Intel stock extends gains after report of possible U.S. government stake

Introduction & Market Context

Kimco Realty (NYSE:KIM), one of the nation’s largest publicly traded owners and operators of open-air, grocery-anchored shopping centers, revealed strong performance metrics in its second quarter 2025 investor presentation. The company continues to benefit from its strategic focus on necessity-based retail in high-barrier-to-entry suburban markets.

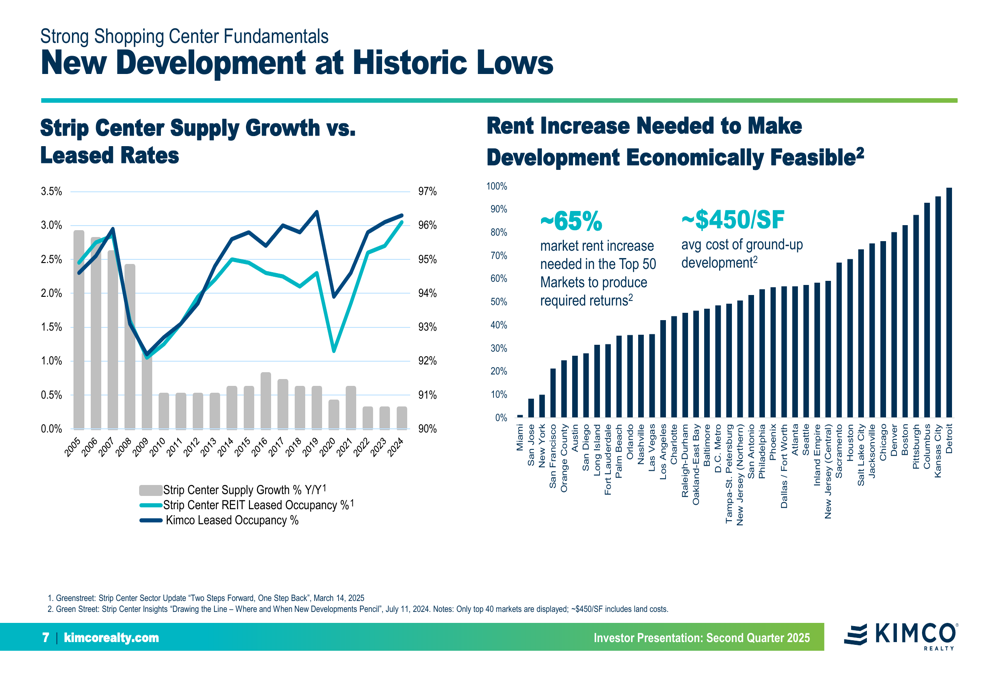

The presentation highlighted how favorable market conditions are supporting Kimco’s business model, with new retail development at historic lows creating a supply-constrained environment. This limited new supply, coupled with high occupancy rates across the sector, has strengthened landlords’ negotiating positions.

As shown in the following chart illustrating strip center supply growth versus leased occupancy rates, new development has remained minimal while occupancy has trended upward:

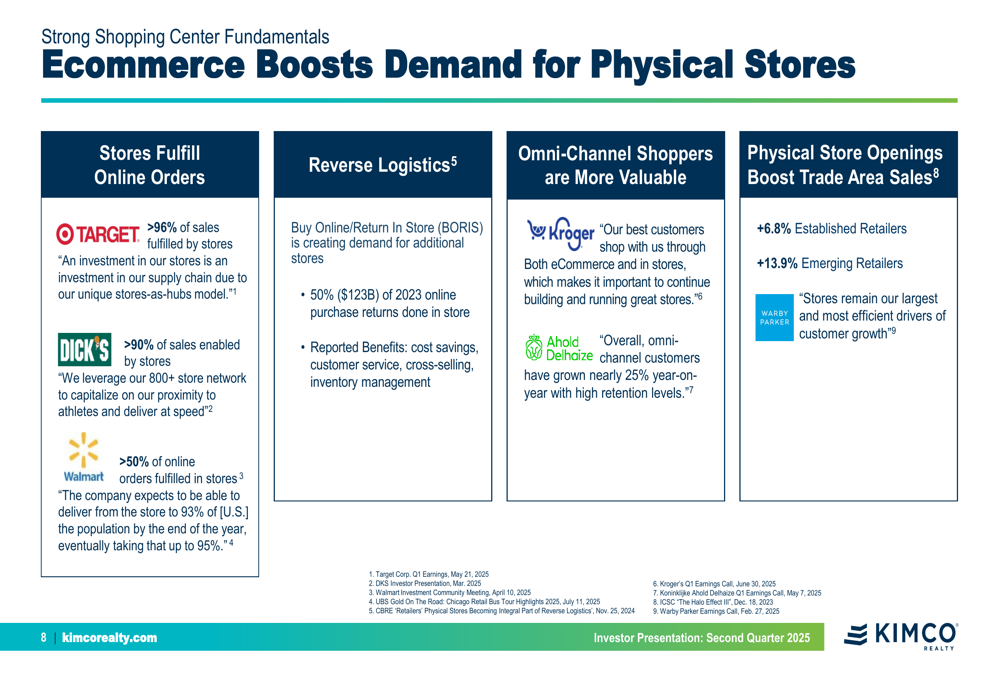

Additionally, Kimco emphasized how e-commerce is actually boosting demand for physical retail space rather than diminishing it. The company noted that major retailers are increasingly using their stores to fulfill online orders, with Target (NYSE:TGT) fulfilling over 96% of sales through stores and Walmart (NYSE:WMT) fulfilling more than 50% of online orders in stores.

Quarterly Performance Highlights

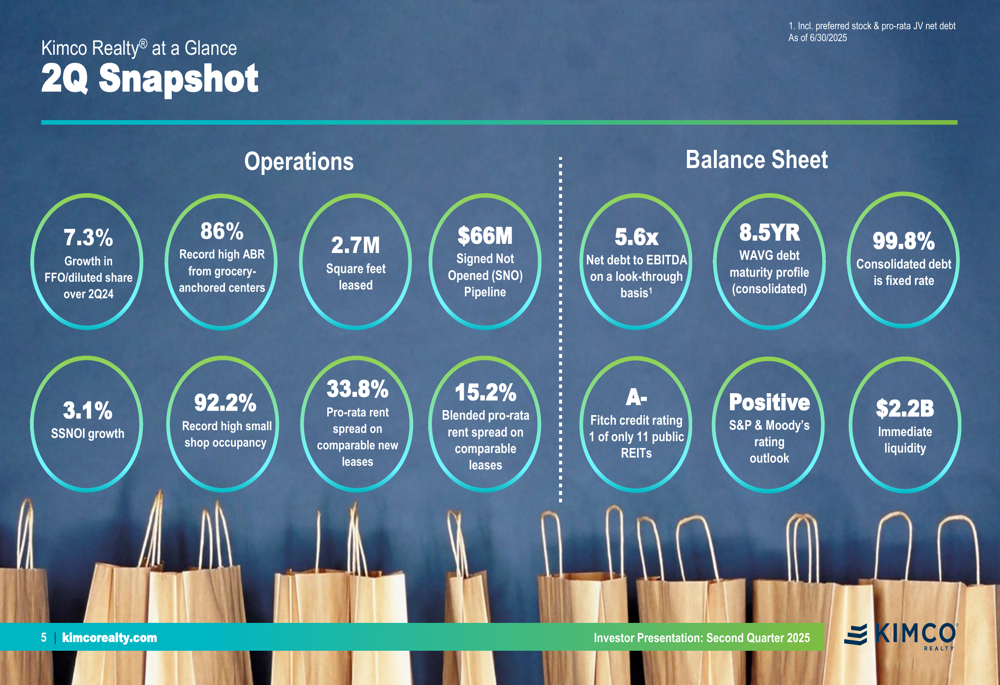

Kimco reported strong financial and operational results for Q2 2025. The company achieved 7.3% growth in funds from operations (FFO) per diluted share compared to Q2 2024, demonstrating solid momentum in its core business.

