Gold prices edge higher on raised Fed rate cut hopes

KinderCare Learning Companies Inc. (NASDAQ:KLC) presented its second-quarter fiscal year 2025 earnings results on August 12, 2025, showing modest revenue growth despite ongoing occupancy challenges. The childcare provider’s stock closed at $9.63, down 1.77% for the day, with shares falling an additional 0.21% in after-hours trading.

Quarterly Performance Highlights

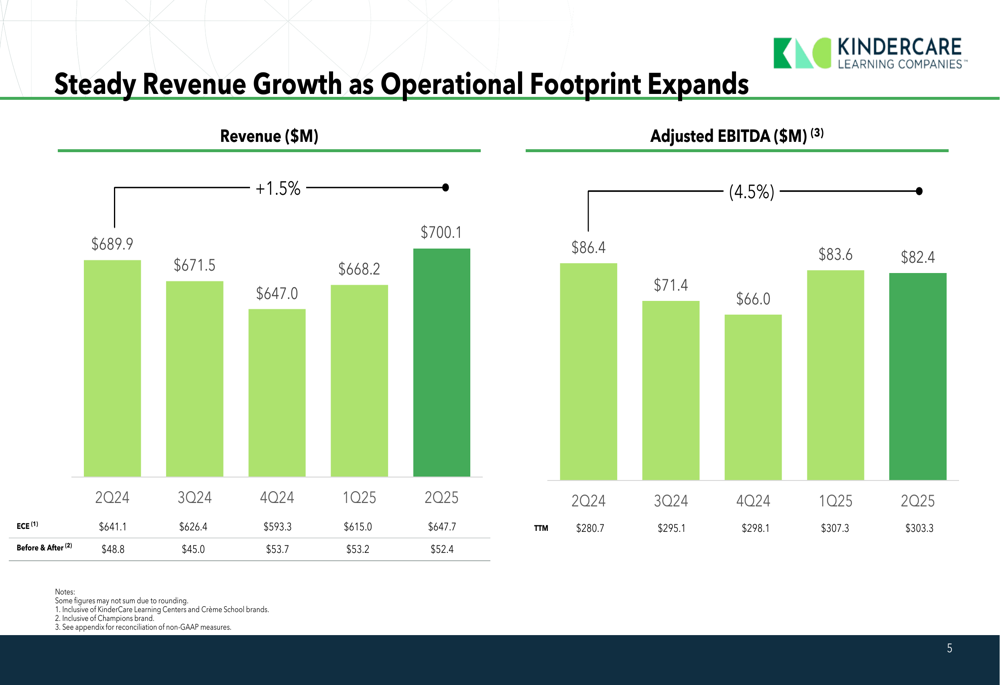

KinderCare reported Q2 revenue of $700.1 million, representing a 1.5% increase from $689.9 million in the same quarter last year. However, Adjusted EBITDA declined 4.5% year-over-year to $82.4 million from $86.4 million in Q2 2024. Net income improved to $38.6 million from $28.5 million in the prior-year period, with diluted earnings per share rising slightly to $0.33 from $0.32.

The company’s same-center occupancy rate fell to 71.0%, down 130 basis points from 72.3% in Q2 2024, though same-center revenue still managed to grow by 1.0% to $637.7 million. This suggests KinderCare’s pricing power and newer center performance are helping offset lower utilization rates.

As shown in the following chart of quarterly revenue and Adjusted EBITDA trends:

"While occupancy declined overall, revenue growth benefited from performance in more recently opened and ramped centers," the company noted in its presentation. This trend highlights KinderCare’s ability to generate revenue growth despite occupancy challenges, likely through a combination of pricing adjustments and operational efficiencies at newer locations.

