Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

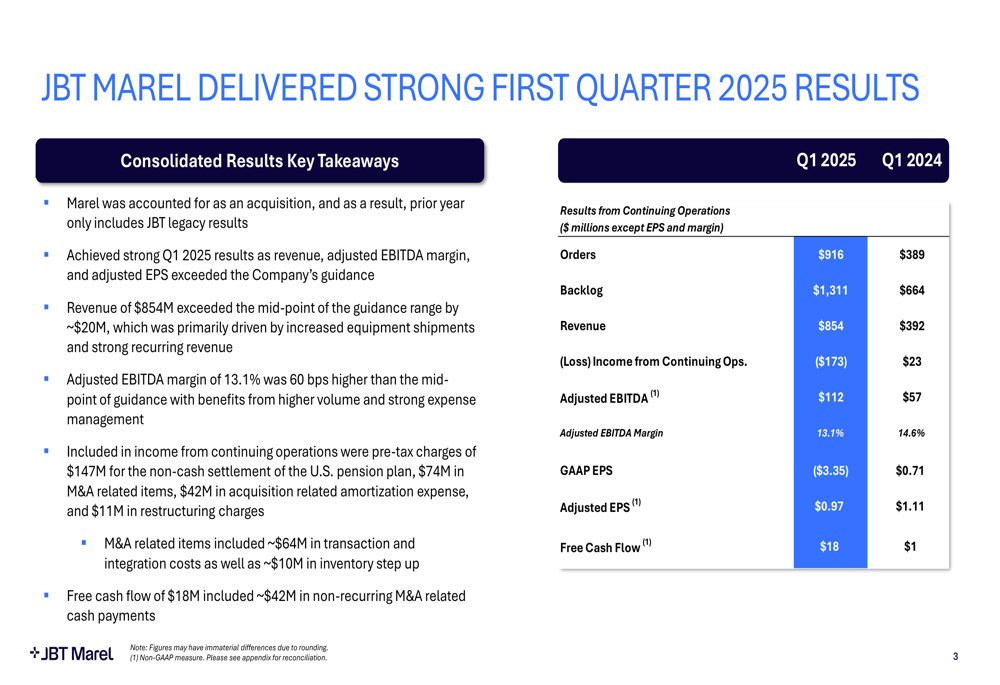

JBTMarel Corp (NYSE:JBTM) released its first quarter 2025 earnings presentation on May 5, 2025, revealing results that exceeded company guidance across key metrics. The food processing equipment manufacturer, formed through the recent merger of JBT and Marel, reported significant year-over-year growth in orders, backlog, and revenue, while implementing strategies to address tariff challenges and manage its leverage position.

The company’s stock has shown positive momentum, trading at $107.16 as of May 2, 2025, with a 1.58% increase. In pre-market trading, the stock was up an additional 0.93% to $108.16, reflecting investor confidence following the strong quarterly performance.

Quarterly Performance Highlights

JBTMarel reported Q1 2025 revenue of $854 million, exceeding the mid-point of guidance by approximately $20 million. This outperformance was primarily driven by increased equipment shipments and strong recurring revenue. The company’s adjusted EBITDA margin reached 13.1%, which was 60 basis points higher than the mid-point of guidance, benefiting from higher volume and strong expense management.

As shown in the following comprehensive results summary:

The company’s orders reached $916 million, compared to $389 million in Q1 2024, while backlog grew to $1,311 million from $664 million in the prior year. However, JBTMarel reported a loss from continuing operations of $173 million, which included significant one-time charges: $147 million for the non-cash settlement of the U.S. pension plan, $74 million in M&A related items, $42 million in acquisition related amortization expense, and $11 million in restructuring charges.

Free cash flow was $18 million, which included approximately $42 million in non-recurring M&A related cash payments, showing improvement from $1 million in Q1 2024.

