How are energy investors positioned?

Introduction & Market Context

Iveco Group NV (BIT:IVG) released its Q2 2025 financial results on July 31, 2025, revealing a 3.5% year-over-year decline in consolidated net revenues to €3.78 billion. The company’s shares fell 5.13% following the presentation, as investors reacted to lowered full-year guidance and mixed performance across business segments.

The results come amid challenging market conditions in Europe, with industry volumes down 13% for light commercial vehicles and 15% for medium and heavy trucks compared to Q2 2024. This represents a slight improvement from Q1 2025, when the company reported a steeper 10% year-over-year revenue decline.

Strategic Announcements

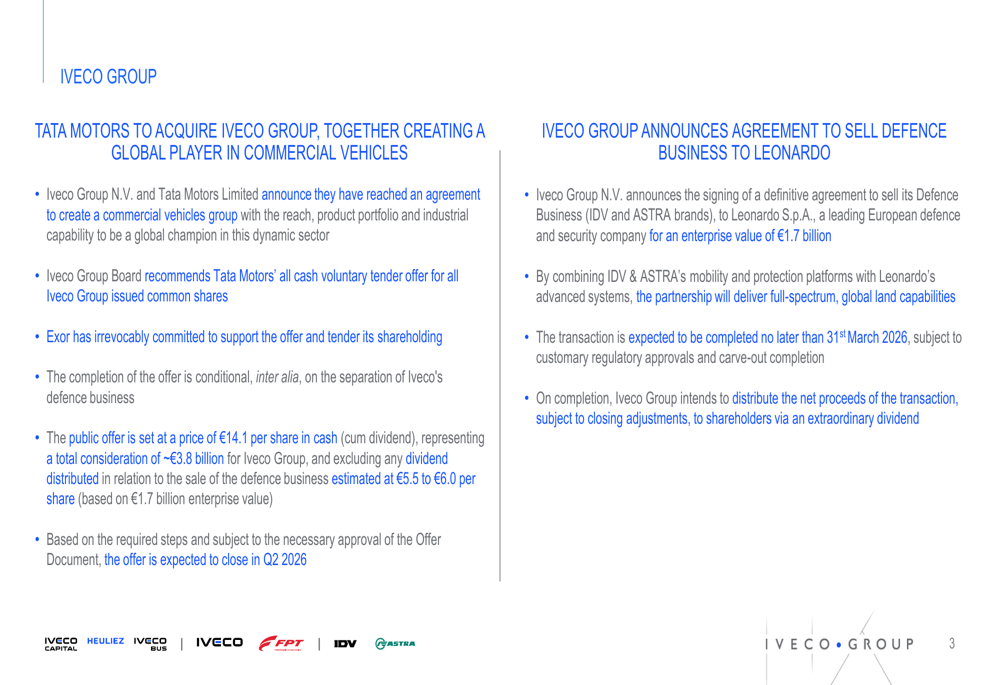

The presentation highlighted two major strategic developments that will reshape Iveco Group’s future. First, Tata Motors (NYSE:TTM) plans to acquire Iveco Group through an all-cash tender offer of €14.1 per share, valuing the company at approximately €3.8 billion. The acquisition aims to create a global commercial vehicle player, with closing expected in Q2 2026.

As shown in the following strategic announcements slide:

Second, Iveco Group has agreed to sell its Defence Business to Leonardo S.p.A. for €1.7 billion. This transaction is expected to complete by March 31, 2026, with proceeds to be distributed to shareholders via an extraordinary dividend.

Quarterly Performance Highlights

Despite market headwinds, Iveco Group reported an adjusted EBIT of €215 million with a 5.7% margin. Industrial Activities generated an adjusted EBIT of €187 million (5.1% margin) and a positive free cash flow of €145 million. Adjusted diluted EPS stood at €0.39.

