These are top 10 stocks traded on the Robinhood UK platform in July

Kaiser Aluminum Corporation (NASDAQ:KALU) reported strong first-quarter 2025 results during its earnings presentation on April 24, 2025, highlighted by a 35% year-over-year increase in EBITDA and improved margins that prompted management to raise full-year guidance. Despite these positive results, the company’s stock was down 8.18% in premarket trading, suggesting investors may have concerns about certain aspects of the outlook.

Quarterly Performance Highlights

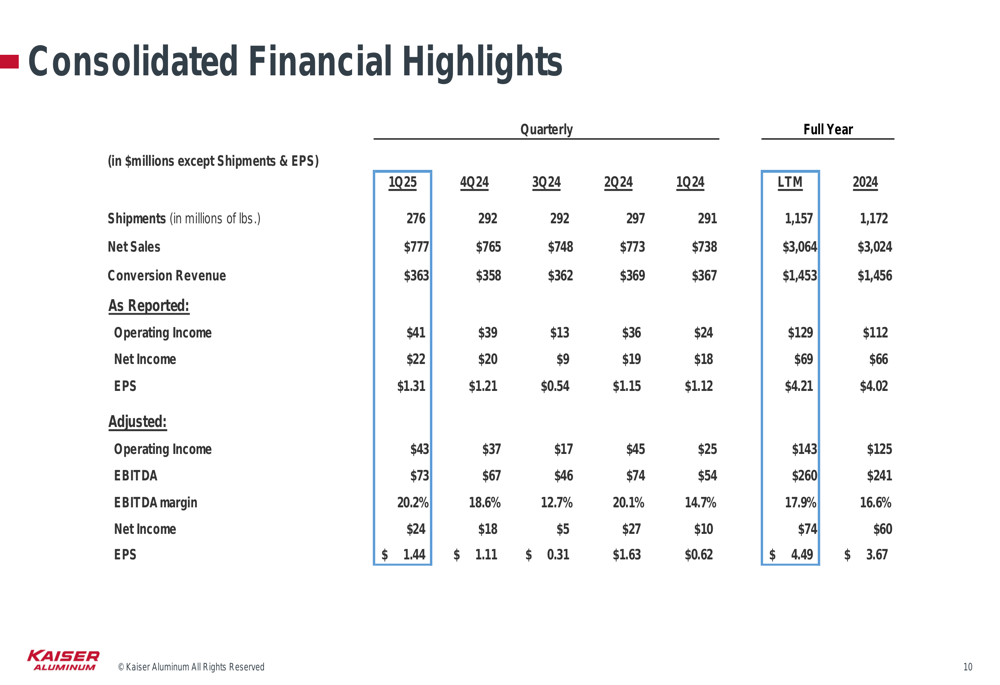

Kaiser Aluminum delivered robust financial performance in Q1 2025, with EBITDA reaching $73 million, up significantly from $54 million in the same period last year. The EBITDA margin expanded to 20.2%, compared to 14.7% in Q1 2024, reflecting improved pricing, favorable product mix, and effective cost management.

"Strong 1Q 2025 Financial Results; Raising Full Year Expectations," noted Chairman, President & CEO Keith Harvey in the presentation, citing operations and end market performance meeting expectations, with additional benefits from "positive tailwind from rapid metal price changes through the quarter."

