Street Calls of the Week

Introduction & Market Context

Jamf (NASDAQ:JAMF), a leader in Apple (NASDAQ:AAPL) ecosystem management, presented its second quarter 2025 earnings results on August 7, 2025, showcasing continued strong performance across key financial metrics. The company maintained its growth trajectory in a competitive enterprise software market, with particular strength in its security offerings, which have become an increasingly important component of its overall business strategy.

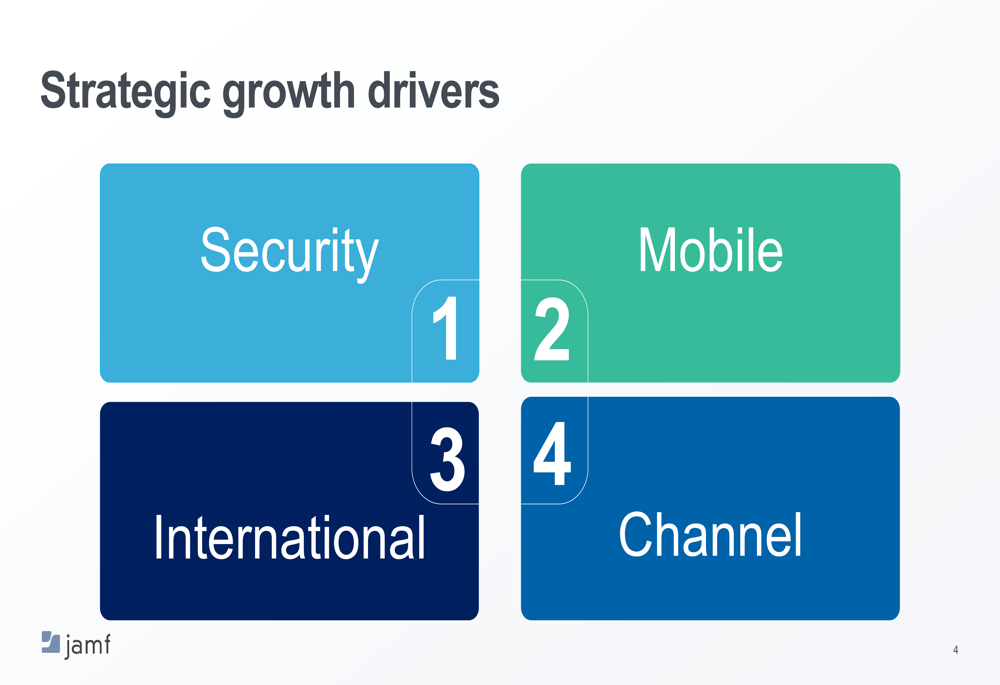

Building on momentum from previous quarters, Jamf’s presentation emphasized its balanced approach to growth and profitability, highlighting four strategic growth drivers: security, mobile, international expansion, and channel partnerships. The company’s performance reflects the ongoing demand for specialized Apple device management solutions across various market segments.