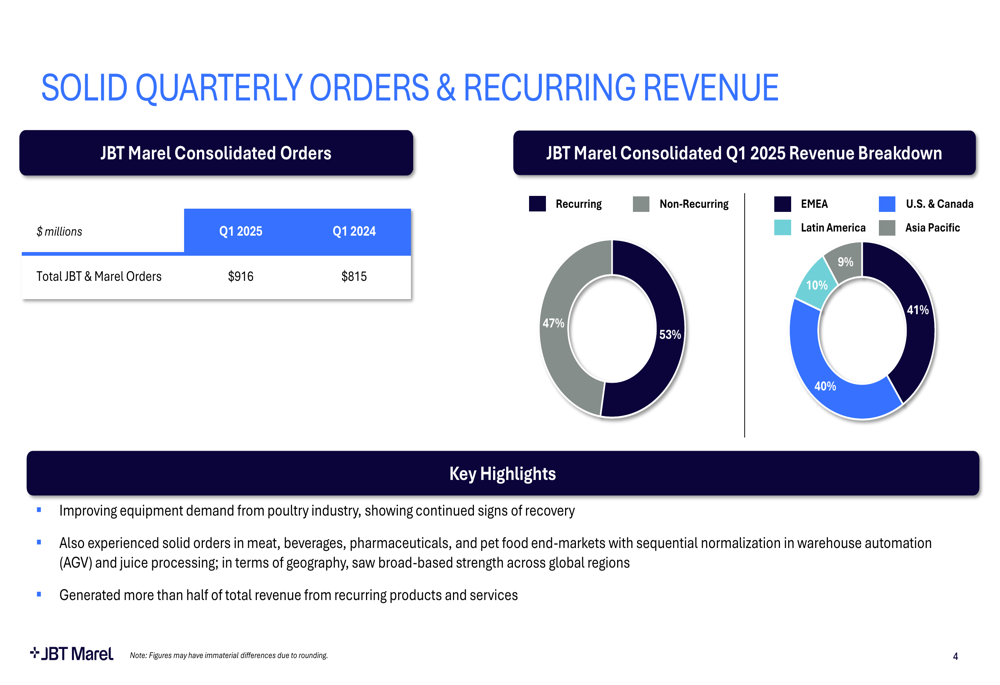

The company’s revenue is well-balanced between recurring and non-recurring sources, with a strong geographic diversification that helps mitigate regional market risks. The following breakdown illustrates this diversification:

Recurring revenue accounted for 47% of total revenue, providing stability to the company’s financial performance. Geographically, Asia Pacific (41%) and EMEA (40%) represented the largest markets, followed by U.S. & Canada (10%) and Latin America (9%).

JBTMarel highlighted improving equipment demand from the poultry industry, which is showing continued signs of recovery. The company also experienced solid orders in meat, beverages, pharmaceuticals, and pet food end-markets, with some normalization in warehouse automation and juice processing segments.