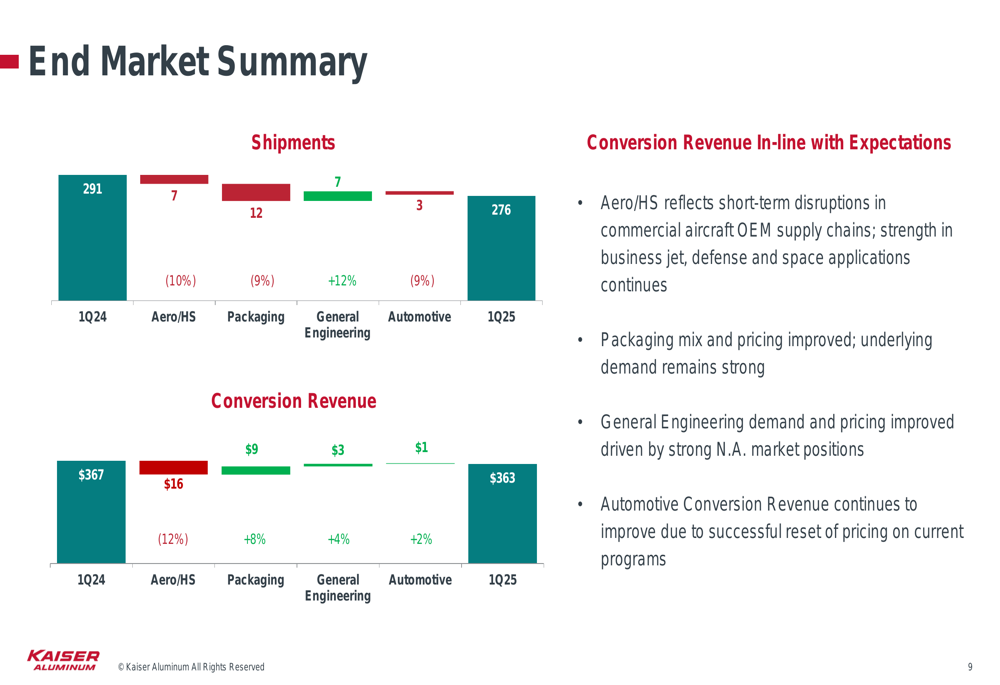

As shown in the following chart of end market performance, shipments decreased slightly to 276 million pounds from 291 million pounds in Q1 2024, while conversion revenue remained relatively stable at $363 million compared to $367 million in the prior-year period:

The company reported net income of $22 million, or $1.31 per diluted share, up from $18 million, or $1.12 per share, in Q1 2024. Adjusted net income, which excludes non-run-rate items, was $24 million, or $1.44 per share, more than double the $0.62 per share reported in Q1 2024.

The consolidated financial highlights demonstrate consistent improvement in profitability metrics over recent quarters:

Detailed Financial Analysis

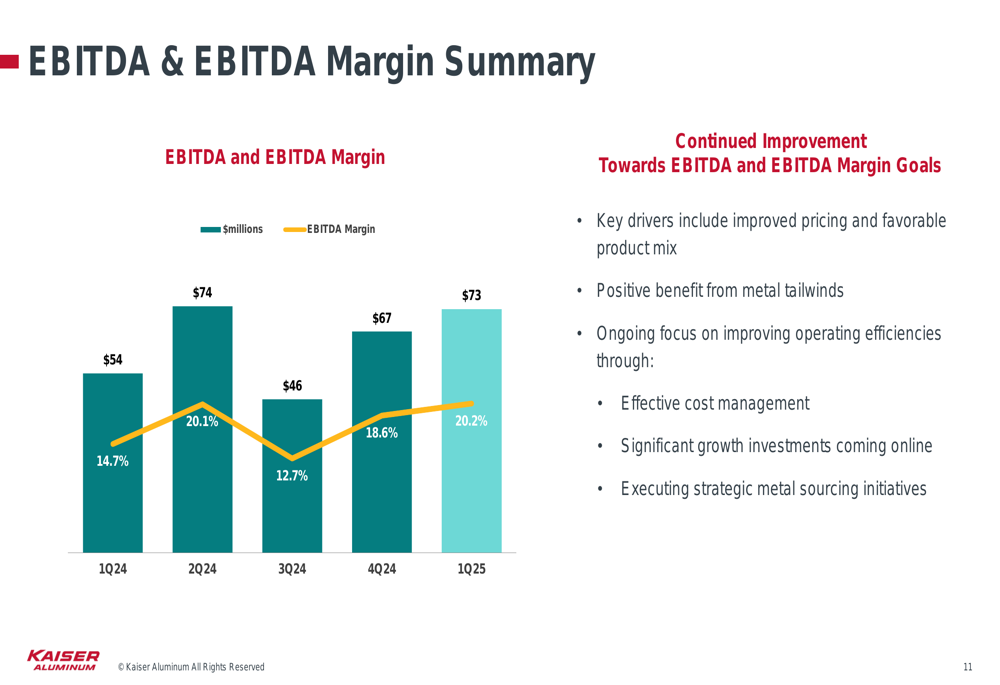

Kaiser’s EBITDA performance has shown a positive trajectory over the past five quarters, with Q1 2025 representing the second-highest quarterly EBITDA in this period. The EBITDA margin has also improved significantly, reaching 20.2% in Q1 2025.