Quarterly Performance Highlights

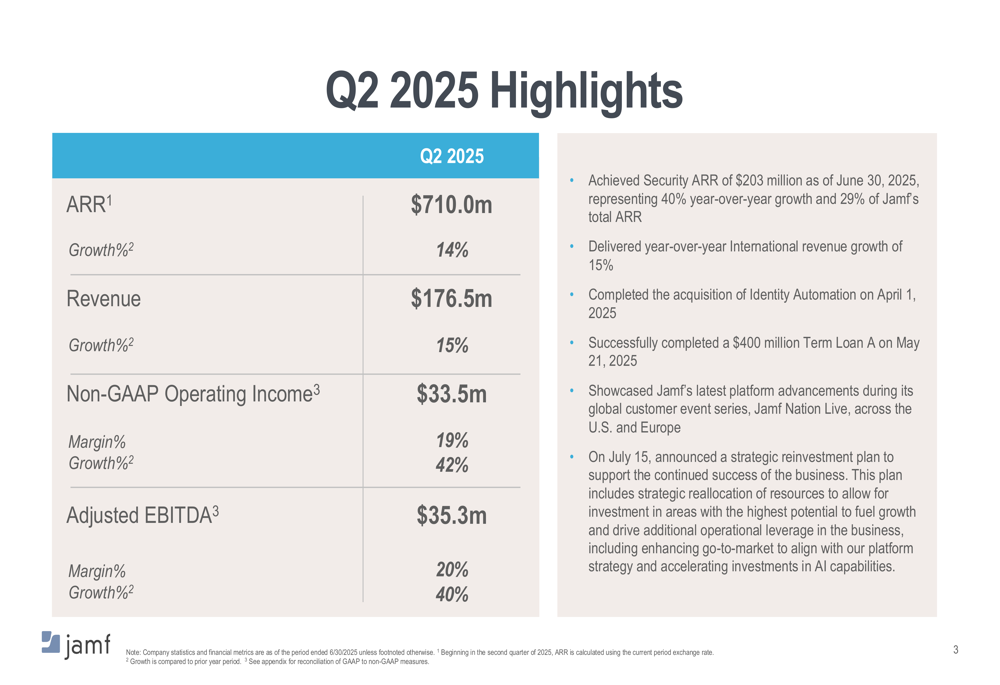

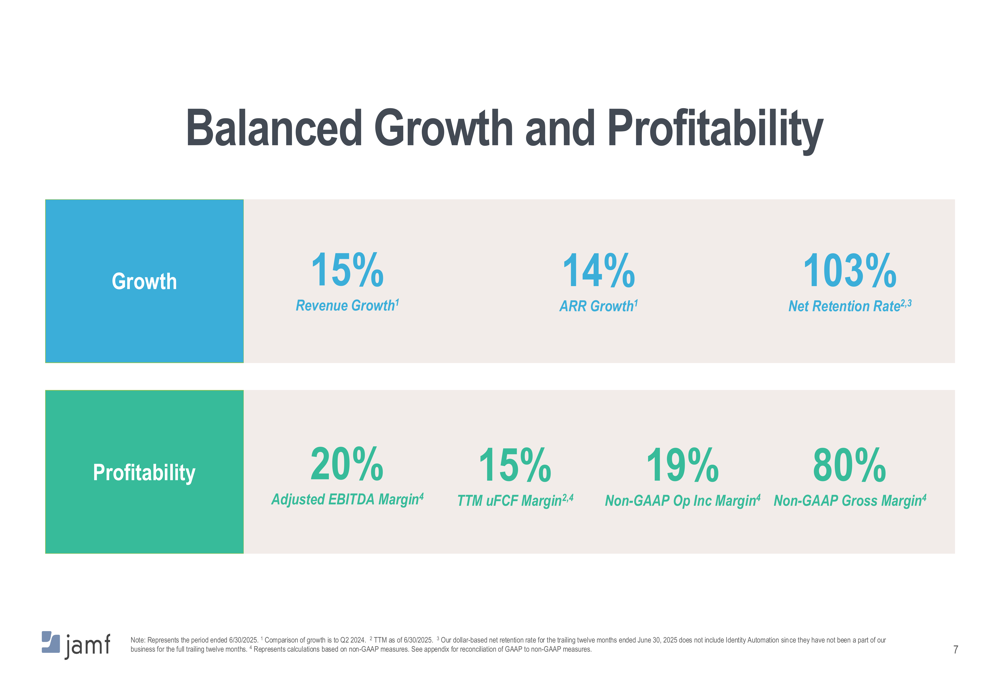

Jamf reported solid financial results for Q2 2025, with revenue reaching $176.5 million, representing a 15% year-over-year increase. Annual Recurring Revenue (ARR) grew to $710.0 million, up 14% compared to the same period last year. The company maintained a healthy Net Retention Rate of 103%, indicating strong customer loyalty and expansion within existing accounts.

As shown in the following chart of quarterly highlights, Jamf demonstrated significant improvement in profitability metrics, with Non-GAAP Operating Income of $33.5 million (19% margin) growing 42% year-over-year, and Adjusted EBITDA of $35.3 million (20% margin) increasing by 40%:

Particularly noteworthy was the performance of Jamf’s security offerings, which generated $203 million in ARR, representing 40% year-over-year growth and now accounting for 29% of the company’s total ARR. This acceleration in security-related revenue (up from 26% growth reported in Q3 2024) underscores the increasing importance of security solutions within Jamf’s product portfolio.

The company’s balanced approach to growth and profitability is illustrated in this comprehensive metrics overview:

International revenue also showed strong performance with 15% year-over-year growth, indicating successful geographic expansion beyond Jamf’s core North American market.