The following snapshot highlights key operational and balance sheet metrics from the quarter:

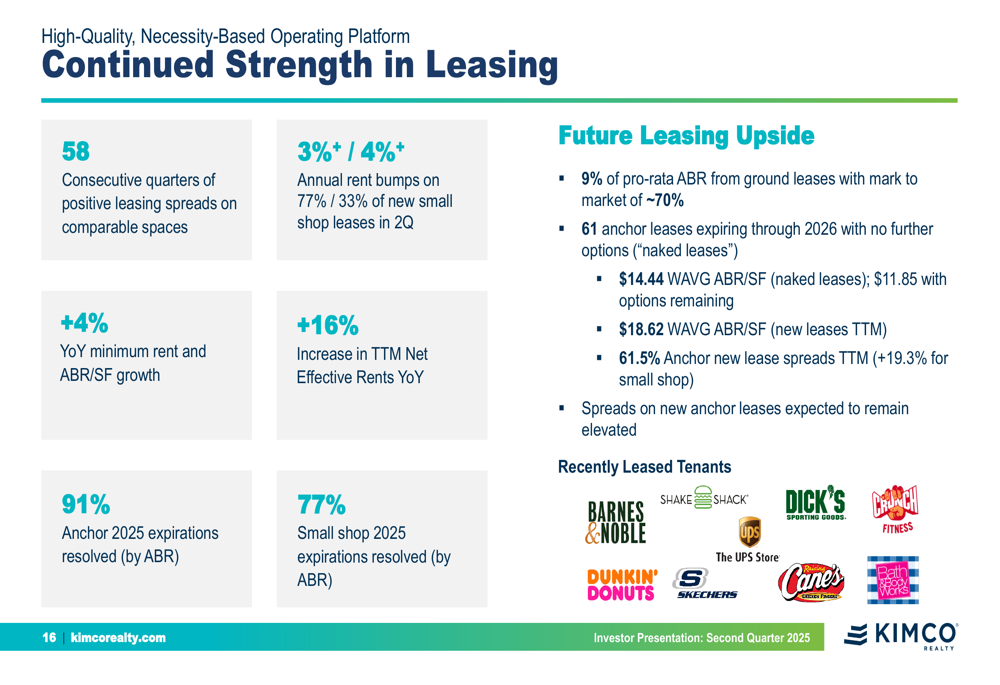

Particularly notable was the company’s leasing performance, with 2.7 million square feet leased during the quarter. Small shop occupancy reached a record high of 92.2%, while pro-rata rent spreads on comparable new leases were an impressive 33.8%. The blended pro-rata rent spread on comparable leases was 15.2%.

Kimco has maintained consistent leasing momentum, with 58 consecutive quarters of positive leasing spreads on comparable spaces. The company has already resolved 91% of anchor and 77% of small shop 2025 lease expirations (by ABR).