The following chart illustrates the company’s EBITDA and margin progression:

Executive Vice President & CFO Neal West presented the financial results, highlighting that key drivers for the continued improvement include "improved pricing and favorable product mix," "positive benefit from metal tailwinds," and "ongoing focus on improving operating efficiencies through effective cost management."

Segment performance was mixed across Kaiser’s end markets. The Aerospace/High Strength segment, which represents the largest portion of conversion revenue, saw a 10% decrease in shipments and a 12% decrease in conversion revenue compared to Q1 2024. The company attributed this to "short-term disruptions" in the supply chain.

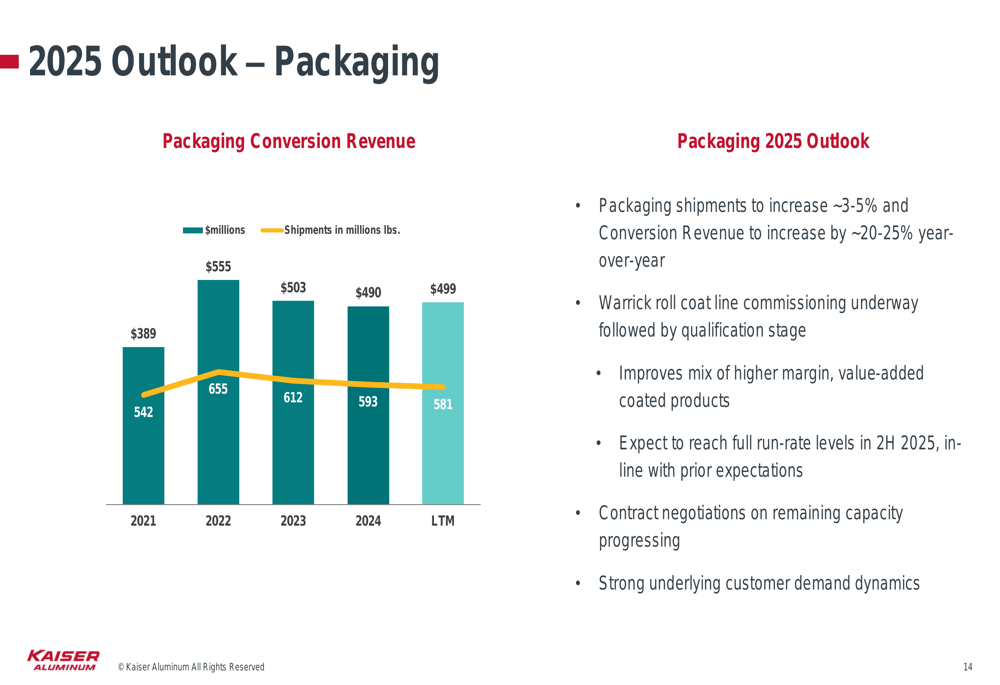

