Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

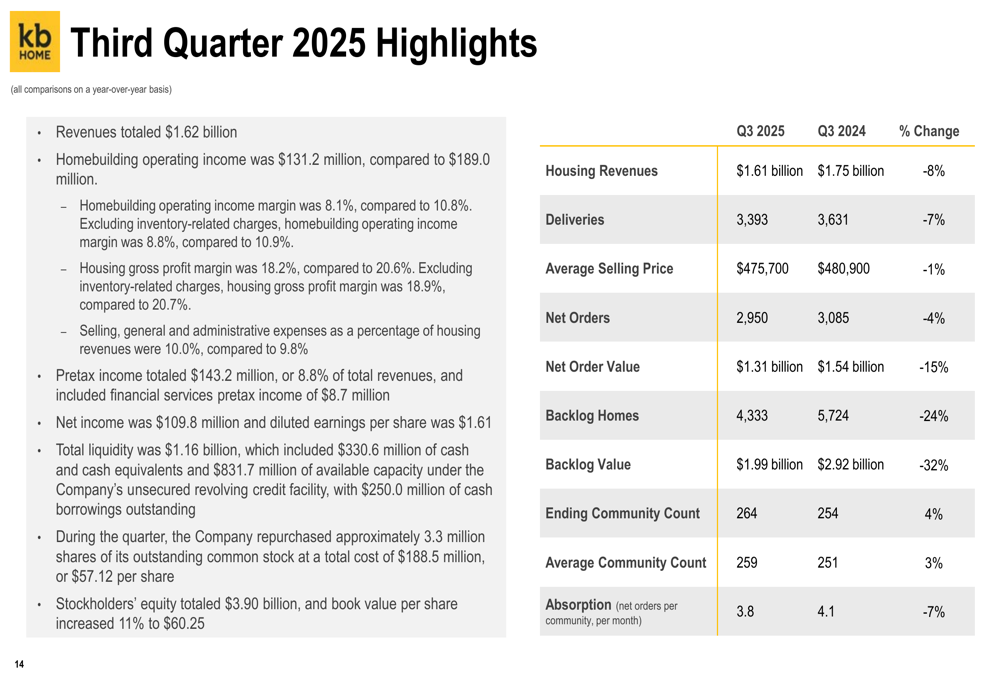

KB Home (NYSE:KBH) presented its third quarter 2025 results on September 24, revealing declining metrics across several key performance indicators amid ongoing housing market challenges. The presentation highlighted the company’s strategic positioning, capital allocation priorities, and long-term growth initiatives despite short-term pressures.

The homebuilder, which operates in 49 markets across 9 states, reported an 8% year-over-year decline in housing revenues to $1.61 billion, reflecting broader industry headwinds including elevated mortgage rates and softening consumer confidence. Following the earnings release, KB Home’s stock closed at $62.41, showing minimal change (-0.04%) in regular trading, with a slight uptick to $62.51 (+0.16%) in after-hours trading.

Quarterly Performance Highlights

KB Home’s third quarter 2025 results showed declines across most key metrics compared to the same period in 2024. Housing revenues fell 8% year-over-year to $1.61 billion, while home deliveries decreased 7% to 3,393 units. The average selling price saw a modest 1% decline to $475,700.

As shown in the following comprehensive overview of the quarter’s performance:

Net orders decreased 4% year-over-year to 2,950, while net order value fell more significantly by 15% to $1.31 billion. The company’s backlog metrics showed even sharper declines, with backlog homes down 24% and backlog value down 32% compared to Q3 2024.