Expansion Strategy and Growth Model

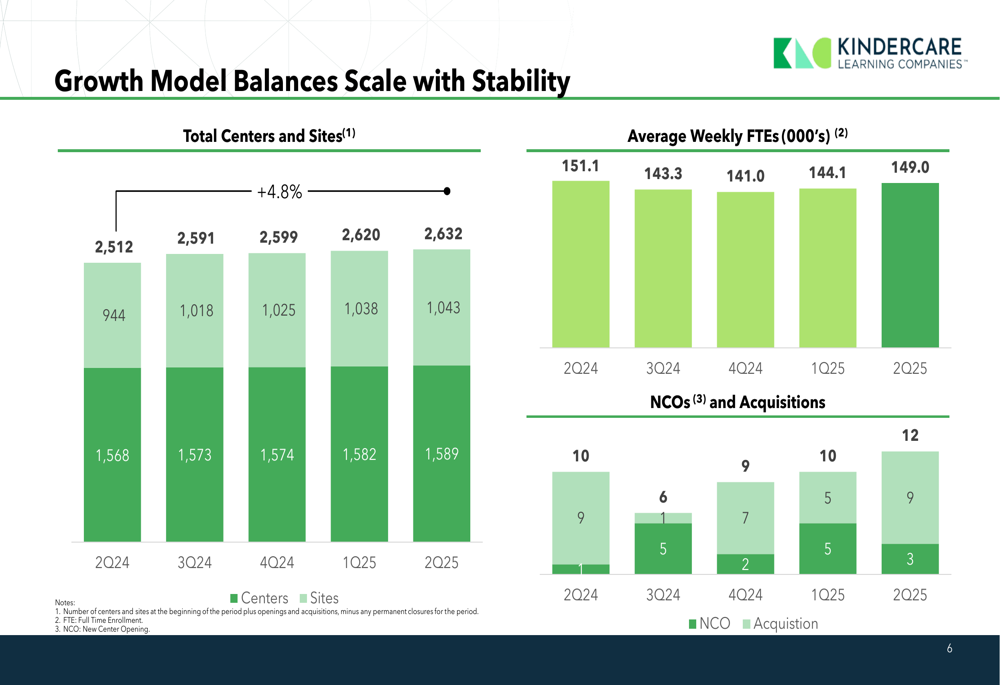

KinderCare continues to expand its operational footprint, with total centers and sites growing 4.8% year-over-year to 2,632, comprising 1,589 early childhood education centers and 1,043 before- and after-school sites. The company added 12 new centers in Q2 2025, including 3 new center openings and 9 acquisitions.

The following chart illustrates KinderCare’s growth model balancing scale with stability:

Notable business achievements in Q2 included a partnership with Maricopa County, Arizona to manage a new on-site facility for county employees, and the expansion of Champions (KinderCare’s before- and after-school program) into five new districts. Additionally, Champ Camp expanded into 13 new districts, with Champions growing by 99 sites over the past 12 months.

