Nvidia shares pop as analysts dismiss AI bubble concerns

Kennametal Inc. (NYSE:KMT) shares jumped over 18% following the release of its Q1 FY26 earnings presentation on November 5, 2025, as the company reported its first quarter of organic growth in two years and exceeded analyst expectations.

Executive Summary

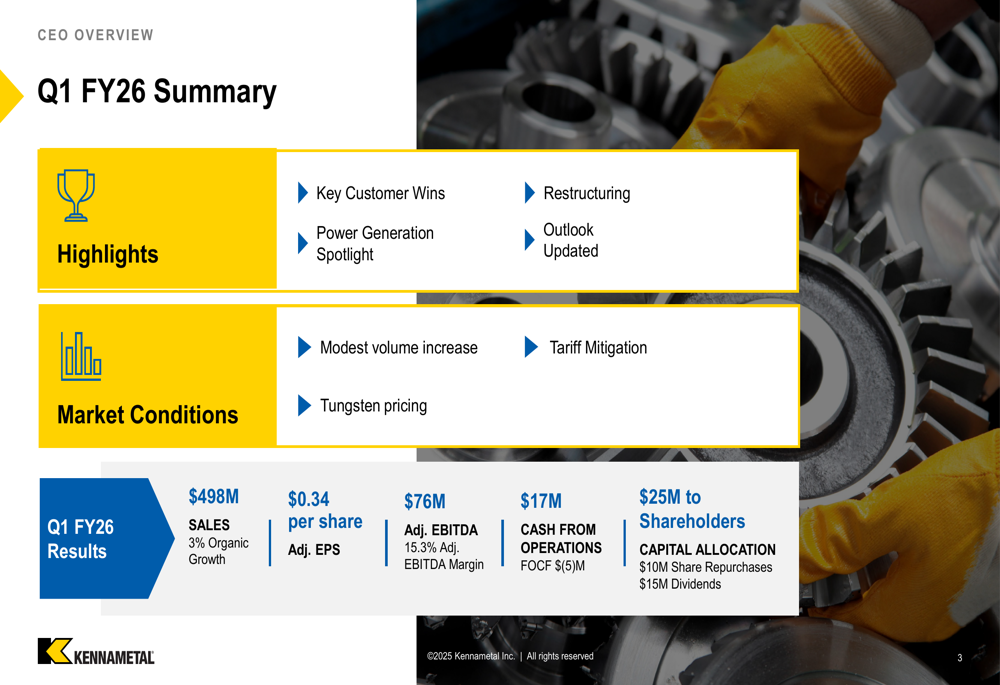

Kennametal delivered a strong start to fiscal year 2026, reporting sales of $498 million with 3% organic growth compared to the prior year. The company achieved adjusted earnings per share of $0.34, up from $0.29 in the same period last year, and significantly above the $0.23 expected by Wall Street analysts.

"We delivered a solid first quarter thanks to modest improvements in a couple of end markets, project wins on the commercial side, and cost improvement actions," noted CEO Sanjay Chowbey during the earnings call.

As shown in the following summary of Q1 FY26 performance, the company saw improvement across multiple metrics:

Quarterly Performance Highlights

Kennametal's return to organic growth was driven by a combination of pricing actions and share gains in key markets. The company's adjusted EBITDA reached $76 million, representing a 15.3% margin – an improvement of 100 basis points compared to the prior year.

The presentation highlighted that growth was particularly strong in the Aerospace & Defense segment (20% year-over-year) and Earthworks (5%), while regional performance was led by the Americas with 7% growth. The company successfully implemented price increases and tariff surcharges to offset rising costs, while also benefiting from $8 million in restructuring savings during the quarter.

