Street Calls of the Week

Introduction & Market Context

Jyske Bank A/S (CPH:JYSK) shares jumped 6.27% on Wednesday after the Danish lender presented its Q1 2025 results, showing resilient earnings despite a challenging interest rate environment. The stock closed at 584.5 DKK, approaching its 52-week high of 598.5 DKK, as investors responded positively to the bank’s ability to maintain growth momentum through diversified revenue streams.

The Q1 presentation revealed that Jyske Bank has successfully navigated lower Danish policy rates by leveraging strong fee income growth and maintaining disciplined cost management. This performance comes as Denmark positions itself to handle potential economic impacts from escalating global trade tensions.

Quarterly Performance Highlights

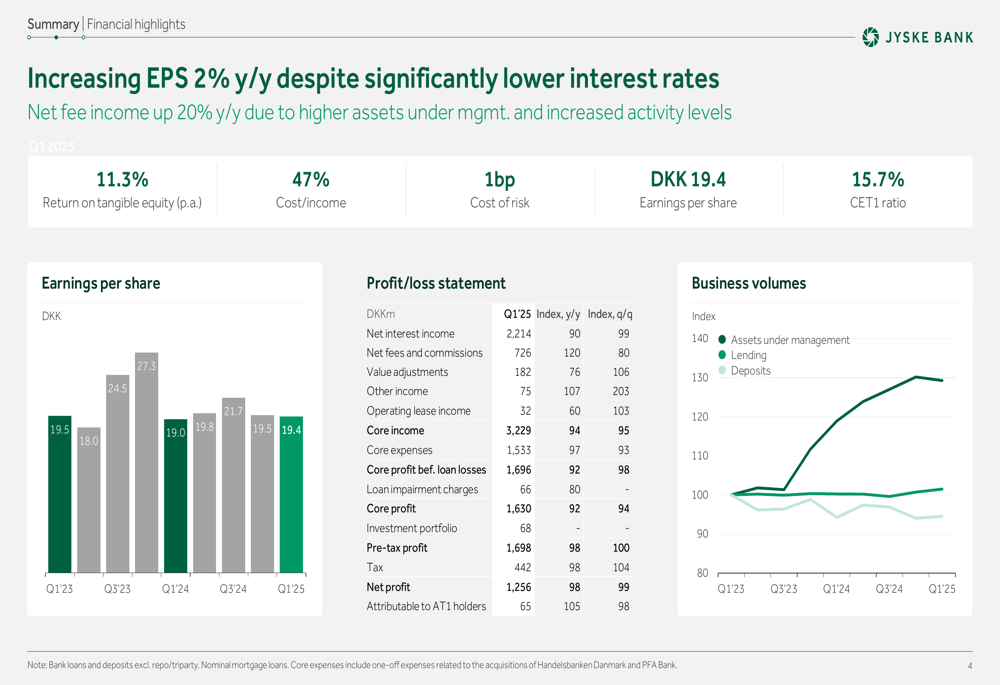

Jyske Bank reported a 2% year-over-year increase in earnings per share for Q1 2025, reaching DKK 19.4 despite facing headwinds from a 1.5 percentage point lower Danish policy rate compared to the same period last year. This resilience was largely driven by fee income, which surged 20% year-over-year to reach its highest Q1 level on record.

As shown in the following financial highlights chart, the bank maintained strong profitability metrics with a return on tangible equity of 11.3% and a cost-to-income ratio of 47%:

