Microsoft’s data-center shortages to persist longer than expected - Bloomberg

Introduction & Market Context

Kimberly-Clark Corporation (NYSE:KMB) released its first quarter 2025 earnings presentation on April 22, 2025, revealing mixed results as the company continues its multi-year "Powering Care" transformation strategy. The consumer products giant reported an organic sales decline but maintained strong productivity gains and strategic restructuring initiatives aimed at long-term growth.

The stock reacted negatively to the results in pre-market trading, down 1.88% to $137.44, reflecting investor concerns about the sales decline despite the company’s insistence that results remain consistent with its full-year plan.

Quarterly Performance Highlights

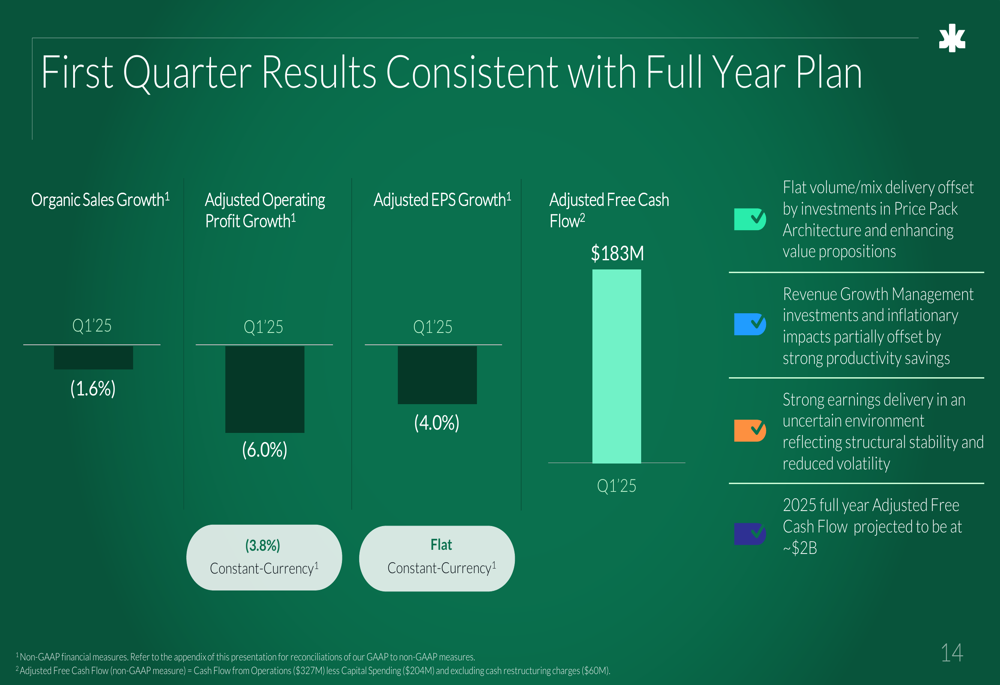

Kimberly-Clark’s Q1 2025 financial results showed an organic sales decline of 1.6%, while adjusted operating profit fell 6.0% and adjusted earnings per share decreased 4.0%. The company generated $183 million in adjusted free cash flow during the quarter, with full-year projections maintained at approximately $2 billion.

As shown in the following chart of key financial metrics:

Management emphasized that flat volume/mix delivery was offset by investments in Price Pack Architecture and enhancing value propositions. The company’s revenue growth management investments and inflationary impacts were partially offset by strong productivity savings, which reached 5.2% of adjusted cost of goods sold in Q1.

Strategic Initiatives

Kimberly-Clark’s "Powering Care" strategy, introduced in 2024, focuses on three key pillars: accelerating pioneering innovation, optimizing margin structure, and rewiring the organization for growth. The company has made significant progress on all three fronts in Q1 2025.