Strategic Initiatives

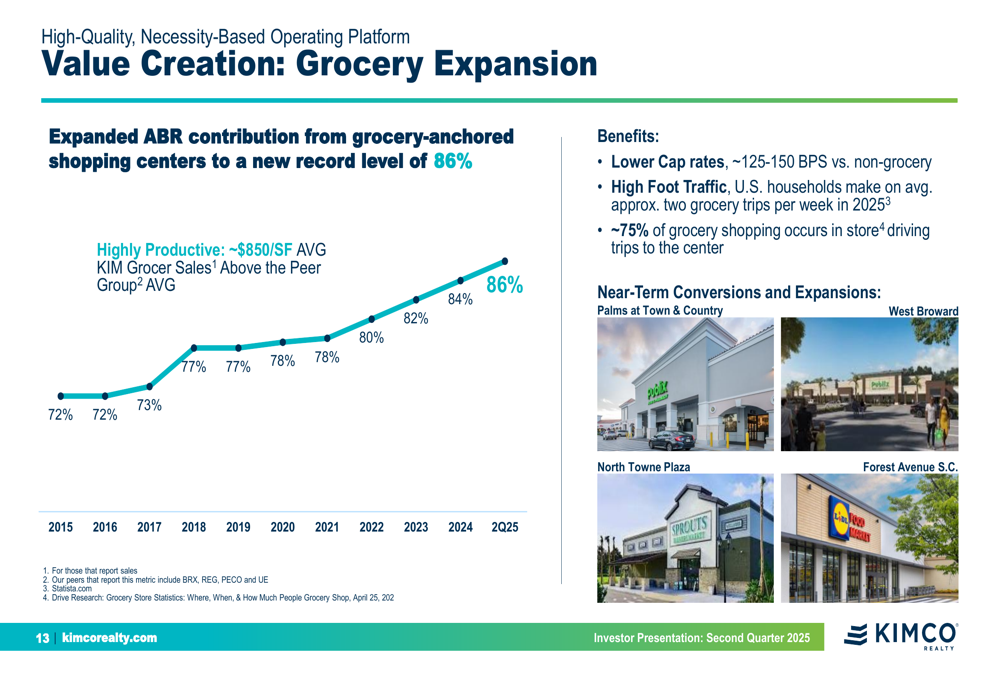

Kimco’s strategy centers around providing essential, necessity-based goods and services in high-barrier-to-entry suburban locations. The company has been strategically increasing its exposure to grocery-anchored centers, which now account for a record 86% of annual base rent (ABR), up from 72% in 2015.

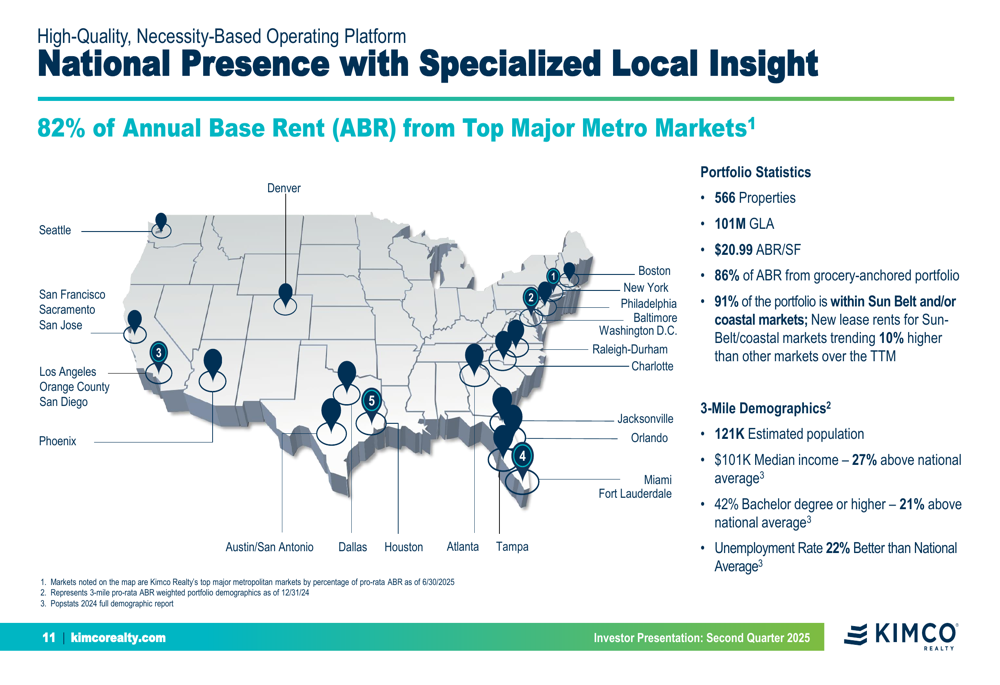

The company maintains a geographically diversified portfolio with a focus on top metropolitan markets. According to the presentation, 82% of ABR comes from major metro markets, and 91% of the portfolio is within Sun Belt and/or coastal markets.

