructure, necessitating a comprehensive recovery plan. The company has implemented a phased approach to restore operations, with Stage One dewatering already completed and Stage Two set to begin in August.

The company’s presentation outlined a conservative and safety-focused restart of mining activities at Kakula, with plans to:

1. Restore pumping and stabilize underground water levels

2. Recommence mining in the western side of Kakula, ramping up to 3.6 million tonnes per annum

3. Develop new access drives to new mining areas in the east

4. Fully dewater the Kakula Mine starting in August

5. Complete geotechnical assessment of existing mine workings in the eastern side by Q4 2025

6. Commence mining in new areas in the eastern side of Kakula by Q2 2026

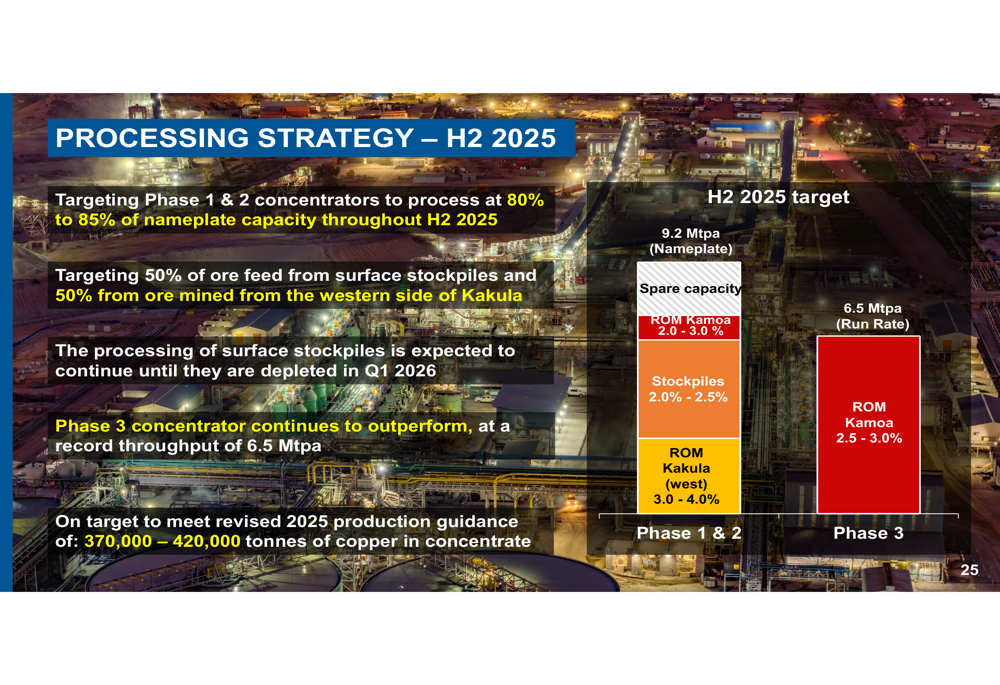

For the second half of 2025, Ivanhoe has developed a processing strategy targeting Phase 1 and 2 concentrators to operate at 80-85% of nameplate capacity, with approximately 50% of ore feed coming from surface stockpiles and 50% from newly mined ore from the western side of Kakula. The Phase 3 concentrator continues to outperform, operating at approximately 30% above design capacity.

As illustrated in the following processing strategy chart for H2 2025:

Strategic Growth Initiatives

Despite operational challenges at Kamoa-Kakula, Ivanhoe continues to advance several strategic growth initiatives across its portfolio:

1. The direct-to-blister smelter at Kamoa-Kakula is expected to commence heat-up in September 2025. As of June 30, 2025, the company had accumulated 31,500 tonnes of unsold copper in concentrate in preparation for the smelter start-up. The smelter is expected to reduce shipping volumes and improve margins through acid credits.

2. The Platreef Project remains on schedule for first production in Q4 2025, representing the first phase of a three-phase expansion plan to make it one of the world’s largest and lowest-cost producers of platinum group metals. The company noted that the metals basket price for the Platreef Project has recovered from cyclical lows to above $1,600 per ounce, with platinum and palladium prices rising by 42% and 26% respectively since Q1 2025.

The following image shows the Platreef Mine’s Phase 1 concentrator facility, which is on track for first ore feed in Q4 2025:

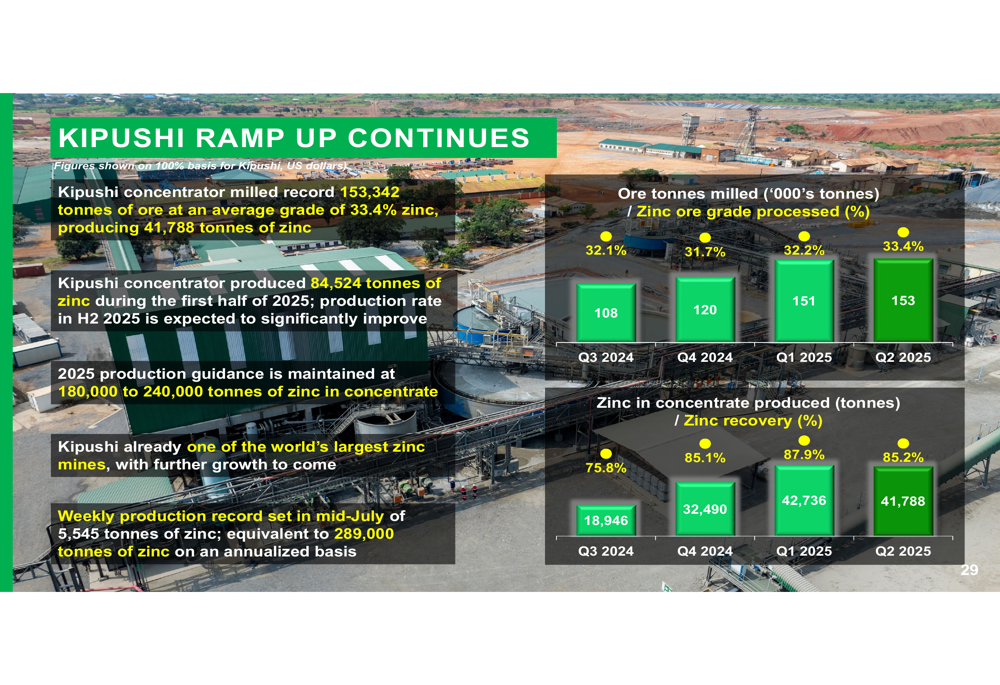

3. The Kipushi zinc operation continues its ramp-up, with the concentrator milling a record 153,342 tonnes of ore at an average grade of 33.4% zinc in Q2 2025, producing 41,788 tonnes of zinc. A debottlenecking program is nearing completion, which will increase processing capacity by 20%.

The following chart shows Kipushi’s production ramp-up progress:

Financial Position and Outlook

Ivanhoe has revised its 2025 cash cost guidance for Kamoa-Kakula to $1.90-$2.20 per pound (previously $1.65-$1.85 per pound), primarily due to the processing of lower-grade ore. The company expects elevated cash costs in the second half of 2025, with improvements anticipated from late 2025 as higher-grade ore becomes available and the smelter begins operations.

The breakdown of cash costs shows increases across multiple categories from Q1 to Q2 2025:

Despite the operational challenges, Ivanhoe maintained its 2025 production guidance of 370,000-420,000 tonnes of copper in concentrate for Kamoa-Kakula and 180,000-240,000 tonnes of zinc in concentrate for Kipushi.

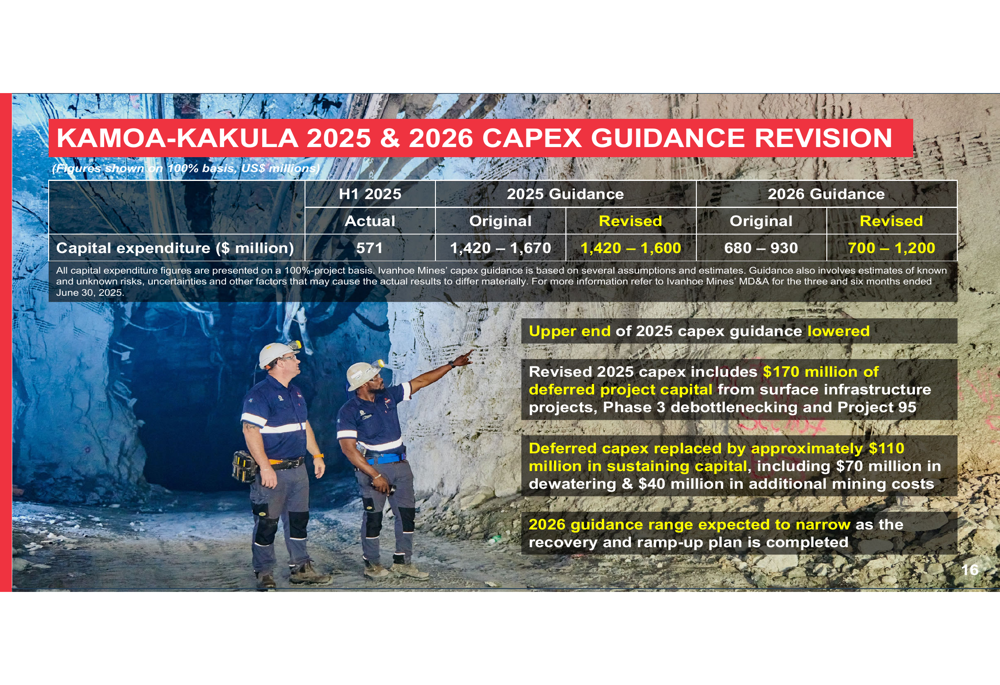

The company has also revised its capital expenditure guidance, as shown in the following table:

Ivanhoe’s pro-rata net debt to adjusted EBITDA ratio increased from 1.49 in Q1 2025 to 1.83 in Q2 2025, still within the company’s target leverage ratio of 1.0x through the cycle.

Looking ahead, Ivanhoe expects to complete an updated recovery and ramp-up plan for Kamoa-Kakula by September 2025, with an updated life-of-mine integrated development plan targeted for Q1 2026. The company remains focused on its phased recovery at Kakula while advancing its strategic growth projects, positioning itself for improved performance as operational challenges are addressed and new production comes online.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.