Functional Brands closes $8 million private placement and completes Nasdaq listing

Introduction & Market Context

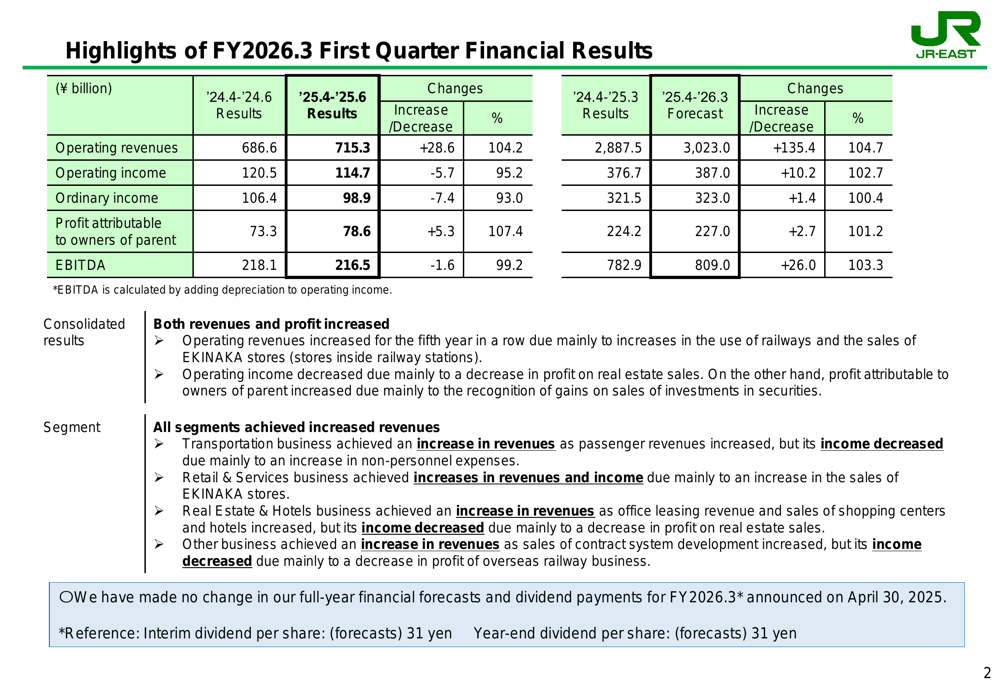

East Japan Railway Co. (9020) released its first quarter FY2026.3 financial results on July 31, 2025, revealing a 4.2% year-over-year revenue increase despite operating income pressure from rising expenses. The company’s stock responded positively to the earnings announcement, rising 4.45% to close at ¥3,756, suggesting investors focused on the revenue growth and maintained full-year guidance rather than the quarterly earnings per share miss.

As shown in the following summary of JR East’s quarterly performance, the company achieved growth across all business segments, with particularly strong results in its core transportation business and retail operations:

Quarterly Performance Highlights

JR East reported consolidated operating revenues of ¥715.3 billion for Q1 FY2026.3, a 4.2% increase from the previous year’s ¥686.6 billion. However, operating income declined 4.8% to ¥114.7 billion, primarily due to increased personnel and maintenance expenses. Profit attributable to owners of parent rose 7.4% to ¥78.6 billion, benefiting from improved non-operating performance.

The company’s earnings per share of ¥60.68 fell short of analyst expectations of ¥71.69, representing a 15.36% miss, despite the revenue slightly exceeding forecasts. JR East maintained its full-year financial forecasts and dividend payment plans, with projected interim and year-end dividends of ¥31 per share each.