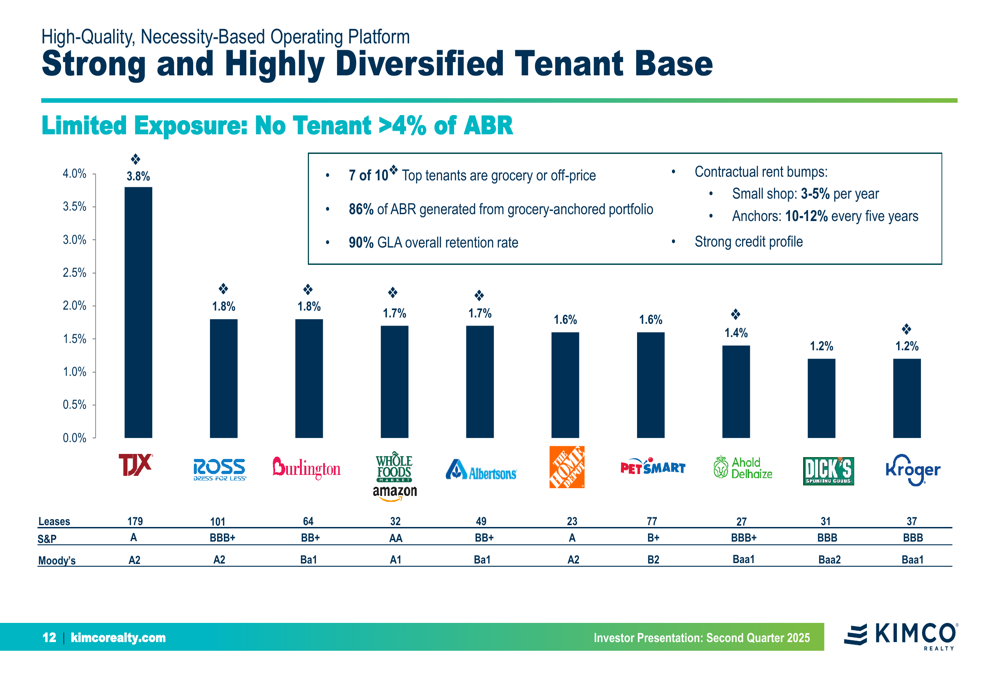

Tenant diversification remains a key strength, with no tenant accounting for more than 4% of ABR. Seven of Kimco’s top 10 tenants are grocery or off-price retailers, providing stability and consistent foot traffic to its centers.

