Lisa Cook sues Trump over firing attempt, emergency hearing set

Introduction & Market Context

KION Group AG (ETR:KGX) presented its second quarter 2025 results on July 30, highlighting a significant increase in order intake despite revenue declines across both business segments. The company’s stock has shown resilience, trading at €52.65 as of July 29, up 0.87% and well above its 52-week low of €28.00.

The material handling equipment and warehouse automation provider continues to navigate a challenging economic environment characterized by ongoing trade conflicts and geopolitical risks, while maintaining its full-year outlook.

Quarterly Performance Highlights

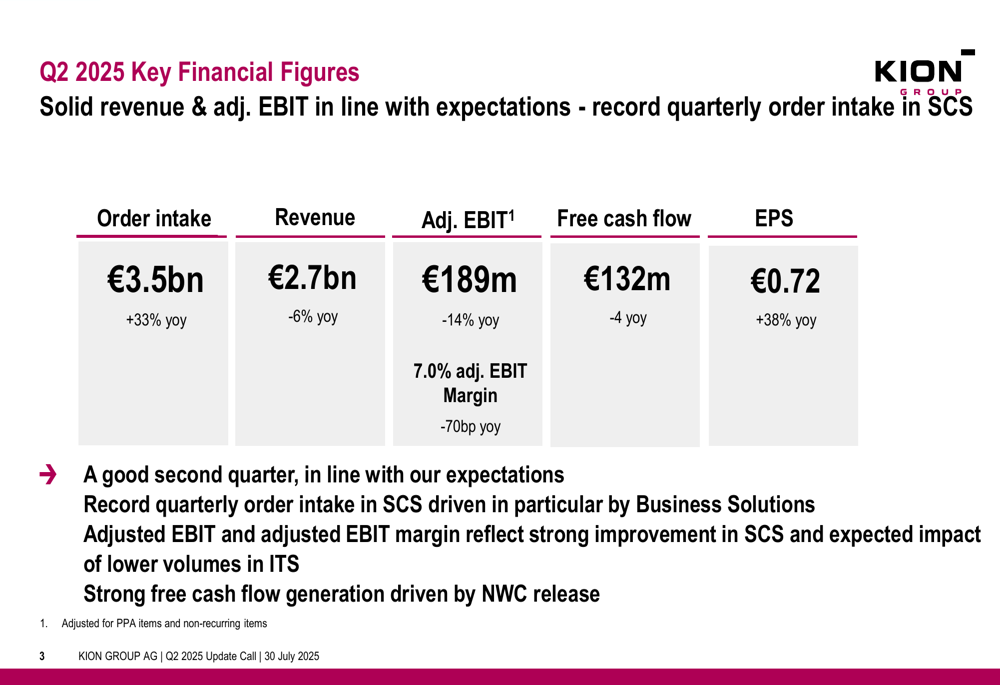

KION reported Q2 2025 order intake of €3.5 billion, a substantial 33% increase year-over-year, driven primarily by exceptional performance in the Supply Chain Solutions (SCS) segment. However, revenue declined 6% to €2.7 billion, while adjusted EBIT fell 14% to €189 million, resulting in a 70 basis point contraction in the adjusted EBIT margin to 7.0%.

As shown in the following chart of key financial figures:

