Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

KGHM Polska Miedź S.A. (WSE:KGH) presented its financial results for the first half of 2025 on August 20, revealing a complex performance picture shaped by favorable metal prices but challenging exchange rate dynamics. The copper and silver producer reported modest revenue growth amid a macroeconomic environment characterized by higher metal prices but offset by unfavorable currency movements.

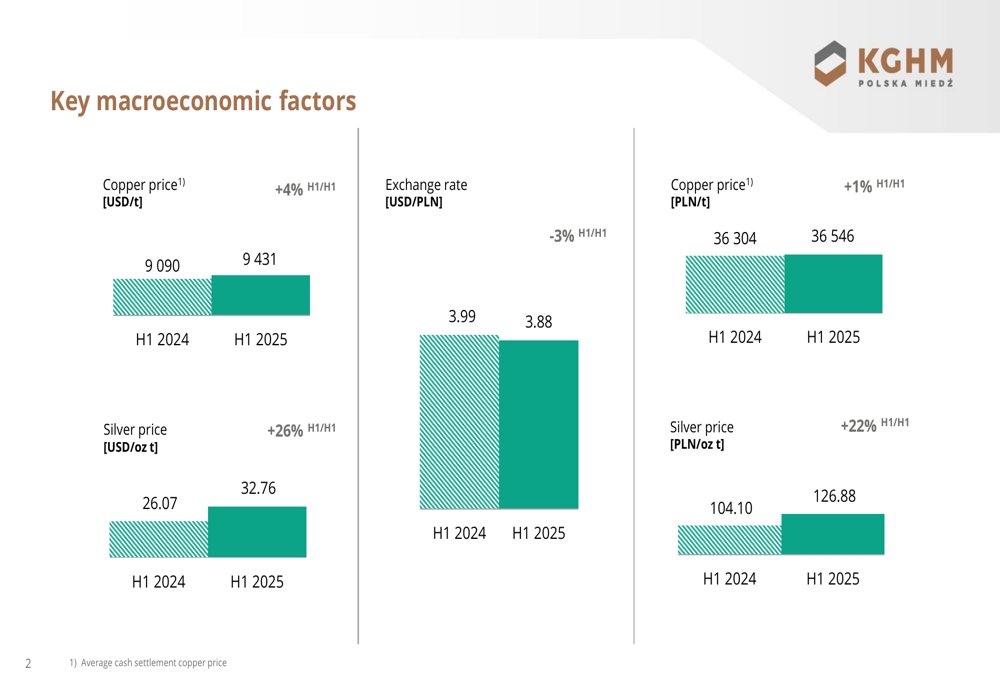

The company operated in a market where copper prices increased by 4% year-over-year to $9,431 per tonne in H1 2025, while silver prices surged by 26% to $32.76 per ounce. However, the strengthening of the Polish zloty against the US dollar (3.88 USD/PLN in H1 2025 vs. 3.99 USD/PLN in H1 2024) partially neutralized these gains when converted to the company’s reporting currency.

As shown in the following chart of key macroeconomic factors:

Financial Performance Highlights

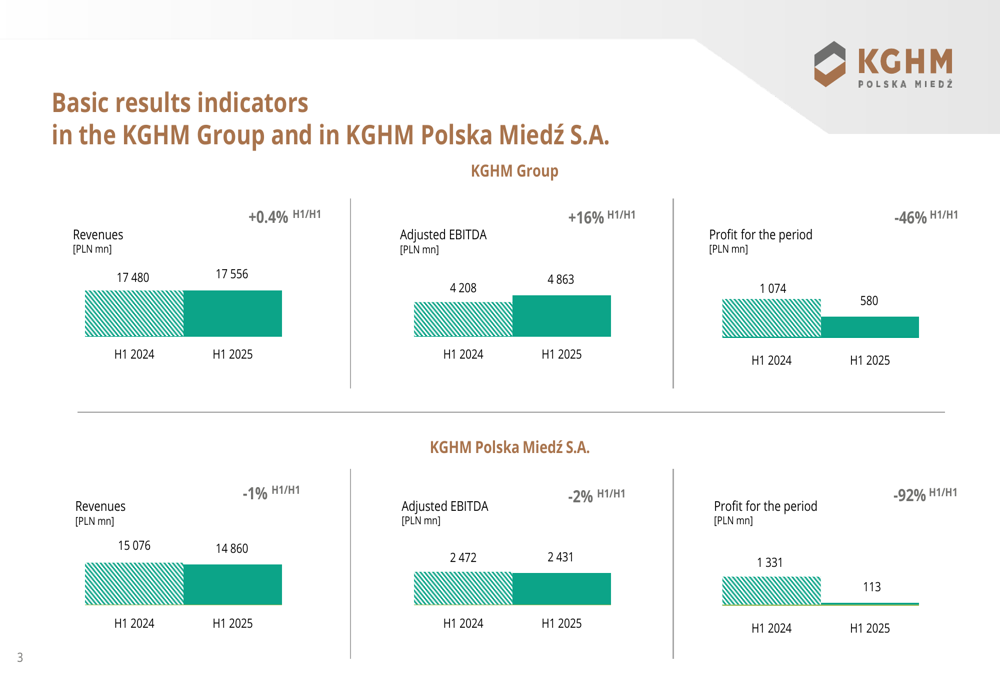

KGHM Group reported revenues of 17,556 million PLN for H1 2025, representing a marginal increase of 0.4% compared to the same period in 2024. Despite modest revenue growth, adjusted EBITDA rose significantly by 16% to 4,863 million PLN, demonstrating improved operational efficiency.

However, the Group’s profit for the period declined substantially by 46% to 580 million PLN, primarily due to negative exchange rate differences amounting to 1,355 million PLN. The parent company, KGHM Polska Miedź S.A., experienced an even more dramatic profit decline of 92% to just 113 million PLN.

The following chart illustrates these basic financial indicators:

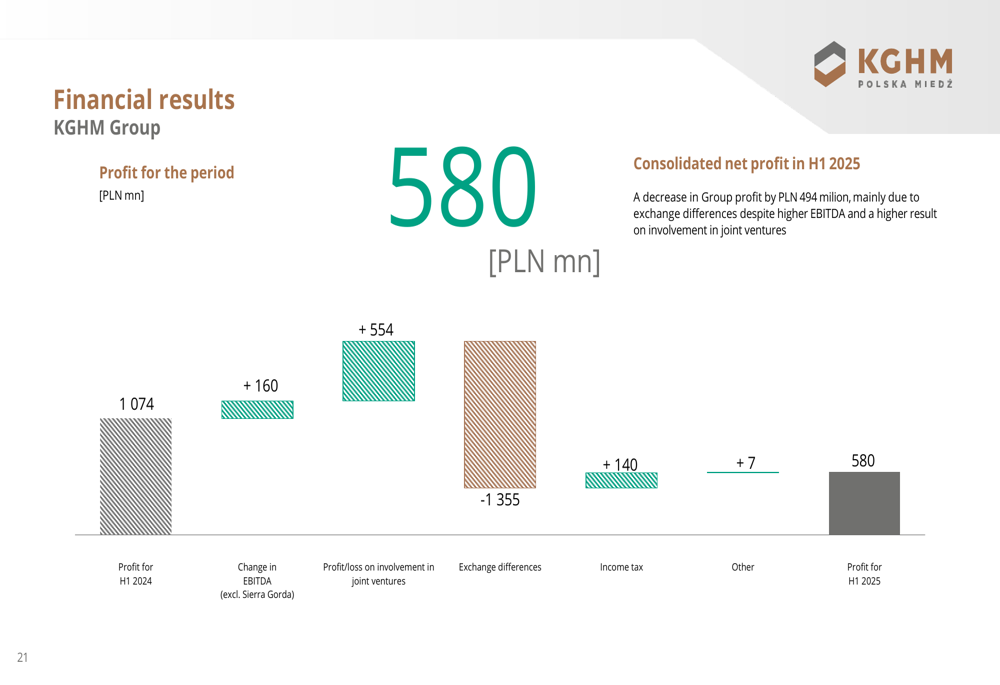

The company’s consolidated net profit was significantly impacted by several factors, with exchange rate differences being the most substantial negative contributor. This was partially offset by improved performance from joint ventures and favorable EBITDA development:

Operational Performance by Segment

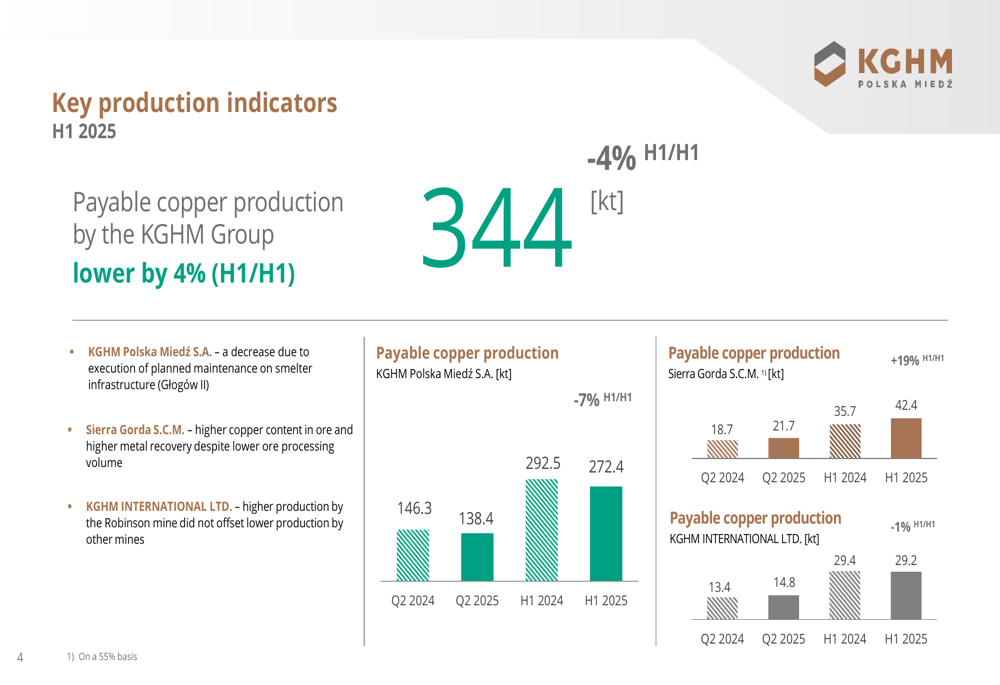

The Group’s payable copper production decreased by 4% year-over-year to 344,000 tonnes in H1 2025. This decline was primarily driven by a 7% reduction in KGHM Polska Miedź S.A.’s production to 272,400 tonnes, attributed to planned maintenance on smelter infrastructure at Głogów II.

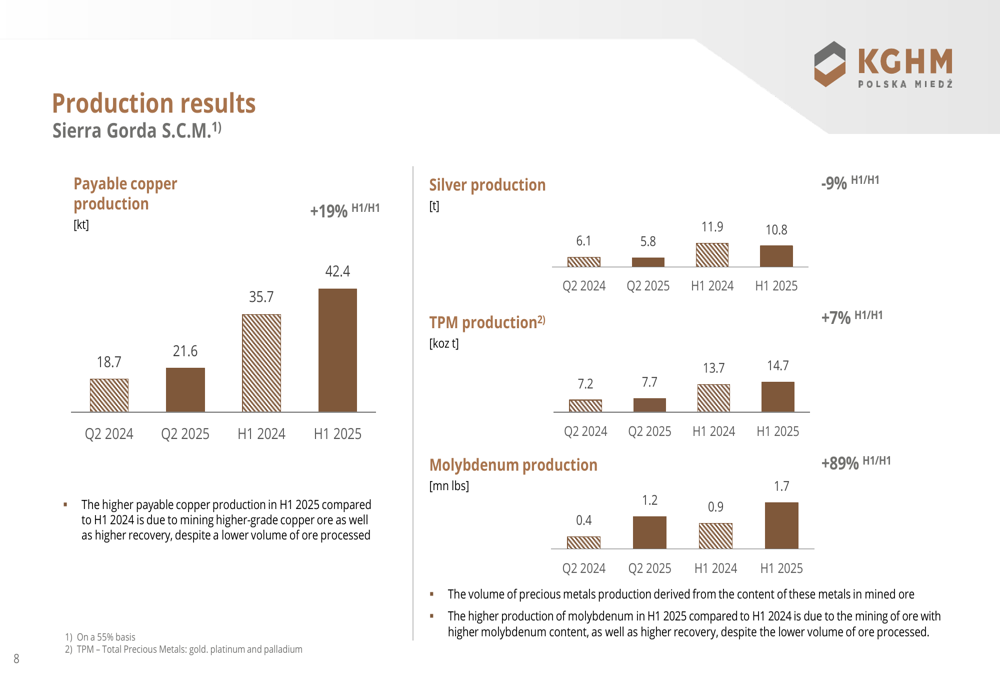

In contrast, Sierra Gorda S.C.M. demonstrated strong operational performance with a 19% increase in copper production to 42,400 tonnes, driven by higher copper content in ore and improved metal recovery despite lower ore processing volumes.