Segment Performance Analysis

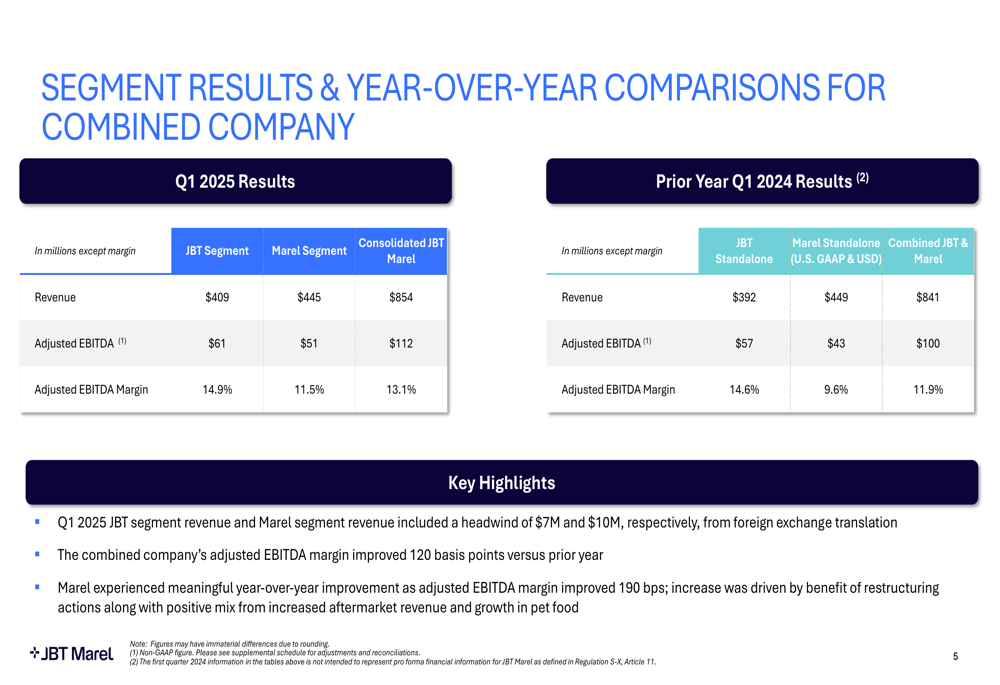

JBTMarel’s performance analysis by segment reveals important insights into the company’s operations following the merger. The JBT segment contributed $409 million in revenue with a 14.9% adjusted EBITDA margin, while the Marel segment generated $445 million with an 11.5% margin.

The detailed segment comparison with prior year results demonstrates significant improvement:

Notably, the Marel segment experienced meaningful year-over-year improvement with adjusted EBITDA margin increasing by 190 basis points compared to the prior year. This improvement was driven by benefits from restructuring actions, positive mix from increased aftermarket revenue, and growth in the pet food segment.

The combined company’s adjusted EBITDA margin improved by 120 basis points versus the prior year, highlighting successful integration efforts. It’s worth noting that Q1 2025 results included headwinds of $7 million and $10 million from foreign exchange translation for the JBT and Marel segments, respectively.

Financial Position and Tariff Mitigation Strategy

JBTMarel reported net debt of approximately $1.89 billion as of March 31, 2025, with a bank leverage ratio of 3.2x (including the benefit of certain run rate synergies). The company’s net debt to trailing twelve months adjusted EBITDA ratio was 3.8x, an improvement of approximately 0.2x from January 2, 2025.

The company maintains ample liquidity of approximately $1.3 billion, providing significant financial flexibility to fund strategic initiatives. Management expects to reduce the bank leverage ratio to below 3.0x by year-end 2025.

