AZTR receives NYSE delisting warning over equity requirement

Introduction & Market Context

Kid ASA (OB:KID), the Nordic home textiles retailer, presented its second quarter 2025 results on August 21, 2025, revealing continued revenue growth amid challenges from its warehouse consolidation project. The company’s stock closed at NOK 155.40 on August 20, down 1.02% ahead of the presentation, reflecting some investor caution about the company’s performance.

The quarter was marked by the operational launch of Kid’s new 57,000 square meter central warehouse in Sweden, a strategic move to consolidate logistics operations that previously operated separately for its Norwegian and Swedish/Finnish/Estonian markets. While this initiative promises long-term efficiency gains, the transition has introduced temporary operational challenges affecting the quarter’s profitability.

Quarterly Performance Highlights

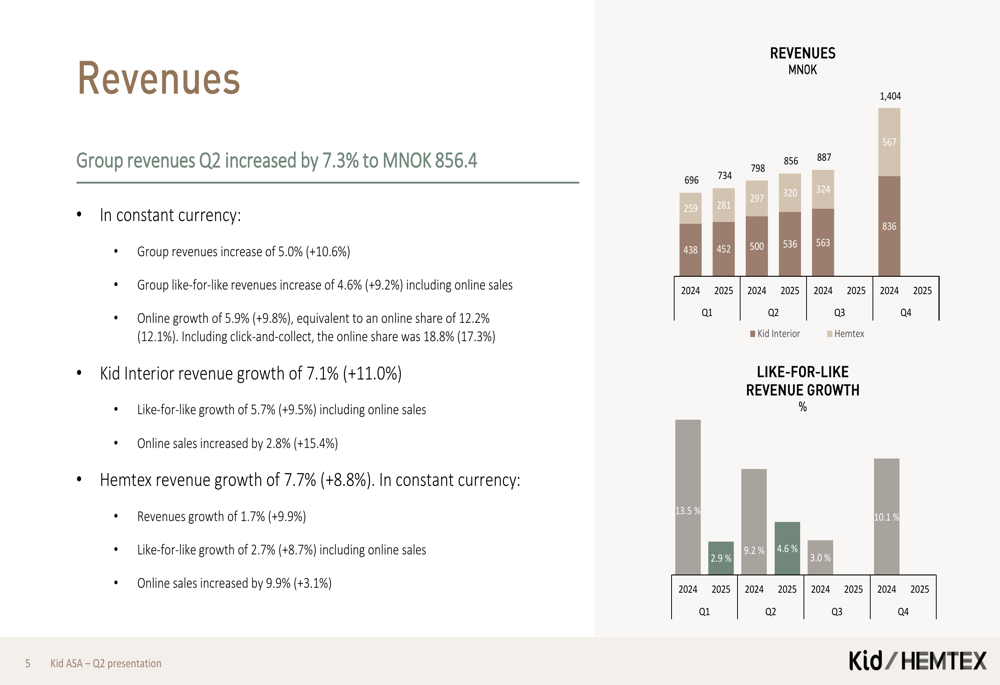

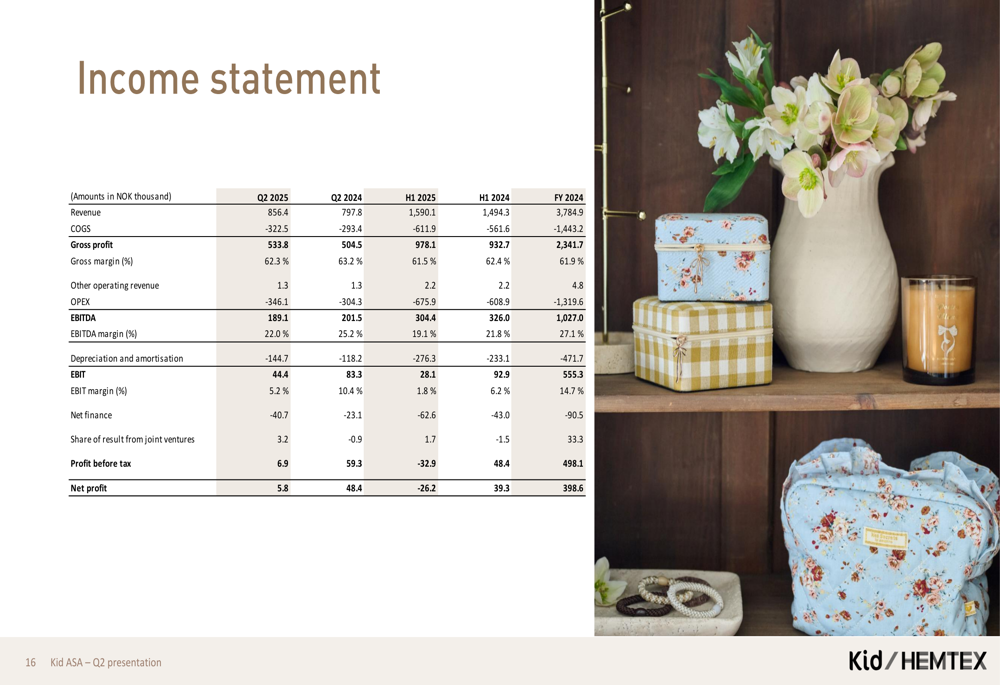

Kid ASA reported group revenues of MNOK 856.4 in Q2 2025, representing a 7.3% increase compared to the same period last year. Like-for-like revenue growth reached 4.6%, while online sales grew by 5.9%, accounting for 12.2% of total revenue. When including click-and-collect sales, the online share expanded to 18.8%, demonstrating the company’s strengthening omnichannel presence.

As shown in the following revenue performance chart:

Both of Kid’s retail segments contributed to the positive revenue development. Kid Interior, the company’s Norwegian operation, delivered 7.1% revenue growth with like-for-like growth of 5.7%. Meanwhile, Hemtex, which operates in Sweden, Finland, and Estonia, achieved 7.7% revenue growth in constant currency, with like-for-like growth of 2.7%.