The following chart details copper production across the Group’s operations:

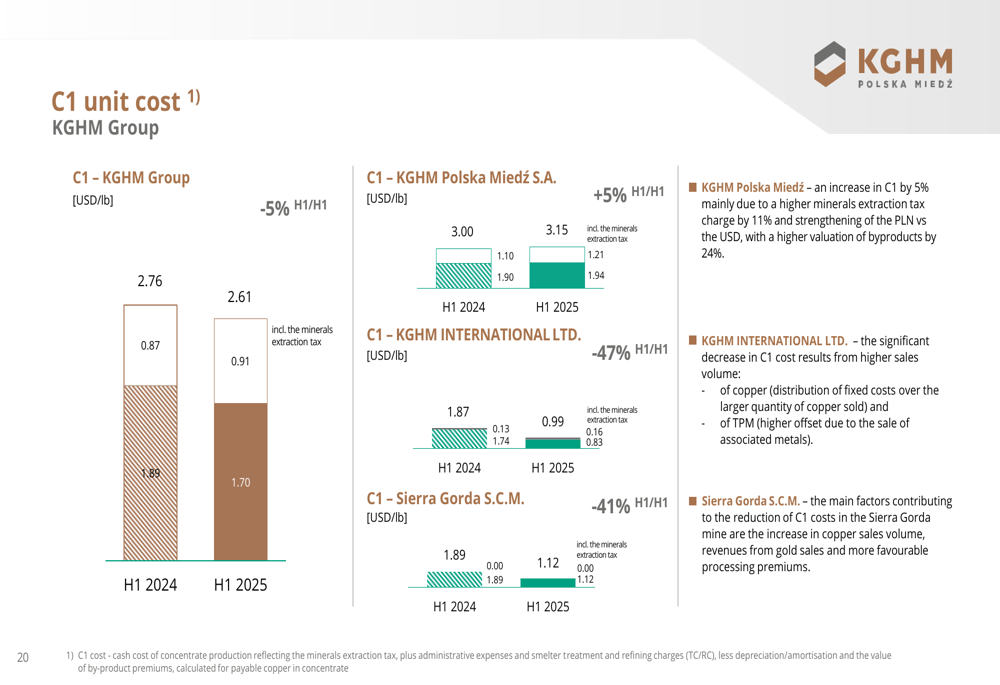

The divergent performance between segments was also evident in production costs. The Group’s C1 cash cost of copper production decreased by 5% to $1.70 per pound. Sierra Gorda achieved a remarkable 41% reduction in C1 cost to $1.12 per pound, while KGHM INTERNATIONAL LTD. saw a 47% decrease to $0.99 per pound. However, KGHM Polska Miedź S.A.’s C1 cost increased by 5% to $3.15 per pound.

As illustrated in the following cost breakdown:

Sierra Gorda’s exceptional performance extended beyond copper production, with molybdenum production increasing by 89% to 1.7 million pounds. The operation also generated significant cash flow, with total payments to KGHM Polska Miedź S.A. reaching $110.8 million in H1 2025.

The following chart details Sierra Gorda’s production metrics:

Capital Expenditures and Development Initiatives

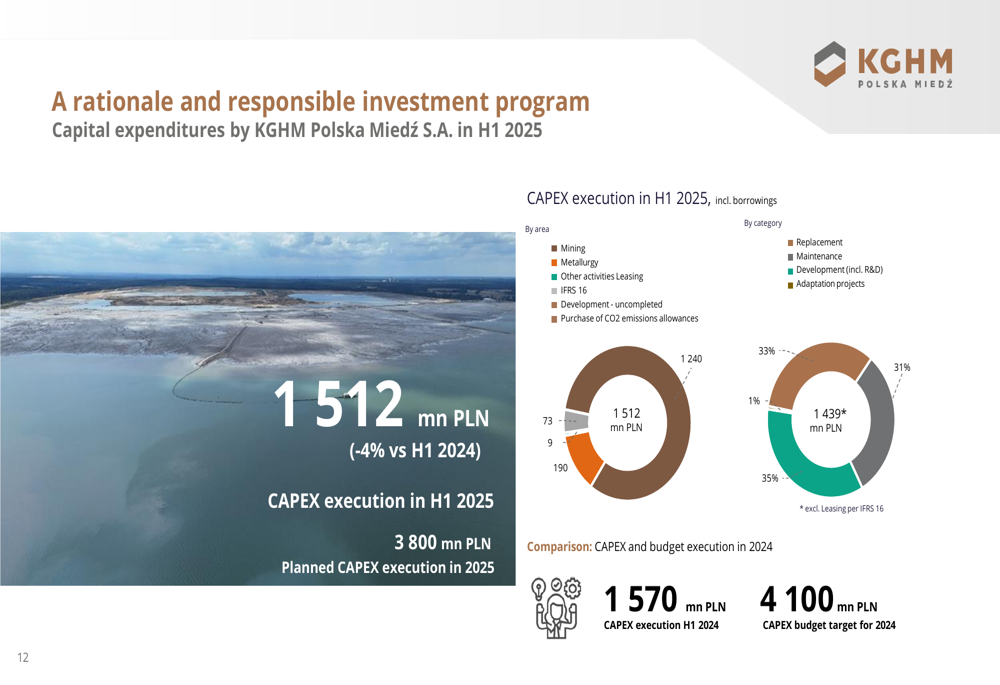

Despite profit pressure, KGHM maintained substantial capital investments, with CAPEX execution reaching 1,512 million PLN in H1 2025, a slight decrease of 4% compared to the previous year. The company plans total CAPEX of 3,800 million PLN for the full year 2025.

Mining investments accounted for the largest portion of capital expenditures, focusing on mine outfitting, machine park replacement, and deposit access programs to maintain future production capacity.

The following chart breaks down capital expenditures by category:

A significant portion of investments was directed toward shaft development as part of the company’s Deposit Access Program, which is crucial for maintaining production levels in Poland. The company highlighted progress on several shaft projects, including GG-1, GG-2, Retków, and Gaworzyce shafts.

Metallurgical investments totaled 190 million PLN, focusing on adaptation and replacement projects at metallurgical plants and concentrators to improve efficiency and environmental performance.

Forward-Looking Statements

KGHM faces several challenges going forward, including managing production costs in its Polish operations and mitigating exchange rate risks. However, the company’s international assets, particularly Sierra Gorda, show promising performance trends that could help offset domestic headwinds.

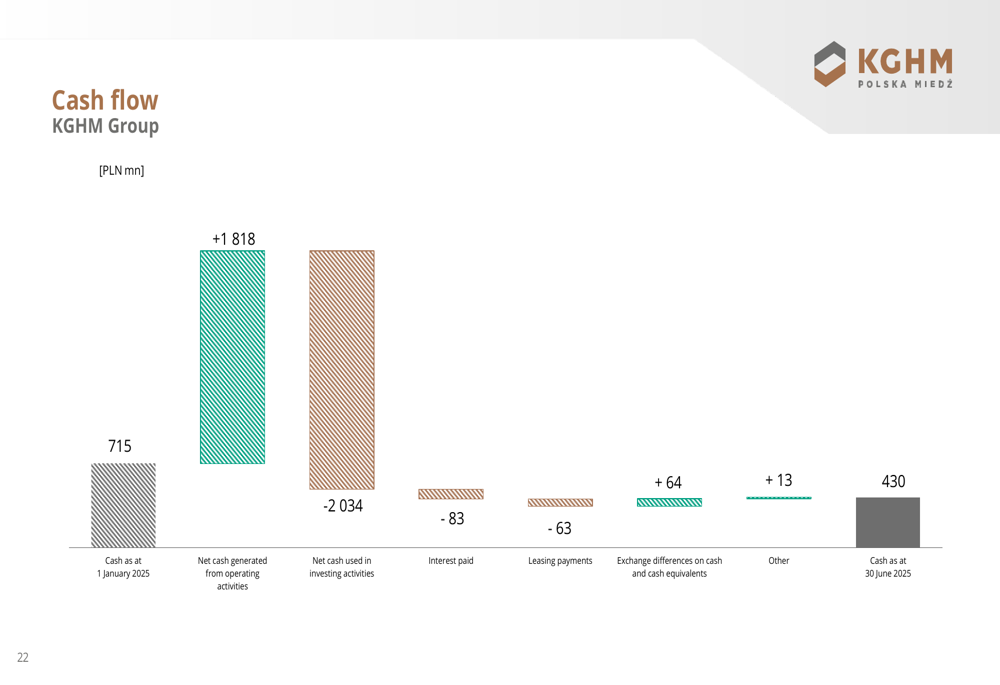

The Group’s cash position decreased from 715 million PLN at the beginning of 2025 to 430 million PLN by June 30, 2025, reflecting the significant capital investments made during the period. Operating activities generated 1,818 million PLN in cash, but this was outpaced by 2,034 million PLN used in investing activities.

While the company did not provide specific guidance for the remainder of 2025, the continued investment in development initiatives suggests confidence in long-term growth prospects despite short-term profit pressures. The contrasting performance between segments highlights the importance of the company’s diversified asset portfolio in navigating market volatility and operational challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.