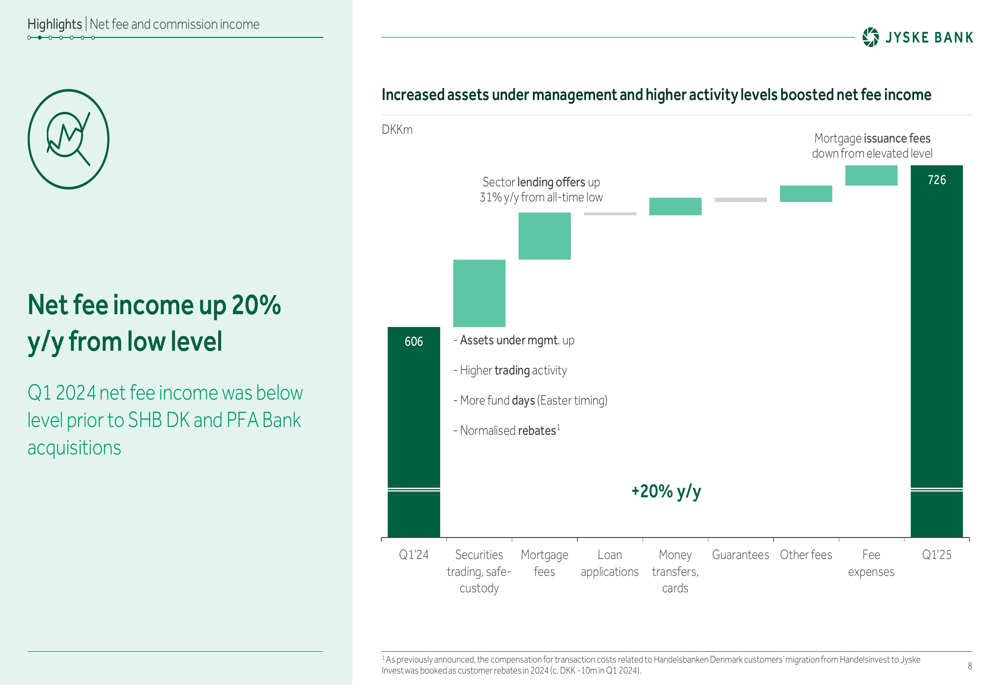

The impressive fee income growth stemmed from multiple sources, with sector lending offers up 31% year-over-year from previously low levels. Other significant contributors included increased assets under management, higher trading activity, and normalized customer rebates following the completion of integration activities related to previous acquisitions.

The following breakdown illustrates the key drivers behind the net fee income growth from DKK 606 million in Q1 2024 to DKK 726 million in Q1 2025:

Customer Satisfaction & Business Growth

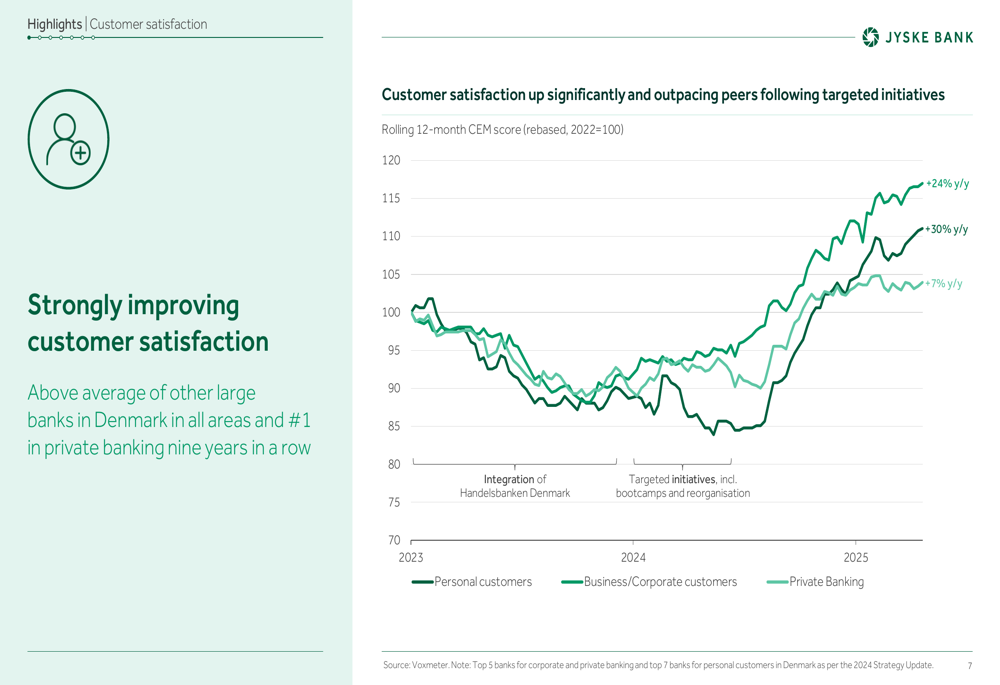

A standout element of Jyske Bank’s Q1 presentation was the significant improvement in customer satisfaction across all segments. The bank reported year-over-year increases of 24% for Private Banking clients, 30% for Business/Corporate customers, and 7% for Personal customers.

These improvements have positioned Jyske Bank above the industry average in Denmark across all customer segments, with its Private Banking service maintaining the #1 position for nine consecutive years. The following chart demonstrates this positive trajectory:

The enhanced customer satisfaction appears to be translating into business growth, with the bank reporting positive trends in both lending and assets under management. This performance suggests that Jyske Bank’s strategic focus on customer experience is yielding tangible financial benefits.

Capital Position & Risk Management

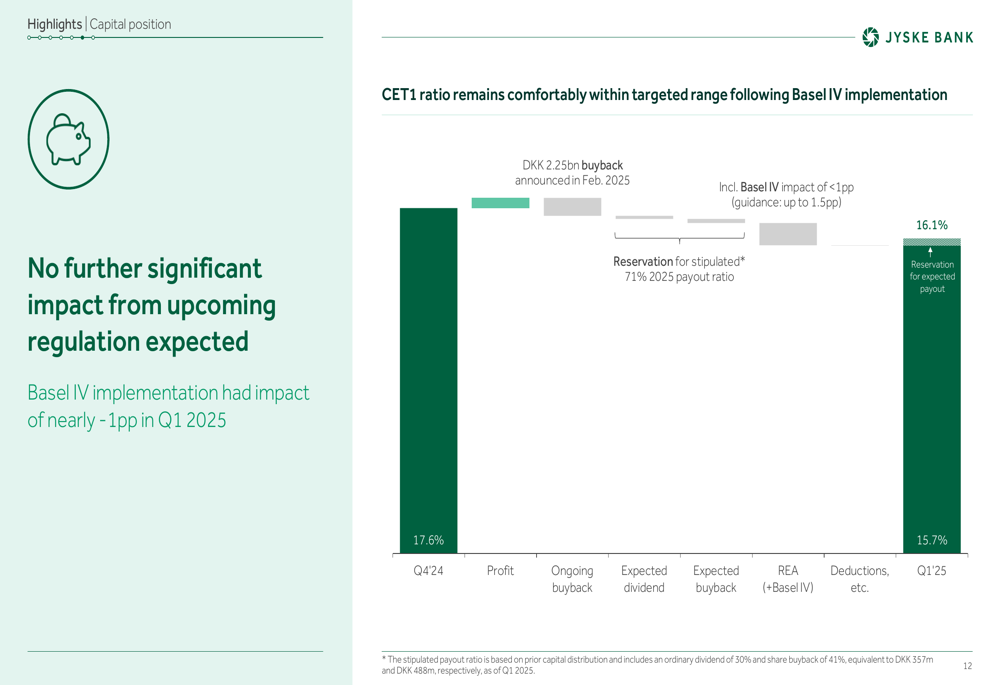

Jyske Bank’s capital position remains solid despite the implementation of Basel IV regulations in Q1 2025, which had an impact of nearly 1 percentage point on the bank’s CET1 ratio. The ratio stood at 15.7% at quarter-end, down from 17.6% in Q4 2024 but still within the bank’s target range.

The following chart details the factors affecting the CET1 ratio during the quarter:

On the risk management front, Jyske Bank increased its post-model adjustments by DKK 0.1 billion in Q1 to reflect potential impacts from trade war scenarios. The bank emphasized that its buffer for macroeconomic risks now exceeds four times the accumulated loan impairment charges of the last decade, demonstrating a conservative approach to credit risk.