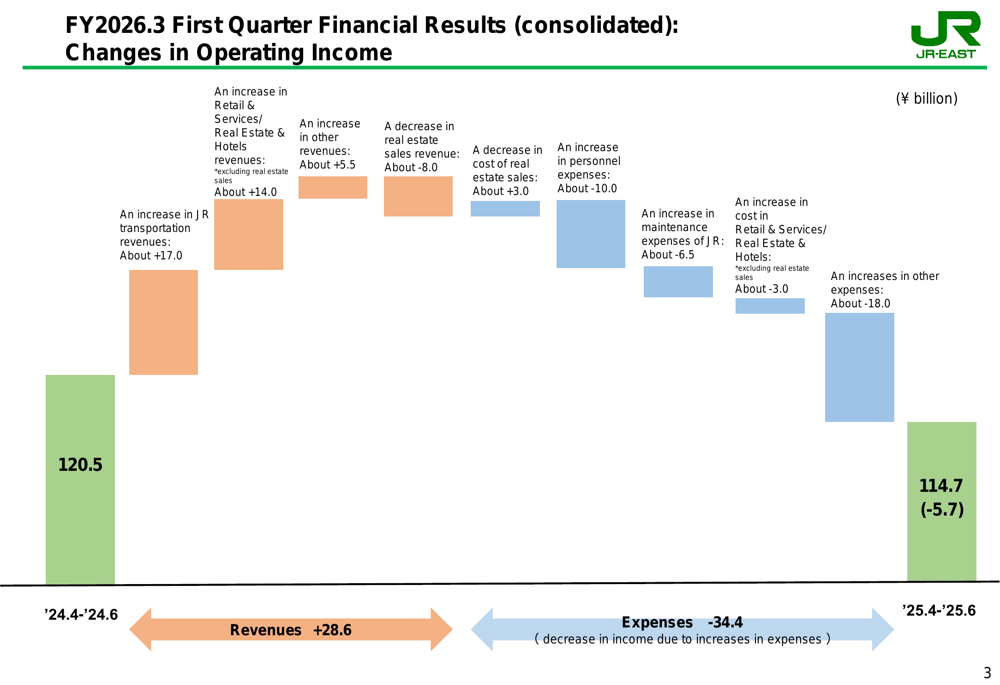

The following waterfall chart illustrates the key factors affecting operating income, with transportation revenue increases offset by higher expenses:

Segment Analysis

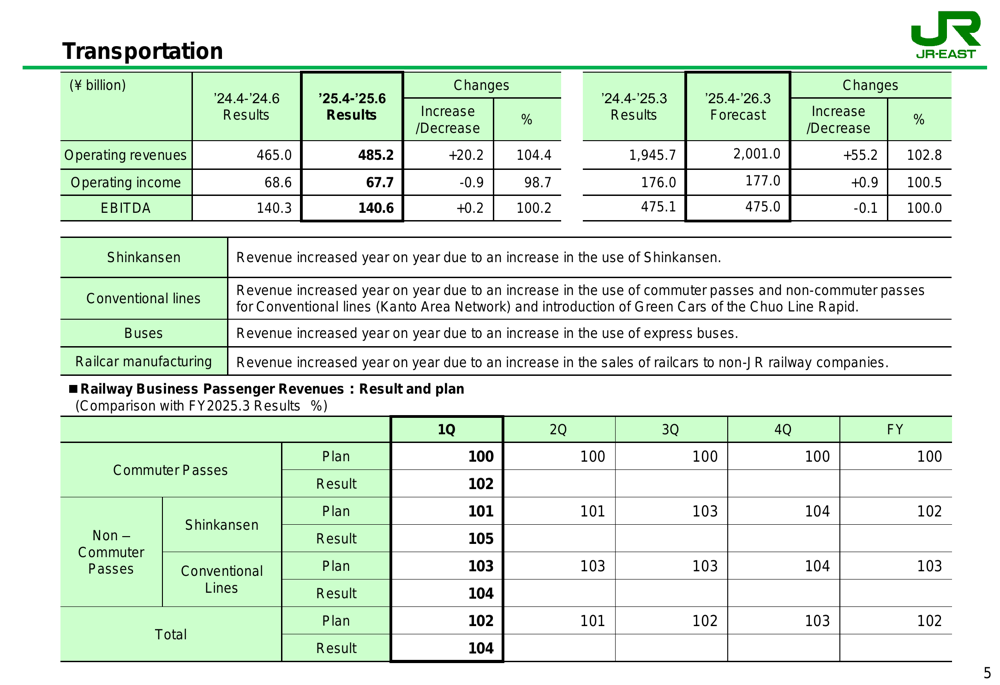

The transportation segment, JR East’s core business, delivered a 4.4% revenue increase to ¥485.2 billion, though operating income slightly decreased by 1.3% to ¥67.7 billion. Shinkansen high-speed rail services were particularly strong, with passenger volume increasing 5.1% and revenues rising 5.5% to ¥140.6 billion, outperforming the company’s quarterly plan.

