These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

JetBlue Airways Corp (NASDAQ:JBLU) presented its first quarter 2025 earnings on April 29, revealing performance within initial guidance ranges but warning of significant revenue pressure ahead. The airline continues to navigate industry-wide demand softness, particularly in off-peak periods, while its premium segments show relative resilience. This comes as JetBlue’s stock has struggled, trading at $4.07 as of April 28, 2025, well below its 52-week high of $8.31, reflecting ongoing investor concerns about the carrier’s path to sustainable profitability.

Quarterly Performance Highlights

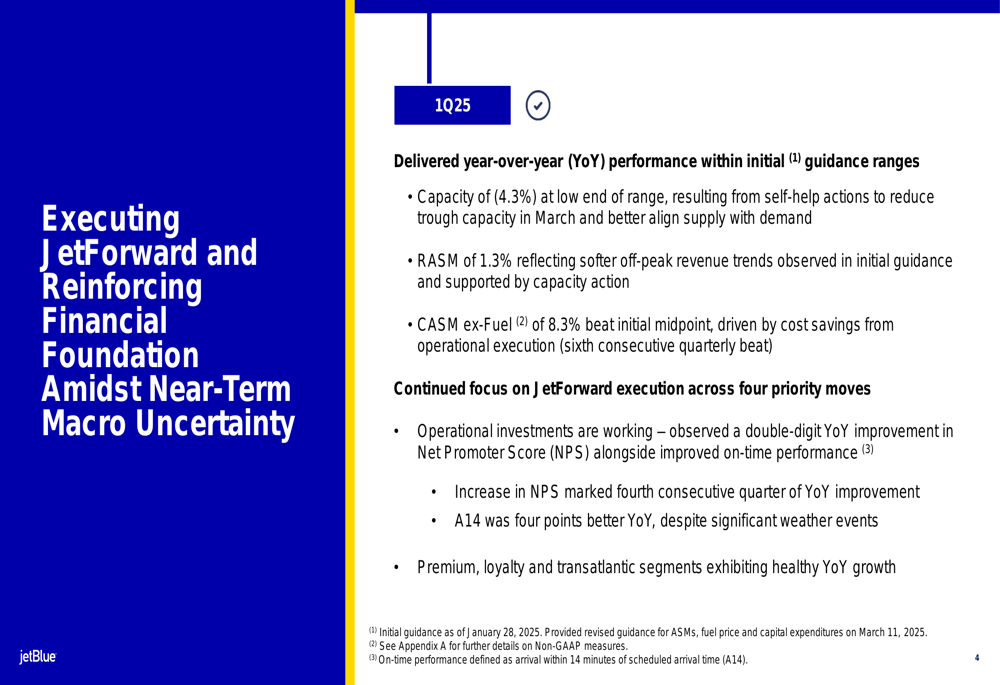

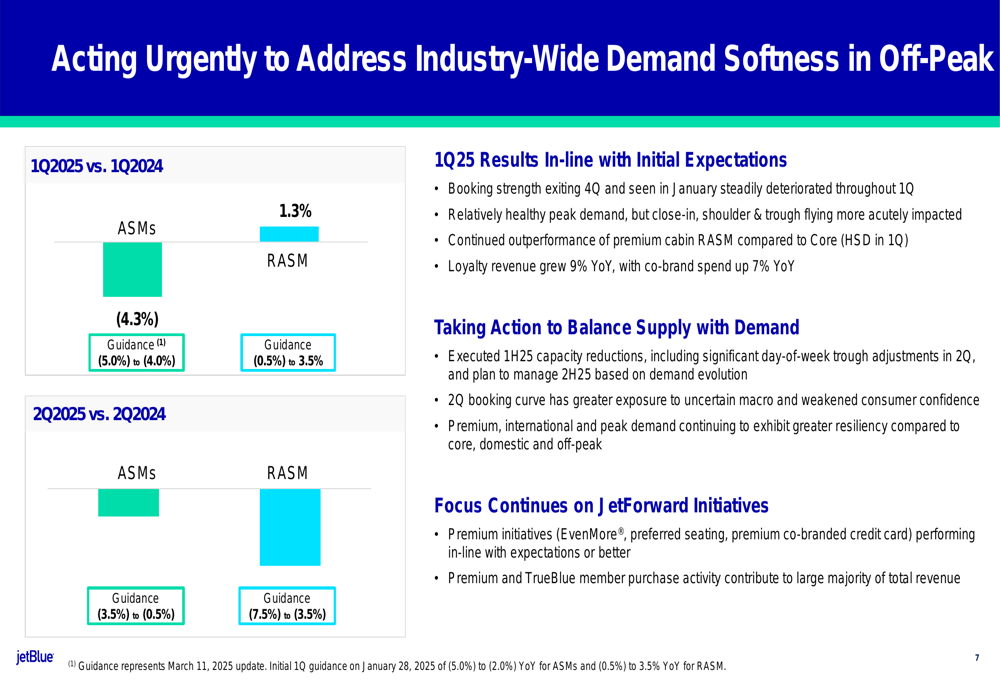

JetBlue reported first quarter results that aligned with initial guidance, with capacity down 4.3% year-over-year at the low end of its projected range. Revenue per available seat mile (RASM) grew 1.3%, reflecting softer off-peak revenue trends, while cost per available seat mile excluding fuel (CASM ex-Fuel) increased 8.3%, beating the initial midpoint guidance.