The company’s approach to innovation is illustrated in its strategy to cascade innovation across different price points:

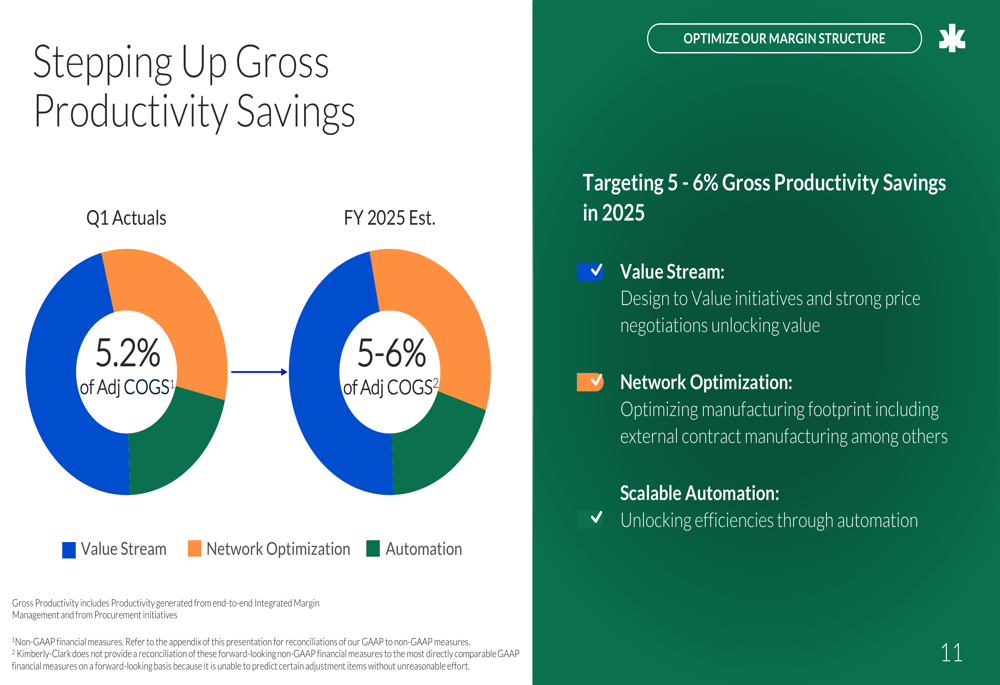

In the productivity realm, Kimberly-Clark has made substantial progress in stepping up gross productivity savings, as shown in the following chart:

The company is targeting 5-6% of adjusted COGS in productivity savings for full-year 2025, with Q1 already delivering 5.2%. These savings are expected to come from value stream initiatives, network optimization, and scalable automation.

On the organizational front, Kimberly-Clark began exiting the private label diaper business in the U.S. in mid-Q1 and has started to see transformation-related SG&A savings flow through with year-on-year cost reduction in Q1. The company established a new Global Growth Organization in December to drive greater global efficiency and effectiveness in marketing and go-to-market capabilities.

Product Innovation Highlights

Kimberly-Clark continues to focus on product innovation across its portfolio. In Indonesia, the company’s adult care business has shown impressive results with thinner, more breathable solutions:

The Confidence Daily Fresh product line in Indonesia has delivered 37% organic growth and 31% volume growth, driven by products that are 30% thinner and more breathable.

Similarly, the Poise brand has shown strong momentum in addressing stigma around light incontinence:

With 6.6% consumption growth in the U.S., a 26% increase in sales year-over-year at a key online customer, and approximately 30 basis points of share gain in the light incontinence category, Poise demonstrates Kimberly-Clark’s ability to grow through innovation and marketing.

Regional Performance Analysis

Kimberly-Clark’s performance varied significantly by region in Q1 2025. North America showed relatively stable results with an organic sales decline of 0.6% but operating profit growth of 1.3%. The region maintained a strong operating margin of 25.4%.

International Personal Care faced more significant challenges with an organic sales decline of 2.8% and an operating profit decline of 19.8%. The segment’s operating margin stood at 14.0%. Management noted increased investment in price-value propositions as consumer environments evolve across Asia and Latin America.