As shown in the transportation segment results below, commuter pass usage in the Tokyo metropolitan area increased 2% year-over-year, while non-commuter pass usage exceeded plan across both Shinkansen and conventional lines:

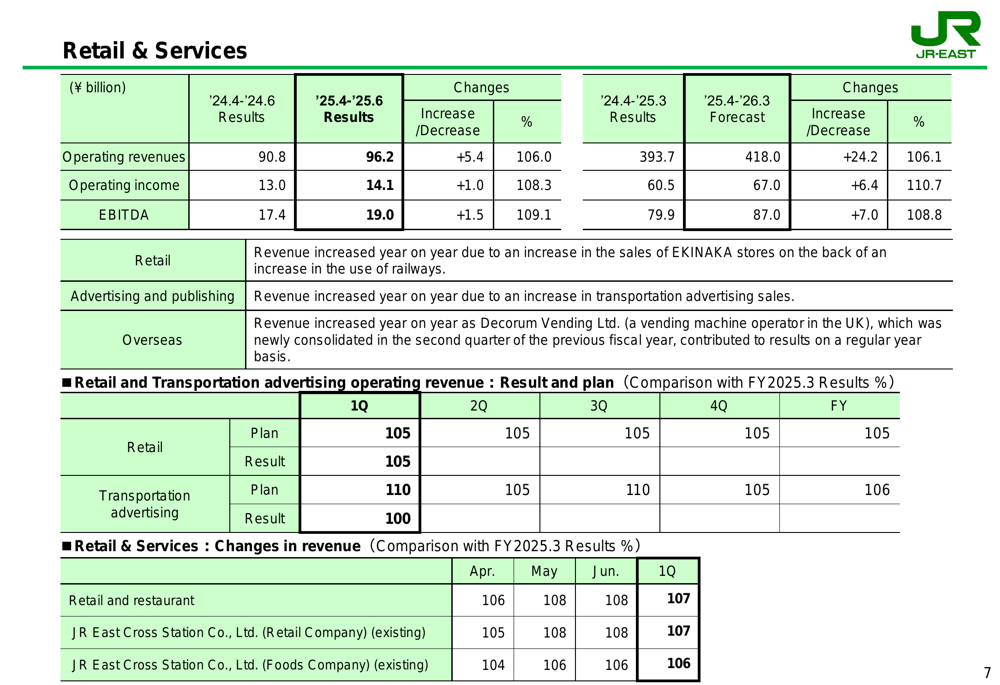

The Retail & Services segment showed robust growth with operating revenues increasing 6.0% to ¥96.2 billion and operating income rising 8.3% to ¥14.1 billion. EBITDA for this segment improved 9.1% to ¥19.0 billion, reflecting strong performance in station retail operations and restaurants, which saw 7% year-over-year growth.

The detailed breakdown of the Retail & Services segment performance demonstrates the strength of JR East’s non-transportation businesses:

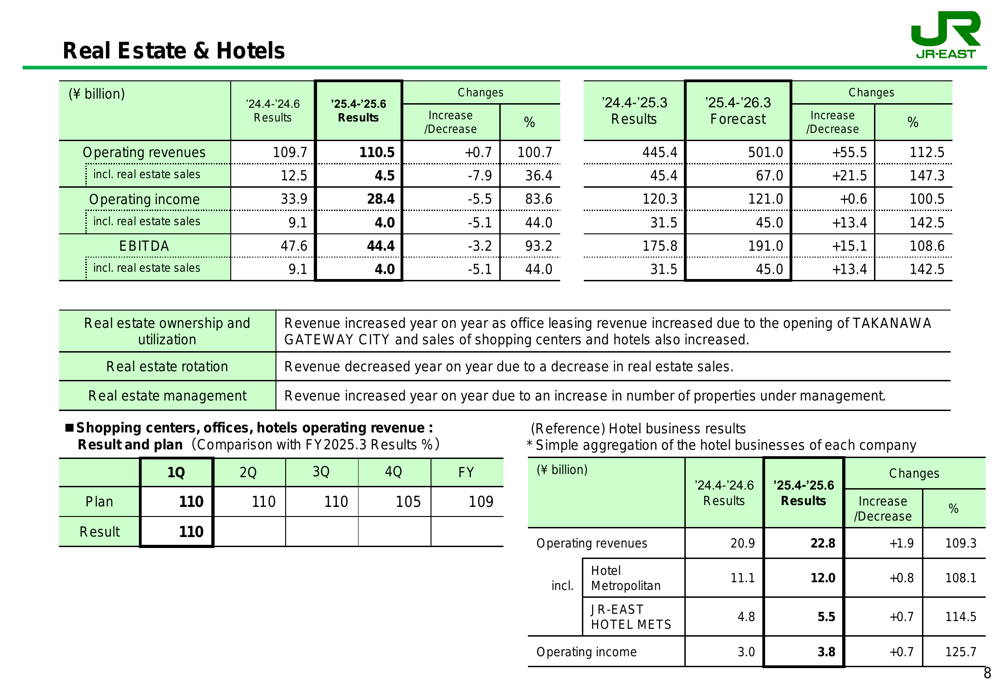

The Real Estate & Hotels segment reported a modest 0.7% increase in operating revenues to ¥110.5 billion, while operating income decreased 16.4% to ¥28.4 billion due to lower real estate sales. However, the hotel business showed impressive results with revenues increasing 9.3% to ¥22.8 billion and operating income surging 25.7% to ¥3.8 billion, driven by strong performance at both Metropolitan Hotels and JR-EAST HOTEL METS properties.

Strategic Initiatives

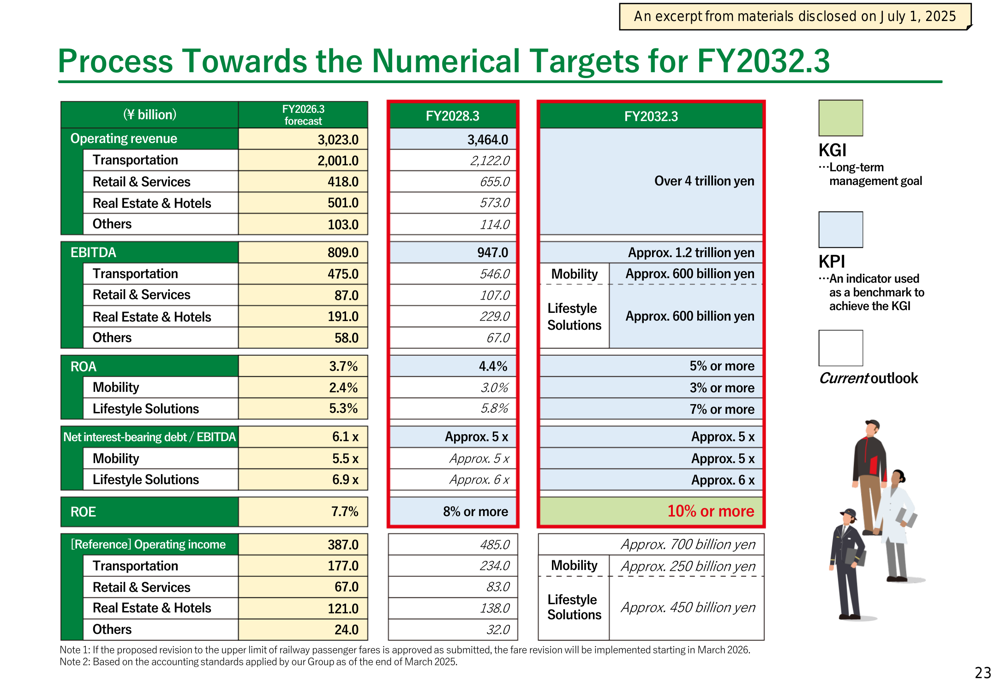

JR East continues to implement its "To the Next Stage 2034" strategy, focusing on dual-axis management centered on Mobility and Lifestyle Solutions. The company aims to achieve ROE of 10% or more by FY2032.3 and exceed ¥4 trillion in operating revenue, up from the current ¥3.02 trillion forecast for FY2026.3.