The company’s key financial metrics for Q2 2025 are summarized in the following slide:

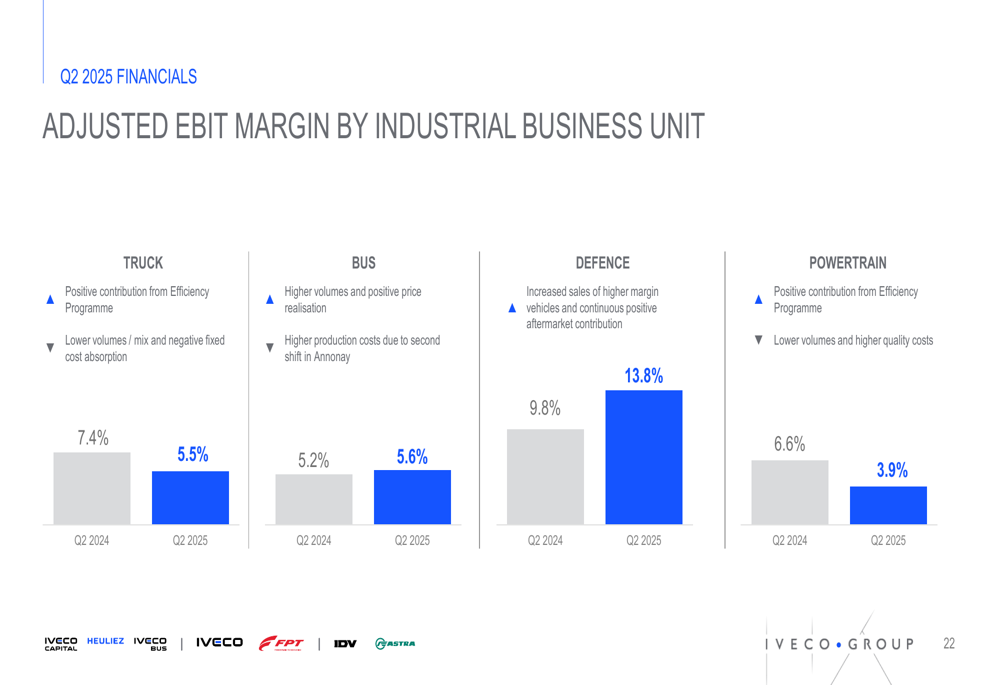

Performance varied significantly across business units. The Defence division was the standout performer with its adjusted EBIT margin increasing from 9.8% to 13.8%, supported by a solid order book of €5 billion. The Bus division also improved its margin from 5.2% to 5.6%, maintaining its #2 position in Europe with a 19.7% market share.

Conversely, the Truck division saw its margin decrease from 7.4% to 5.5%, while Powertrain’s margin fell from 6.6% to 3.9%, impacted by lower volumes and higher quality costs.

The following chart illustrates the adjusted EBIT margin by business unit:

Detailed Financial Analysis

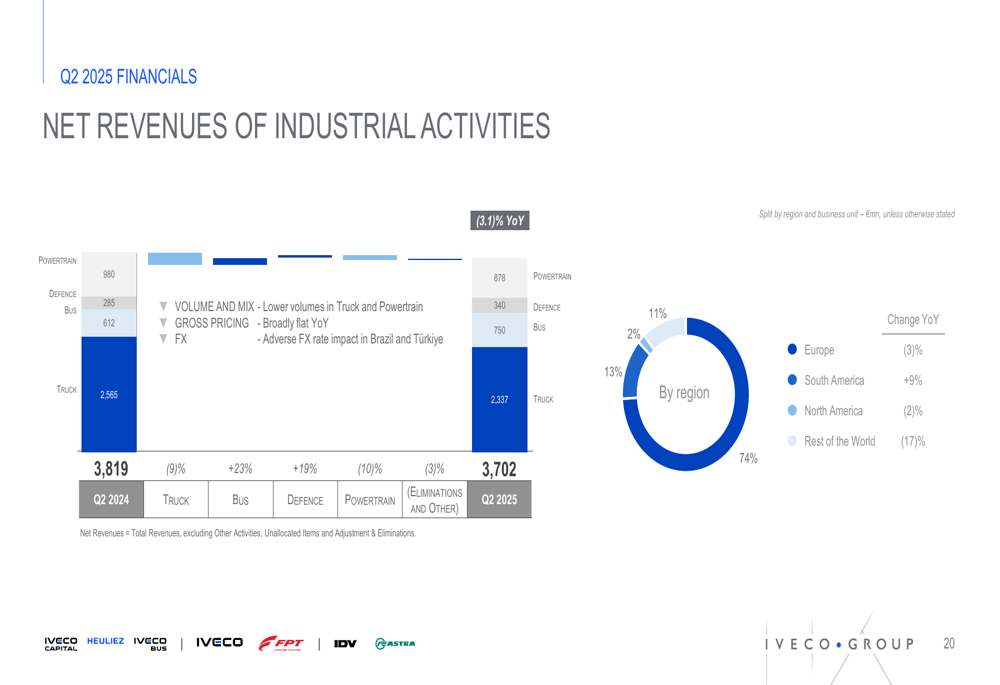

Net revenues of Industrial Activities decreased by 3.1% year-over-year, primarily due to lower volumes in the Truck and Powertrain segments and adverse FX impact in Brazil and Türkiye. By region, Europe (which accounts for 74% of revenues) saw a 3% decline, while South America grew by 9%. North America decreased by 2%, and Rest of the World fell by 17%.

The breakdown of net revenues by business unit and region is shown in the following slide:

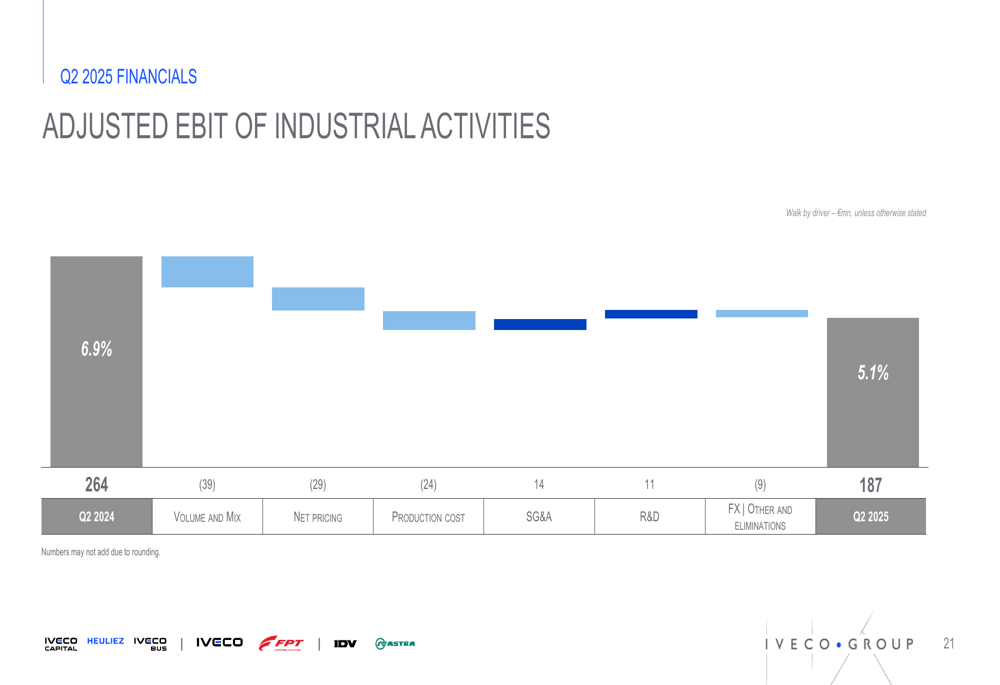

The adjusted EBIT of Industrial Activities declined from €264 million (6.9% margin) in Q2 2024 to €187 million (5.1% margin) in Q2 2025. This decrease was primarily driven by negative volume and mix effects (-€39 million), lower net pricing (-€29 million), and increased production costs (-€24 million). These negative factors were partially offset by improvements in SG&A (+€14 million) and R&D (+€11 million).

