Gold prices steady ahead of Fed decision; weekly weakness noted

Introduction & Market Context

Keyera Corp . (TSX:KEY) presented its latest investor outlook on May 15, 2025, highlighting the company’s strategic positioning within Canada’s energy infrastructure sector. The midstream operator, whose stock closed at $44.29 on May 14, has seen its share price increase by 0.7% and is currently trading near its 52-week high of $47.90, reflecting investor confidence in the company’s growth trajectory.

The presentation comes after Keyera reported strong Q3 2024 results, with net earnings of $185 million and adjusted EBITDA of $322 million, demonstrating the company’s operational resilience and financial discipline through various economic cycles.

Executive Summary

Keyera’s May 2025 investor presentation outlines an ambitious growth strategy centered around expanding its fee-based infrastructure business while leveraging its marketing capabilities as a competitive differentiator. The company is projecting a 7-8% compound annual growth rate (CAGR) in fee-based adjusted EBITDA from 2024 through 2027, supported by several capital-efficient growth projects and increasing utilization of existing assets.

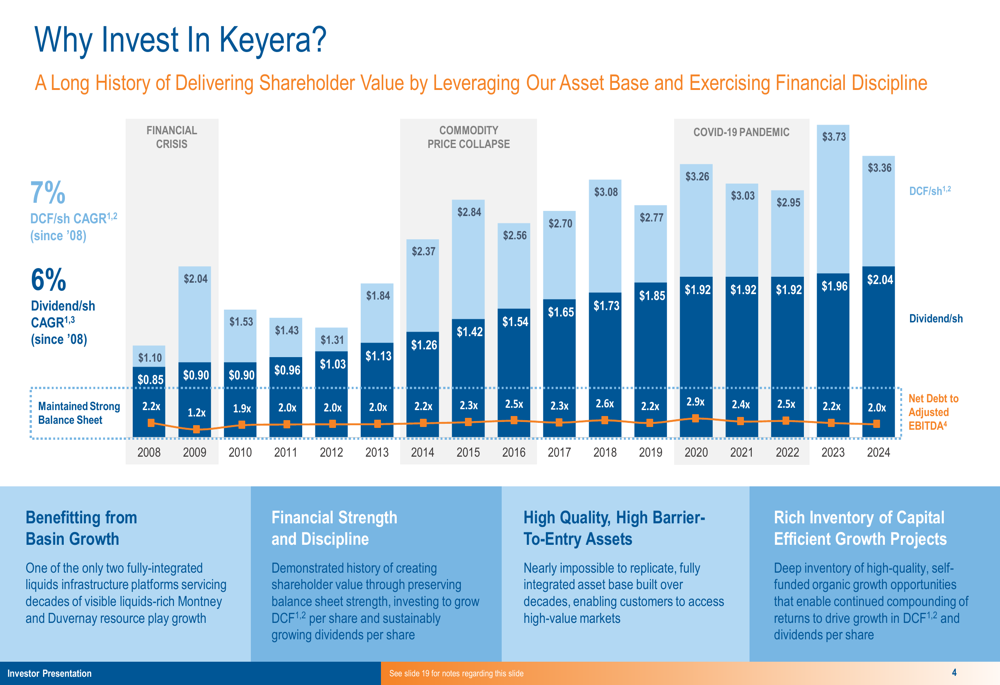

The presentation emphasizes Keyera’s historical performance, highlighting a distributable cash flow (DCF) per share CAGR of 7% and dividend per share CAGR of 6% since 2008, demonstrating consistent shareholder value creation through multiple economic cycles.

