Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Introduction & Market Context

Kimball Electronics (NASDAQ:KE) presented its fourth quarter fiscal 2025 results on August 14, 2025, highlighting sequential improvements in key financial metrics despite year-over-year revenue declines. The electronics manufacturing services provider reported progress in its strategic pivot toward medical manufacturing while demonstrating strong cash flow generation and significant debt reduction.

In premarket trading following the presentation, Kimball Electronics shares rose 4.91% to $22.00, building on the previous day’s close of $20.97. This positive market reaction suggests investors are encouraged by the company’s strategic direction and financial discipline despite top-line challenges.

Quarterly Performance Highlights

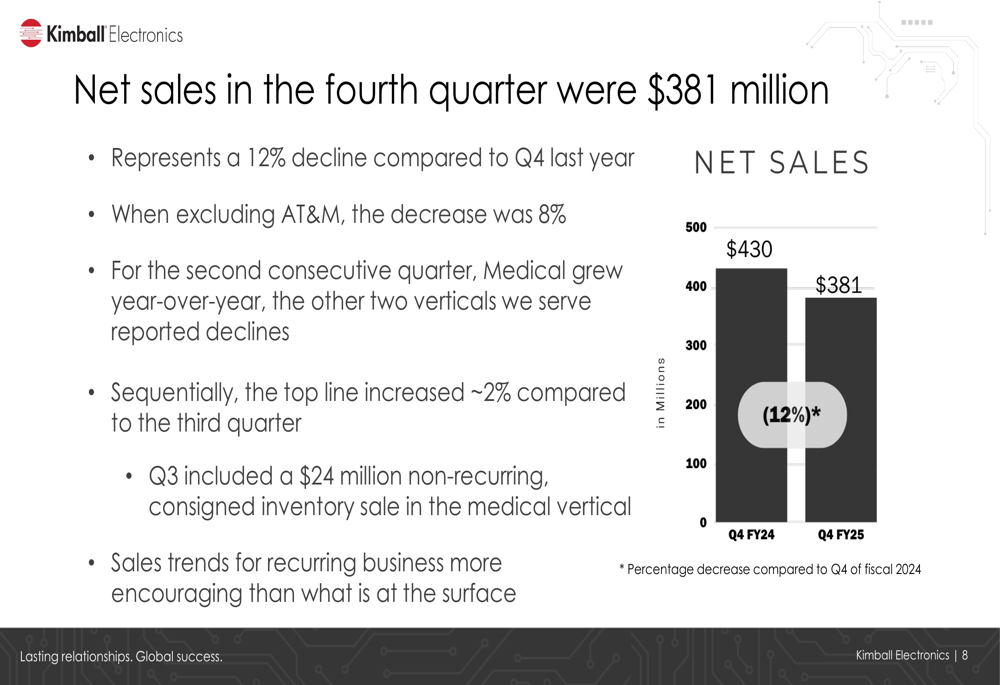

Kimball Electronics reported net sales of $381 million for Q4 FY2025, representing a 12% decline compared to the same period last year, or 8% when excluding the divested AT&M business. Despite the year-over-year decrease, sales increased approximately 2% sequentially from the third quarter.

As shown in the following chart of quarterly net sales:

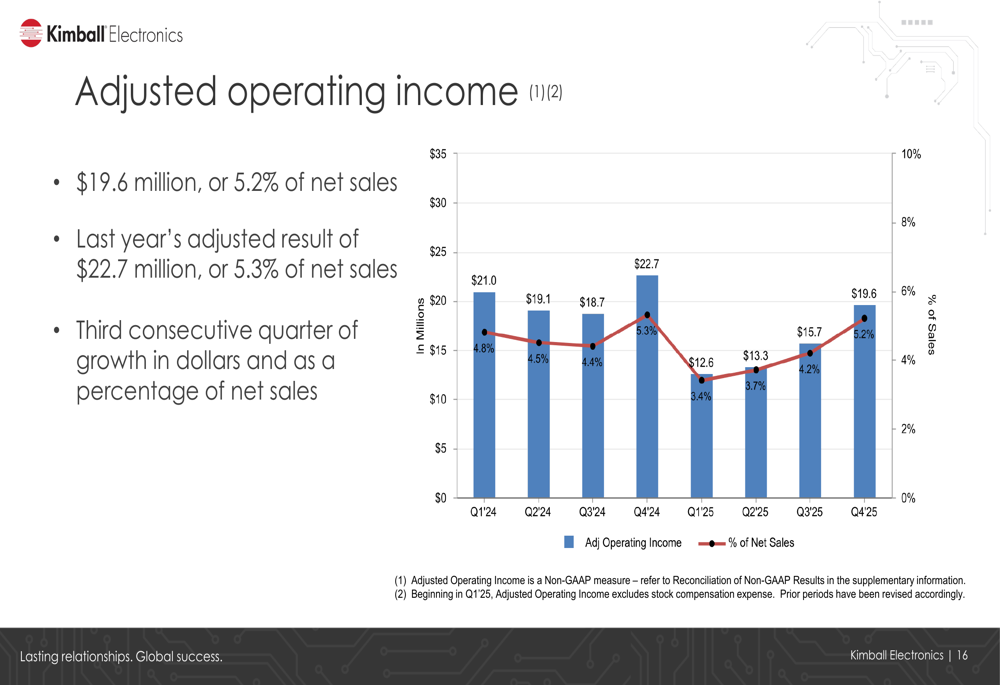

The company’s adjusted operating income was $19.6 million, or 5.2% of net sales, compared to $22.7 million, or 5.3% of net sales, in the prior year. This marks the third consecutive quarter of growth in adjusted operating income, both in dollars and as a percentage of net sales.

The following chart illustrates the trend in adjusted operating income:

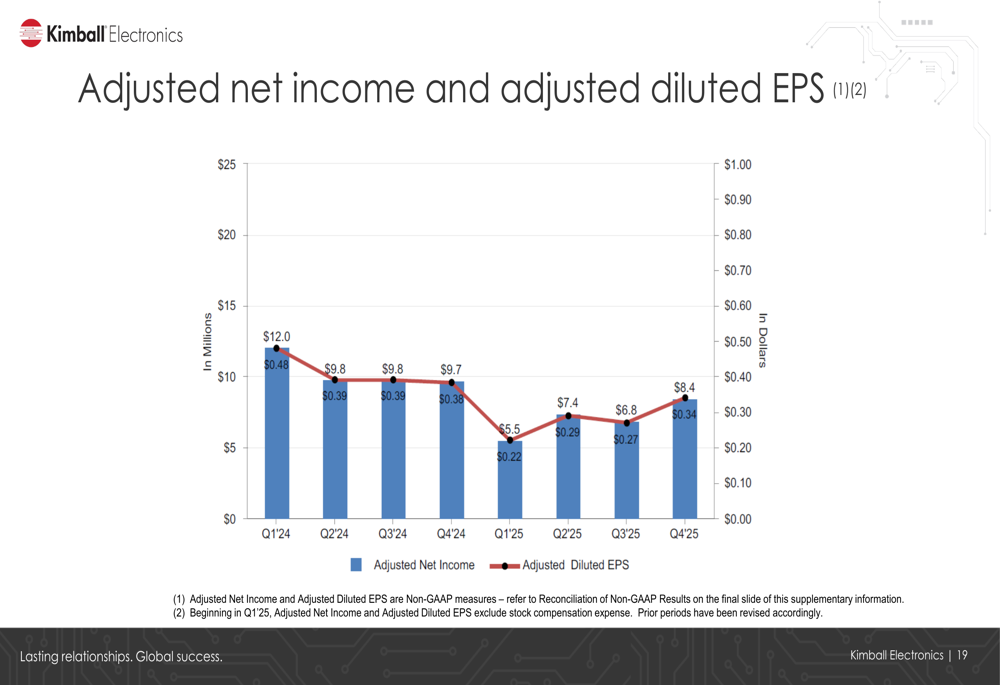

Adjusted diluted earnings per share came in at $0.34 for the quarter, compared to $0.38 in Q4 FY2024. The company’s effective tax rate was 48.3%, up from 44.0% in the same quarter last year.