The waterfall chart below illustrates these changes:

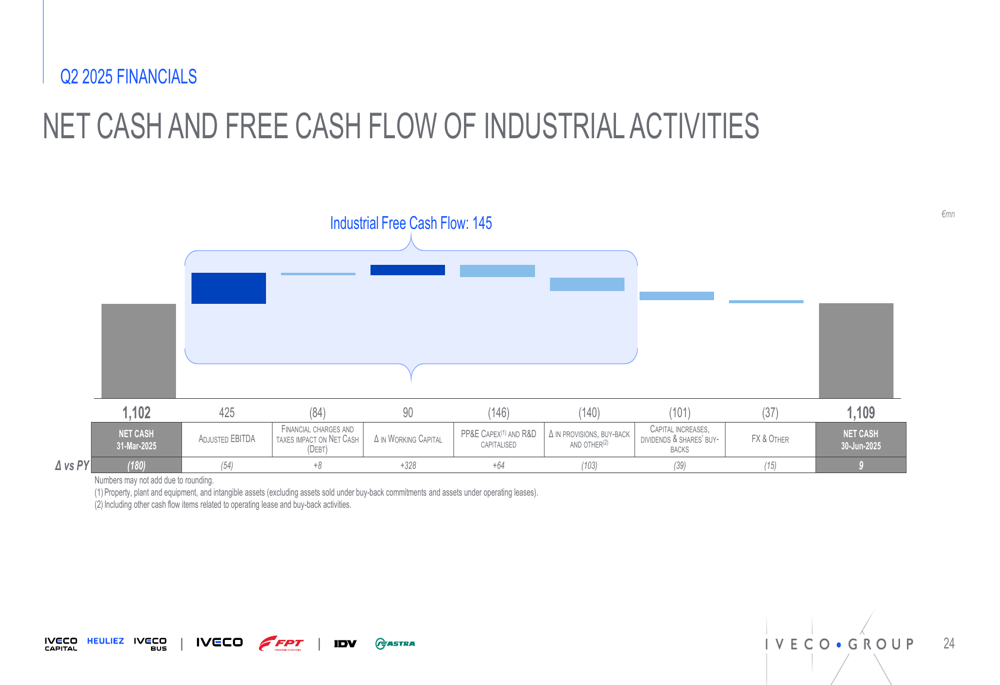

On the positive side, Iveco Group maintained a strong liquidity position with available liquidity of €4.7 billion, comprising €2.8 billion in cash and marketable securities and €1.9 billion in undrawn committed facilities. The company also generated a positive Industrial Activities free cash flow of €145 million during the quarter.

The following slide details the net cash and free cash flow movements:

Electric Vehicle Portfolio

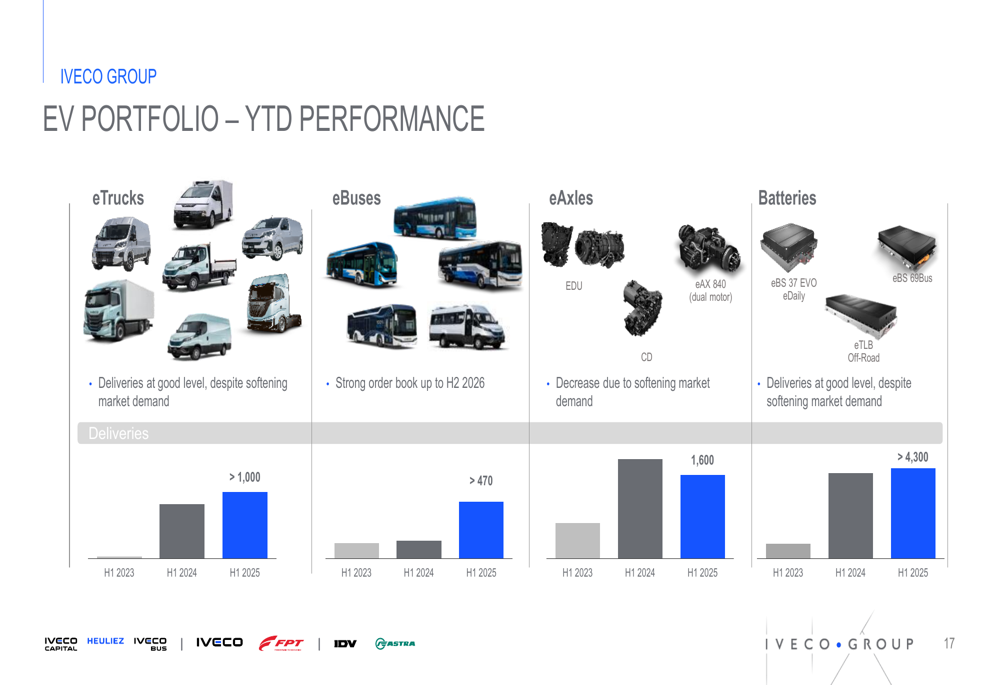

Despite market challenges, Iveco Group’s EV portfolio showed resilience with good delivery levels in eTrucks and a strong order book for eBuses extending to H2 2026. The company reported over 1,000 eTruck deliveries, more than 470 eBus deliveries, 1,600 eAxle deliveries, and over 4,300 battery deliveries in H1 2025.

The EV portfolio performance is illustrated in the following slide:

Forward-Looking Statements

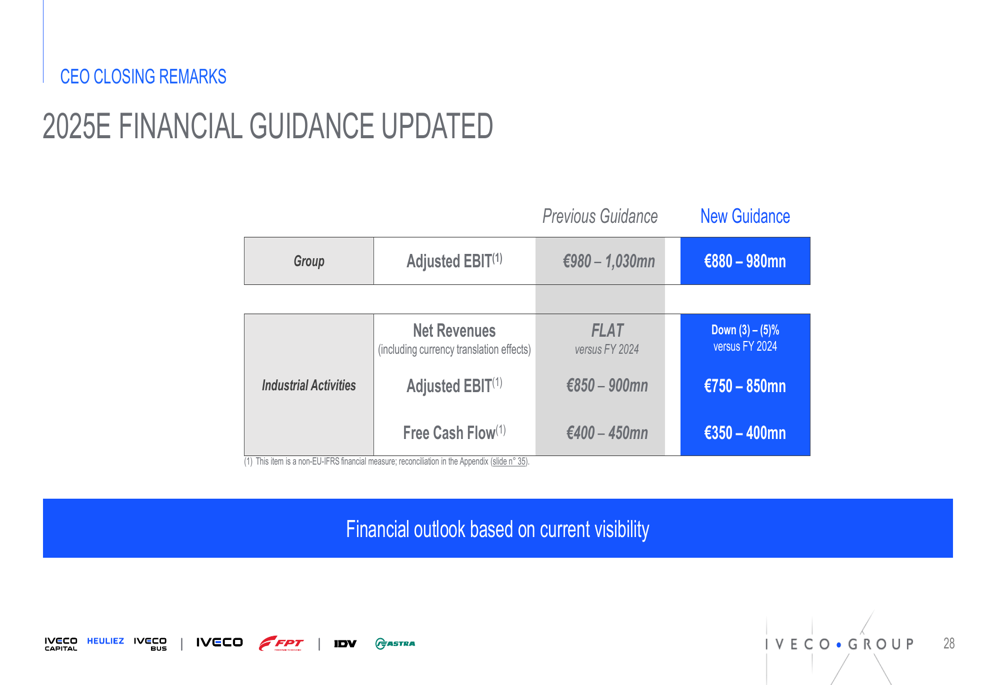

In a significant update, Iveco Group lowered its full-year 2025 financial guidance. The company now expects:

- Net revenues to decline by 3-5% (previously expected to be flat)

- Adjusted EBIT between €880-980 million (down from €980-1,030 million)

- Industrial Activities adjusted EBIT between €750-850 million (down from €850-900 million)

- Free cash flow between €350-400 million (down from €400-450 million)

The revised guidance reflects expectations of a slower progressive industry recovery, as shown in the following slide:

The industry volume outlook for 2025 remains challenging, with European light commercial vehicle volumes expected to decline by 10-15% and medium & heavy trucks by 5-10% compared to 2024. South American markets are projected to show some growth, while other regions are expected to remain flat.

Despite these challenges, management highlighted several positive factors, including continued year-over-year growth in order intake, sustained momentum in the Bus and Defence segments, and progress in the company’s Efficiency Programme. The acquisition by Tata Motors is also expected to create new opportunities for global expansion once completed.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.