The company highlighted a double-digit year-over-year improvement in Net Promoter Score (NPS), marking the fourth consecutive quarter of improvement, suggesting operational reliability initiatives are gaining traction with customers.

As shown in the following overview of JetBlue’s Q1 performance:

Premium cabin revenue significantly outperformed core offerings, with high single-digit RASM growth in the first quarter. Loyalty revenue grew 9% year-over-year, with co-brand spend up 7%, demonstrating the resilience of JetBlue’s higher-yield segments despite broader market challenges.

Strategic Initiatives

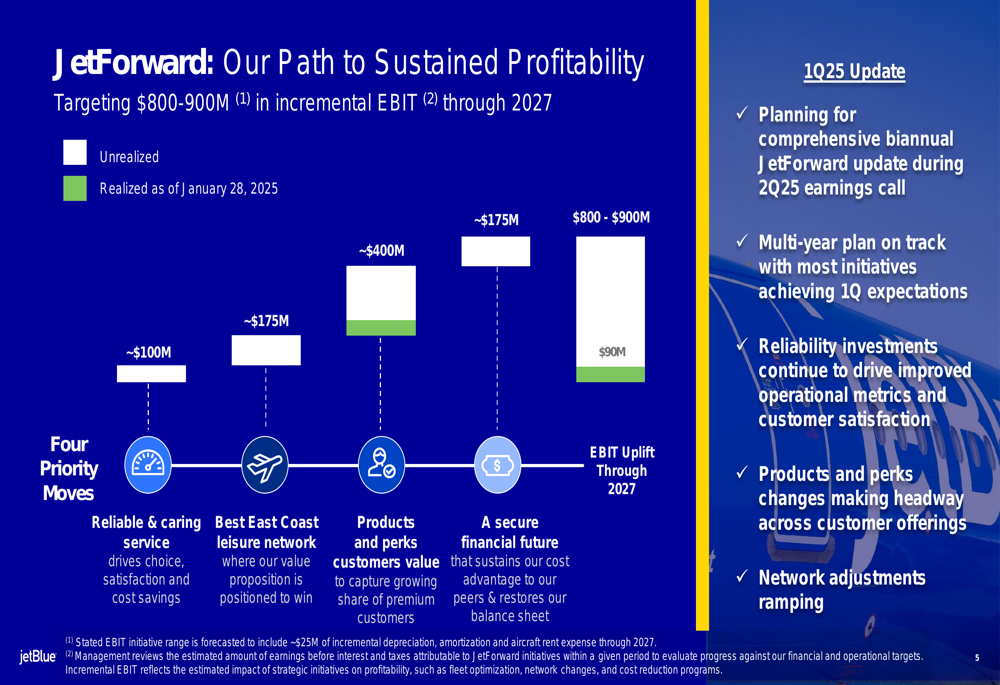

JetBlue continues to execute its "JetForward" strategic plan, which targets $800-900 million in incremental earnings before interest and taxes (EBIT) through 2027. The plan focuses on four key areas: reliable and caring service, optimizing the East Coast leisure network, enhancing products and perks customers value, and securing a stable financial future.