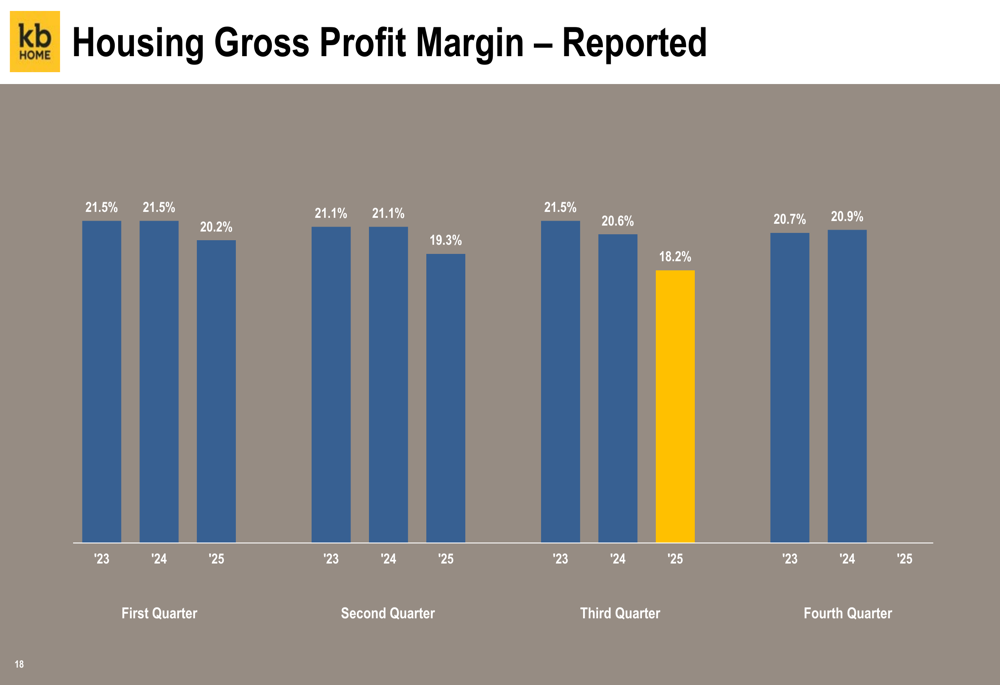

Profitability metrics also faced pressure, with the housing gross profit margin declining to 18.2% in Q3 2025 from 20.6% in Q3 2024:

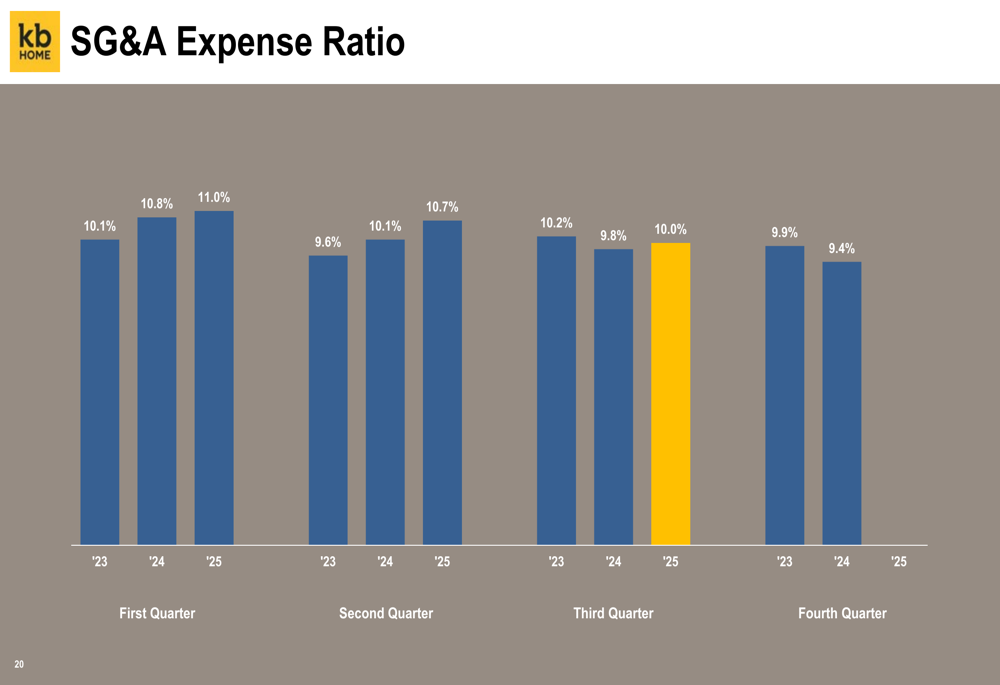

The SG&A expense ratio slightly increased to 10.0% from 9.8% in the prior year period:

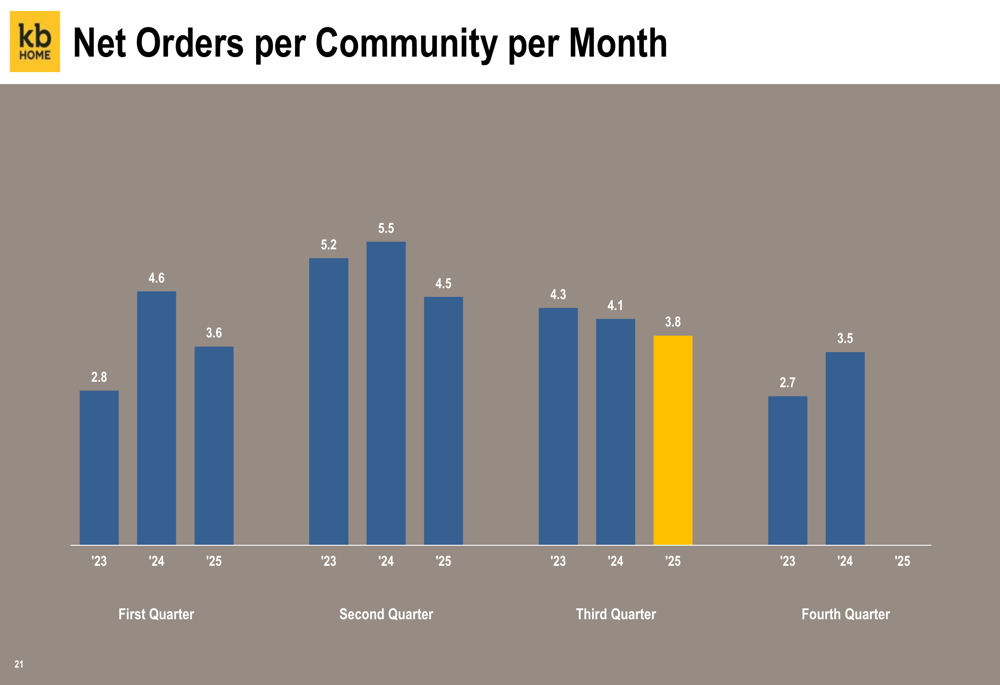

Despite these challenges, KB Home maintained a healthy absorption rate of 3.8 homes per community per month, though this represented a 7% decrease from the previous year:

Strategic Initiatives

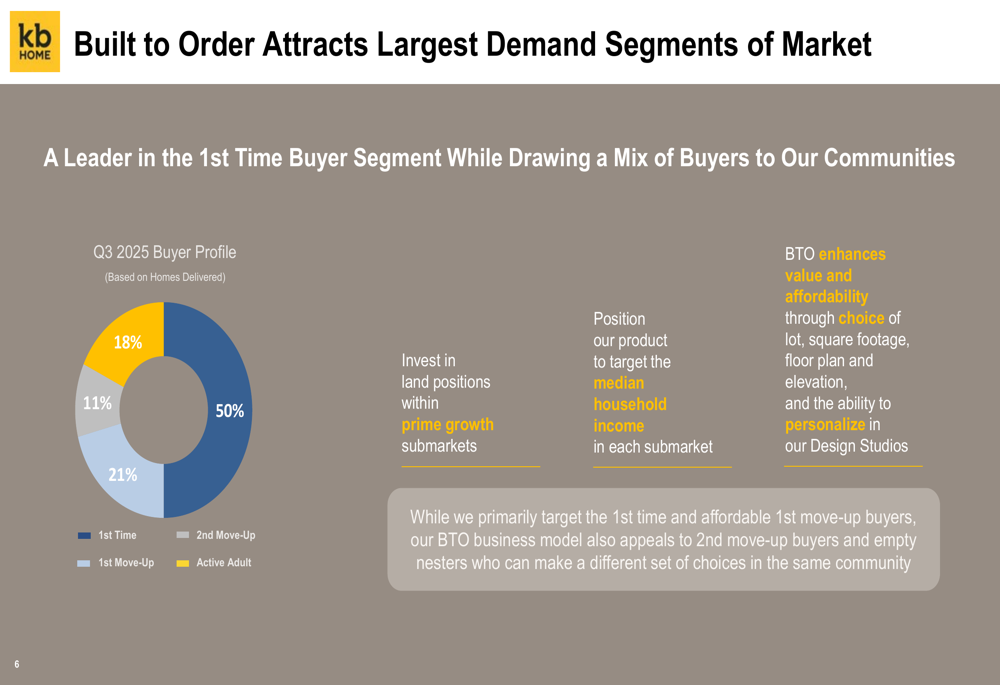

KB Home continues to emphasize its Built-to-Order (BTO) model as a key differentiator in the market. This approach allows homebuyers to personalize their homes, which the company believes provides a competitive advantage. The presentation highlighted that the BTO model attracts a diverse range of buyers, with first-time homebuyers representing 50% of deliveries in Q3 2025, followed by first move-up (18%), active adult (21%), and second move-up (11%) segments.

The company’s buyer profile is illustrated in the following chart:

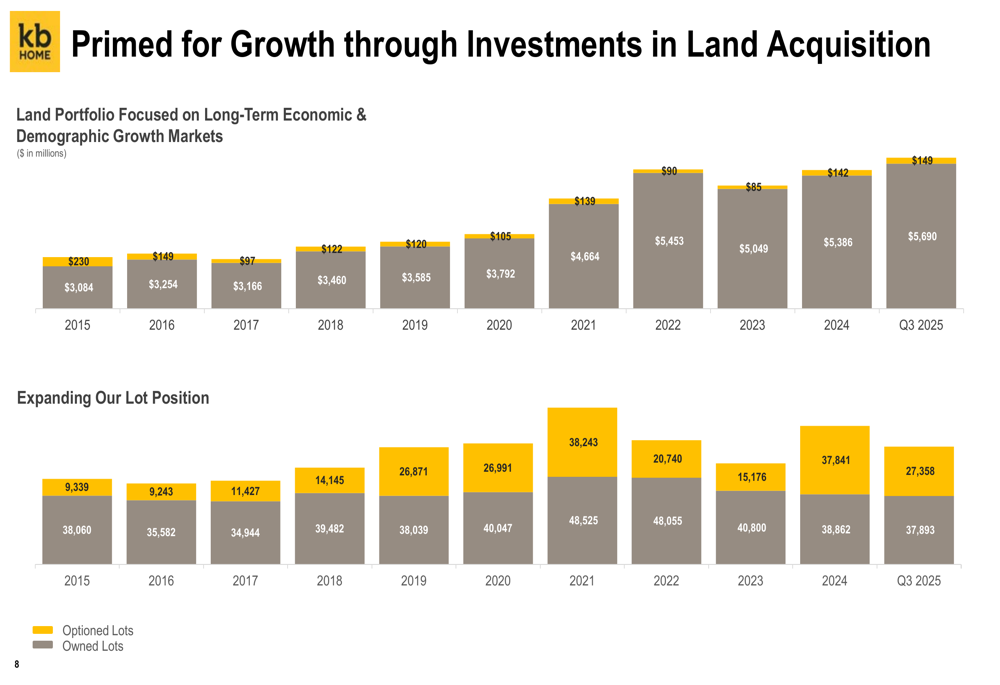

KB Home has maintained its focus on land acquisition and community count growth as part of its long-term strategy. The company reported a 4% year-over-year increase in ending community count to 264, and a 3% increase in average community count to 259 for Q3 2025. This investment in land positions is intended to support future growth, as shown in the following chart tracking the company’s owned and optioned lots:

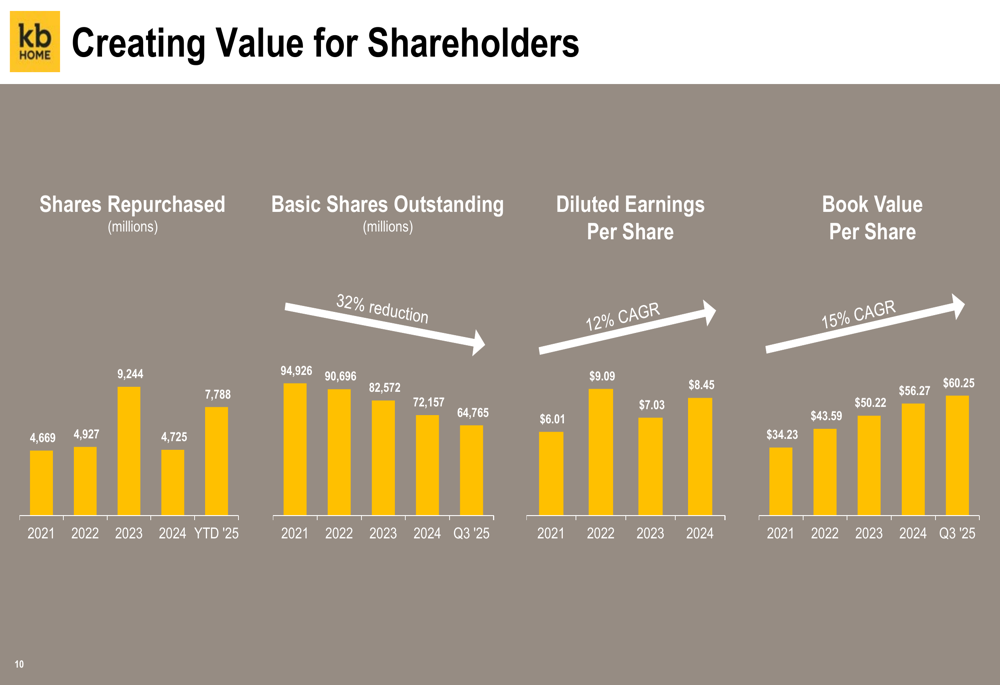

A key component of KB Home’s capital allocation strategy has been returning value to shareholders through share repurchases and dividends. Since Q2 2021, the company has returned over $1.8 billion to stockholders, with significant share repurchase activity reducing the basic shares outstanding from 94.9 million in 2021 to 64.8 million in Q3 2025, a 32% reduction.

The following chart illustrates the company’s share repurchase activity and its impact on key per-share metrics:

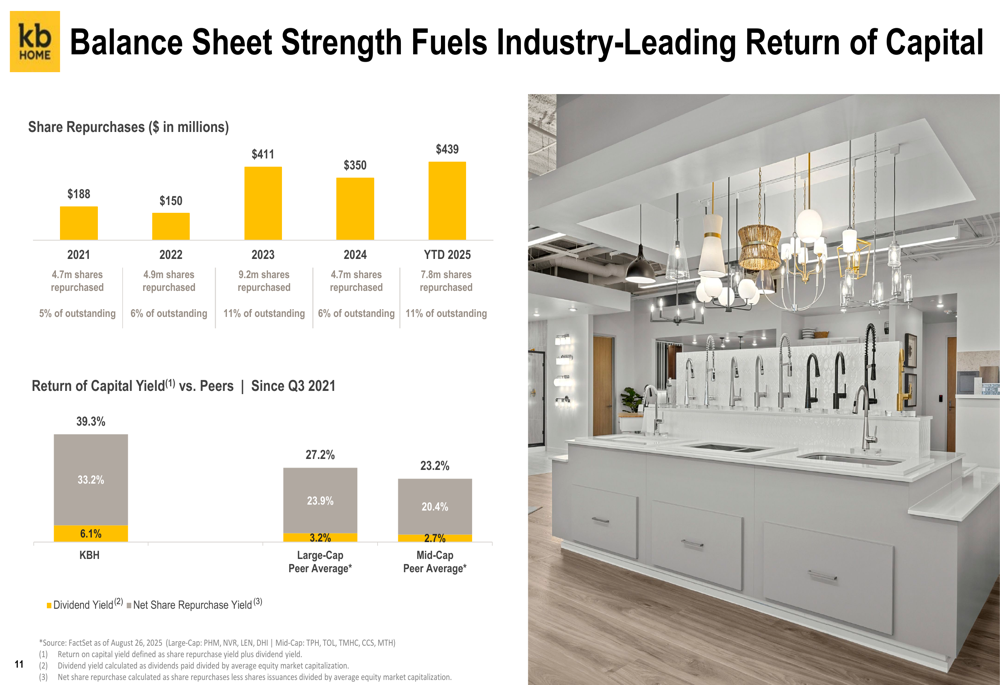

KB Home’s capital return yield of 39.3% since Q3 2021 significantly outpaces its peer group averages:

Sustainability and Governance

KB Home continues to position itself as a leader in sustainable homebuilding, highlighting achievements including over 200,000 ENERGY STAR certified homes, more than 25,000 solar homes, and approximately $1.3 billion in cumulative utility bill savings for homeowners.

The company’s sustainability credentials are showcased in the following comprehensive overview:

On the corporate governance front, KB Home emphasized that nine of its ten directors are independent, with directors elected annually under a majority voting standard. The company reported that directors received an average of 97% support in 2025, indicating strong shareholder confidence in the board’s oversight.

Forward-Looking Statements

Despite current market challenges, KB Home presented a positive long-term outlook based on its established brand, differentiated business model, and strategic market positioning. The company highlighted its focus on first-time and first move-up buyers, which it views as tapping into a large demographic opportunity with Millennials and Gen Z.