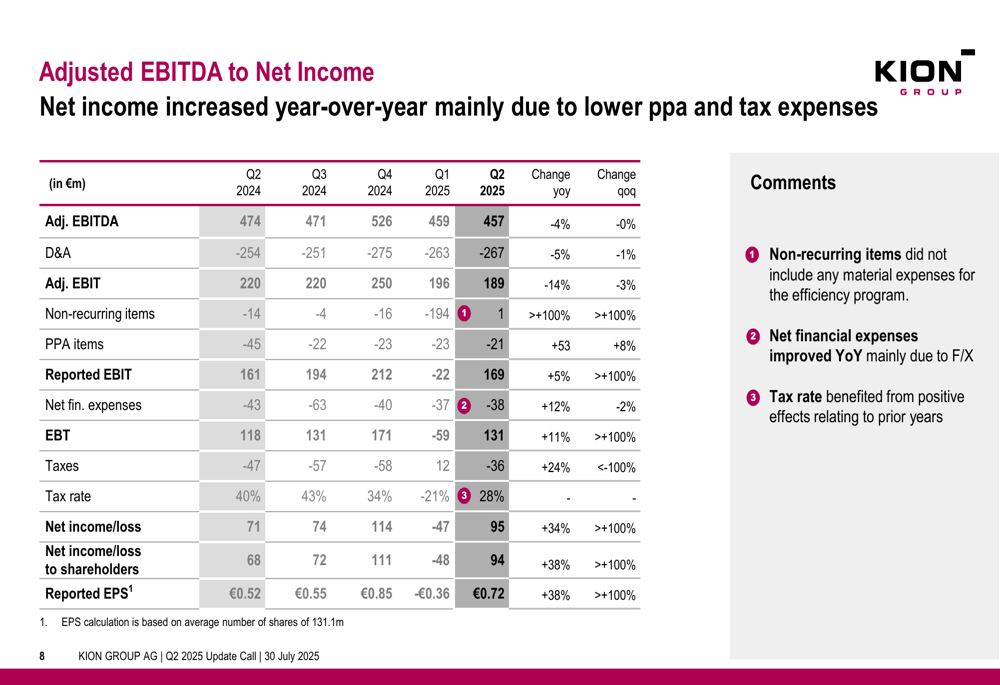

Despite operational challenges, earnings per share improved significantly to €0.72, representing a 38% increase compared to Q2 2024. This improvement was primarily driven by lower PPA (Purchase Price Allocation) items and a more favorable tax rate of 28% versus 40% in the prior-year period.

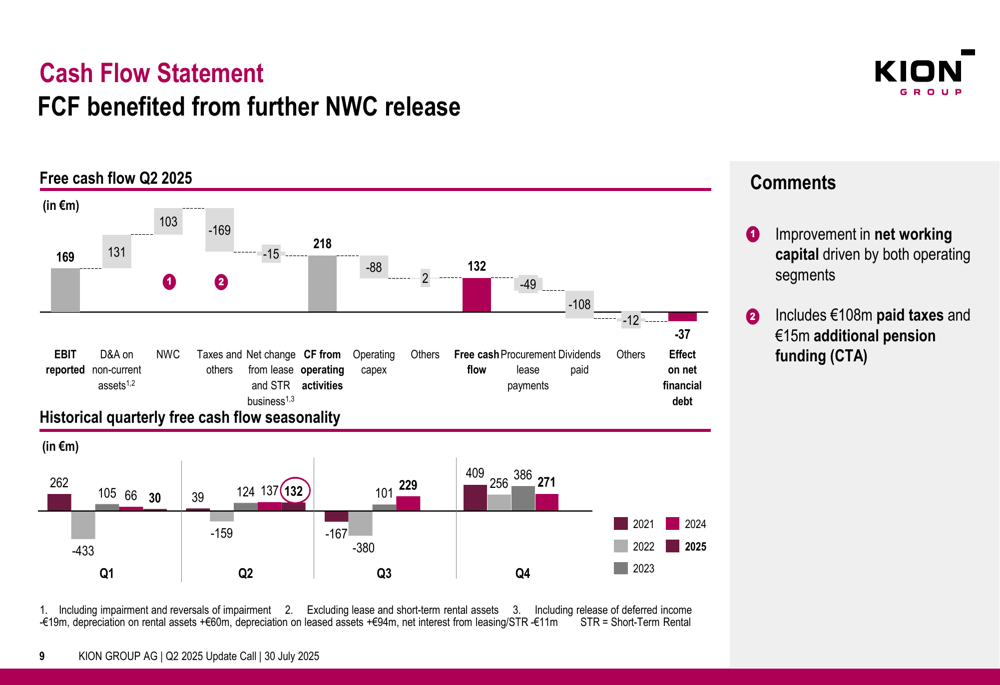

Free cash flow remained strong at €132 million, only 4% below the previous year’s level, benefiting from further net working capital release.