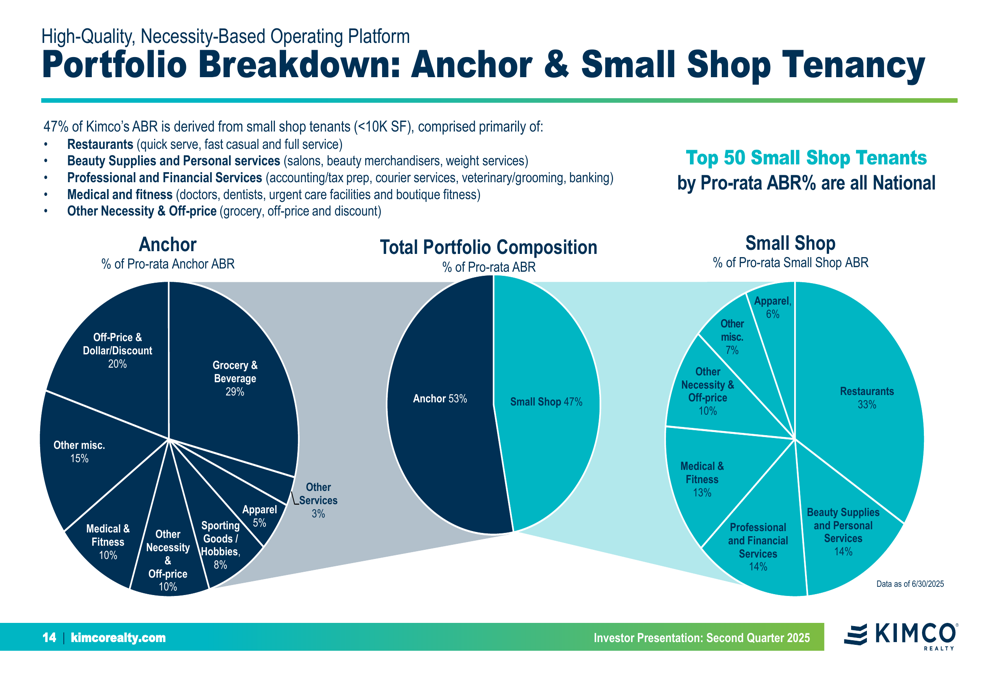

Kimco’s portfolio is well-balanced between anchor tenants (53% of ABR) and small shop tenants (47% of ABR). The small shop component is particularly valuable as it typically generates higher rents per square foot and provides services that complement the anchor retailers.

Balance Sheet Strength & Capital Allocation

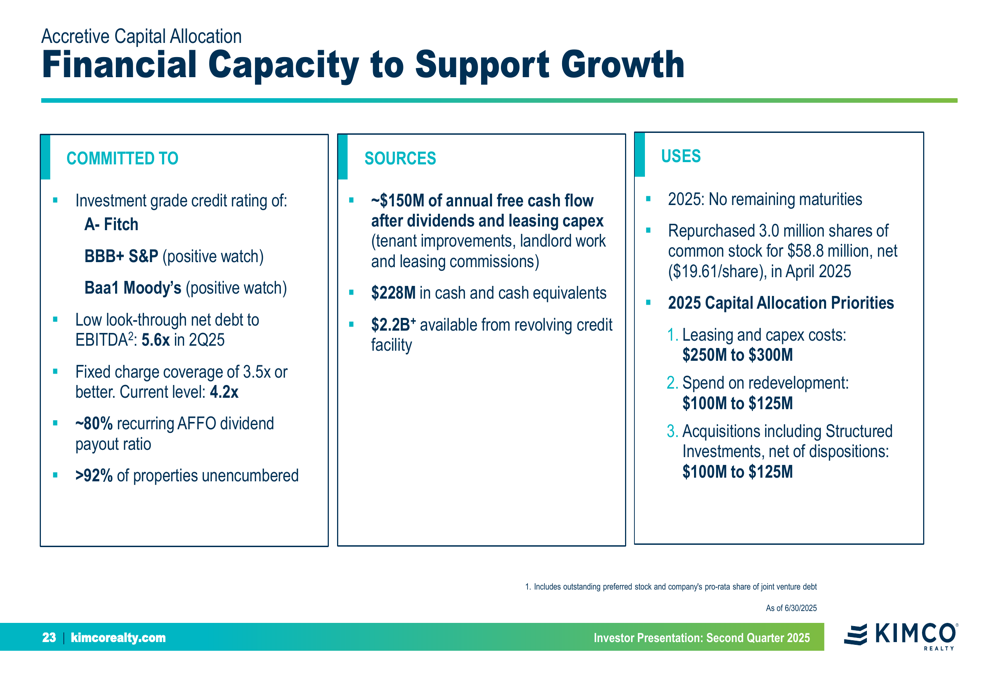

Kimco emphasized its financial strength, maintaining an A- credit rating from Fitch (one of only 11 public REITs with such a rating) and positive outlooks from S&P and Moody’s. The company reported a net debt to EBITDA ratio of 5.6x on a look-through basis and immediate liquidity of $2.2 billion.