Strategic Initiatives

Jamf outlined four key strategic growth drivers that form the foundation of its business strategy: Security, Mobile, International, and Channel. These pillars represent the company’s focused approach to market expansion and revenue growth:

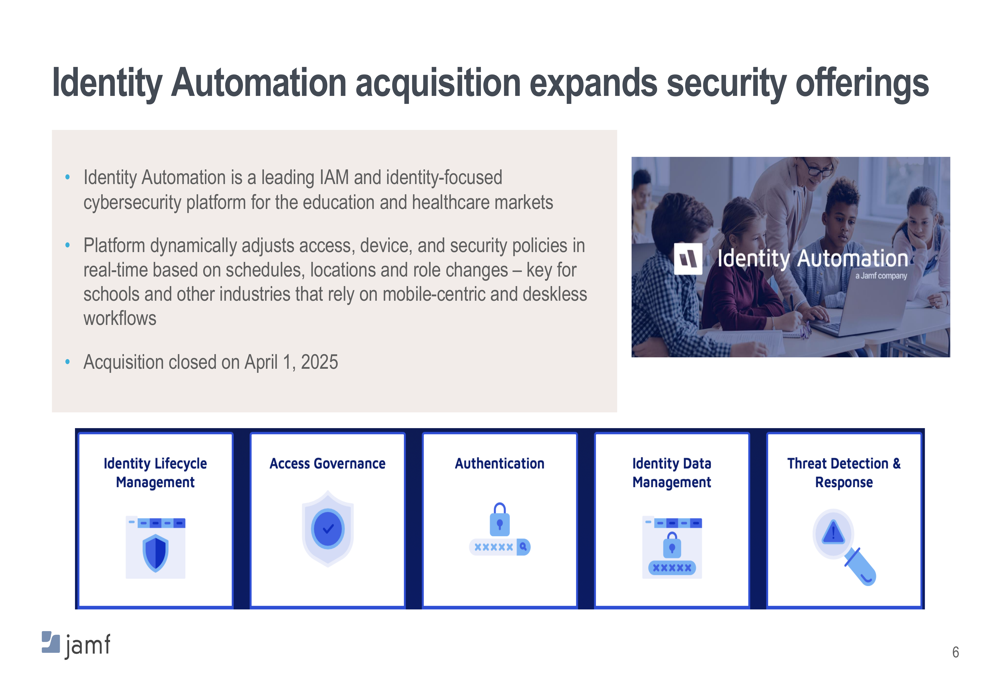

A significant development during the quarter was the acquisition of Identity Automation, a leading identity and access management (IAM) cybersecurity platform focused on the education and healthcare markets. The acquisition, which closed on April 1, 2025, strengthens Jamf’s security offerings by adding capabilities that dynamically adjust access, device, and security policies in real-time based on schedules, locations, and role changes.

As illustrated in the following slide, the Identity Automation acquisition enhances Jamf’s capabilities across several critical security domains:

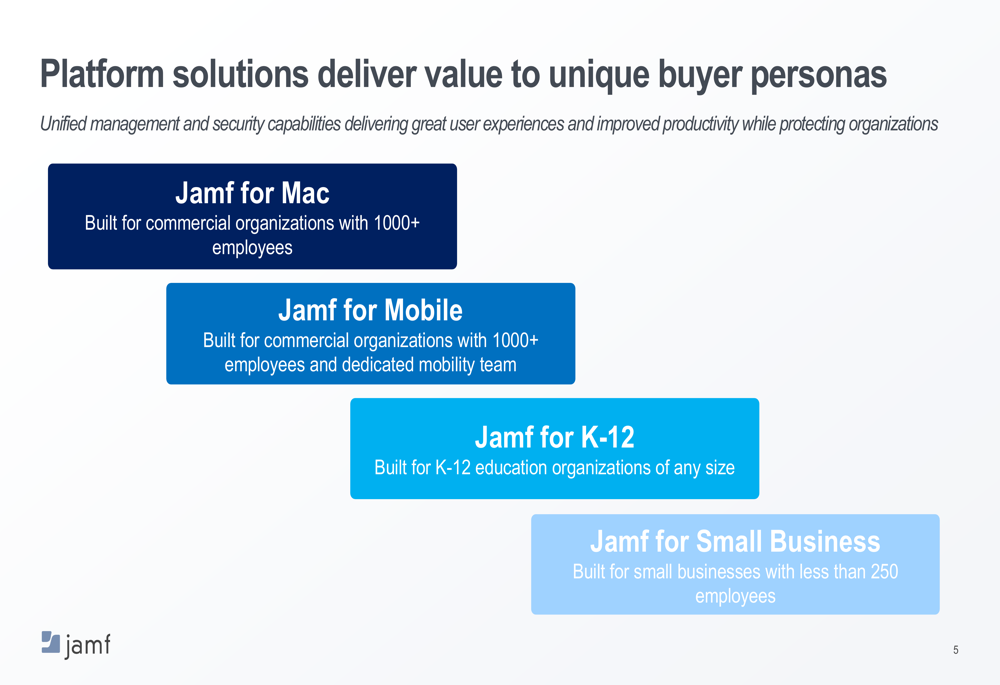

The company also highlighted its platform solutions tailored to specific buyer personas, demonstrating a segmented go-to-market strategy designed to address the unique needs of different customer types:

Additionally, Jamf completed a $400 million Term Loan A during the quarter and announced a strategic reinvestment plan, though specific details of this plan were not elaborated in the presentation materials.