Segment Analysis

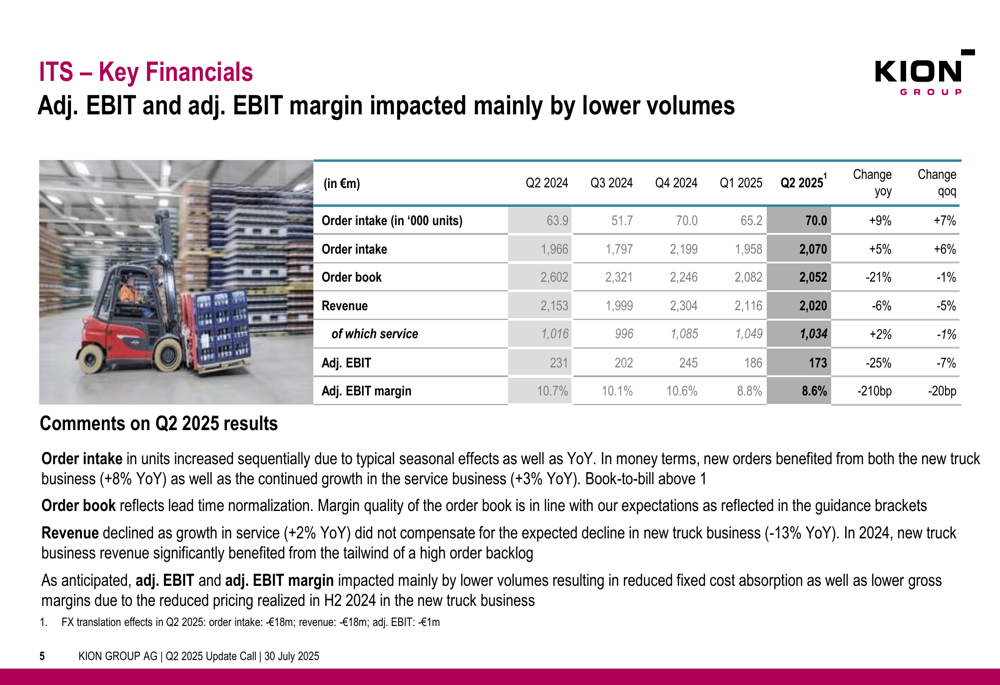

KION’s two operating segments showed markedly different performance trajectories in Q2 2025. The Industrial Trucks & Services (ITS) segment, which manufactures forklifts and other material handling equipment, faced volume and profitability challenges:

The ITS segment saw order intake increase 5% year-over-year to €2.07 billion, with unit orders up 9%. However, revenue declined 6% to €2.02 billion, with service revenue providing some stability by growing 2% to €1.03 billion. Adjusted EBIT fell 25% to €173 million, with the margin contracting 210 basis points to 8.6%, primarily due to lower volumes.