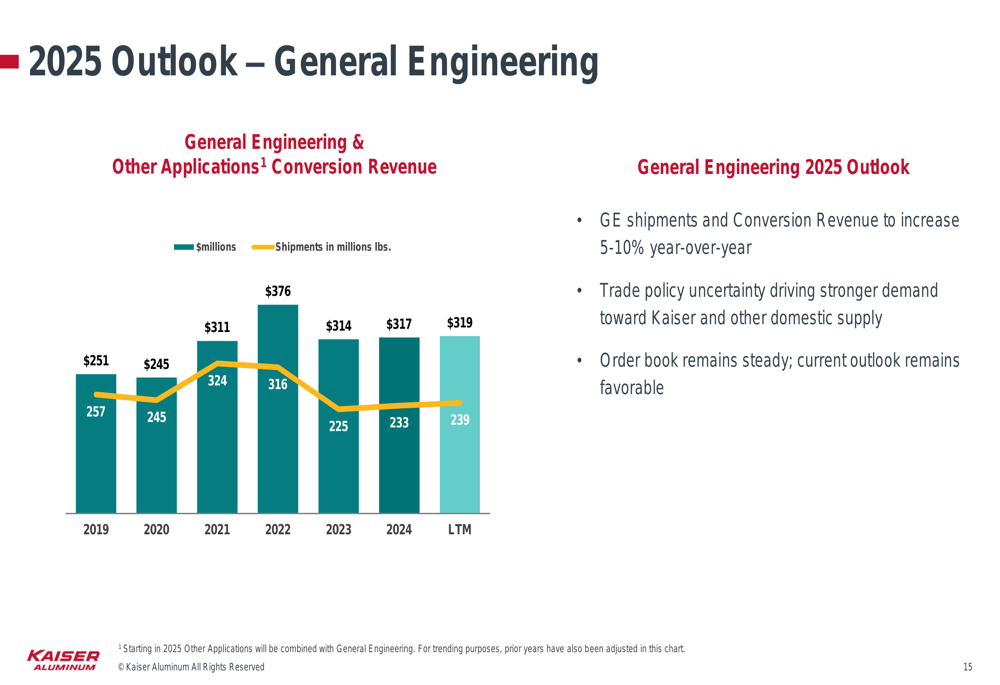

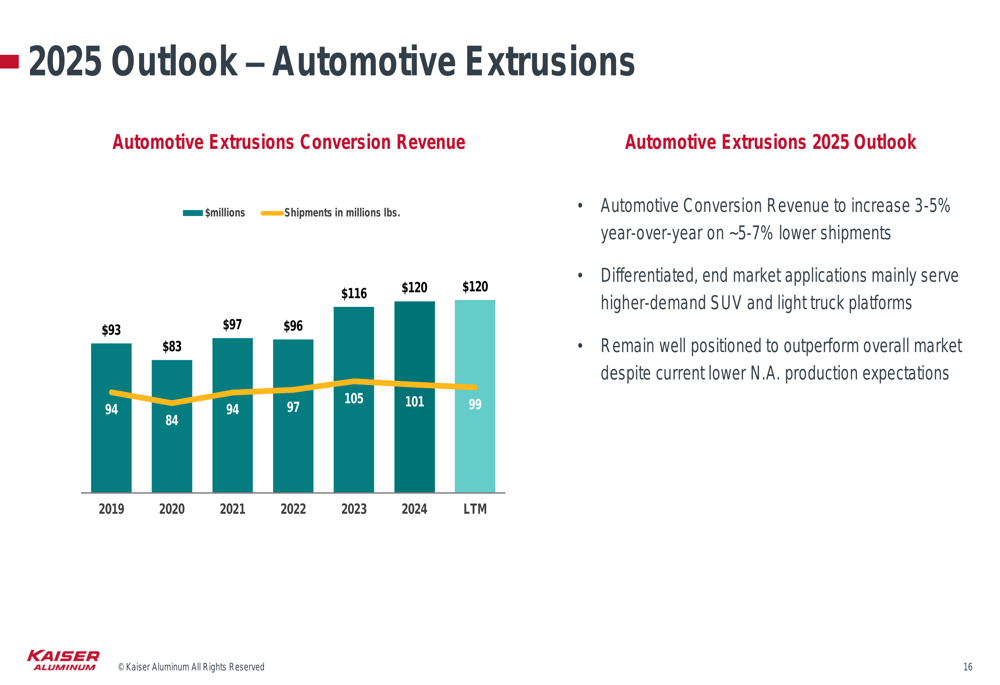

In contrast, the Packaging (NYSE:PKG) segment showed strong growth with a 9% increase in shipments and an 8% increase in conversion revenue. General Engineering shipments increased by 12% with a 4% rise in conversion revenue, while Automotive shipments decreased by 9% but conversion revenue increased by 2%.

Strategic Initiatives

Kaiser Aluminum is nearing completion of significant growth capital projects that are expected to drive future performance. The Warrick roll coat line is currently in the commissioning phase, with customer qualifications pending. This investment is designed to improve the mix of higher-margin, value-added coated products in the Packaging segment.

