Boeing launches virtual pilot training platform

Introduction & Market Context

Juniper Networks (NYSE:JNPR) released its Q1 2025 investor presentation on May 1, 2025, revealing a mixed financial picture with strong year-over-year improvements but sequential declines from the previous quarter. The networking equipment provider, currently trading at $36.56 (as of June 24, 2025), sits comfortably within its 52-week range of $33.42 to $39.79.

The presentation highlights Juniper’s continued recovery from the challenging market conditions of early 2024, with significant year-over-year revenue growth despite the typical seasonal slowdown in the first quarter. The company’s improved cash position and steady free cash flow generation suggest underlying financial stability amid ongoing industry transformation.

Quarterly Performance Highlights

Juniper reported Q1 2025 revenue of $1,280 million, representing an 11.4% increase from Q1 2024 ($1,149 million), though down 8.8% sequentially from Q4 2024 ($1,404 million). This pattern reflects both the company’s recovery trajectory and typical seasonal patterns in the networking equipment market.

Non-GAAP earnings per share for Q1 2025 reached $0.43, showing substantial improvement from $0.29 in Q1 2024 (up 48.3% year-over-year), but declining from $0.64 in Q4 2024. This quarterly revenue and earnings trend can be clearly observed in the following chart:

The chart illustrates Juniper’s performance over the past ten quarters, showing the company’s gradual recovery from the revenue and earnings trough experienced in early 2024. While Q1 2025 shows the typical seasonal decline from Q4, the year-over-year comparison demonstrates meaningful improvement in both revenue and profitability.

Detailed Financial Analysis

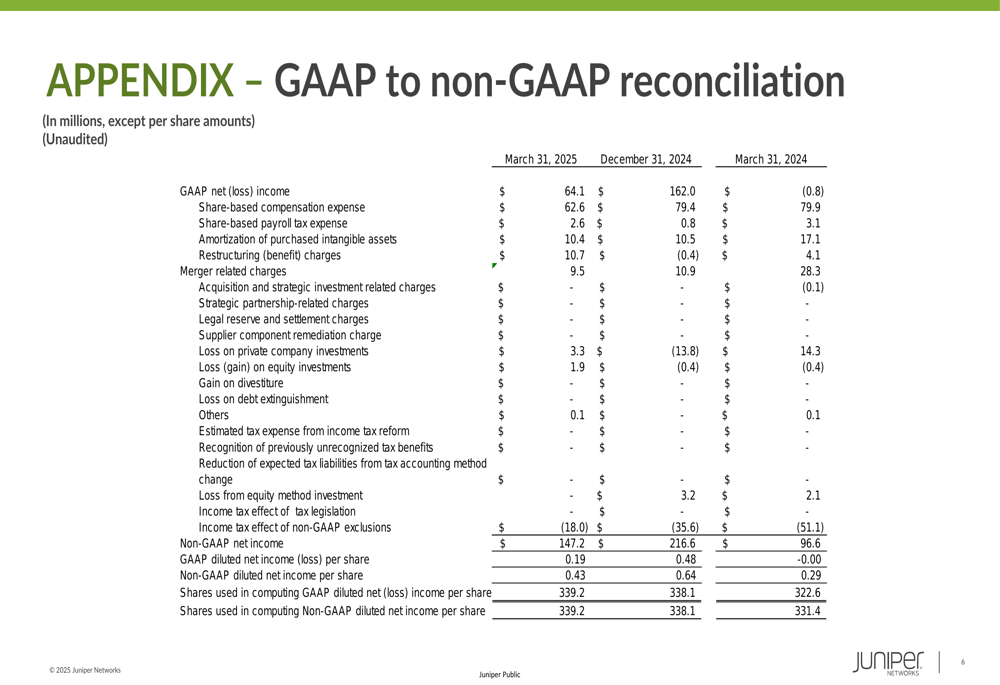

Juniper’s Q1 2025 financial results reveal significant differences between GAAP and non-GAAP metrics. The company reported GAAP net income of $64.1 million ($0.19 per diluted share) for Q1 2025, compared to a GAAP net loss of $0.8 million in Q1 2024, representing a substantial year-over-year improvement.

On a non-GAAP basis, which excludes share-based compensation, amortization of purchased intangible assets, restructuring charges, and related tax effects, Juniper reported net income of $147.2 million ($0.43 per diluted share) for Q1 2025, up from $96.6 million ($0.29 per diluted share) in Q1 2024.