Forward-Looking Statements

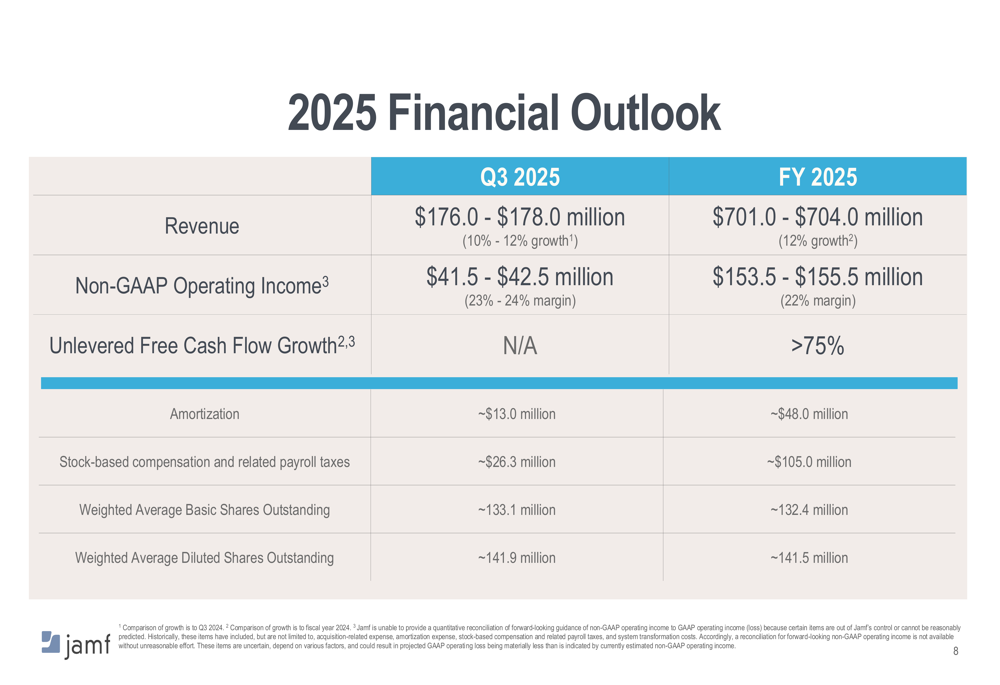

Jamf provided guidance for both the third quarter and full year 2025, projecting continued growth but at a slightly moderated pace compared to Q2 results. For Q3 2025, the company expects revenue between $176.0 and $178.0 million, representing 10-12% growth, with Non-GAAP Operating Income between $41.5 and $42.5 million (23-24% margin).

For the full year 2025, Jamf forecasts revenue of $701.0 to $704.0 million, reflecting 12% growth, and Non-GAAP Operating Income of $153.5 to $155.5 million (22% margin). The company also projects unlevered free cash flow growth exceeding 75% for the fiscal year.

The following slide details Jamf’s financial outlook for the remainder of 2025:

The projected revenue growth rate for Q3 2025 (10-12%) represents a slight deceleration from the 15% growth achieved in Q2, potentially reflecting broader market conditions or the timing of customer deployments.

Detailed Financial Analysis

Jamf’s presentation included detailed reconciliations between GAAP and non-GAAP financial measures. The company maintained a strong Non-GAAP Gross Margin of 80%, demonstrating the high-value nature of its software solutions and efficient delivery model.

The company’s GAAP operating loss for Q2 2025 was $15 million, an improvement from the $20 million loss in Q2 2024. After adjusting for amortization expense ($13 million), stock-based compensation ($28 million), and acquisition-related expenses ($3 million), among other items, Non-GAAP operating income reached $33.5 million.

Unlevered free cash flow for the first half of 2025 was $52 million, compared to $22 million in the first half of 2024, representing significant improvement in cash generation. The trailing twelve months unlevered free cash flow margin stood at 15%, highlighting Jamf’s ability to convert revenue into cash.

The company’s balance sheet was strengthened by the completion of a $400 million Term Loan A, providing additional financial flexibility for strategic investments and potential future acquisitions.

Overall, Jamf’s Q2 2025 presentation portrayed a company successfully balancing growth and profitability, with particular strength in high-growth segments like security while maintaining disciplined financial management. The slight moderation in projected growth rates for upcoming quarters will be an important area for investors to monitor as the company continues to execute on its strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.