The quarterly earnings trend is depicted in this chart:

Segment Performance Analysis

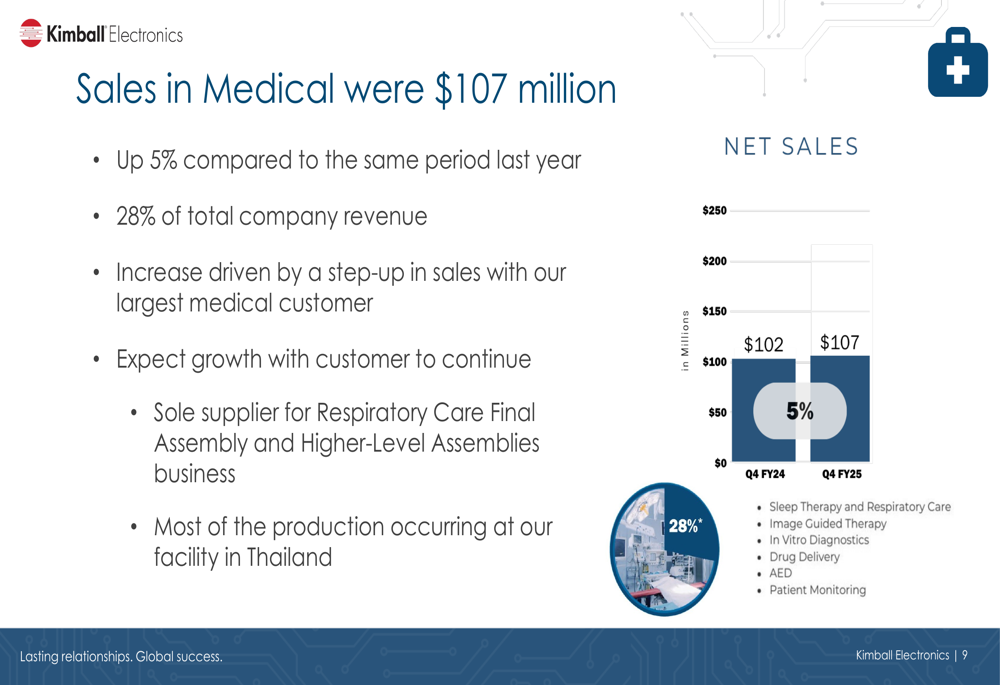

The medical segment emerged as a bright spot, with sales reaching $107 million, up 5% year-over-year and representing 28% of total company revenue. This growth was primarily driven by increased sales to the company’s largest medical customer, for whom Kimball serves as the sole supplier for respiratory care final assembly and higher-level assemblies.

The following chart shows the growth in medical segment sales:

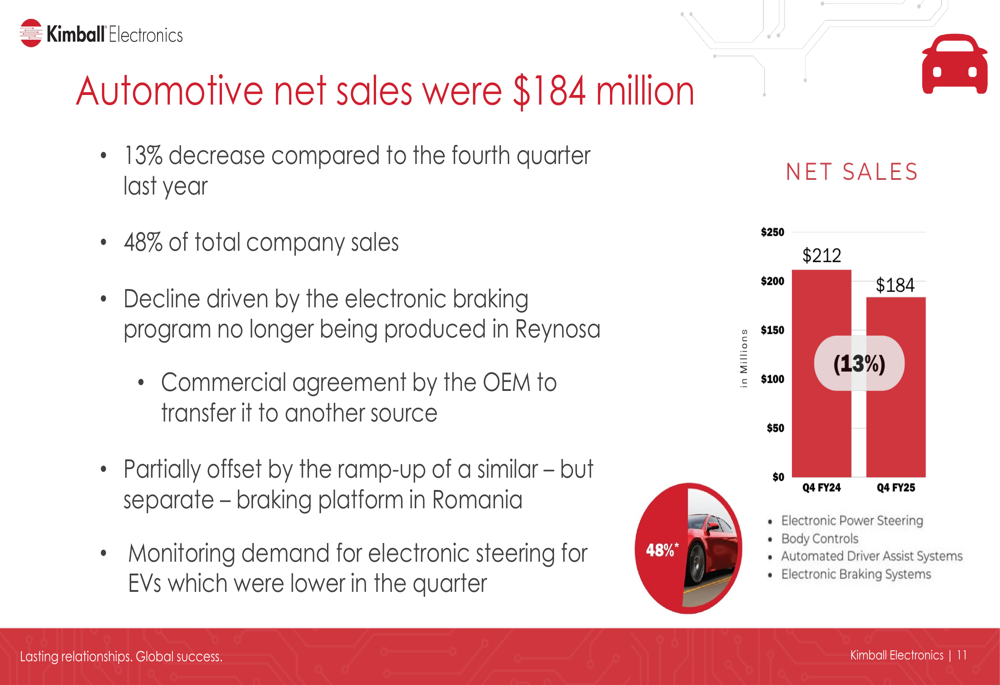

In contrast, the automotive segment, which accounts for 48% of total revenue, saw sales decline 13% year-over-year to $184 million. This decrease was primarily attributed to the end of an electronic braking program in Reynosa, partially offset by the ramp-up of a similar platform in Romania. The company also noted lower demand for electronic steering components for electric vehicles.

The automotive segment performance is illustrated here:

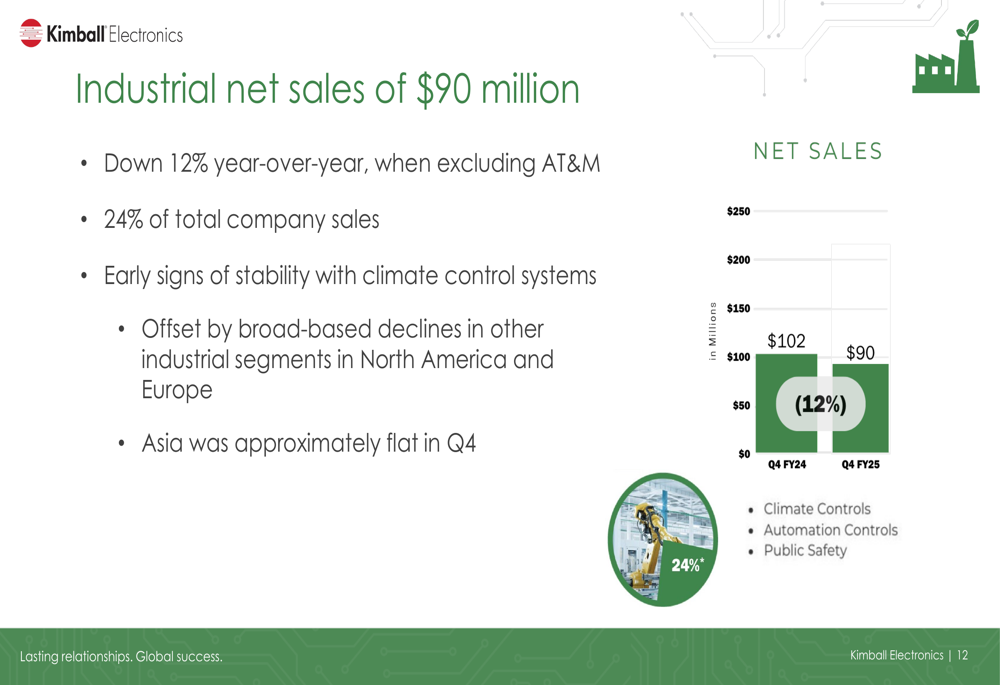

The industrial segment reported sales of $90 million, down 12% year-over-year when excluding AT&M, and representing 24% of total company revenue. While the company observed early signs of stability in climate control systems, this was offset by broad-based declines in other industrial segments in North America and Europe.

The industrial segment trend is shown in this chart:

Balance Sheet Improvements

Kimball Electronics demonstrated strong financial discipline with its sixth consecutive quarter of positive cash flow. Cash generated by operating activities in Q4 was $78.1 million, bringing the full-year total to a record $183.9 million. Cash and cash equivalents stood at $88.8 million at the end of the quarter.