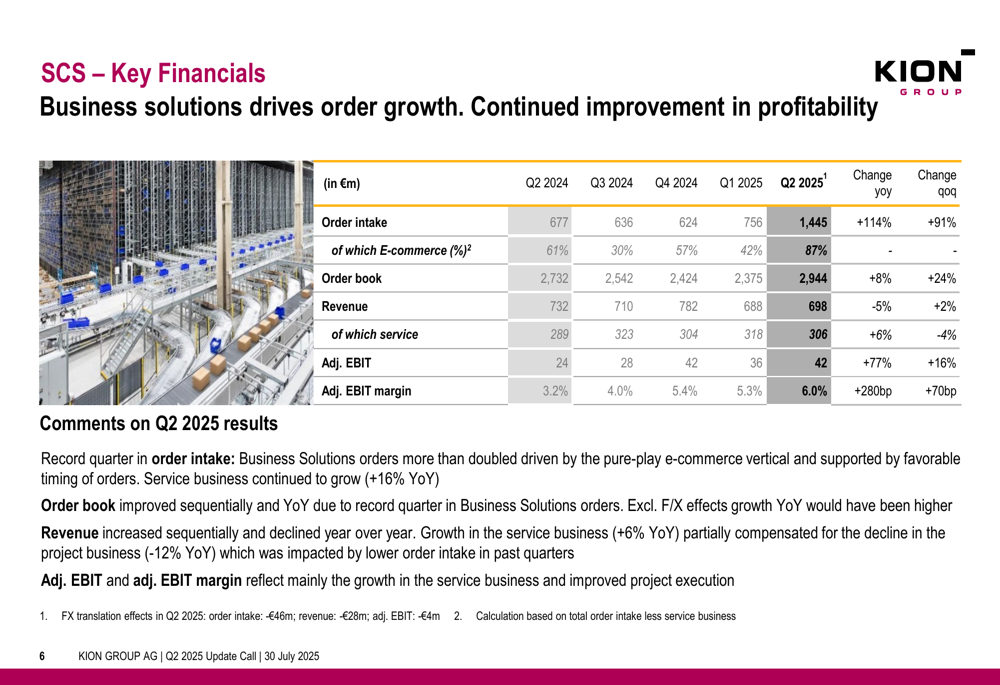

In contrast, the Supply Chain Solutions (SCS) segment, which specializes in warehouse automation and software, delivered exceptional order growth:

SCS order intake more than doubled (+114%) to €1.45 billion, with e-commerce representing 87% of orders compared to 61% in Q2 2024. While revenue declined 5% to €698 million, service revenue grew 6% to €306 million. Adjusted EBIT increased 77% to €42 million, with the margin expanding 280 basis points to 6.0%, demonstrating significant progress toward the company’s target of achieving a 10% margin by 2027.

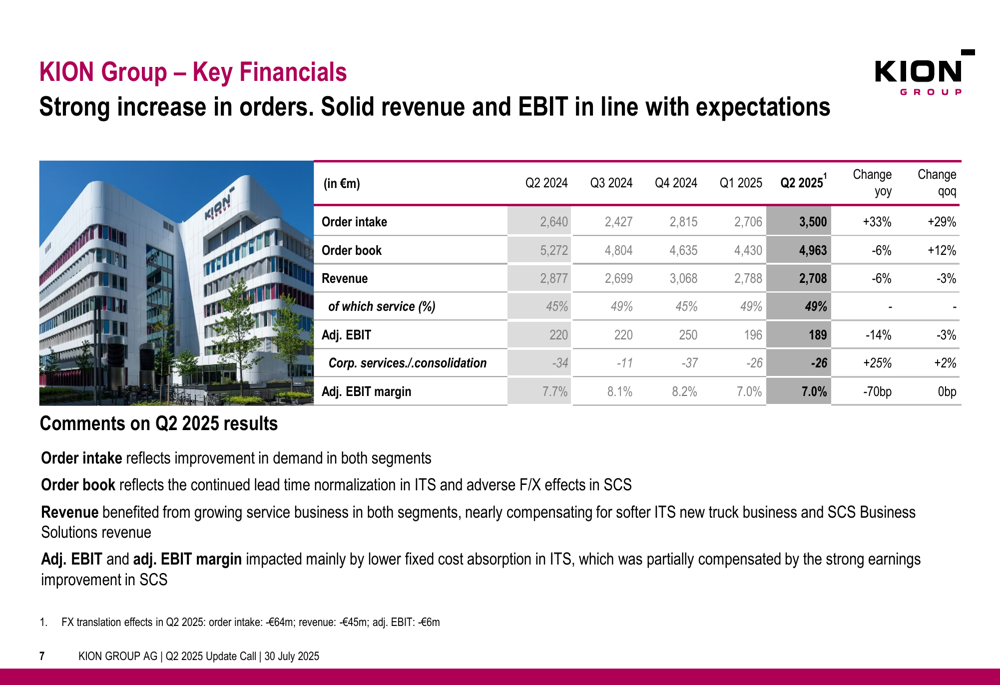

The consolidated financial performance shows the combined impact of both segments:

Financial Position and Cash Flow

KION maintained a solid financial position in Q2 2025, with stable leverage ratios despite a slight increase in net financial debt. The company’s net financial debt stood at €986 million as of June 2025, representing a leverage ratio of 0.5x, unchanged from March 2025.