As shown in the following chart of Keyera’s DCF per share growth and financial performance through various economic cycles:

Strategic Initiatives

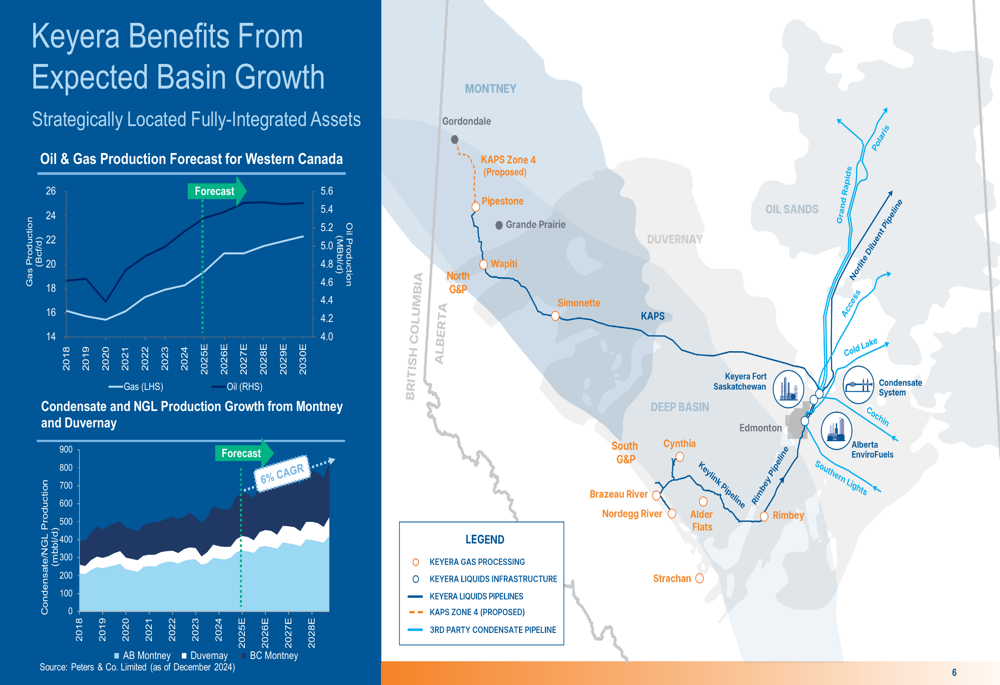

Keyera’s growth strategy is anchored in its strategic positioning within Western Canada’s energy basins, particularly the Montney, Duvernay, and conventional deep basin areas. The company projects significant production growth in these regions, with gas production forecast to increase from 17 Bcf/d in 2024 to 21 Bcf/d by 2030, and oil production rising from 4.6 Mbbl/d to 5.2 Mbbl/d over the same period.

The following chart illustrates the expected basin growth that Keyera is positioned to benefit from:

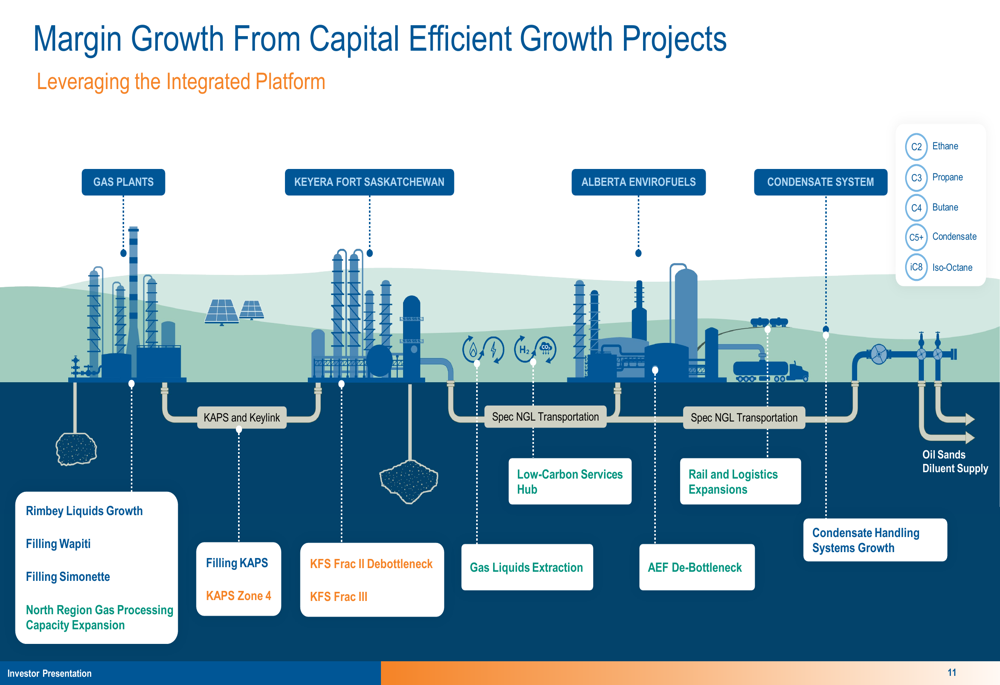

To capitalize on this growth, Keyera has sanctioned several strategic projects, including:

1. Frac II Debottleneck - Adding 8,000 bpd of fractionation capacity with expected in-service date in mid-2026

2. KFS Frac III - Adding 47,000 bpd of fractionation capacity with expected in-service date in 2028

3. KAPS Zone 4 - An 85 km expansion of the KAPS pipeline system with expected in-service date in late 2027

These projects form part of Keyera’s integrated infrastructure platform, which is designed to drive margin growth through capital-efficient investments, as illustrated in the following diagram:

Detailed Financial Analysis

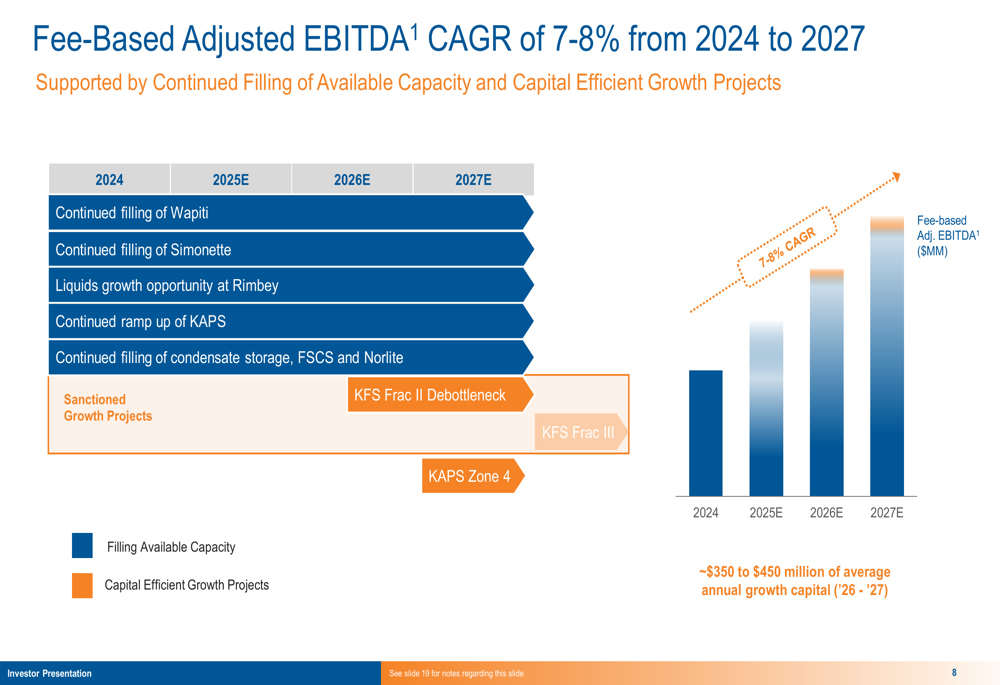

Keyera’s 2025 financial guidance includes marketing realized margin of $310-$350 million, growth capital expenditures of $300-$330 million, maintenance capital expenditures of $70-$90 million, and cash taxes of $100-$110 million. The company’s fee-based adjusted EBITDA is projected to grow at a 7-8% CAGR from 2024 to 2027.

The company’s 2025 guidance and growth projections are clearly presented in the following slide:

Keyera maintains a strong financial position with a net debt to adjusted EBITDA ratio of 2.0x as of Q1 2025, investment grade credit ratings, and total liquidity of $1.6 billion. The company’s disciplined capital allocation strategy focuses on preserving financial strength, investing for margin growth, and increasing cash returns to shareholders.