The reconciliation between GAAP and non-GAAP results provides important context for understanding Juniper’s underlying operational performance:

The largest adjustments between GAAP and non-GAAP results come from share-based compensation expense ($53.9 million) and amortization of purchased intangible assets ($31.8 million), highlighting the significant impact of these non-cash expenses on reported earnings.

Balance Sheet Strength

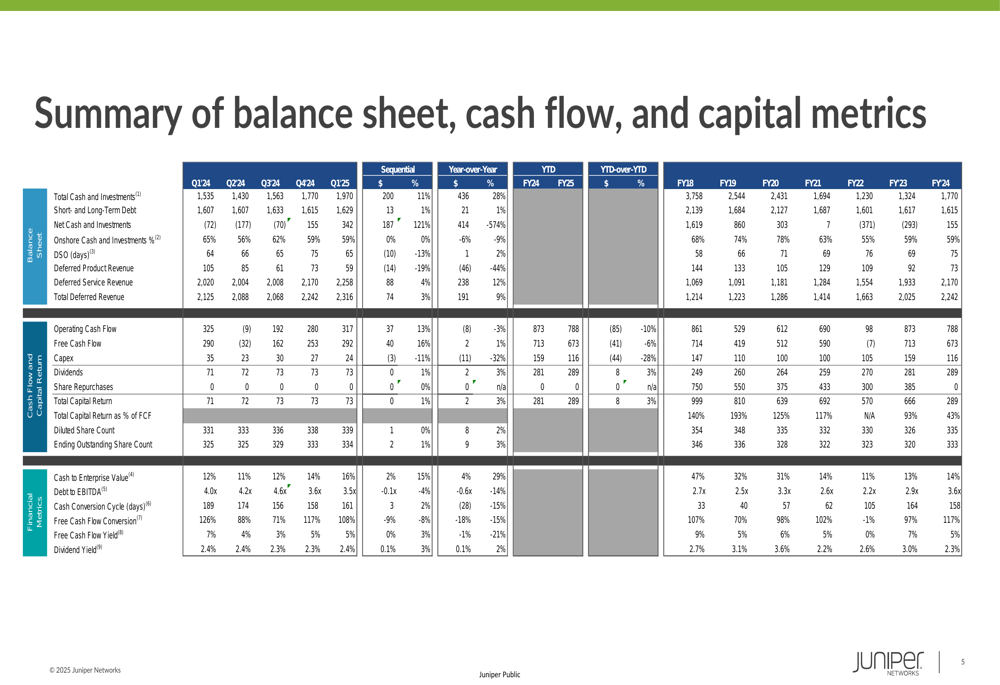

One of the most notable improvements in Juniper’s financial position is its strengthened balance sheet. As of Q1 2025, the company reported total cash and investments of $1,970 million, up from $1,535 million in Q1 2024. More significantly, Juniper has shifted from a net debt position of $72 million in Q1 2024 to a net cash position of $342 million in Q1 2025.

The company’s cash flow metrics remain solid, with Q1 2025 operating cash flow of $317 million (slightly down from $325 million in Q1 2024) and free cash flow of $292 million (marginally up from $290 million in Q1 2024). These figures suggest Juniper maintains strong cash generation capabilities despite market fluctuations.

The following table provides a comprehensive overview of Juniper’s balance sheet, cash flow, and capital metrics:

The table reveals several positive trends, including improved cash position, stable cash flow generation, and consistent shareholder returns through dividends and share repurchases. The company’s days sales outstanding (DSO) remained relatively stable at 65 days in Q1 2025 compared to 64 days in Q1 2024, indicating consistent operational efficiency in accounts receivable management.

Forward-Looking Statements

While specific forward guidance was not detailed in the presentation slides, Juniper included standard forward-looking statements and disclaimers noting that future results could be affected by various factors including economic conditions, supply chain issues, and regulatory changes. The company also referenced the ongoing impact of COVID-19 as a potential factor that could affect future performance.

Investors should note that Juniper’s presentation includes the standard cautions about non-GAAP financial measures and statements of product direction (SOPD). The company explicitly states that SOPD information is subject to change and should not be relied upon for purchasing decisions, highlighting the inherent uncertainty in forward-looking product roadmaps.

The overall presentation suggests Juniper is maintaining its recovery trajectory while navigating seasonal patterns and ongoing industry challenges. The improved year-over-year performance and strengthened balance sheet provide a solid foundation for the company’s operations throughout 2025, though sequential quarterly comparisons indicate the typical cyclicality of the networking equipment market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.