EUR/USD likely to find a peak near 1.25: UBS

Introduction & Market Context

J.M. Smucker (NYSE:SJM) released its fiscal fourth quarter 2025 results on June 10, showing a 3% decline in net sales and a significant net loss per share, primarily due to goodwill impairment charges. The market reacted negatively to the results, with the stock falling 5.92% to $105.23 in premarket trading, extending the downward trend that began after disappointing Q3 results earlier this year.

The company’s Q4 performance reflects ongoing challenges in its Sweet Baked Snacks segment, which saw substantial declines in both sales and profit, while other segments like Frozen Handheld & Spreads showed strong growth. Despite these mixed results, J.M. Smucker provided an optimistic outlook for fiscal 2026, projecting net sales growth of 2-4%.

Quarterly Performance Highlights

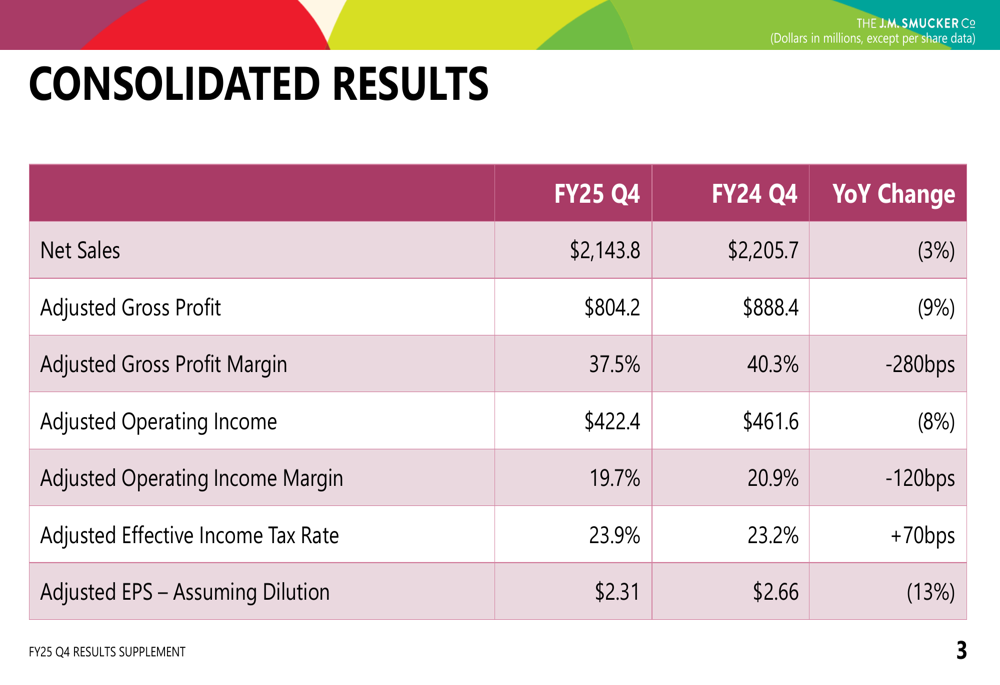

J.M. Smucker reported Q4 net sales of $2.14 billion, down 3% from the prior year, with comparable net sales (excluding divestitures and foreign currency exchange) decreasing 1%. The company posted a net loss per diluted share of $6.85, primarily due to goodwill impairment charges, while adjusted earnings per share came in at $2.31, a 13% decrease from the previous year.

As shown in the following consolidated results chart, the company experienced margin pressure with adjusted gross profit declining 9% to $804.2 million and adjusted gross profit margin contracting 280 basis points to 37.5%:

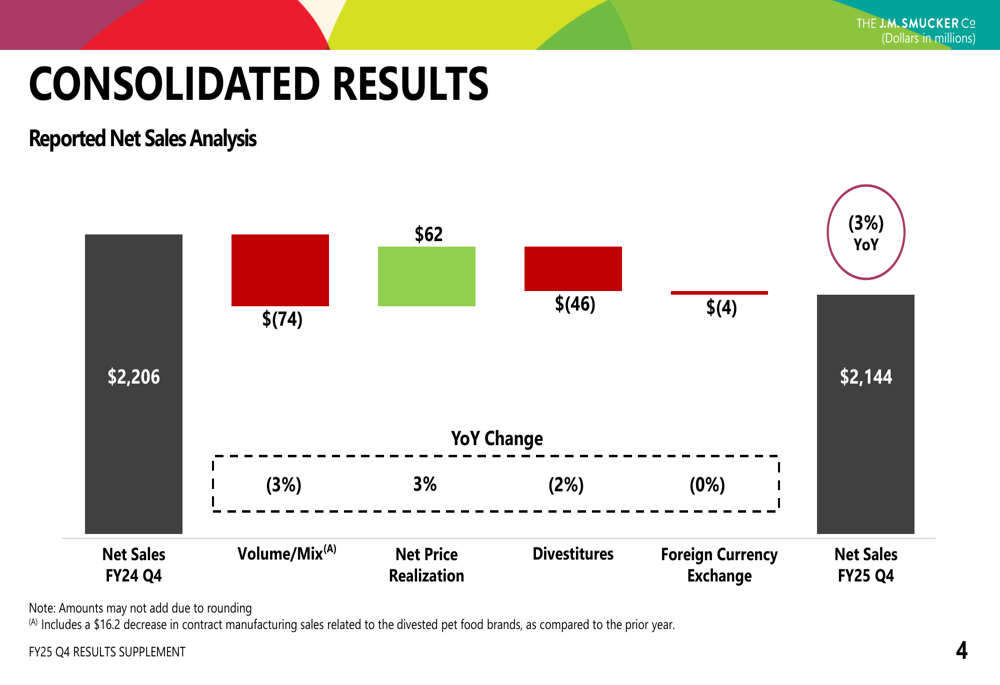

The decline in net sales was driven by negative volume/mix of $74 million, partially offset by positive net price realization of $62 million. Divestitures and foreign currency exchange also negatively impacted reported sales:

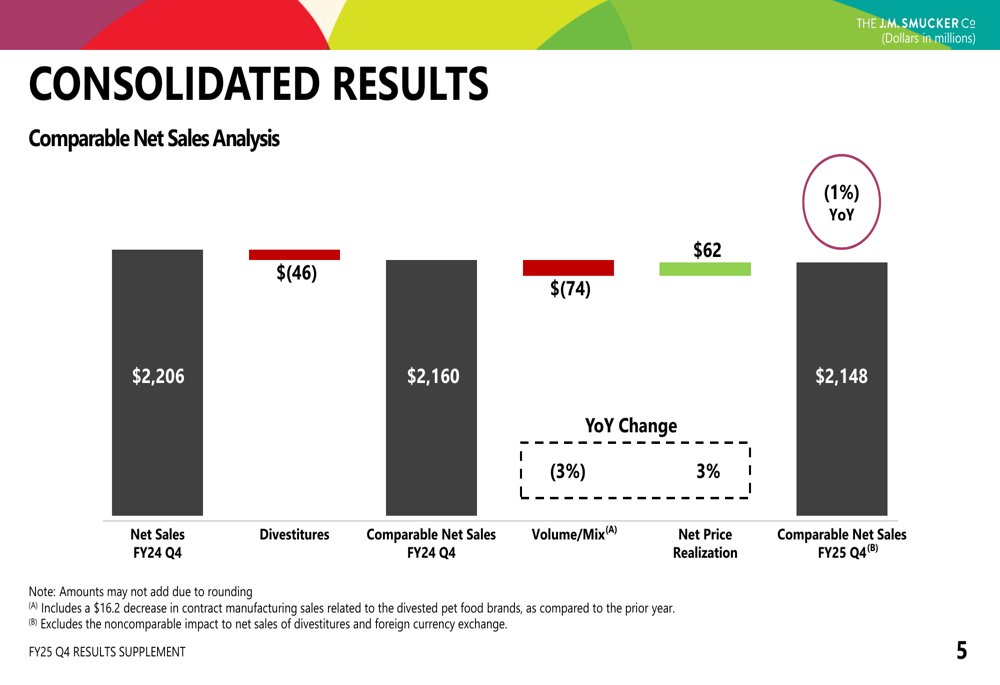

When looking at comparable net sales, which excludes the impact of divestitures and foreign currency exchange, the company saw a 1% decline, with the same volume/mix and pricing dynamics:

Detailed Financial Analysis

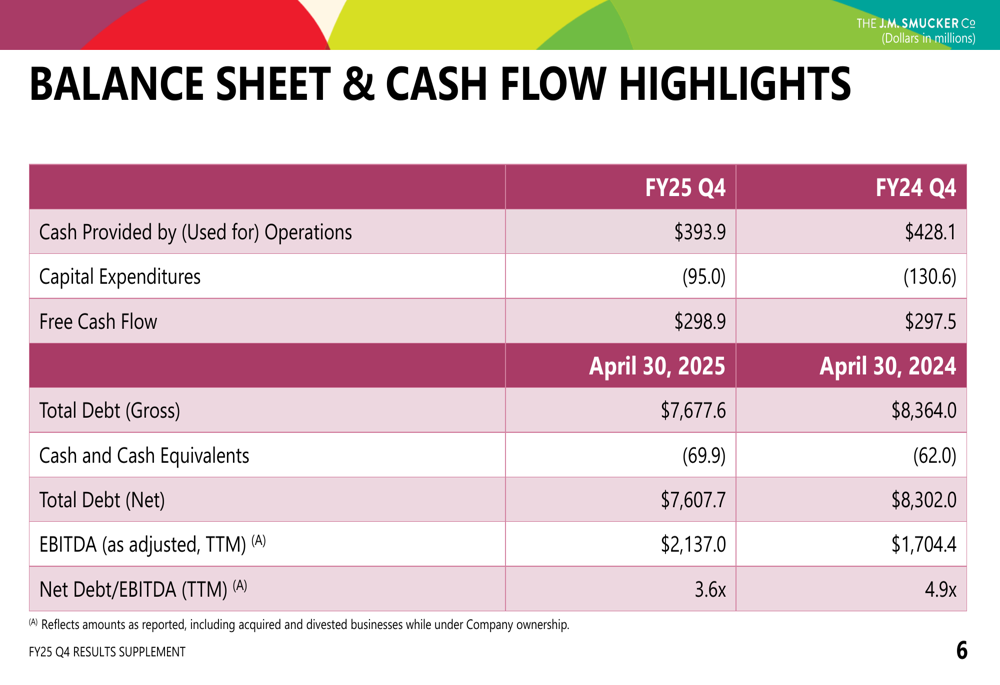

J.M. Smucker’s balance sheet showed improvement with total debt decreasing to $7.68 billion as of April 30, 2025, compared to $8.36 billion a year earlier. The company’s net debt to EBITDA ratio improved significantly to 3.6x from 4.9x in the prior year, reflecting progress in deleveraging efforts. Free cash flow remained stable at $298.9 million compared to $297.5 million in the prior year:

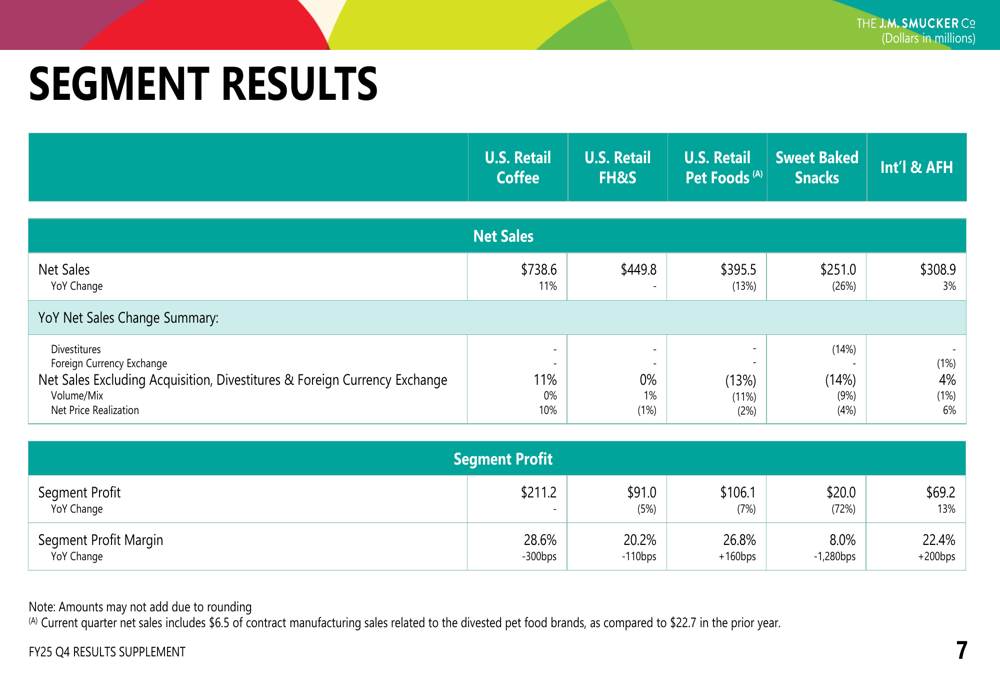

Segment performance varied widely across the company’s portfolio. U.S. Retail Coffee showed modest growth with net sales up 1%, while U.S. Retail Frozen Handheld & Spreads delivered strong performance with sales increasing 11%. However, U.S. Retail Pet Foods and Sweet Baked Snacks faced significant challenges, with sales declining 13% and 26%, respectively. The Sweet Baked Snacks segment was particularly concerning, with segment profit plummeting 72% year-over-year:

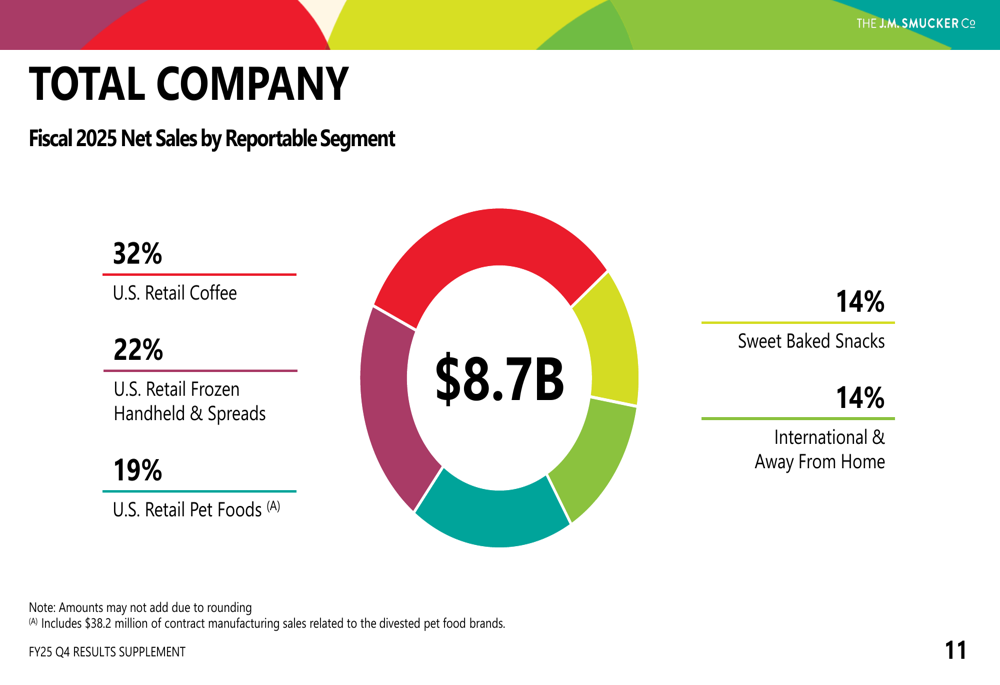

The company’s overall sales mix for fiscal 2025 shows U.S. Retail Coffee as the largest segment at 32% of total sales, followed by U.S. Retail Frozen Handheld & Spreads at 22%, U.S. Retail Pet Foods at 19%, and both Sweet Baked Snacks and International & Away From Home each contributing 14%:

Strategic Initiatives

J.M. Smucker is actively managing its portfolio through strategic divestitures. The company is divesting the Voortman business and certain Sweet Baked Snacks value brands, which accounted for approximately $134.7 million in sales. This move appears to be a response to the underperformance in the Sweet Baked Snacks segment, which has faced challenges since the Hostess acquisition.

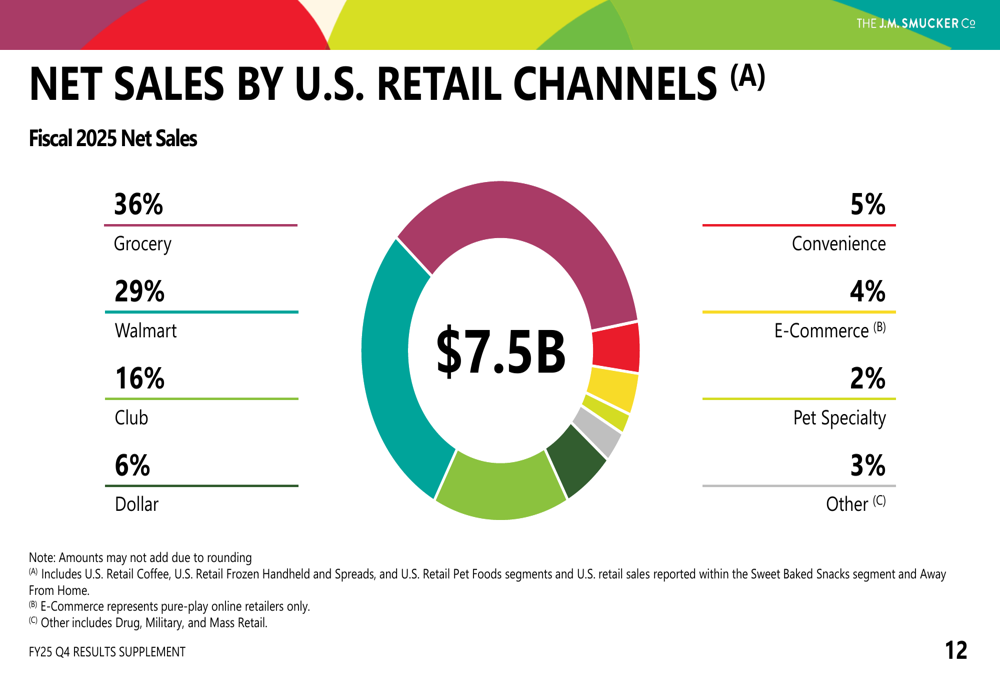

The company’s channel strategy remains focused on traditional grocery (36% of U.S. retail sales) and Walmart (NYSE:WMT) (29%), with growing emphasis on club stores (16%) and e-commerce (4%):