The bank also addressed concerns about trade tensions, noting that Denmark has limited direct exposure to US tariffs, with only 3% of Danish exports directly affected by the implemented 10% US tariff. Early observations from Q2 2025 showed higher deposits due to seasonality, no significant changes to credit demand in April, positive value adjustments, and only a modest decline in assets under management.

Forward-Looking Statements

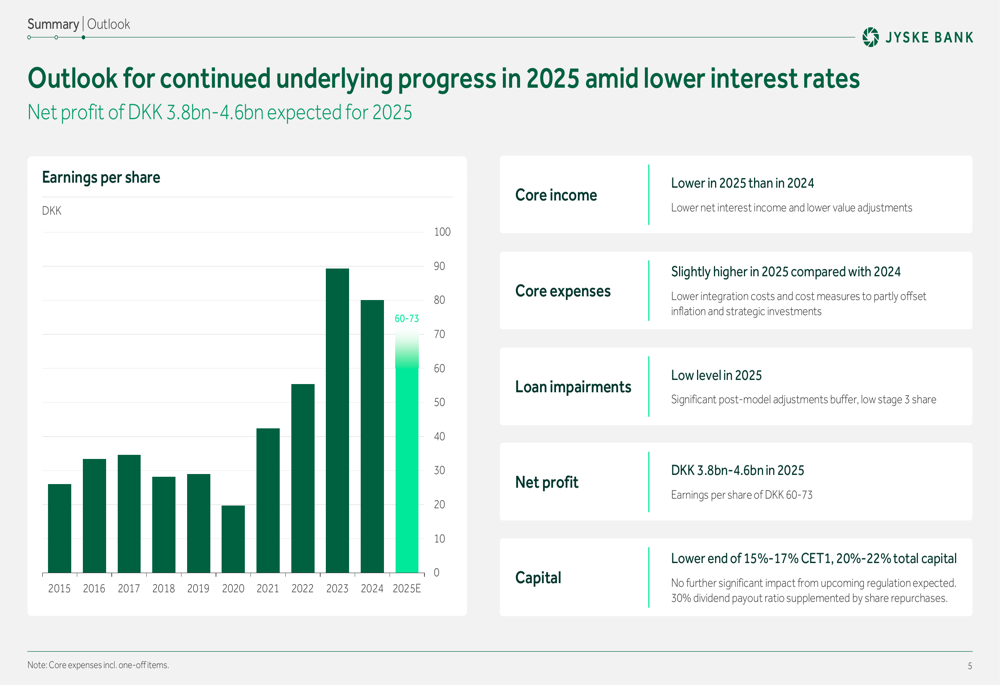

Looking ahead to the full year 2025, Jyske Bank maintained its net profit guidance of DKK 3.8-4.6 billion, translating to earnings per share of DKK 60-73. This outlook factors in expectations for lower core income compared to 2024, primarily due to reduced net interest income and lower value adjustments.

The bank projects slightly higher core expenses in 2025 compared to 2024, as inflation and strategic investments will be partially offset by lower integration costs and other cost measures. Loan impairments are expected to remain at a low level, supported by the significant buffer of post-model adjustments and a low stage 3 share.

As shown in the following outlook chart, Jyske Bank’s projected 2025 earnings per share would continue the positive long-term trend despite near-term interest rate pressures:

Capital distribution plans include maintaining the CET1 ratio at the lower end of the 15%-17% target range, with a 30% dividend payout ratio supplemented by share repurchases. The bank has already announced a DKK 2.25 billion buyback program in February 2025, demonstrating confidence in its financial position and commitment to shareholder returns.

With its diversified revenue streams, improving customer satisfaction metrics, and prudent approach to risk management, Jyske Bank appears well-positioned to navigate the challenging interest rate environment and potential macroeconomic headwinds in 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.