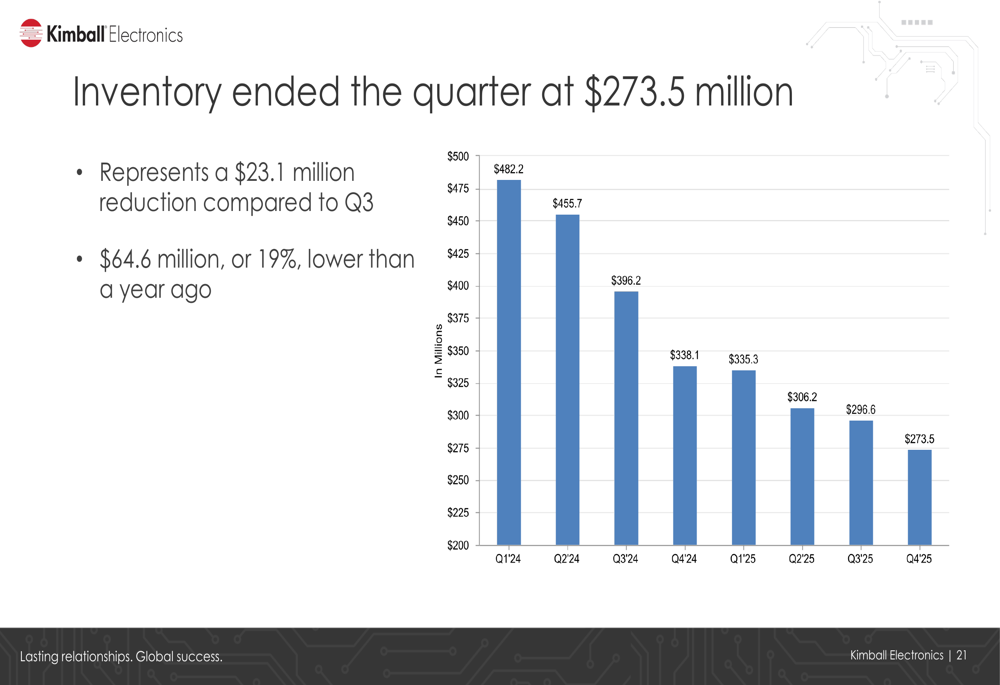

The company significantly improved its inventory management, reducing inventory levels to $273.5 million, down 19% from the prior year. Cash conversion days improved to 85 days, compared to 100 days in Q4 FY2024 and 99 days in Q3 FY2025, representing the lowest level in three years.

The inventory reduction trend is clearly visible in this chart:

Perhaps most notably, borrowings were reduced to $147.5 million, down $31.3 million from the third quarter and a substantial $147.3 million (50%) lower than at the beginning of the fiscal year. This significant debt reduction strengthens the company’s balance sheet and provides flexibility for future investments.

Strategic Initiatives

A key focus of the presentation was Kimball Electronics’ strategic pivot toward expanding its medical contract manufacturing organization (CMO) capabilities. The company highlighted its new medical facility in Indianapolis, which provides expanded production capabilities including cold chain management, complete device assembly, and precision-molded plastics.

The facility currently manufactures medical disposables, single-use surgical instruments, and selected drug delivery devices, with plans to explore applications in cardiology, orthopedics, minimally invasive surgery, and surgical instruments and packaging.

CEO Ric Phillips emphasized that the medical market presents a compelling opportunity to diversify revenue and leverage the company’s core strengths in complex, regulated manufacturing environments. The medical CMO strategy is expected to yield higher EBITDA margins while serving blue-chip customers with long product life cycles and a high degree of visibility.

Forward-Looking Statements

Looking ahead to fiscal 2026, Kimball Electronics characterized the upcoming year as a "transition" period. The company provided guidance for net sales of $1.350-$1.450 billion, representing a 2-9% decrease compared to fiscal 2025. Adjusted operating income is expected to be 4.0-4.25% of net sales, compared to 4.1% in fiscal 2025.

Management explained that two significant events from fiscal 2025 impact the forward guidance: the loss of the braking program in Reynosa, which will have a $60 million unfavorable impact, and the non-recurrence of a large consigned inventory sale that occurred in Q3. Excluding these items, the company expects its top line to be approximately flat year-over-year, with modest growth in medical and industrial offset by a decline in automotive.

Capital expenditures are projected at $50-60 million for fiscal 2026, with approximately $30 million allocated to the new Indianapolis facility and the remainder supporting growth, automation, and maintenance.

The company anticipates a return to growth in fiscal 2027, with better capacity utilization expected to result in higher margins. Management remains committed to generating positive cash flow and deploying capital toward growing its CMO business, with both organic investments and potential inorganic options to augment its position in the medical manufacturing space.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.