Can anything shut down the Gold rally?

Introduction & Market Context

Kaiser Aluminum Corporation (NASDAQ:KALU) presented its second quarter 2025 earnings results on July 24, 2025, highlighting improved financial performance and strategic positioning despite ongoing challenges in certain market segments. The company’s stock closed at $92.43 prior to the earnings release, representing a significant recovery from its 52-week low of $46.81 and approaching its 52-week high of $96.43.

Following a first quarter that saw an impressive EPS beat but revenue miss, Kaiser’s Q2 presentation focused on its progress toward margin targets and the expected benefits from major capital investments nearing completion. The company is navigating a complex market environment with varying performance across its key segments while maintaining its commitment to long-term growth and shareholder value.

Quarterly Performance Highlights

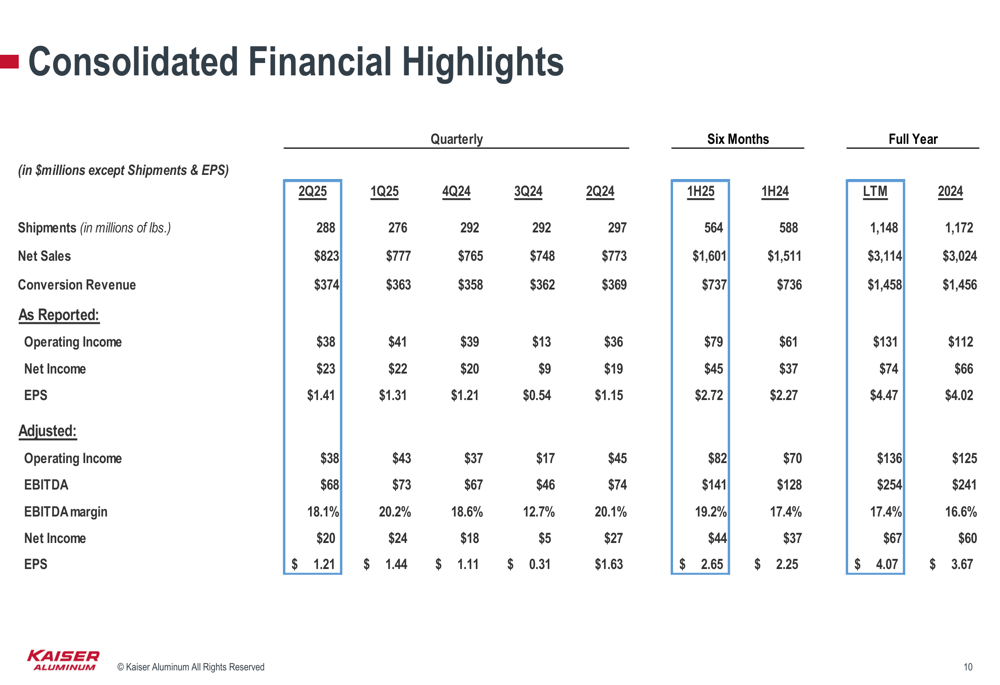

Kaiser reported Q2 2025 EBITDA of $68 million with an 18.1% EBITDA margin, showing strong pricing and improved product mix coupled with favorable metal pricing. While this represents a slight decrease from Q1 2025’s $73 million EBITDA, the company emphasized it remains on track with its strategic objectives.

As shown in the following consolidated financial highlights table, Kaiser continues to demonstrate solid performance across key metrics:

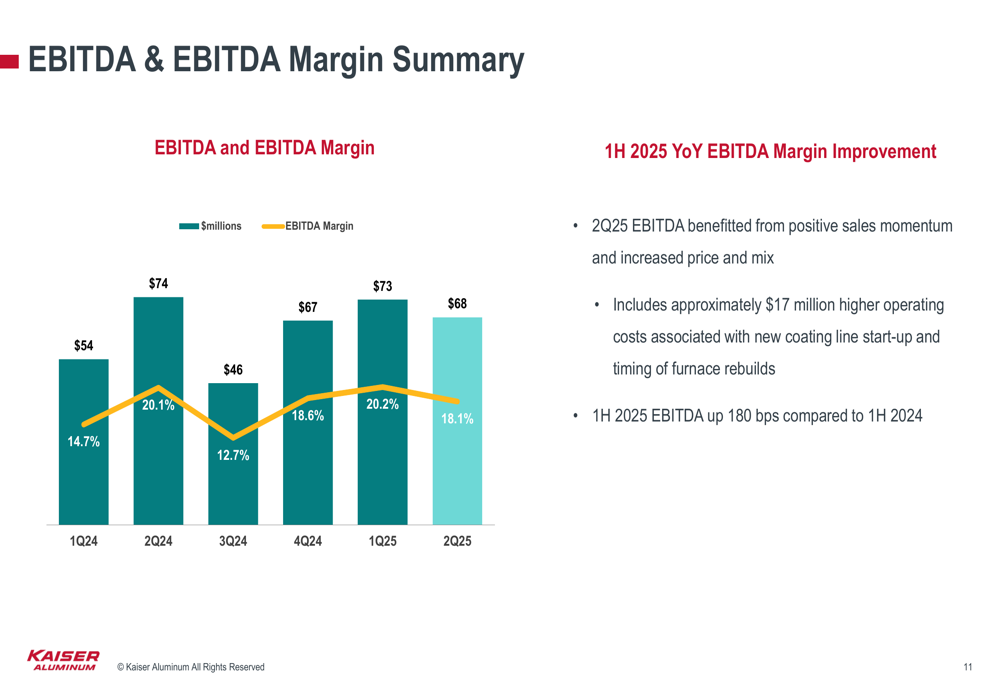

The company noted that Q2 2025 EBITDA included approximately $17 million in higher operating costs associated with the new coating line start-up and timing of furnace rebuilds. Despite these temporary cost increases, Kaiser’s EBITDA margin shows a positive trend, with first half 2025 EBITDA margin up 180 basis points compared to the same period in 2024.

The following chart illustrates Kaiser’s EBITDA and margin progression over recent quarters:

End Market Analysis

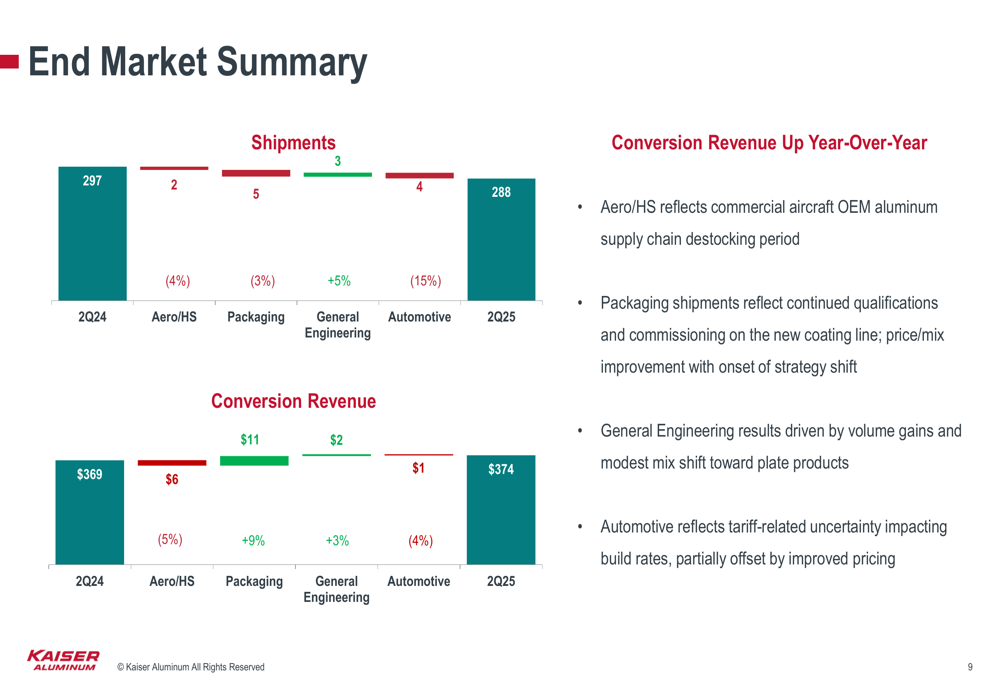

Kaiser’s performance varies significantly across its four key market segments, with each facing unique dynamics and challenges. The company provided a detailed breakdown of shipments and conversion revenue by end market:

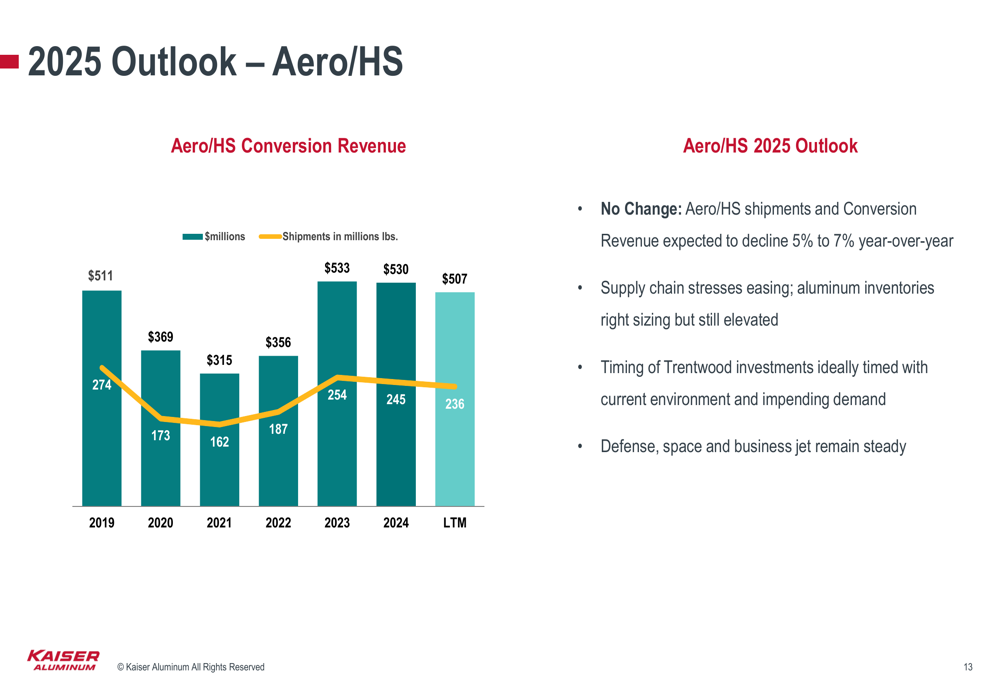

In the aerospace and high-strength (Aero/HS) segment, Kaiser reported that commercial aircraft OEM aluminum supply chains are going through a destocking period. Despite this temporary challenge, the company maintains a positive long-term outlook for this segment as illustrated in the following chart:

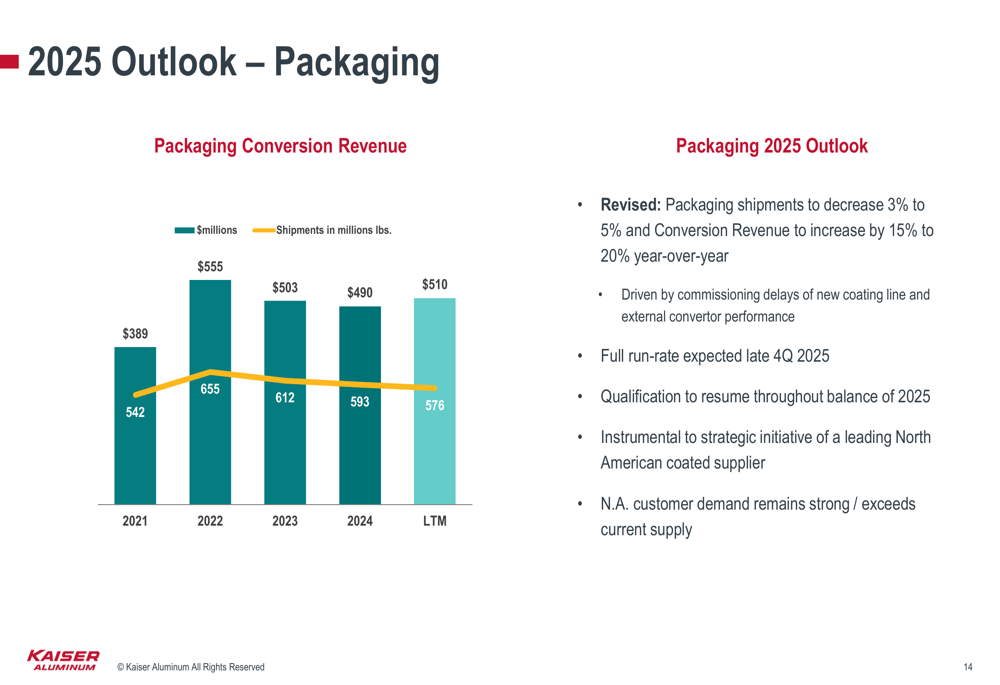

The packaging segment shows improving price/mix dynamics as Kaiser implements its strategic shift, though shipments reflect ongoing qualifications and commissioning on the new coating line:

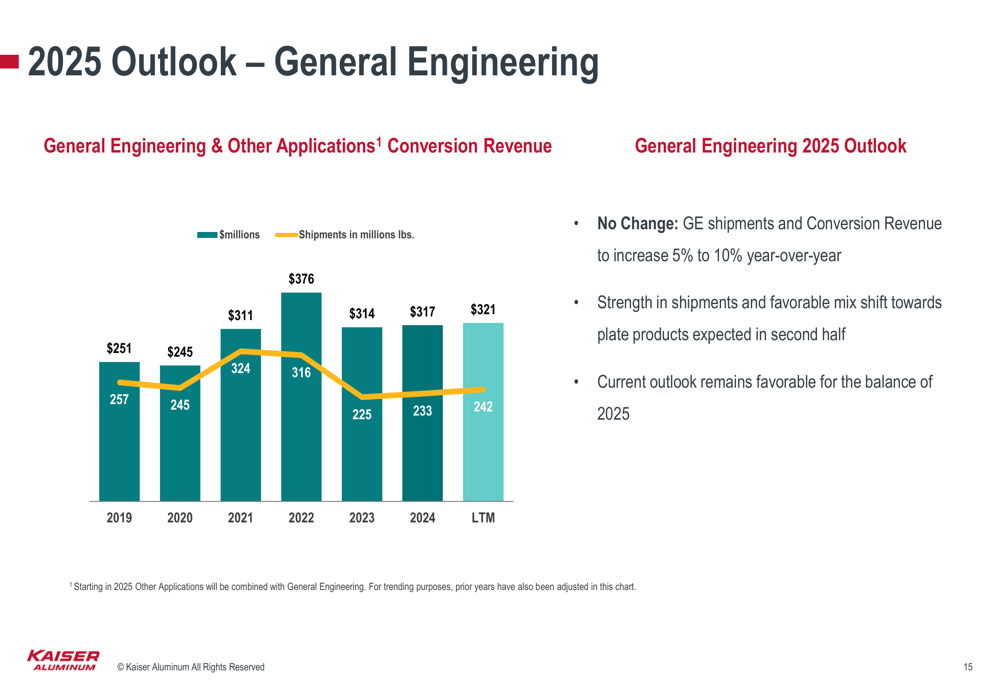

General Engineering results were driven by volume gains and a modest mix shift toward plate products, with a favorable outlook for the remainder of 2025:

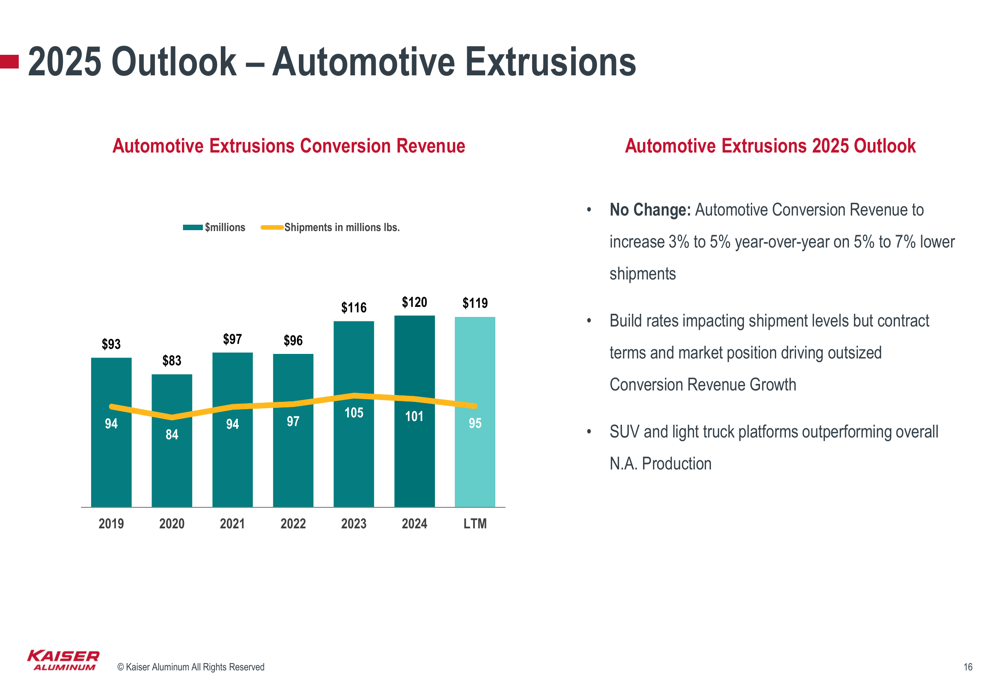

In the Automotive segment, Kaiser noted that tariff-related uncertainty is impacting build rates, though this is partially offset by improved pricing:

Strategic Initiatives & Investments

Kaiser emphasized that its strategic investments are well-timed to position the company for future growth. Two key initiatives highlighted in the presentation include:

1. Warrick roll coat line: Customer qualifications are underway with full run-rate expected by late Q4 2025. This investment is described as "instrumental to strategic initiative of a leading North American coated supplier."