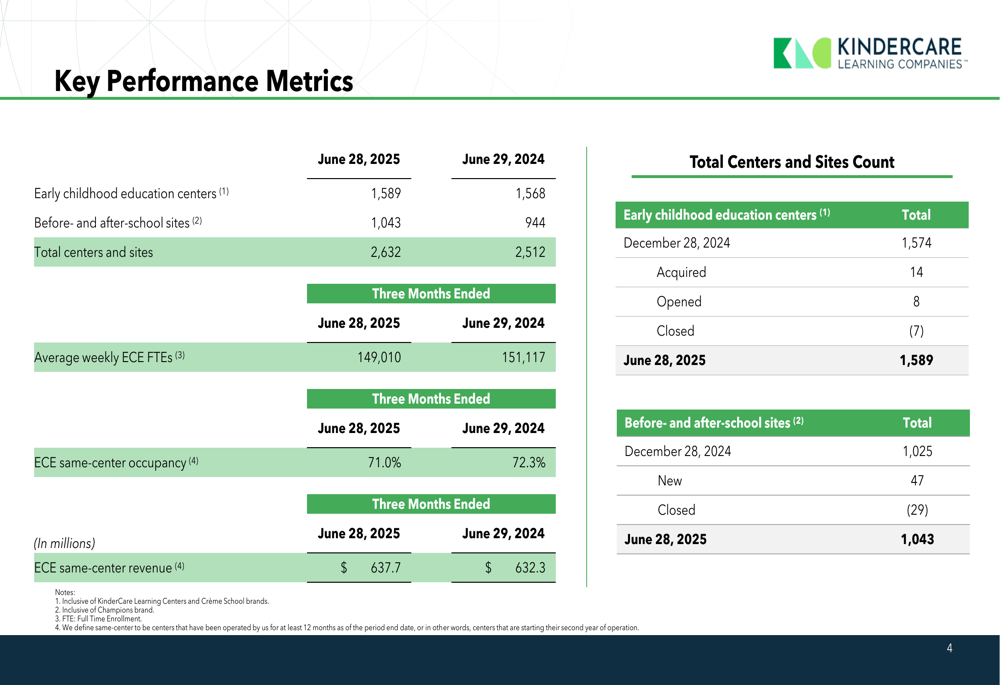

The company’s key performance metrics show the expansion trajectory:

While the total number of centers and sites has increased significantly, average weekly FTEs (full-time equivalents) decreased slightly from 151,117 in Q2 2024 to 149,010 in Q2 2025, potentially reflecting the occupancy challenges the company is facing.

Financial Position and Guidance

KinderCare maintains a solid financial position with $313.4 million in liquidity, including $119.0 million in unrestricted cash and $262.5 million in revolver availability (less $68.1 million in outstanding letters of credit). The company’s net debt stands at $807.4 million, resulting in a leverage ratio of 2.7x based on trailing twelve-month Adjusted EBITDA of $303.3 million.

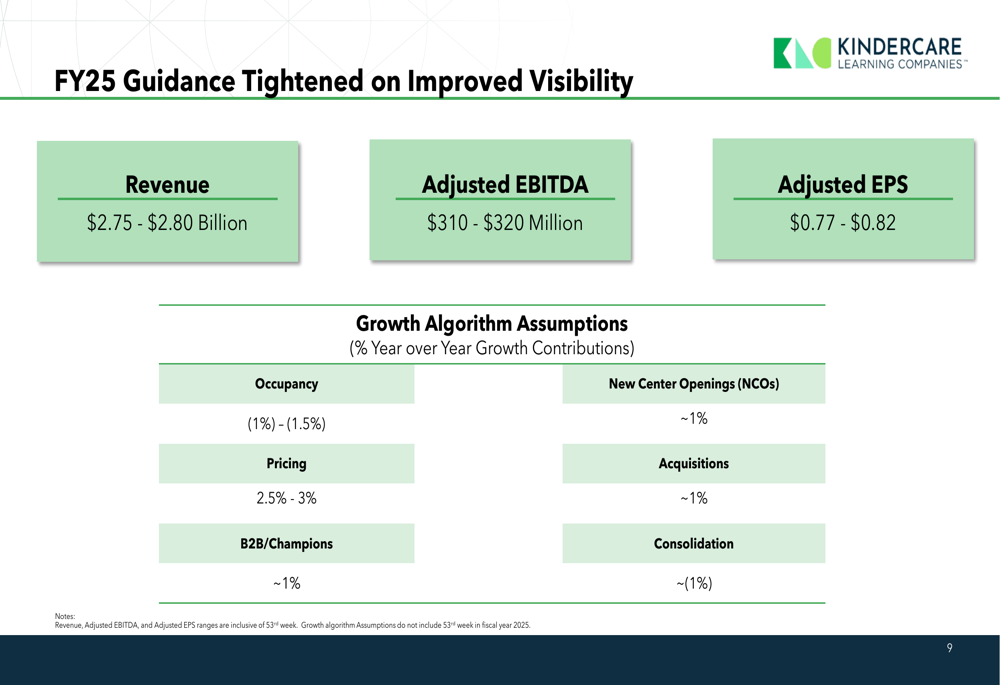

Based on improved visibility for the second half of the year, KinderCare narrowed its FY25 guidance ranges:

The company now expects full-year revenue between $2.75 billion and $2.80 billion, tightening from the previous range of $2.75-$2.85 billion mentioned in its Q1 earnings. Adjusted EBITDA is projected at $310-$320 million, with Adjusted EPS between $0.77 and $0.82.

