Eos Energy stock falls after Fuzzy Panda issues short report

Introduction & Market Context

Kapsch TrafficCom (KTCG) presented its first quarter 2025/26 results on August 20, 2025, revealing a complex financial picture characterized by significant revenue declines offset by improved profitability. The mobility technology company, which specializes in tolling and traffic management solutions, continues to navigate a challenging operational environment while focusing on efficiency improvements and debt reduction.

Quarterly Performance Highlights

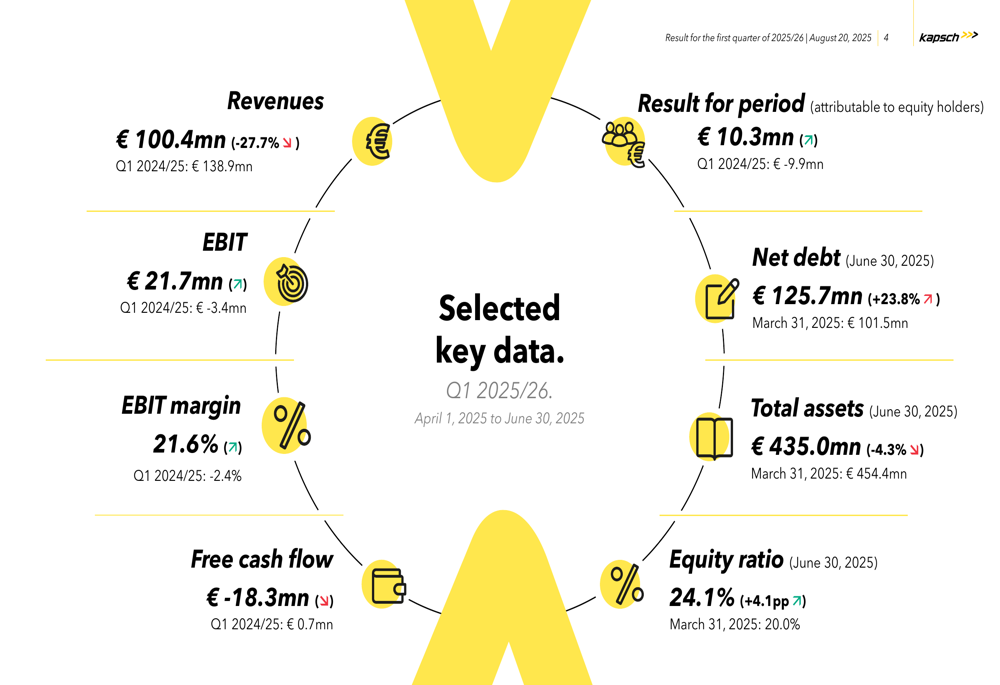

Despite a substantial 28% year-over-year revenue decline, Kapsch TrafficCom reported several positive developments in Q1 2025/26, most notably a settlement agreement with the Federal Republic of Germany that will result in a €27 million cash inflow in the second quarter. This settlement, combined with efficient cost management, helped drive EBIT growth despite the revenue challenges.

As shown in the following key highlights from the company’s presentation:

The company’s selected financial metrics for the quarter reveal the mixed performance picture. While revenues fell sharply to €100.4 million, EBIT increased to €21.7 million, resulting in a significantly improved EBIT margin of 21.6%. However, free cash flow turned negative at -€18.3 million, and net debt increased to €125.7 million, up 23.8% from the end of the previous fiscal year.