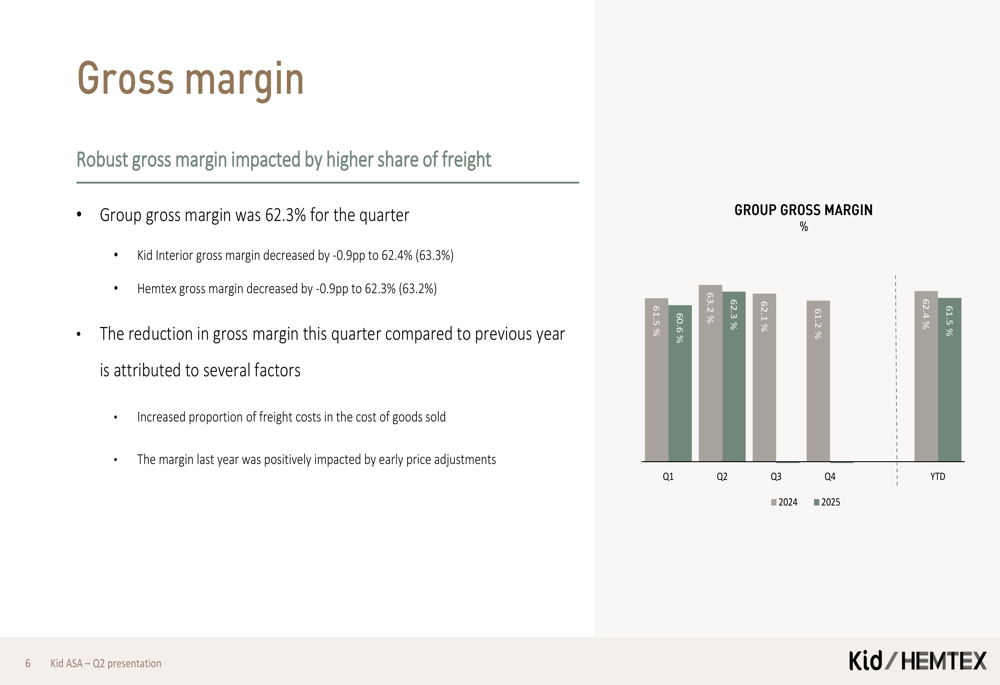

Despite the revenue gains, profitability metrics showed pressure. Gross margin decreased by 0.9 percentage points to 62.3%, attributed to an increased proportion of freight costs and the absence of early price adjustments that had positively impacted the previous year’s margin.

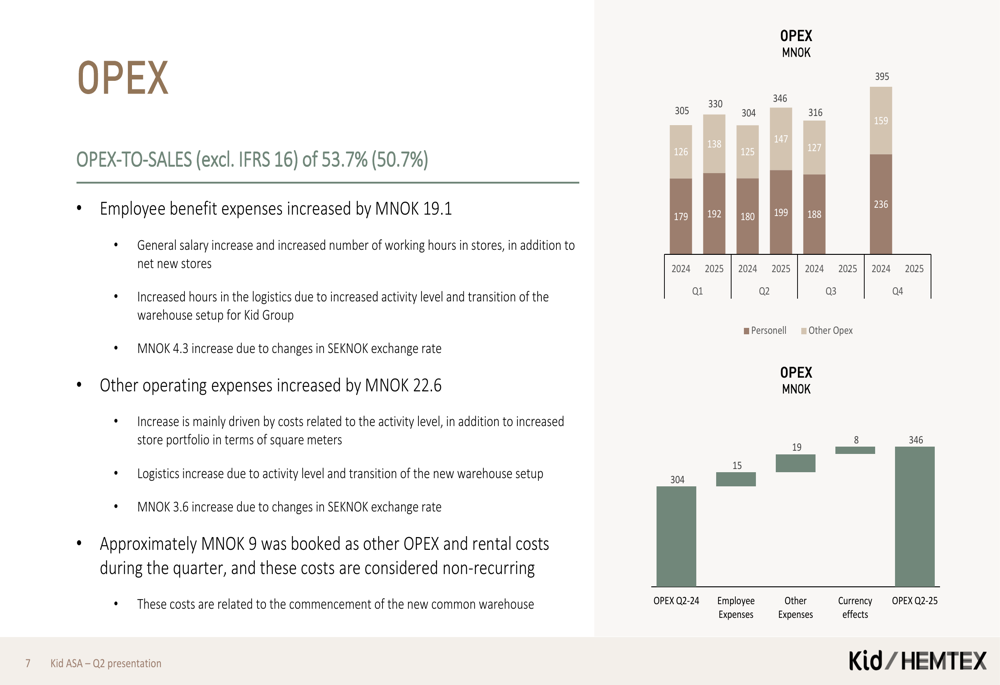

Operating expenses increased by 13.7% year-over-year, with the OPEX-to-sales ratio rising to 53.7% from 50.7% in Q2 2024. This increase was driven by general salary increases, expanded working hours, and approximately MNOK 9 in non-recurring costs related to the new warehouse launch.