2. Trentwood Phase VII: On track for completion in early Q4 2025. This investment aligns with the current aerospace market environment and anticipated future demand growth.

These investments are expected to drive significant EBITDA and EBITDA margin expansion starting in 2026, supporting Kaiser’s progress toward margin targets in the mid-to-high 20% range.

Forward-Looking Statements

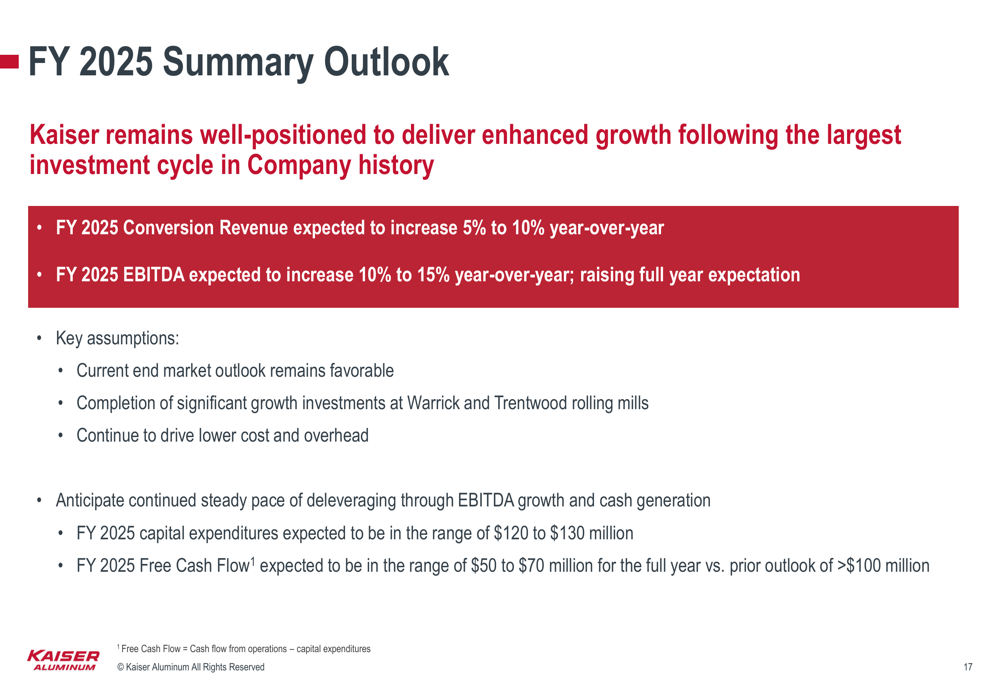

Kaiser provided a comprehensive outlook for fiscal year 2025, raising its EBITDA expectations while acknowledging some adjustments to its free cash flow projections:

Key elements of the 2025 outlook include:

- Conversion Revenue expected to increase 5-10% year-over-year

- EBITDA expected to increase 10-15% year-over-year (raised from previous guidance)

- Capital expenditures projected at $120-130 million

- Free Cash Flow expected to be $50-70 million, revised downward from the previous outlook of >$100 million mentioned in Q1 reporting

This revision in Free Cash Flow expectations represents a notable adjustment from the company’s Q1 2025 outlook, likely reflecting the impact of higher operating costs associated with new investments and ongoing market challenges.

Conclusion

Kaiser Aluminum’s Q2 2025 presentation portrays a company making strategic investments for long-term growth while navigating varying conditions across its end markets. The raised EBITDA guidance signals management’s confidence in the company’s operational improvements and strategic positioning, despite temporary headwinds in certain segments and higher near-term costs associated with major capital projects.

As these investments reach completion in late 2025, investors will be watching closely to see if Kaiser can deliver on its promises of significant EBITDA expansion and progress toward its mid-to-high 20% margin targets in 2026 and beyond. The reduced Free Cash Flow outlook for 2025 suggests some caution may be warranted in the near term, even as the company maintains its focus on long-term value creation through strategic positioning and operational excellence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.