The following chart illustrates JR East’s projected path toward these ambitious financial targets:

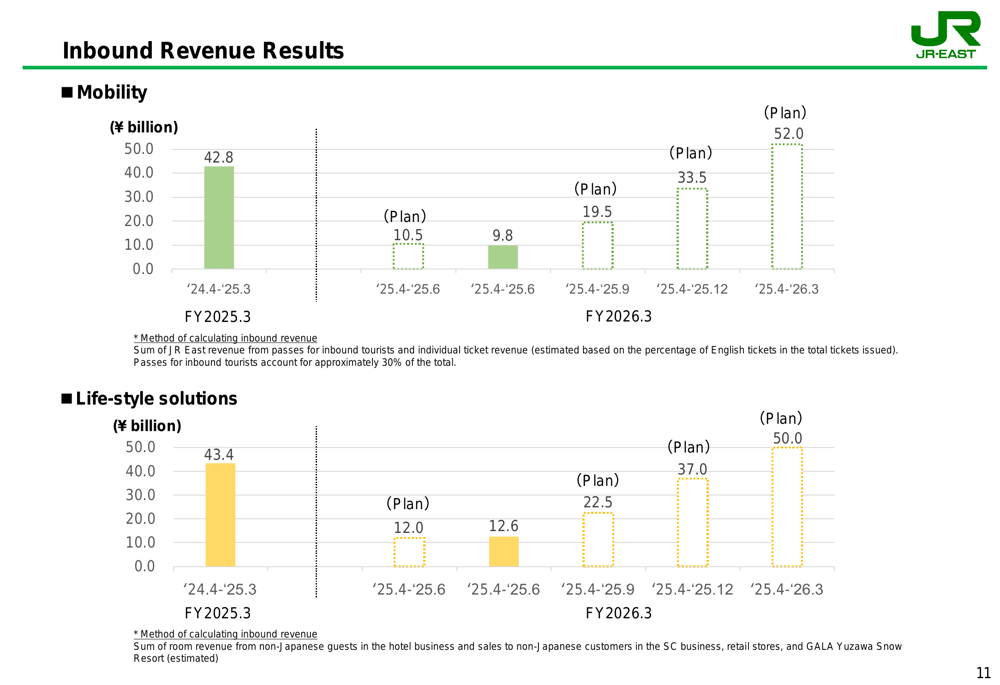

Inbound tourism remains a key growth driver, with the company targeting ¥52 billion in mobility-related inbound revenue and ¥50 billion in lifestyle solutions inbound revenue for FY2026.3. However, Q1 results for mobility-related inbound revenue slightly underperformed at ¥9.8 billion against a plan of ¥10.5 billion, while lifestyle solutions inbound revenue exceeded expectations at ¥12.6 billion versus a plan of ¥12.0 billion.

The company’s inbound revenue performance and targets are visualized in the following chart:

Financial Position and Capital Allocation

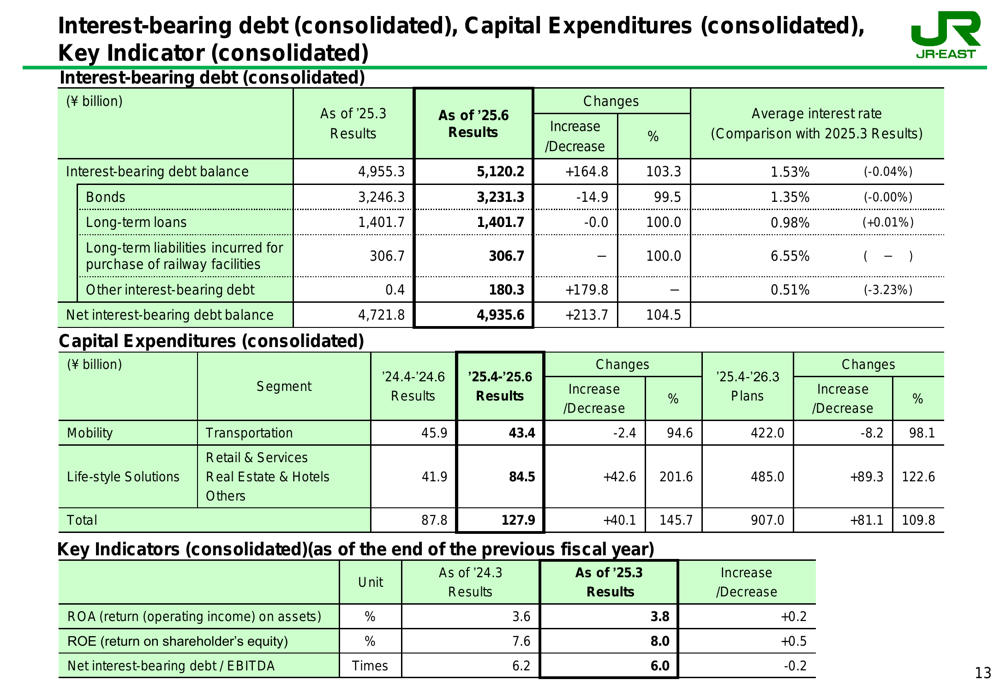

JR East’s interest-bearing debt increased 3.3% to ¥5,120.2 billion as of June 2025, with an average interest rate of 1.53%, down 0.04 percentage points from March 2025. Capital expenditures rose significantly by 45.7% to ¥127.9 billion, with particularly strong growth in the Life-style Solutions segment, where investments more than doubled to ¥84.5 billion.

The company’s financial position and capital expenditure breakdown are detailed in the following table:

JR East plans to gradually increase its dividend payout ratio to 40% by FY2028.3 as growth investments such as the TAKANAWA GATEWAY CITY development project stabilize. For FY2026.3, the company has maintained its dividend forecast of ¥62 per share, split equally between interim and year-end payments.

Forward-Looking Statements

Despite the mixed Q1 results, JR East has maintained its full-year FY2026.3 forecasts, projecting operating revenues of ¥3,023.0 billion (up 4.7% year-over-year), operating income of ¥387.0 billion (up 2.7%), and profit attributable to owners of parent of ¥227.0 billion (up 1.2%).

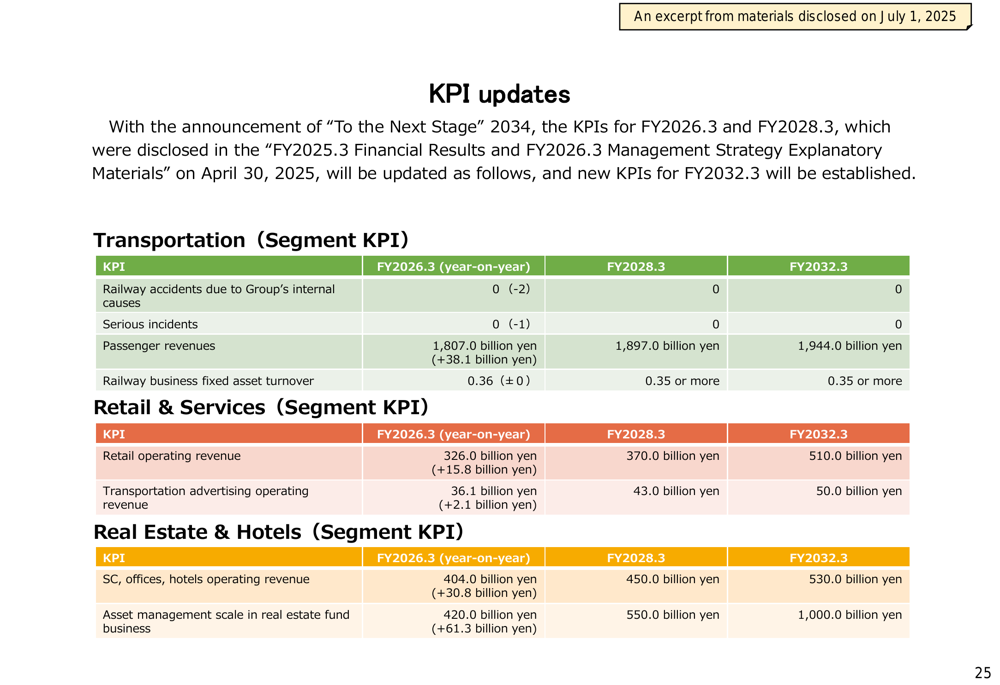

The company has established several key performance indicators to track progress toward its long-term goals, including railway safety, retail revenue growth, and digital transformation metrics:

JR East faces several challenges, including rising maintenance and personnel expenses that pressured Q1 operating income. The company noted that personnel expenses increased by approximately ¥10 billion due to salary adjustments, while maintenance expenses rose by about ¥6.5 billion. Additionally, earthquake rumors pose a potential threat to inbound tourism, which has become an increasingly important revenue source.

Despite these challenges, JR East’s continued revenue growth across all segments and strong performance in Shinkansen and hotel operations suggest the company is making progress on its strategic initiatives while navigating cost pressures in a post-pandemic operating environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.