The following chart illustrates JetBlue’s path to sustained profitability through the JetForward initiative:

The company reported that its multi-year plan remains on track, with reliability investments driving operational improvements and product enhancements making headway. JetBlue plans to provide comprehensive biannual JetForward updates during its second quarter earnings call.

Detailed Financial Analysis

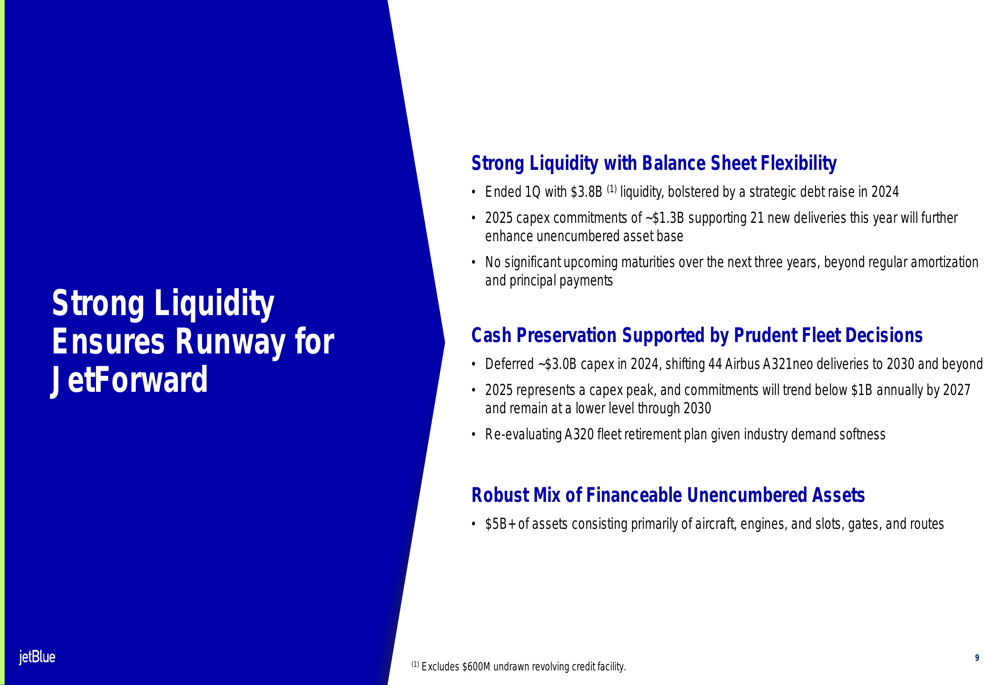

JetBlue maintains a strong liquidity position, ending the first quarter with $3.8 billion in liquidity. The airline faces capital expenditure commitments of approximately $1.3 billion in 2025, which represents a peak year for capital spending. Management emphasized that the company has no significant debt maturities over the next three years and possesses over $5 billion in financeable unencumbered assets.

The following slide details JetBlue’s liquidity position:

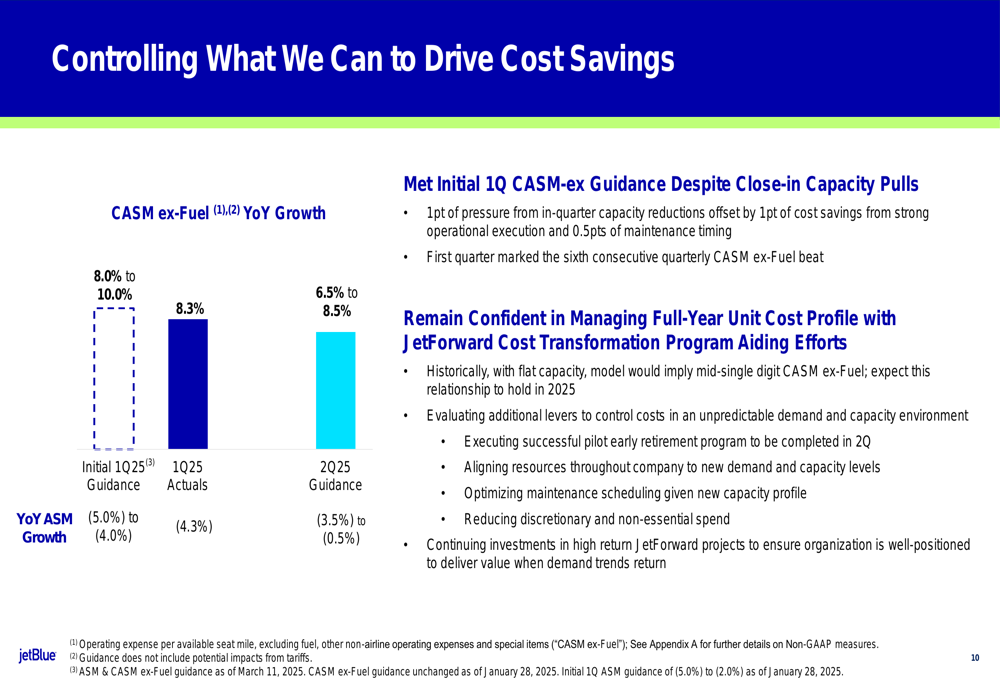

On the cost front, JetBlue successfully met its initial first quarter CASM ex-Fuel guidance despite close-in capacity reductions. The company noted that one percentage point of pressure from in-quarter capacity reductions was offset by one percentage point of cost savings.

As illustrated in the following cost control overview:

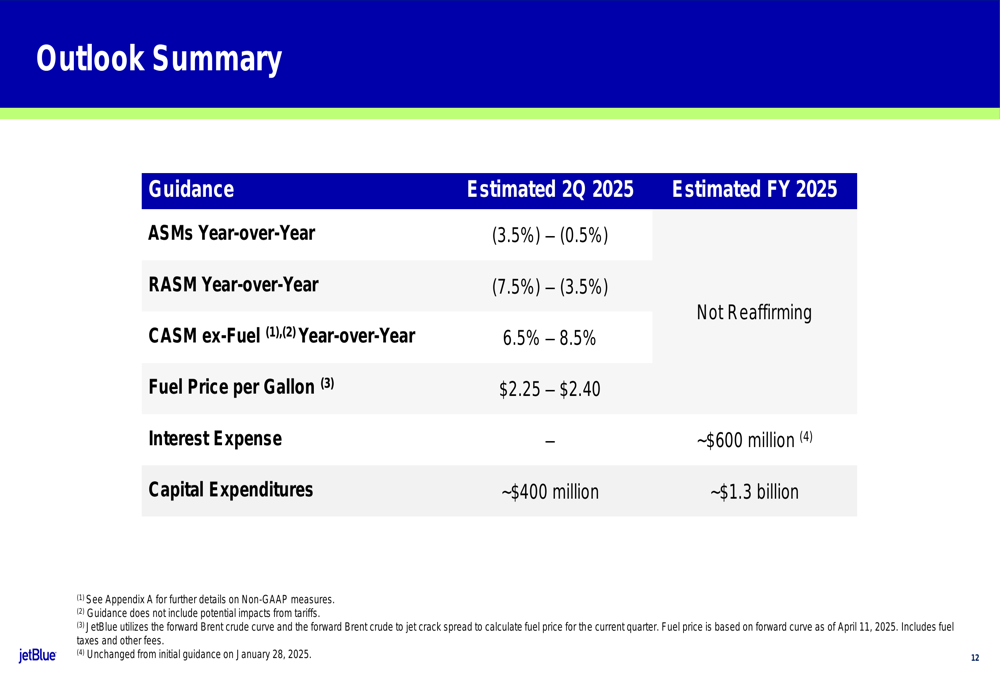

JetBlue has revised its second quarter CASM ex-Fuel guidance to 6.5% to 8.5% year-over-year growth, down from the initial 8% to 10% range, demonstrating progress in cost management despite capacity constraints.