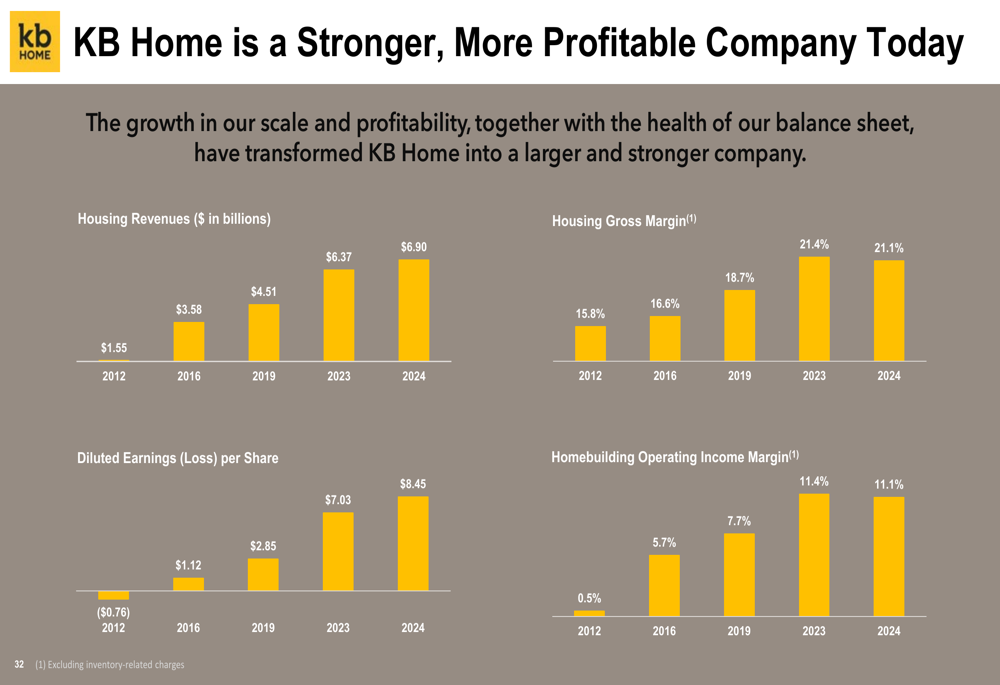

The presentation emphasized KB Home’s transformation over time into a stronger, more profitable company. Key metrics showing this evolution include growth in diluted earnings per share from $0.76 in 2012 to $8.45 in 2024, and improvement in homebuilding operating income margin from 0.5% in 2012 to 11.1% in 2024.

The company’s financial strength improvements are illustrated in the following comparison:

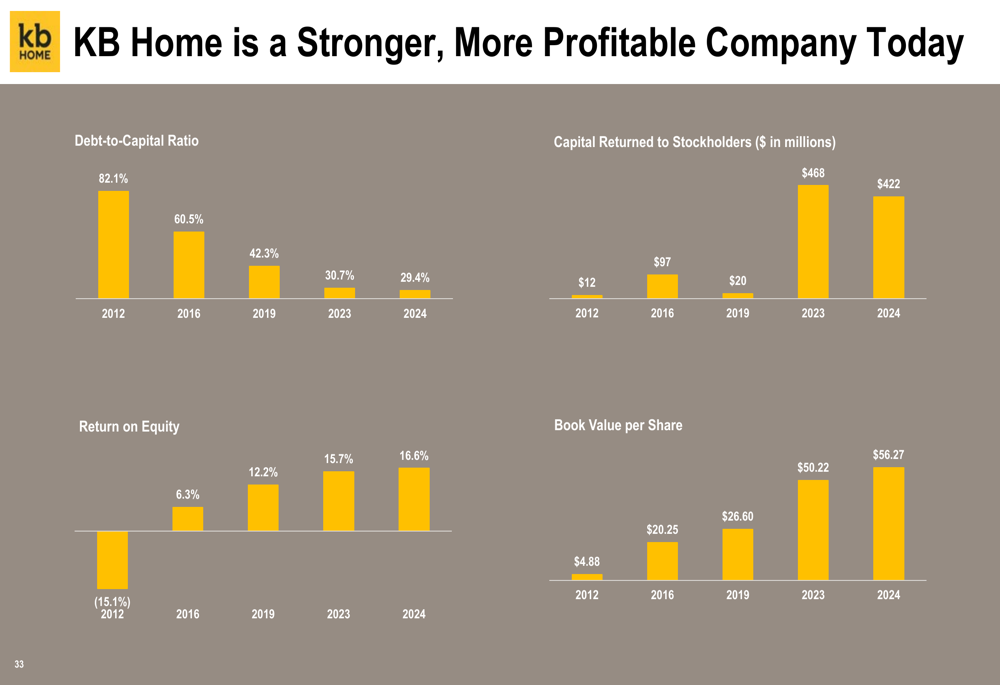

Additional financial metrics showing KB Home’s strengthened position include a reduction in debt-to-capital ratio from 82.1% in 2012 to 29.4% in 2024 (though this increased slightly to 33.2% in Q3 2025), and growth in book value per share from $4.88 in 2012 to $56.27 in 2024:

Looking ahead, KB Home faces continued challenges in the housing market, as evidenced by the declining metrics in Q3 2025. The company’s previous earnings call in Q2 2025 had revised its full-year housing revenue guidance to $6.3-$6.5 billion, with expected deliveries of approximately 13,200 homes. The Q3 results suggest that these targets may be under pressure as the company navigates through market headwinds.

Nevertheless, KB Home’s presentation emphasized its resilience through various housing cycles and its strategic positioning to capitalize on long-term demographic trends, supported by its differentiated business model and strong financial foundation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.