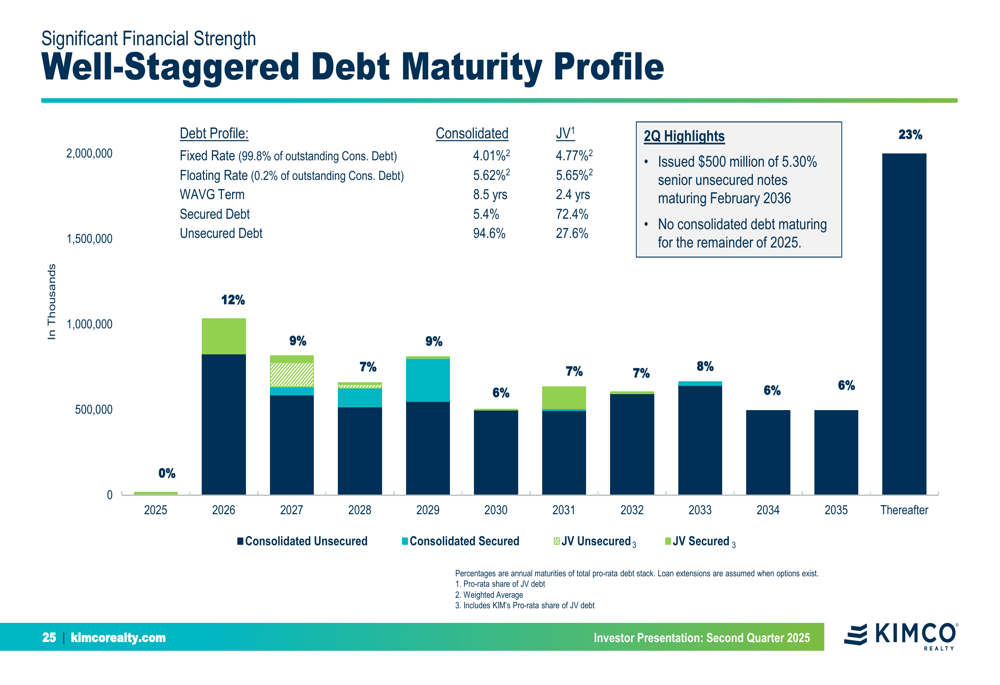

The company’s debt maturity profile is well-staggered, with a weighted average maturity of 8.5 years for consolidated debt. Notably, 99.8% of consolidated debt is fixed rate, providing protection against interest rate fluctuations.

For 2025, Kimco outlined its capital allocation priorities, including $250-300 million for leasing and capex costs, $100-125 million for redevelopment projects, and $100-125 million for net acquisitions including structured investments.

The company highlighted its capital recycling strategy, having completed $132 million in acquisitions at a 7.0% cap rate and $58 million in dispositions at a 5.4% cap rate year-to-date, creating immediate value through the spread.