Detailed Financial Analysis

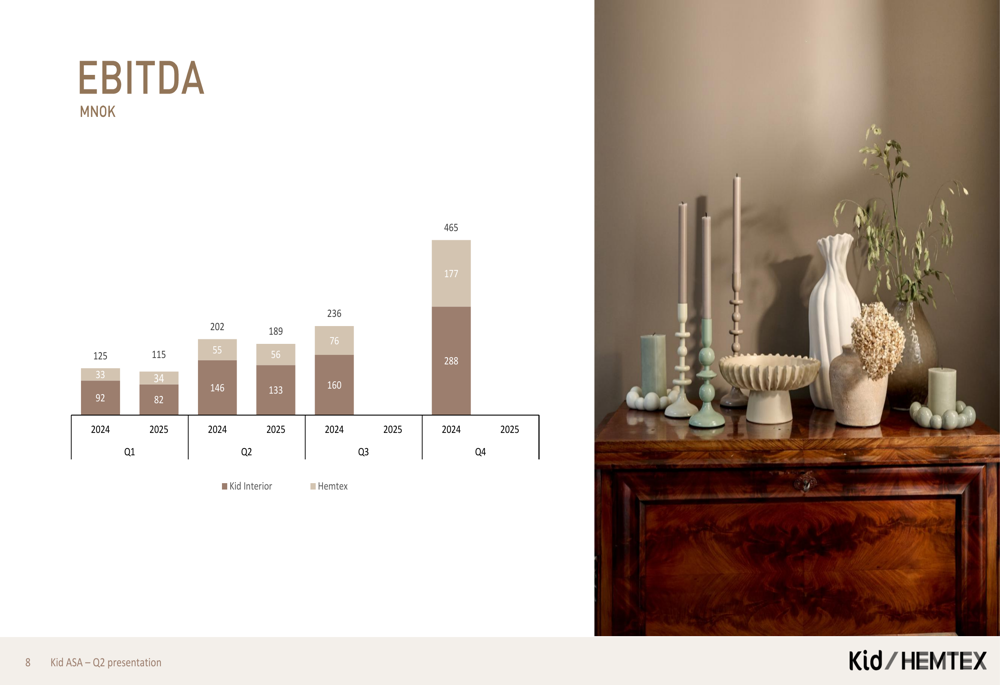

The combination of revenue growth, margin pressure, and increased operating expenses resulted in EBITDA of MNOK 189.1 for Q2 2025, down MNOK 12.4 from the same period last year. Kid Interior’s EBITDA declined to MNOK 133 from MNOK 146 in Q2 2024, while Hemtex maintained relatively stable EBITDA at MNOK 56.

The quarter’s net income was significantly impacted by a MNOK 25.0 impairment of right-of-use asset and MNOK 8.8 in disagio (foreign exchange losses), resulting in earnings per share of NOK -0.07, compared to NOK 1.19 in Q2 2024. This represents a substantial decline in profitability despite the revenue growth.

The comprehensive income statement shows the financial performance across key metrics:

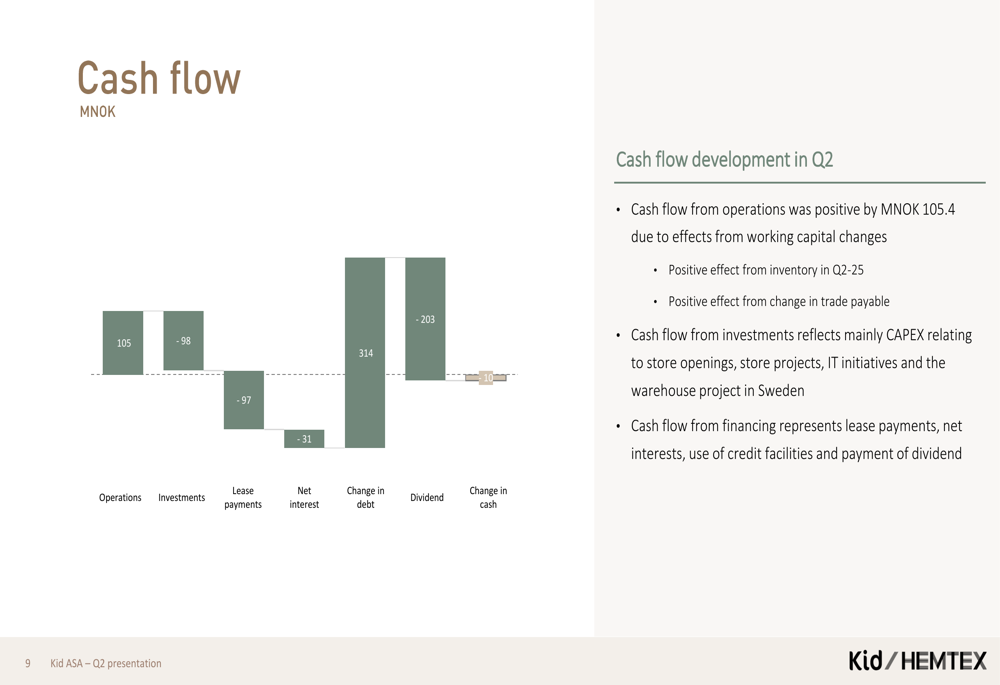

Cash flow from operations remained positive at MNOK 105.4, benefiting from working capital improvements, particularly in inventory management and trade payables. However, significant cash outflows were directed toward investments (MNOK -98), primarily for store openings, IT initiatives, and the warehouse project in Sweden.

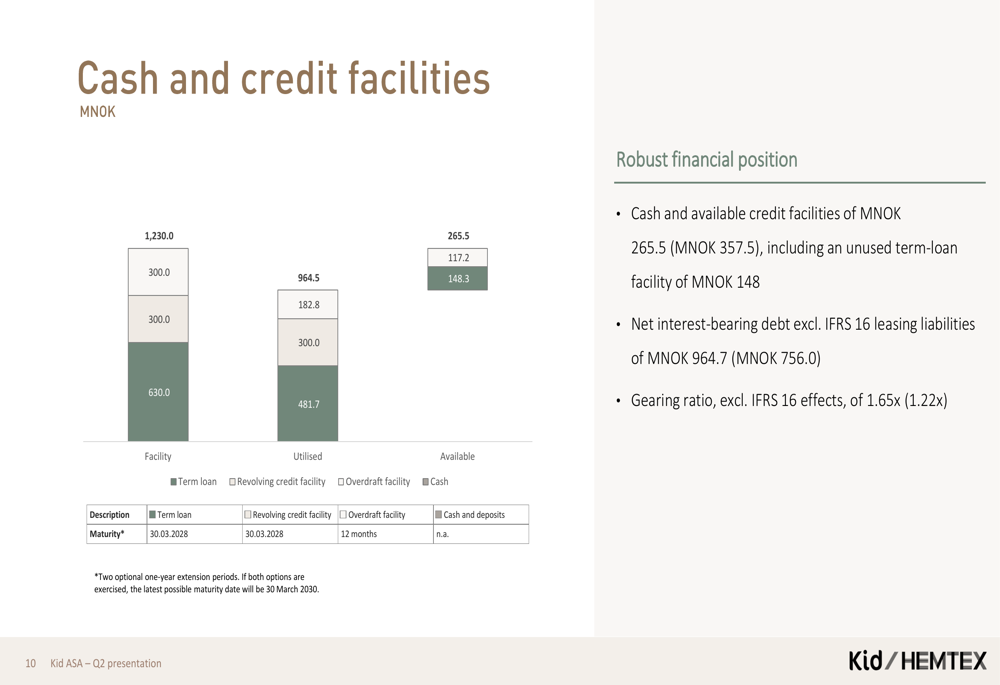

Kid’s financial position shows increased leverage, with net interest-bearing debt (excluding IFRS 16 leasing liabilities) rising to MNOK 964.7 from MNOK 756.0 a year earlier. The gearing ratio increased to 1.65x from 1.22x, reflecting the company’s investments in growth initiatives and the warehouse consolidation project.

Strategic Initiatives

The central warehouse project represents Kid’s most significant strategic initiative, aimed at capitalizing on operational synergies between its Norwegian and Swedish operations. The company noted that while the transition has introduced temporary efficiency challenges, performance is gradually improving, though it will take time before all solutions work seamlessly and the full saving potential materializes.