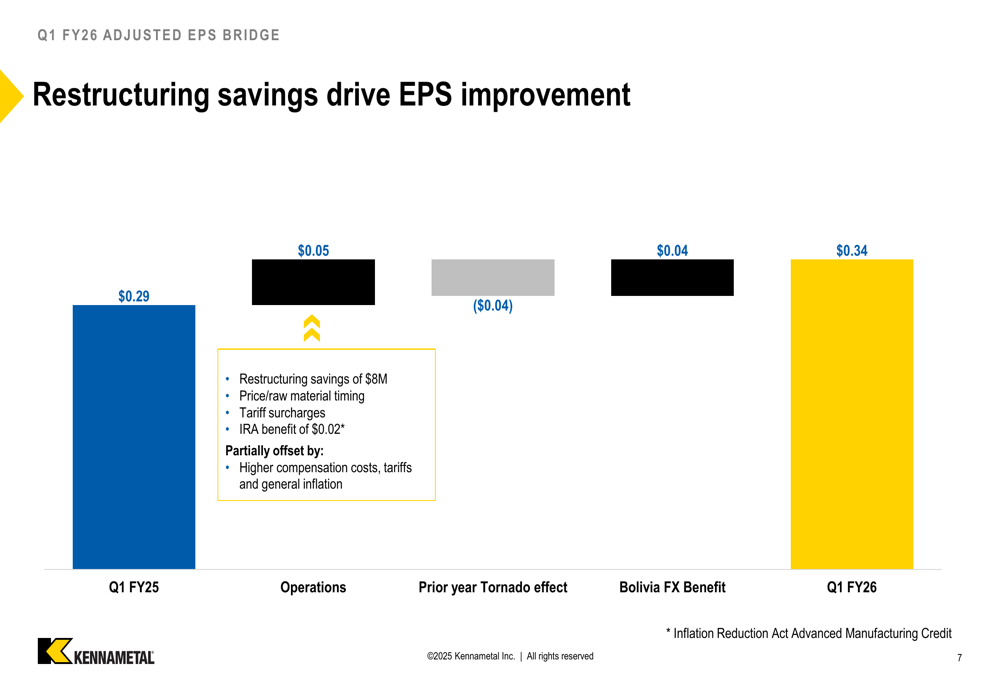

This waterfall chart illustrates how various factors contributed to the improvement in adjusted EPS from $0.29 in Q1 FY25 to $0.34 in Q1 FY26:

The company returned $25 million to shareholders during the quarter through $10 million in share repurchases (475,000 shares) and $15 million in dividends, demonstrating its commitment to shareholder value while maintaining financial flexibility.

Segment Performance

Kennametal operates through two main business segments: Metal Cutting and Infrastructure, both of which reported organic growth of 3% during the quarter.