International Family Care & Professional reported an organic sales decline of 2.3% and an operating profit decline of 3.6%, with an operating margin of 13.4%. Volume growth of 0.5% was offset by increased price investment, primarily in Western Europe as competition intensified.

2025 Outlook

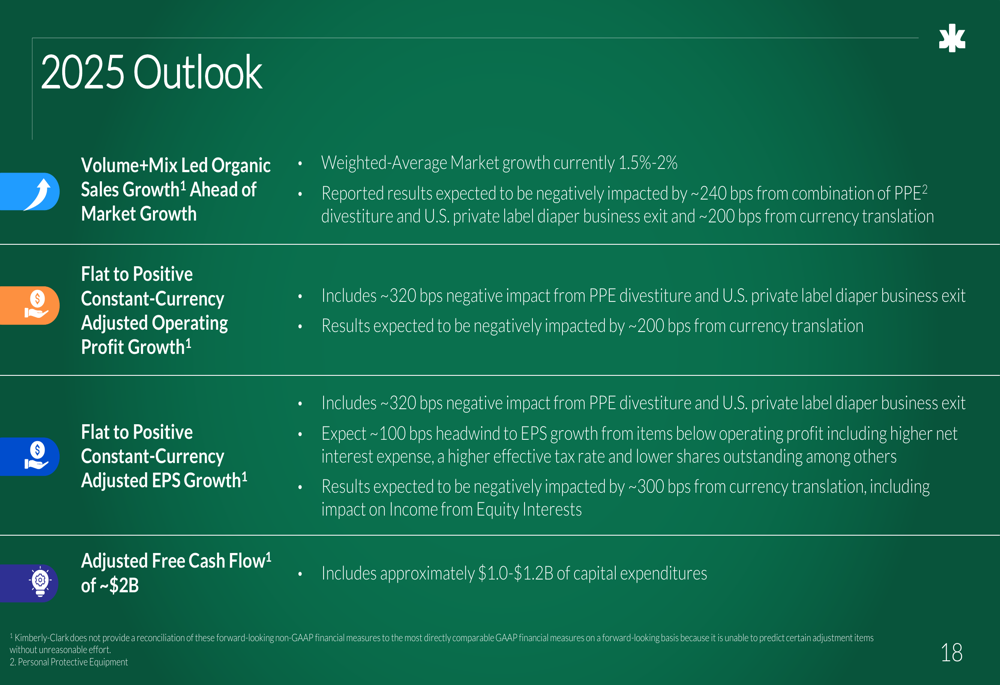

Despite the mixed Q1 results, Kimberly-Clark maintained its full-year 2025 outlook, as detailed in the following slide:

The company expects volume and mix-led organic sales growth ahead of market growth (currently estimated at 1.5%-2%). However, reported results are expected to be negatively impacted by approximately 240 basis points from the combination of the PPE divestiture and U.S. private label diaper business exit, plus an additional 200 basis points from currency translation.

Kimberly-Clark anticipates flat to positive constant-currency adjusted operating profit growth and adjusted EPS growth, though both metrics will face headwinds from divestitures, business exits, and currency translation. The company continues to project adjusted free cash flow of approximately $2 billion for the full year.

Conclusion

Kimberly-Clark’s Q1 2025 results present a mixed picture as the company continues its transformation journey. While organic sales declined, the company maintained strong productivity gains and made progress on strategic initiatives. The shift from pricing-led to volume/mix-led growth faces challenges in the current consumer environment, particularly in certain international markets.

The company’s focus on innovation, productivity, and organizational restructuring aims to position it for long-term growth, but investors will be watching closely to see if the volume-led strategy can deliver improved results in subsequent quarters. With the stock trading at $137.44 in pre-market, down 1.88% from its previous close of $140.07, the market appears cautious about the company’s near-term prospects despite management’s confidence in the full-year outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.