Forward-Looking Statements

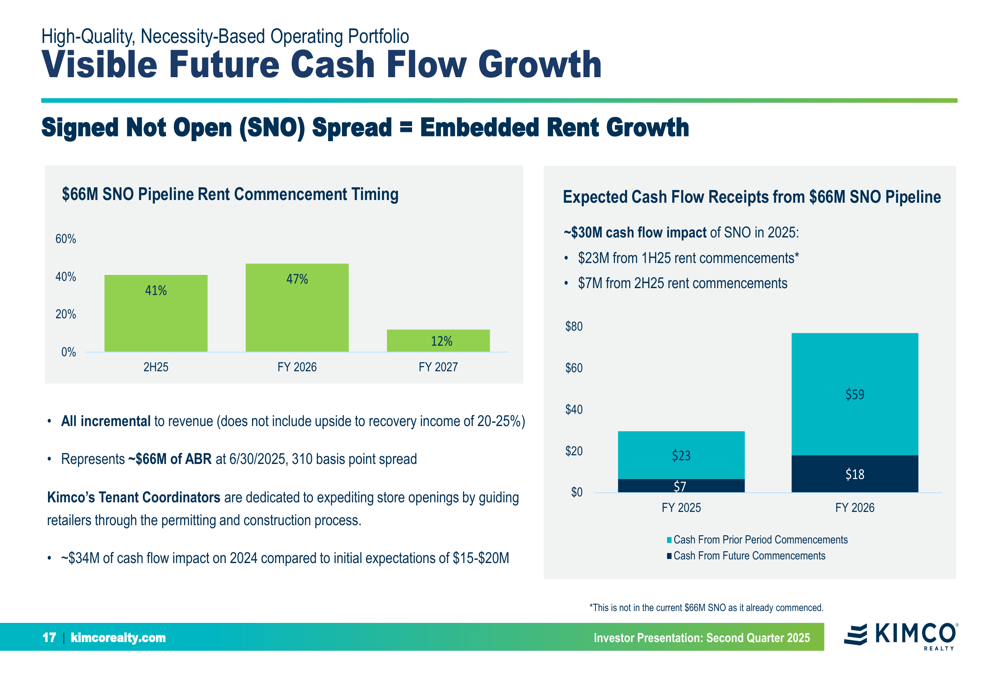

A significant driver of future growth for Kimco is its $66 million Signed Not Opened (SNO) pipeline, which represents leases that have been signed but where tenants have not yet taken occupancy and begun paying rent. The company expects approximately $30 million in cash flow impact from this pipeline in 2025.

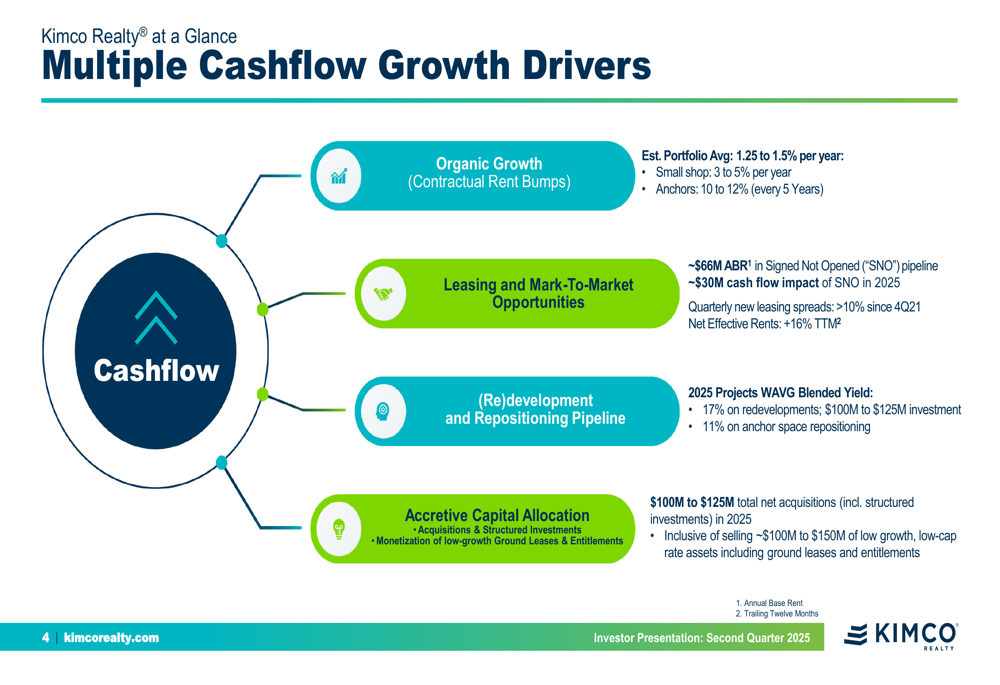

Kimco also outlined multiple cash flow growth drivers, including contractual rent bumps averaging 1.25-1.5% per year across the portfolio, leasing and mark-to-market opportunities, redevelopment and repositioning projects, and accretive capital allocation.

The company’s redevelopment initiatives are expected to generate attractive returns, with anchor repositioning projects targeting an 11% weighted average blended stabilized yield and retail redevelopment projects targeting a 17% yield.

In summary, Kimco Realty’s Q2 2025 presentation portrayed a company with strong operational performance, a clear strategic focus on grocery-anchored centers, and a solid balance sheet to support future growth initiatives. The company appears well-positioned to benefit from favorable supply-demand dynamics in the retail real estate sector and the evolving relationship between e-commerce and physical retail.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.