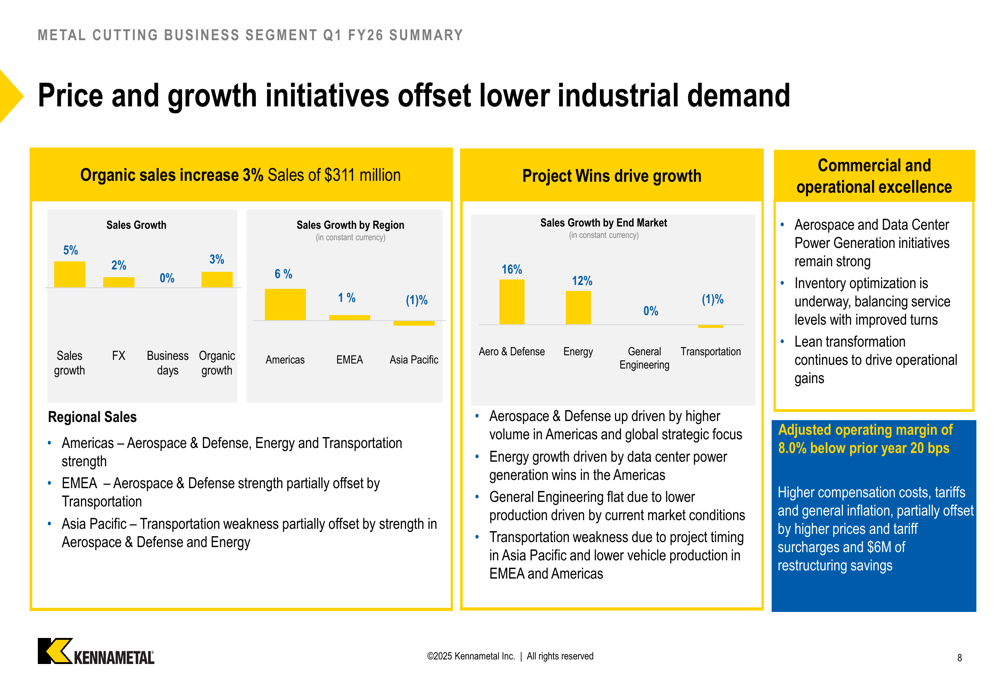

The Metal Cutting segment generated sales of $311 million, with particularly strong performance in Energy (16% growth) and Aerospace & Defense (12% growth). The segment's adjusted operating margin was 8.0%, slightly below the prior year by 20 basis points, primarily due to higher compensation costs, tariffs, and general inflation, partially offset by pricing actions and $6 million in restructuring savings.

As shown in this breakdown of the Metal Cutting segment performance:

The Infrastructure segment reported sales of $187 million, with exceptional growth in Aerospace & Defense (28%) and solid performance in Earthworks (5%). The segment's adjusted operating margin improved significantly to 8.8%, up 190 basis points from the prior year, driven by favorable price/raw material timing and $2 million in restructuring savings.

Strategic Initiatives

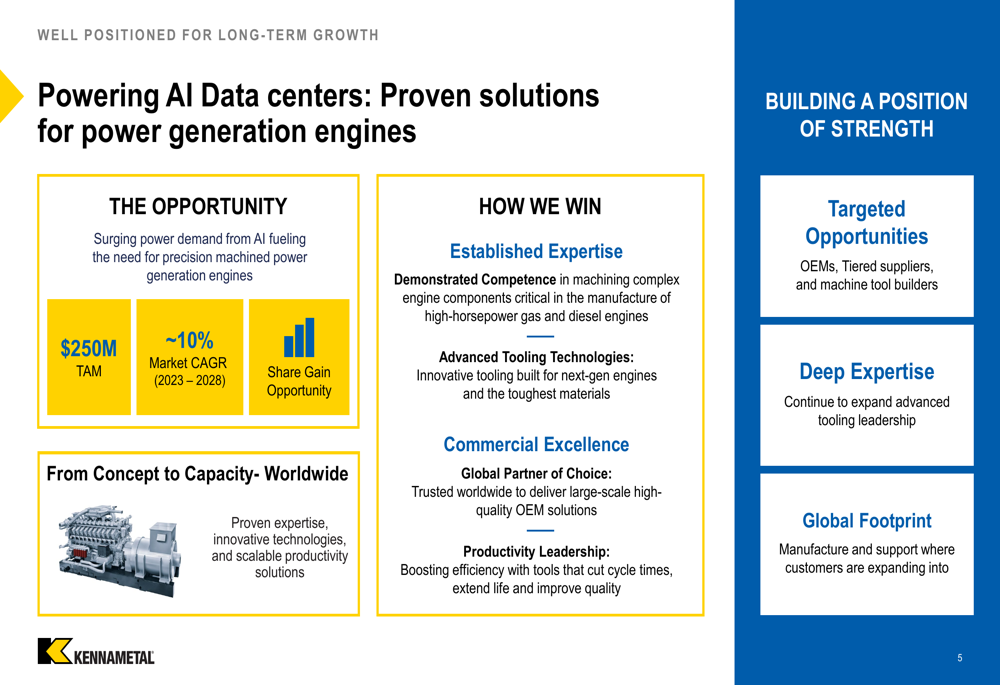

A key strategic focus highlighted in the presentation is Kennametal's growing presence in the power generation market for AI data centers. The company identified this as a $250 million total addressable market with a projected CAGR of approximately 10% from 2023-2028.

The following slide details Kennametal's approach to capitalizing on the increasing power demands of AI infrastructure:

The company's strategy leverages its established expertise in machining complex engine components, advanced tooling technologies, and global commercial presence to win in this growing market segment.

Additionally, Kennametal continues to implement its restructuring initiatives, which delivered $8 million in savings during Q1 and are on track to achieve approximately $35 million for the full fiscal year. The company is also focused on inventory optimization, balancing service levels with improved turns, while continuing its lean transformation to drive operational gains.