The guidance assumes occupancy will decline 1-1.5% year-over-year, offset by pricing increases of 2.5-3%, along with contributions from B2B partnerships, Champions expansion, new center openings, and acquisitions.

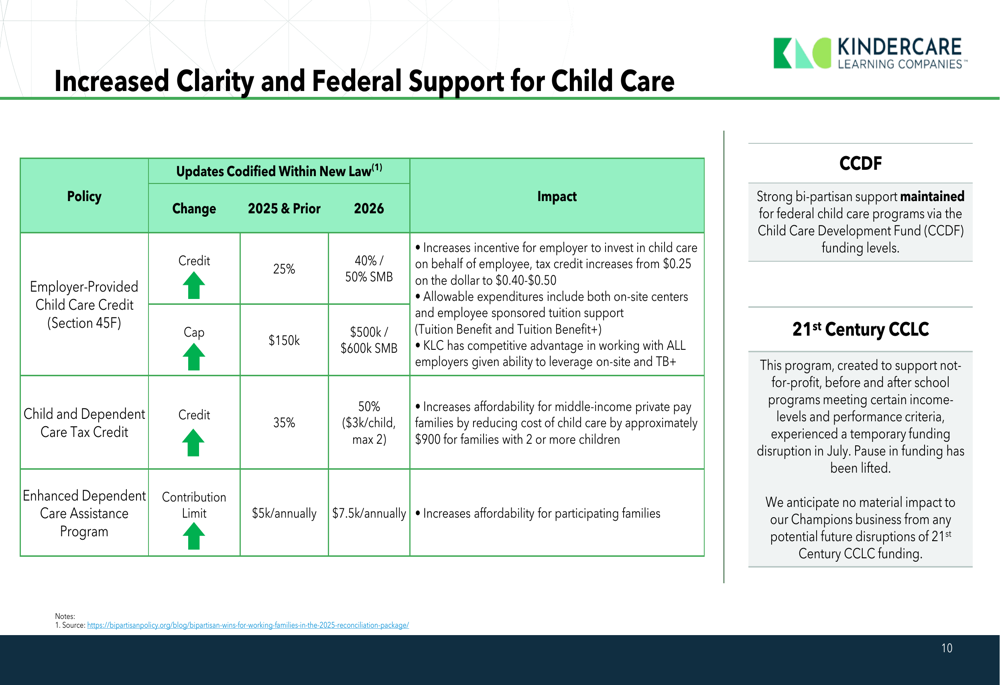

Regulatory Tailwinds and Industry Outlook

KinderCare highlighted recent legislative changes that could provide significant tailwinds for the childcare industry. These include enhancements to the Employer Provided Child Care Credit (Section 45F), with the credit percentage increasing from 25% to 40% (50% for small and medium businesses) and the cap rising from $150,000 to $500,000 ($600,000 for SMBs).

The following slide details the increased clarity and federal support for childcare:

The company sees particular opportunity in the small and medium-sized business market, noting that childcare remains a "must-have" benefit for employees returning to the office. According to KinderCare’s presentation, 64% of parents are willing for employers to offset the cost of childcare, and among Gen Z workers, childcare benefits are the most important factor in job retention.

KinderCare also emphasized the importance of family engagement in driving performance and resilience. The company has seen family engagement rise from 40% in Spring 2014 to 67% in 2024, with fully engaged families generating word-of-mouth referrals, supporting enrollment stability, strengthening teacher retention, and providing constructive feedback.

Despite the challenges in occupancy rates, KinderCare’s strategic expansion, pricing power, and potential regulatory tailwinds position the company to navigate the current environment. However, investors appear cautious, as evidenced by the stock’s continued decline from the $13 level reported after Q1 earnings to the current price of $9.63.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.