The free cash flow of €132 million benefited significantly from net working capital improvements, as illustrated in the following cash flow statement:

The reconciliation from adjusted EBITDA to net income shows how lower PPA items and a reduced tax rate contributed to the 38% increase in earnings per share:

Outlook & Strategic Initiatives

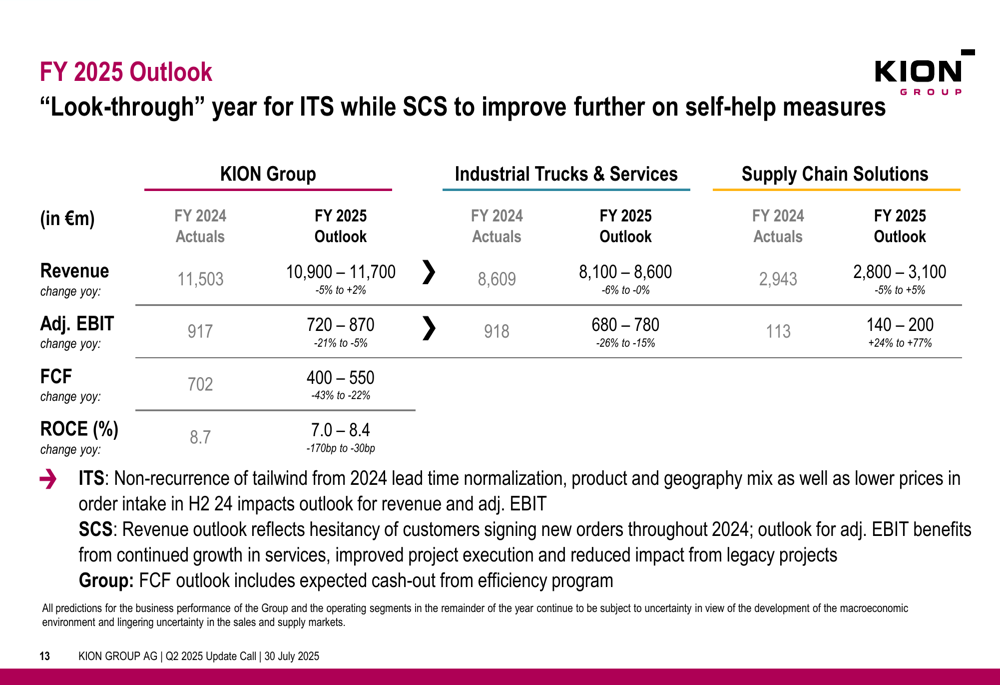

Despite the mixed Q2 results, KION confirmed its full-year 2025 outlook for both segments and the group overall, subject to no significant disruptions to supply chains:

The company expects group revenue between €10.9 billion and €11.7 billion for fiscal year 2025, representing a change of -5% to +2% year-over-year. Adjusted EBIT is projected to be between €720 million and €870 million (-21% to -5% YoY), with free cash flow between €400 million and €550 million.

KION continues to implement its efficiency program, which aims to achieve sustainable annual cost savings of €140-€160 million from 2026 onwards. However, this program will result in non-recurring items of approximately €240-€260 million, mostly in the second half of 2025.

The company’s key strategic focus remains on expanding capacity in production, research and development, and its sales and service networks, particularly in the APAC and Americas regions. Management emphasized three key takeaways from the quarter:

KION’s performance in the first half of 2025 aligns with the mixed results reported in Q1, where the company missed EPS expectations but maintained stable stock performance. The acceleration in order intake from 11% growth in Q1 to 33% in Q2 suggests improving momentum, particularly in the SCS segment, which could translate to revenue growth in future quarters as these orders are fulfilled.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.