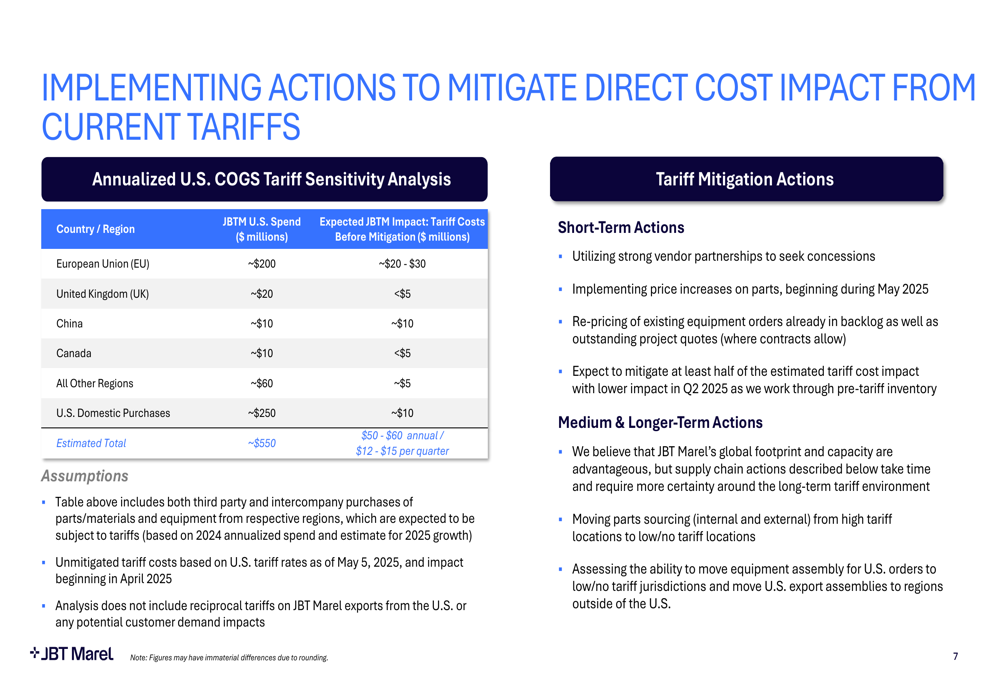

A key challenge facing JBTMarel is the impact of current tariffs on its cost structure. The company has developed a comprehensive mitigation strategy to address this issue:

The tariff sensitivity analysis shows a potential annual impact of $50-60 million before mitigation efforts. To address this, JBTMarel is implementing both short-term actions (vendor partnerships, price increases, re-pricing of existing orders) and medium to long-term strategies (relocating parts sourcing and equipment assembly to low/no tariff jurisdictions).

Forward Outlook

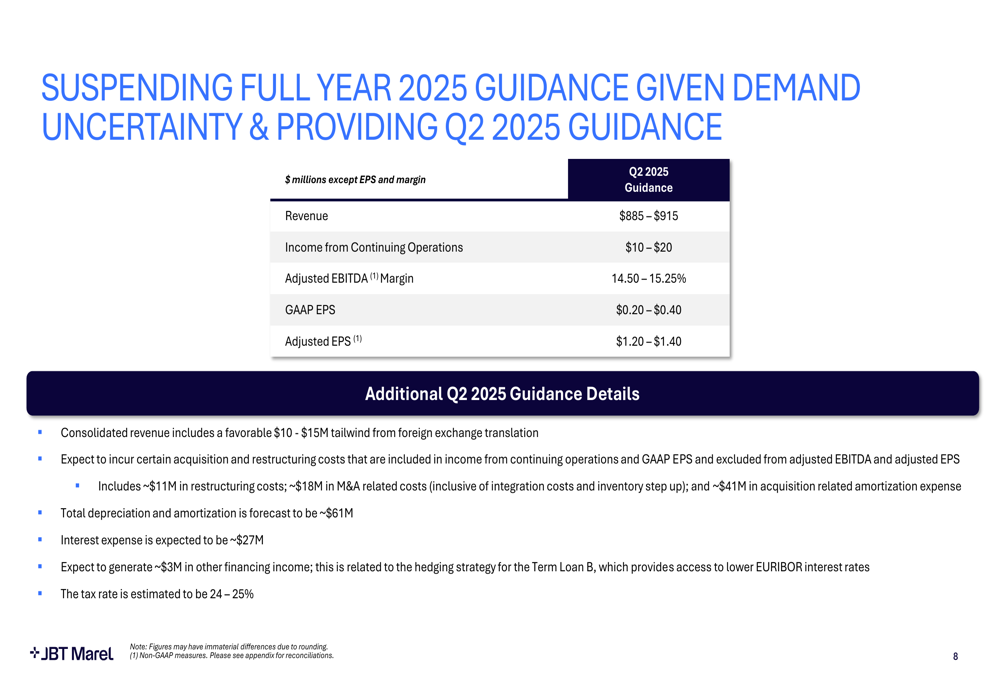

While JBTMarel has suspended its full-year 2025 guidance, the company provided a detailed outlook for Q2 2025:

For Q2 2025, JBTMarel expects revenue between $885-915 million, income from continuing operations of $10-20 million, and adjusted EBITDA margin of 14.50-15.25%. The adjusted EPS guidance is $1.20-1.40, compared to GAAP EPS of $0.20-0.40.

The Q2 guidance includes a favorable $10-15 million tailwind from foreign exchange translation. The company also expects to incur certain acquisition and restructuring costs, including approximately $11 million in restructuring costs, $18 million in M&A related costs, and $41 million in acquisition related amortization expense.

This outlook represents sequential improvement in margins compared to Q1 2025, suggesting continued operational efficiencies and realization of synergies from the merger. The company’s focus on tariff mitigation and leverage reduction positions it well for sustainable growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.