Additionally, the Trentwood Phase VII project remains on track for completion in the second half of 2025. These investments are expected to differentiate Kaiser’s market position for superior quality products and drive a "step-change in EBITDA and EBITDA margin performance," according to the presentation.

Forward-Looking Statements

Kaiser Aluminum raised its full-year 2025 outlook, now expecting consolidated EBITDA to increase by 5-10% year-over-year. The company also projects consolidated conversion revenue to grow by 5-10% compared to 2024.

The following chart summarizes the company’s 2025 outlook:

By segment, Kaiser provided the following outlook for 2025:

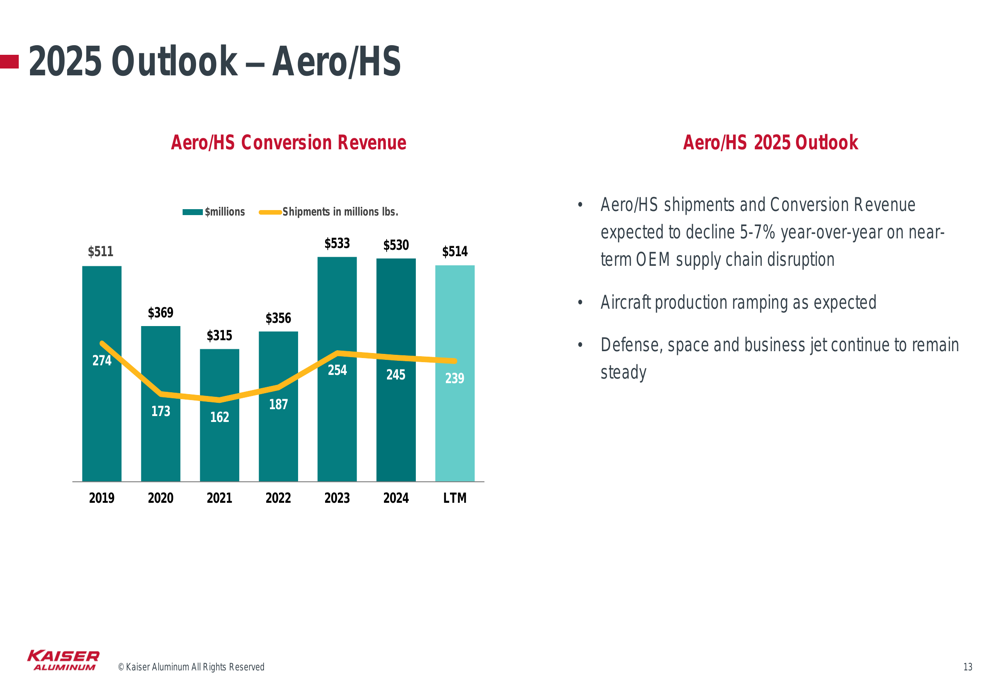

Aerospace/High Strength: Shipments and conversion revenue expected to decline 5-7% year-over-year due to near-term OEM supply chain disruption, though aircraft production is ramping as expected, and defense, space, and business jet markets remain steady.

Packaging: Shipments projected to increase 3-5% and conversion revenue to grow 20-25% year-over-year, with the Warrick roll coat line expected to reach full run-rate levels in the second half of 2025.

General Engineering: Both shipments and conversion revenue forecast to increase 5-10% year-over-year, with trade policy uncertainty driving stronger demand toward domestic suppliers.

Automotive Extrusions: Conversion revenue expected to increase 3-5% year-over-year despite 5-7% lower shipments, as the company focuses on "differentiated, end market applications mainly serving higher-demand SUV and light truck platforms."

Capital expenditures for 2025 are expected to be in the range of $120-130 million, with free cash flow projected to exceed $100 million. The company anticipates its balance sheet will strengthen throughout the year with a "continued steady pace of deleveraging."

Despite the positive results and outlook, Kaiser Aluminum’s stock was trading down significantly in premarket trading. This market reaction may reflect concerns about the projected decline in the Aerospace/High Strength segment, which has historically been a key driver of the company’s performance, or broader market concerns about aluminum demand and pricing.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.