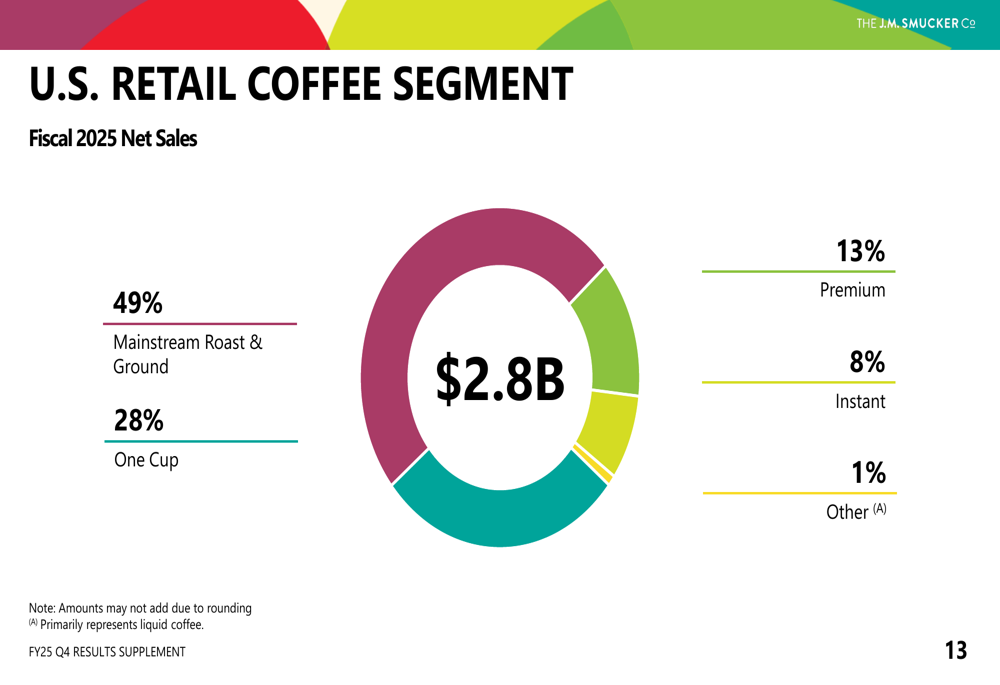

Within the U.S. Retail Coffee segment, which has shown resilience despite record-high coffee prices, mainstream roast and ground products account for nearly half of sales (49%), followed by single-serve coffee pods (28%):

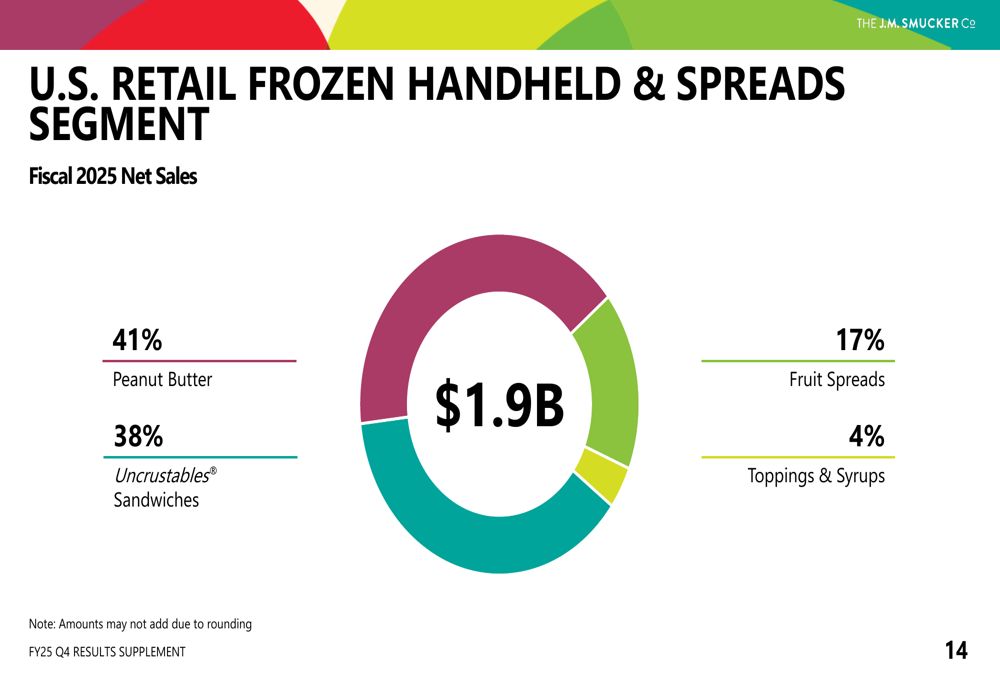

The U.S. Retail Frozen Handheld & Spreads segment, which delivered the strongest growth in Q4, is led by peanut butter (41% of segment sales) and Uncrustables (38%), the latter being a key growth driver for the company:

Forward-Looking Statements

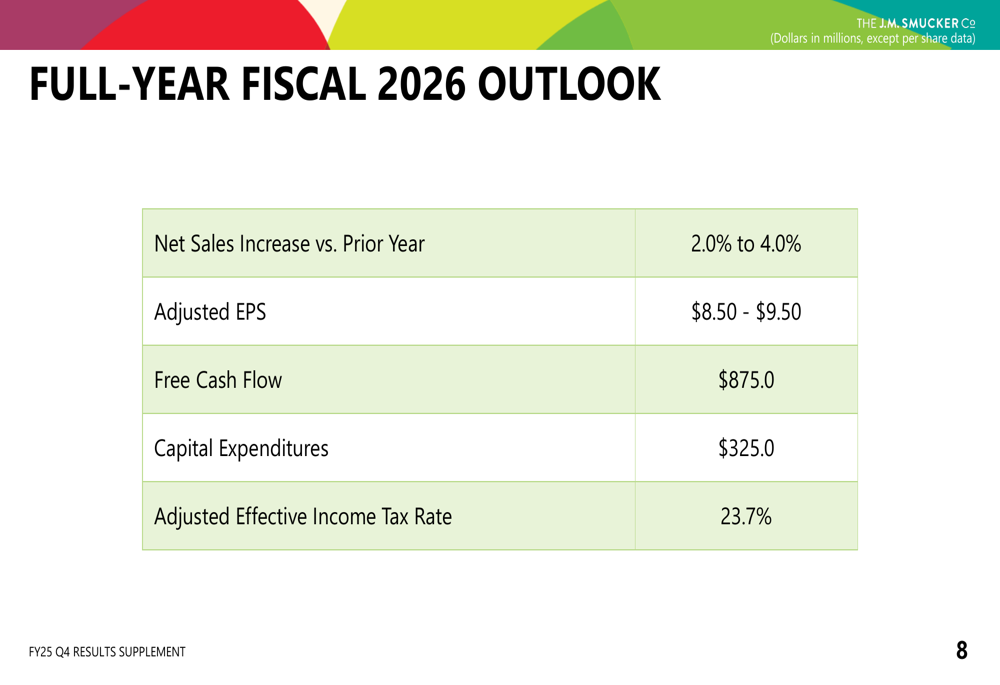

Despite the challenges in Q4, J.M. Smucker provided an optimistic outlook for fiscal 2026, projecting net sales growth of 2-4% compared to fiscal 2025. The company expects adjusted earnings per share in the range of $8.50 to $9.50 and free cash flow of $875 million:

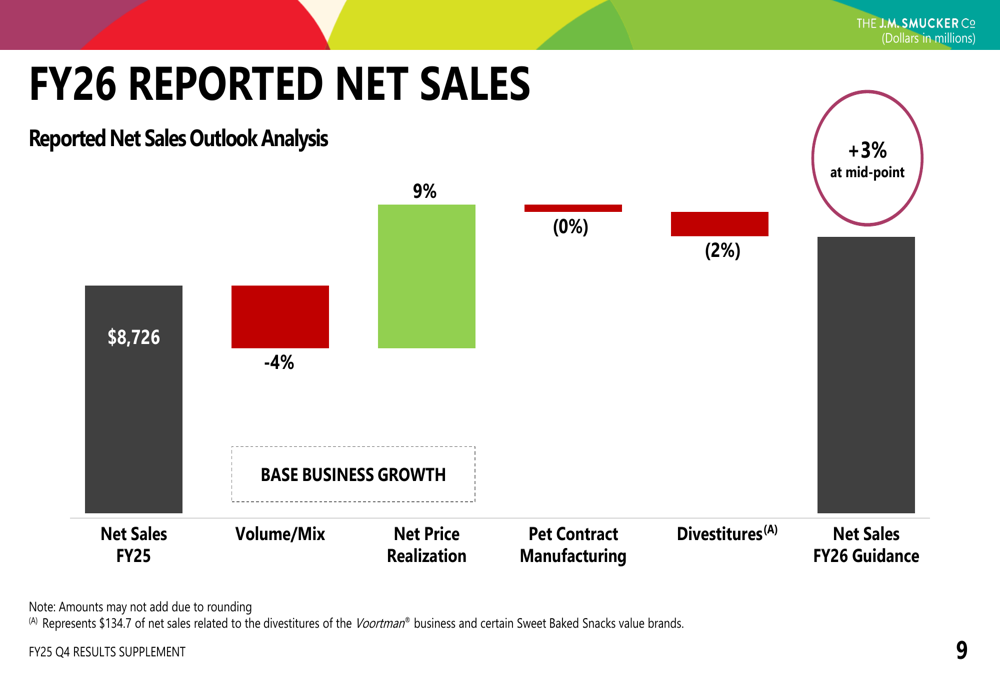

The projected net sales growth for fiscal 2026 is expected to be driven primarily by net price realization (+9%), partially offset by negative volume/mix (-4%) and the impact of divestitures (-2%):

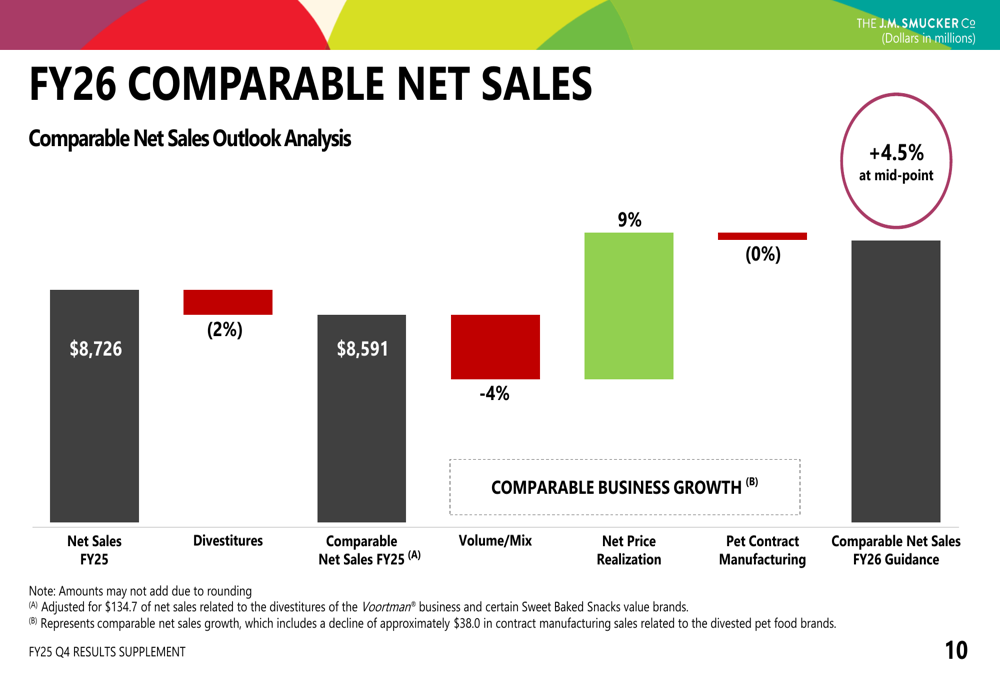

On a comparable basis, excluding the impact of divestitures, the company expects net sales growth of approximately 4.5% at the midpoint of guidance:

This forward guidance comes despite the significant challenges faced in the Sweet Baked Snacks segment and aligns with CEO Mark Smucker’s previous statements expressing confidence in the Hostess acquisition despite the recent impairment charges. The company’s ability to deliver on this optimistic outlook will likely depend on successfully addressing the underperformance in the Sweet Baked Snacks segment while continuing to leverage growth in stronger segments like Frozen Handheld & Spreads.

The market’s negative reaction to the results suggests investors remain cautious about the company’s ability to overcome these challenges, particularly given the significant goodwill impairment charges related to the Hostess acquisition and the continued underperformance of the Sweet Baked Snacks segment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.