Forward-Looking Statements

JetBlue’s outlook for the second quarter reflects significant challenges, with capacity projected to decrease between 3.5% and 0.5% year-over-year. More concerning is the RASM guidance showing a decline of 7.5% to 3.5% year-over-year, indicating substantial revenue pressure ahead.

The company attributed this outlook to deteriorating booking trends throughout the first quarter after a strong January, with close-in, shoulder, and trough flying periods most acutely impacted. Management noted that the second quarter booking curve has greater exposure to uncertain macroeconomic conditions and weakened consumer confidence.

The following slide details JetBlue’s approach to addressing demand softness:

JetBlue has executed capacity reductions for the first half of 2025, including significant day-of-week trough adjustments in the second quarter, and plans to manage second-half capacity based on demand evolution.

Despite these challenges, the company emphasized that premium, international, and peak demand continue to exhibit greater resilience compared to core, domestic, and off-peak segments.

The complete outlook summary for the second quarter is shown below:

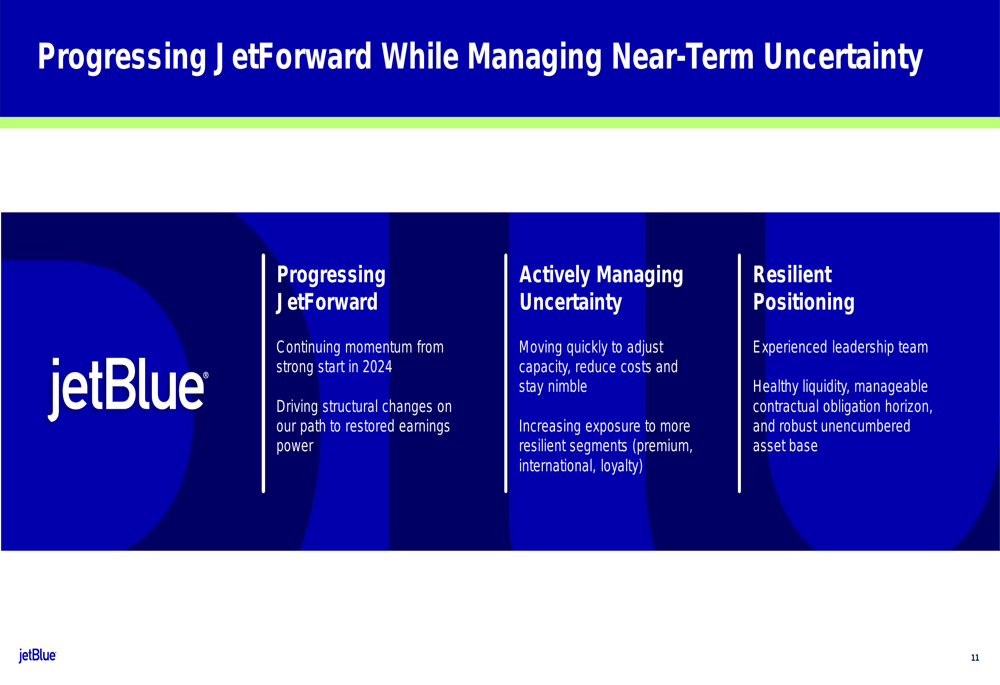

JetBlue’s strategy for navigating the current uncertainty focuses on three pillars: progressing the JetForward initiative, actively managing near-term uncertainty through capacity adjustments, and maintaining its resilient positioning with experienced leadership and healthy liquidity.

As JetBlue faces headwinds in the coming quarters, the execution of its JetForward plan and ability to adapt to changing demand patterns will be critical in determining whether the airline can achieve its long-term profitability goals in an increasingly challenging market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.