Gold prices steady ahead of Fed decision, Trump’s tariff deadline

Introduction & Market Context

JinkoSolar Holding Co., Ltd. (NYSE:JKS), a leading global solar module manufacturer, presented its Q1 2025 earnings results on April 29, 2025, revealing significant financial challenges amid ongoing industry headwinds. Despite maintaining its position as the industry’s top module supplier, the company reported substantial declines in shipments, revenue, and profitability compared to both the previous quarter and the same period last year.

The presentation highlighted JinkoSolar’s continued focus on technological innovation, global manufacturing expansion, and product portfolio optimization as strategies to navigate the challenging market environment. The company’s financial results reflect broader pressures facing the solar industry, including pricing challenges and market adjustments.

Quarterly Performance Highlights

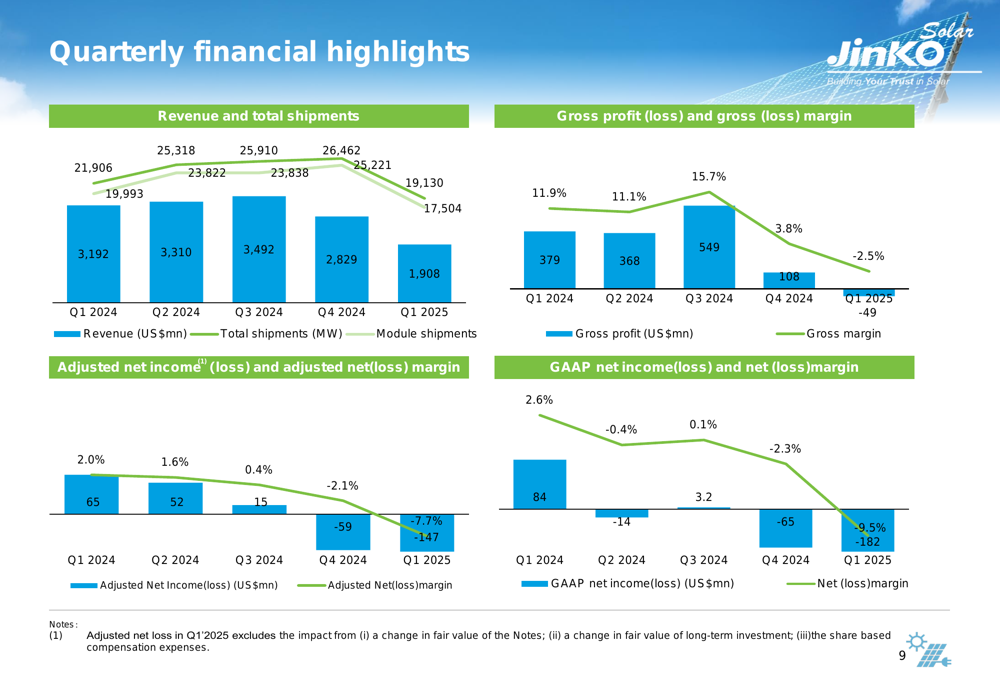

JinkoSolar reported total shipments of 19,130 MW in Q1 2025, representing a 27.7% decrease quarter-over-quarter and a 12.7% decline year-over-year. Module shipments, which accounted for the majority of total shipments at 17,504 MW, decreased by 30.6% from the previous quarter.

Revenue fell sharply to US$1.91 billion, down 33.0% sequentially and 39.9% compared to Q1 2024. More concerning was the company’s shift to negative profitability, with a gross loss margin of 2.5%, compared to positive margins of 3.8% in Q4 2024 and 11.9% in Q1 2024.

As shown in the following detailed quarterly financial data:

The company reported a net loss attributable to shareholders of US$182 million, with an adjusted net loss of US$147 million after excluding the impact from changes in fair value of convertible senior notes, long-term investments, and share-based compensation expenses. The net loss margin deteriorated to -9.5%, compared to -2.3% in the previous quarter and a positive 2.6% in the same period last year.