Financial Position

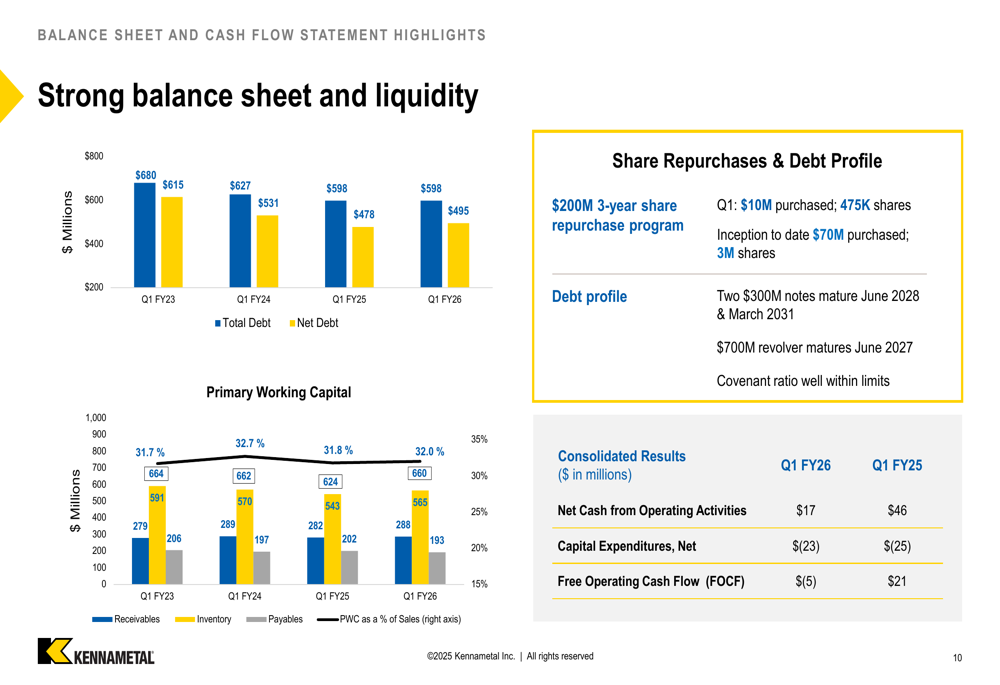

Kennametal maintained a strong balance sheet during the quarter, though free operating cash flow was negative at $(5) million compared to $21 million in the prior year. The company attributed this primarily to timing of working capital and capital expenditures.

The following chart illustrates the company's balance sheet and cash flow highlights:

Primary working capital as a percentage of sales was 32% at the end of the quarter, with the company targeting this same level by fiscal year-end. Kennametal's debt profile includes two $300 million notes maturing in June 2028 and March 2031, as well as a $700 million revolver maturing in June 2027, with covenants well within limits.