Detailed Financial Analysis

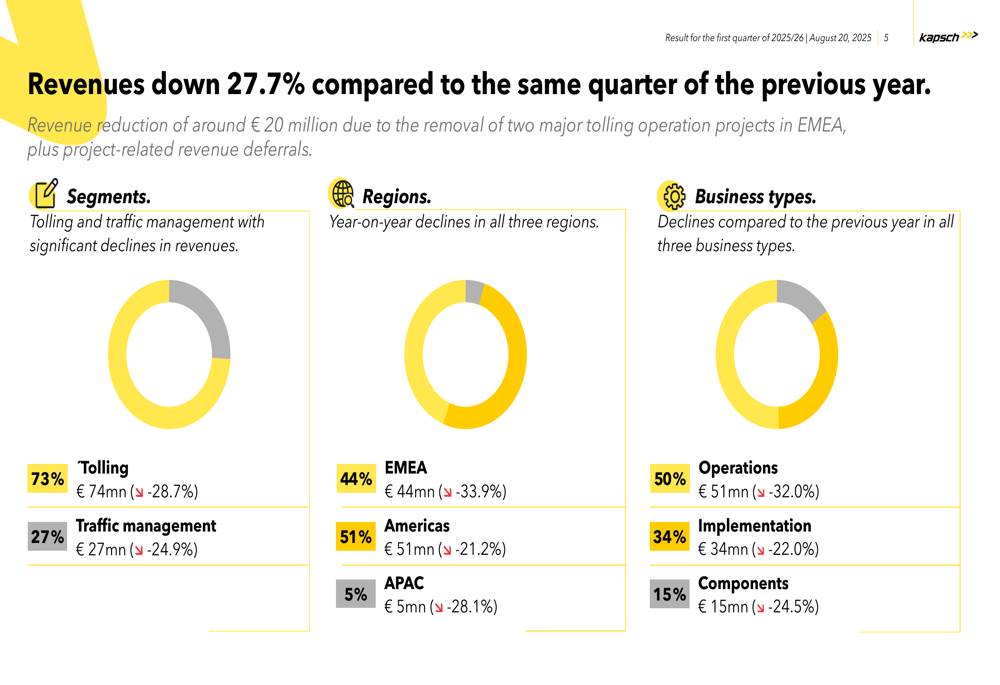

Kapsch TrafficCom’s revenue decline of 27.7% was attributed primarily to the removal of two major tolling operation projects in the EMEA region and project-related revenue deferrals. The revenue breakdown shows declines across all segments, regions, and business types, with operations experiencing the steepest drop at 32%.

The following chart illustrates the company’s revenue distribution across different segments, regions, and business types:

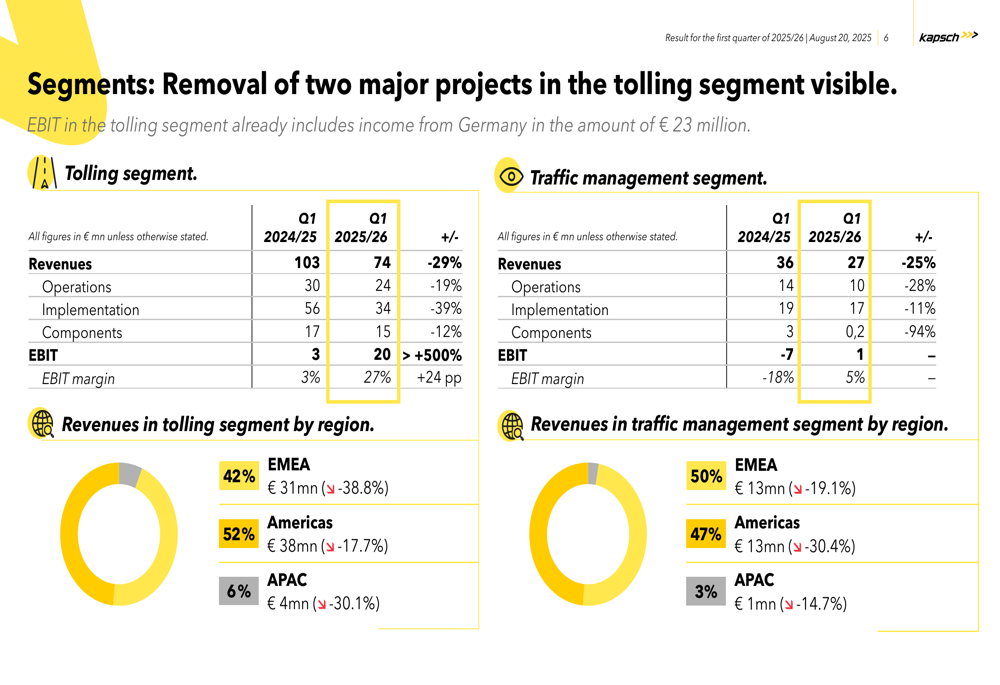

In the segment analysis, tolling remains the dominant business segment, accounting for 73% of total revenue at €74 million, though it experienced a 28.7% year-over-year decline. The traffic management segment, representing 27% of revenue at €27 million, saw a slightly smaller decline of 24.9%.

Geographically, the Americas region has become the largest revenue contributor at 51% of total revenue, while EMEA now accounts for 44%, following the steepest regional decline of 33.9%. The APAC region remains a small portion of the business at just 5% of revenue.