The income statement summary further illustrates the extent of the financial challenges:

Despite these challenges, JinkoSolar maintained a relatively stable cash position of US$3.77 billion, only slightly down from US$3.80 billion at the end of Q4 2024. However, the company’s total debt increased to US$6.41 billion, up from US$5.56 billion in the previous quarter and US$4.00 billion a year ago.

Strategic Initiatives

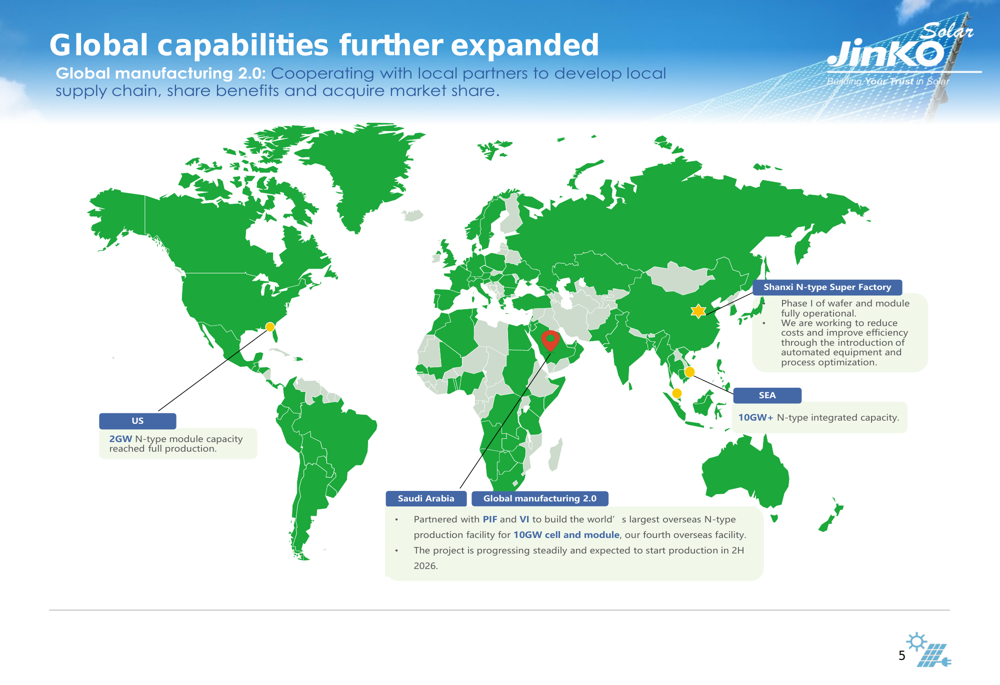

JinkoSolar continues to expand its global manufacturing footprint as part of its localization strategy. The company highlighted several key developments in its global capabilities:

In the United States, JinkoSolar’s 2GW N-type module capacity has reached full production. The company’s Shanxi N-type Super Factory in China has completed Phase I of wafer and module production. In Southeast Asia, the company has established over 10GW of N-type integrated capacity.

A significant development is JinkoSolar’s partnership with PIF and VI to build what it describes as the world’s largest overseas N-type production facility in Saudi Arabia, with 10GW cell and module capacity. This will be the company’s fourth overseas facility and is expected to start production in the second half of 2026.

The company is also optimizing its product portfolio, with a strong focus on its premium N-type offerings:

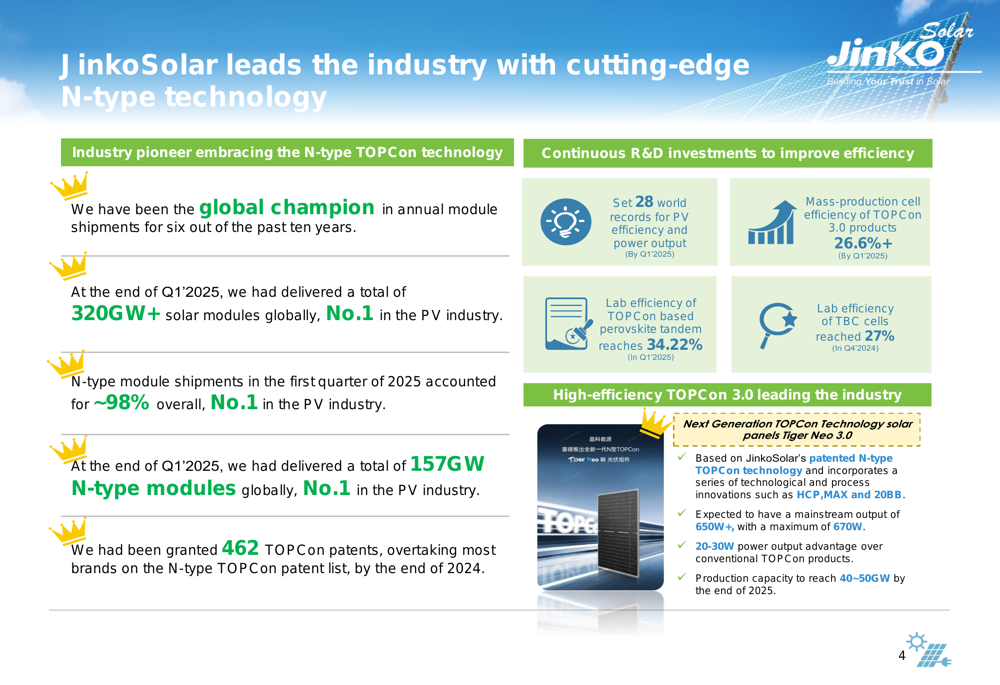

Tiger Neo modules accounted for 98% of overall shipments in Q1 2025, demonstrating the company’s successful transition to higher-efficiency products. JinkoSolar is also expanding its energy storage system (ESS) business, with Q1 2025 shipments of 310 MWh, representing significant year-over-year growth. The company targets ESS shipments of 6GWh for the full year 2025, with overseas markets as a strategic priority.

Competitive Industry Position

Despite financial challenges, JinkoSolar maintains its position as an industry leader. The company’s module shipments for Q1 2025 ranked first in the industry at 17.5 GW. By the end of the quarter, JinkoSolar became the first module manufacturer to have delivered a total of over 320 GW of solar modules globally, covering nearly 200 countries and regions.

The company’s business highlights underscore its market leadership and technological achievements:

JinkoSolar’s technological innovation continues to advance, with its N-type TOPCon-based perovskite tandem solar cell setting a new record conversion efficiency of 34.22%. The company has also been recognized as a Tier 1 energy storage provider by Bloomberg New Energy Finance for the fourth consecutive quarter.

The company’s global sales capabilities remain strong, with 70% of modules shipped overseas in Q1 2025. Shipments to Indo-Pacific markets grew by 150% quarter-over-quarter and nearly 10% year-over-year. North American shipments accounted for approximately 5% of total shipments in the quarter.

Forward-Looking Statements

Looking ahead, JinkoSolar provided guidance for Q2 2025 module shipments of 20.0-25.0 GW, suggesting a potential recovery from Q1 levels. For the full year 2025, the company expects module shipments of 85-100 GW and ESS shipments of approximately 6 GWh.

The company’s business plan outlines several key targets and initiatives for 2025:

JinkoSolar aims to increase the mass production cell efficiency of its high-efficiency TOPCon products to approximately 27% by the end of 2025. The company plans to expand its manufacturing capacity, with targets of 120GW for mono wafer, 95GW for cell, and 130GW for module production by year-end, including 40-50GW for TOPCon 3.0 products.

The company also emphasized its focus on optimizing its assets and liabilities structure while maintaining a healthy cash reserve. JinkoSolar plans to continue refining its market strategies and supply chain management while improving technology and product competitiveness to navigate the challenging market environment.

With an order book visibility for 2025 currently at 60-70% overall, and exceeding 80% in the Indo-Pacific and Middle East/Africa regions, JinkoSolar appears positioned to maintain its market leadership despite the current financial headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.