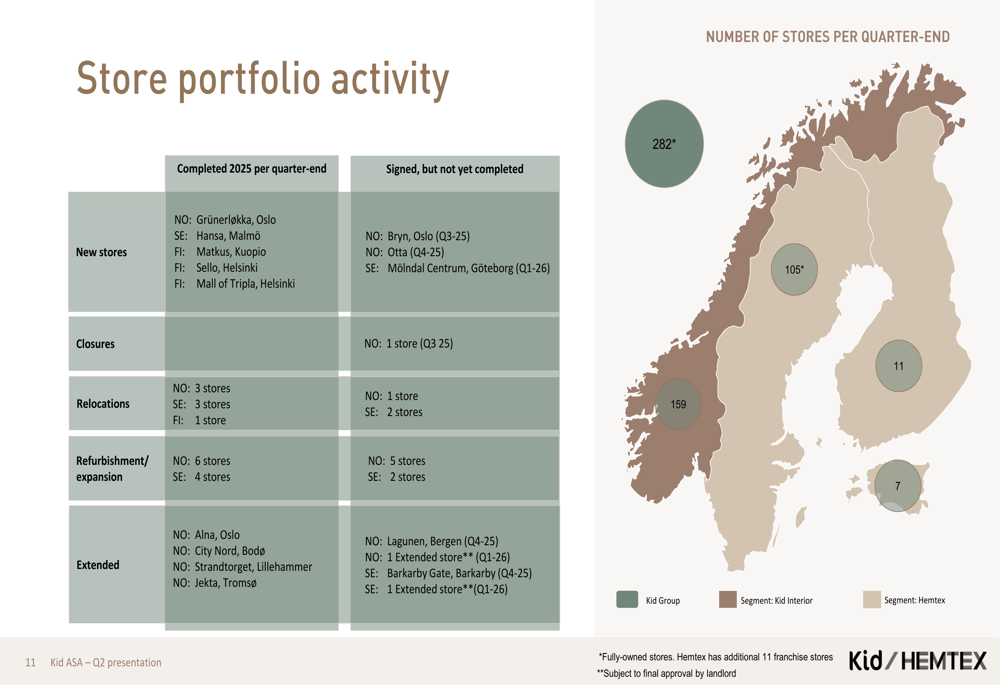

Store expansion continued during the quarter, with four new store openings (one Kid Interior and three Hemtex locations) and 15 completed store projects, including refurbishments and relocations. The company completed its stated ambition of establishing 15 "Extended" stores in Norway, which feature expanded product assortments.

Kid is also preparing for digital expansion, with plans to launch the Hemtex brand in Germany and other EU markets in Q4 2025. This represents an important step in the company’s international growth strategy beyond its Nordic home markets.

The company’s store portfolio shows its strong Nordic presence:

Forward-Looking Statements

Looking ahead to the second half of 2025, Kid plans eight additional store projects across its Kid Interior and Hemtex brands, including refurbishments, enlargements, and relocations. Two new "Extended" stores are scheduled to open—one in Norway and one in Sweden.

Management emphasized that the focus in coming periods will be on ramping up operations and implementing more automation solutions in the new warehouse to increase capacity, efficiency, and store inventory management. This suggests that the company expects the warehouse transition challenges to continue in the near term, with gradual improvements as operations stabilize.

The digital pilot for launching the Hemtex brand in Germany and other EU markets is progressing as planned, with the launch expected in Q4 2025. This initiative represents a potentially significant growth avenue for Kid beyond its current Nordic footprint.

Kid ASA’s Q2 2025 presentation reveals a company in transition—growing revenues while navigating operational challenges from its warehouse consolidation project. While the revenue performance demonstrates continued consumer demand for Kid’s home textile and decor offerings, the pressure on profitability metrics suggests that investors may need to exercise patience as the company works through its operational transformation to realize the full benefits of its strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.