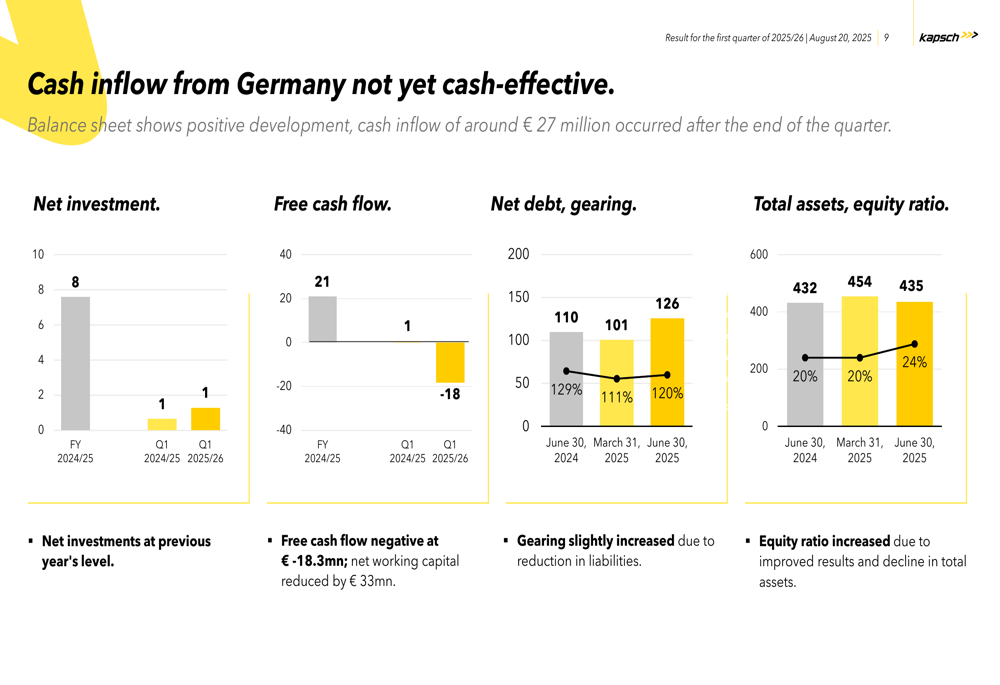

The company’s financial position shows some concerning trends in cash flow and debt levels, though the equity ratio has improved to 24.1%, up 4.1 percentage points from March 31, 2025. The negative free cash flow of €18.3 million in Q1 2025/26 contrasts with the positive €1 million in the same quarter of the previous year.

The following chart illustrates key financial position metrics:

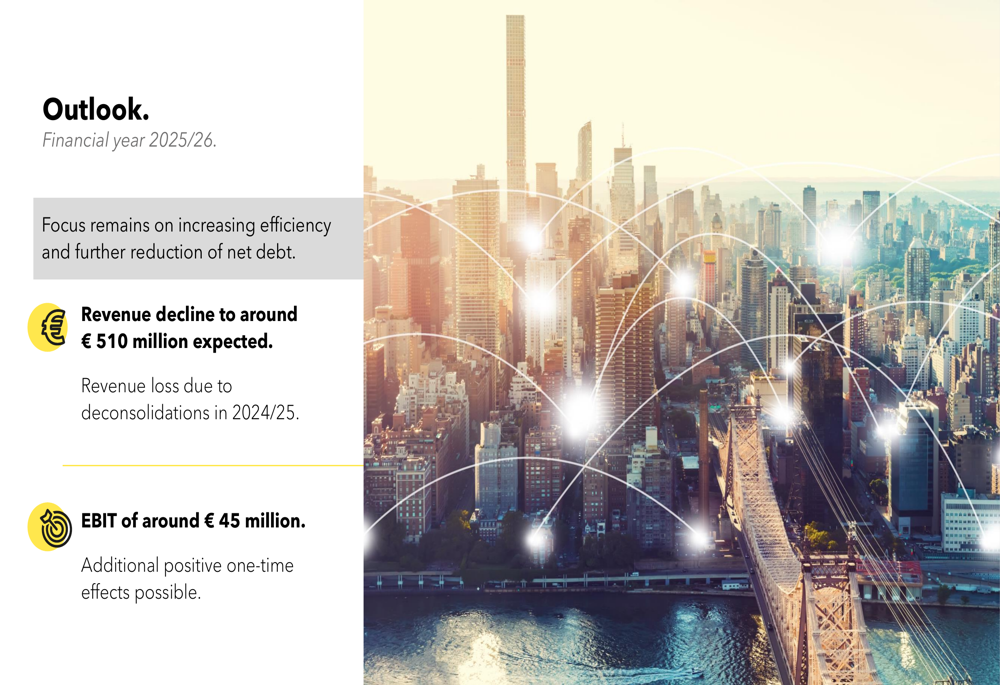

Forward-Looking Statements

Looking ahead to the full financial year 2025/26, Kapsch TrafficCom expects revenue to decline to approximately €510 million, primarily due to deconsolidations that occurred in the previous financial year. Despite this revenue drop, the company forecasts EBIT of around €45 million, with additional positive one-time effects possible.

Management emphasized that the focus remains on increasing efficiency and further reducing net debt, continuing the strategic direction set in previous quarters.

The company’s ability to maintain profitability despite significant revenue challenges suggests that its cost management and operational efficiency initiatives are bearing fruit. However, the increasing net debt and negative free cash flow indicate ongoing financial pressures that will require careful management in the coming quarters.

The €27 million settlement with Germany expected in Q2 should provide some financial relief, potentially helping to address the debt situation. Investors will likely be watching closely to see if Kapsch TrafficCom can stabilize its revenue while continuing to improve its operational efficiency and financial position.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.