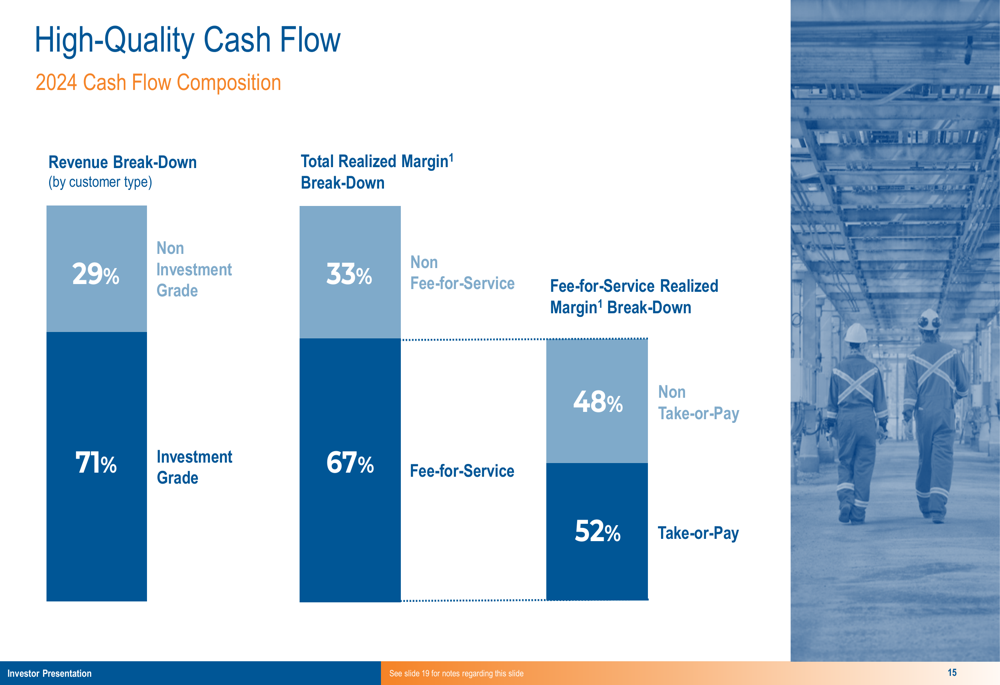

The quality of Keyera’s cash flow is highlighted by its customer and revenue composition, with 71% of revenue coming from investment grade customers and 67% of realized margin derived from fee-for-service arrangements, as shown in the following breakdown:

Marketing as a Competitive Advantage

Keyera positions its marketing segment as a unique differentiator that connects customers to high-value markets while generating superior returns on invested capital compared to peers. The marketing cash flow is strategically reinvested to accelerate fee-for-service growth, creating a virtuous cycle of value creation.

The following slide illustrates Keyera’s marketing strategy and performance relative to peers:

This marketing advantage has contributed to Keyera’s strong financial performance, though the recent earnings call noted potential challenges in Q4 2024 for the marketing segment due to market adjustments and softening crude prices.

Forward-Looking Statements

Looking beyond 2027, Keyera has identified several growth opportunities including liquids extraction, AEF debottlenecking, expanding gathering and processing capacity in the North Region, enhancing rail and logistics capabilities, and developing a conventional energy and low-carbon hub at Josephburg.

The company’s projected fee-based adjusted EBITDA growth through 2027 is supported by continued filling of available capacity and capital-efficient growth projects, as illustrated in the following chart:

Keyera also emphasizes its commitment to sustainability, having reduced emission intensity by 21% from 2019 to 2023, with further targets for GHG reduction. The company highlights its governance practices, including 50% female senior vice presidents and 40% female independent board directors.

Conclusion

Keyera’s May 2025 investor presentation outlines a clear growth strategy leveraging the company’s integrated infrastructure platform and strategic positioning within Western Canada’s energy basins. With a projected 7-8% CAGR in fee-based adjusted EBITDA through 2027, disciplined capital allocation, and strong financial position, Keyera appears well-positioned to continue delivering shareholder value while navigating the evolving energy landscape.

Investors should note that while the presentation focuses on growth opportunities, recent earnings calls have acknowledged some operational challenges and potential near-term market adjustments that could impact quarterly performance. Nevertheless, the company’s long-term growth trajectory remains supported by fundamental basin development and strategic capital investments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.