Forward-Looking Statements

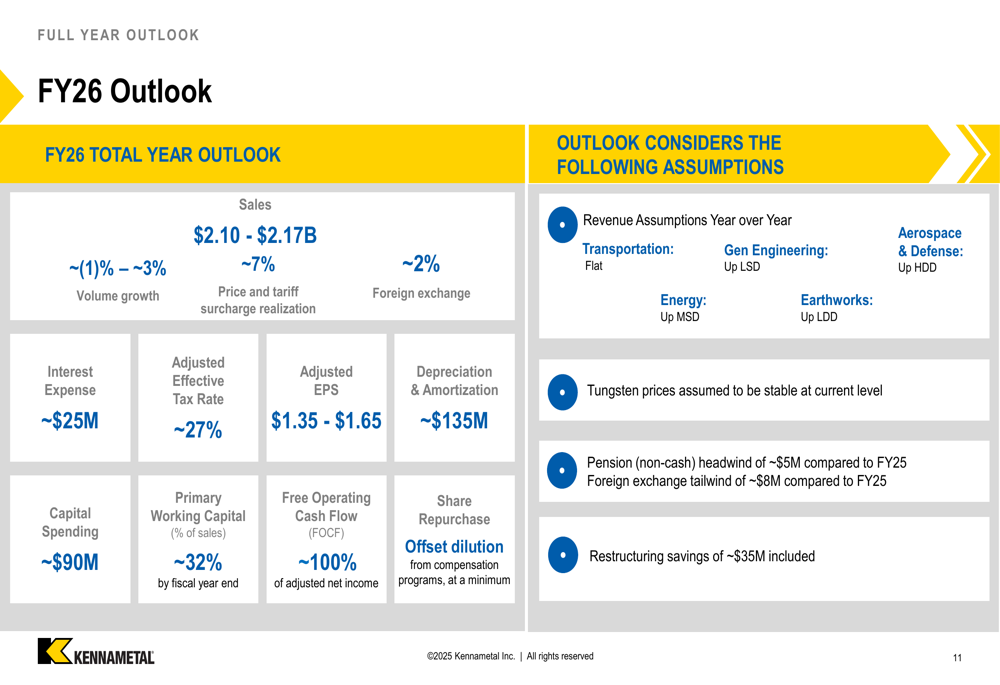

Looking ahead, Kennametal provided an optimistic outlook for fiscal year 2026, projecting sales between $2.10 billion and $2.17 billion, representing volume growth of approximately -1% to 3%, with price and tariff surcharge realization of approximately 7%.

The company expects adjusted earnings per share of $1.35 to $1.65 for the full year, with free operating cash flow projected at approximately 100% of adjusted net income.

As shown in this detailed outlook for FY26:

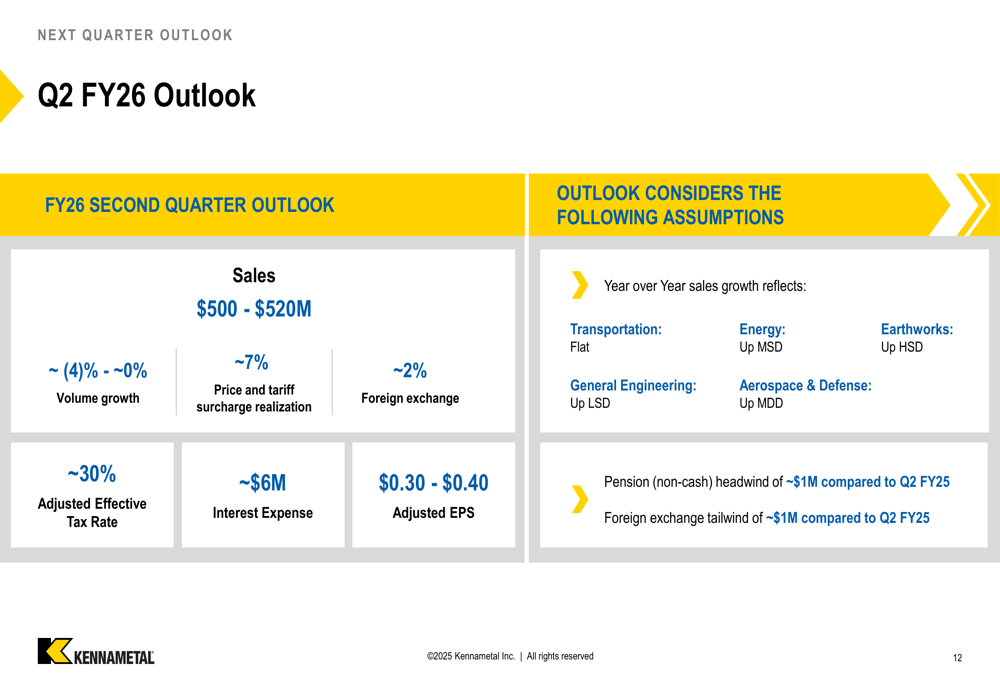

For the upcoming second quarter of FY26, Kennametal forecasts sales of $500-$520 million and adjusted EPS of $0.30-$0.40. The company expects continued strength in Aerospace & Defense (up mid-double digits) and Earthworks (up high single digits), with modest growth in General Engineering and Energy.

"We continue to make steady progress on our strategic growth initiatives, lean transformation, and structural cost improvement," added CEO Chowbey, expressing confidence in the company's ability to navigate market challenges while capitalizing on growth opportunities.

The market's strongly positive reaction to Kennametal's results and outlook reflects investor confidence in the company's strategy and execution, with the stock closing up 18.23% following the earnings release, near its 52-week high of $32.18.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.