Street Calls of the Week

Kirby Corporation (NYSE:KEX) reported strong second quarter 2025 results on July 31, with earnings per share climbing 17% year-over-year despite facing navigational challenges in its marine transportation segment. However, the stock dropped 5.9% in premarket trading to $112.92, suggesting investors may have expected even stronger performance or were concerned about elements of the company’s outlook.

Quarterly Performance Highlights

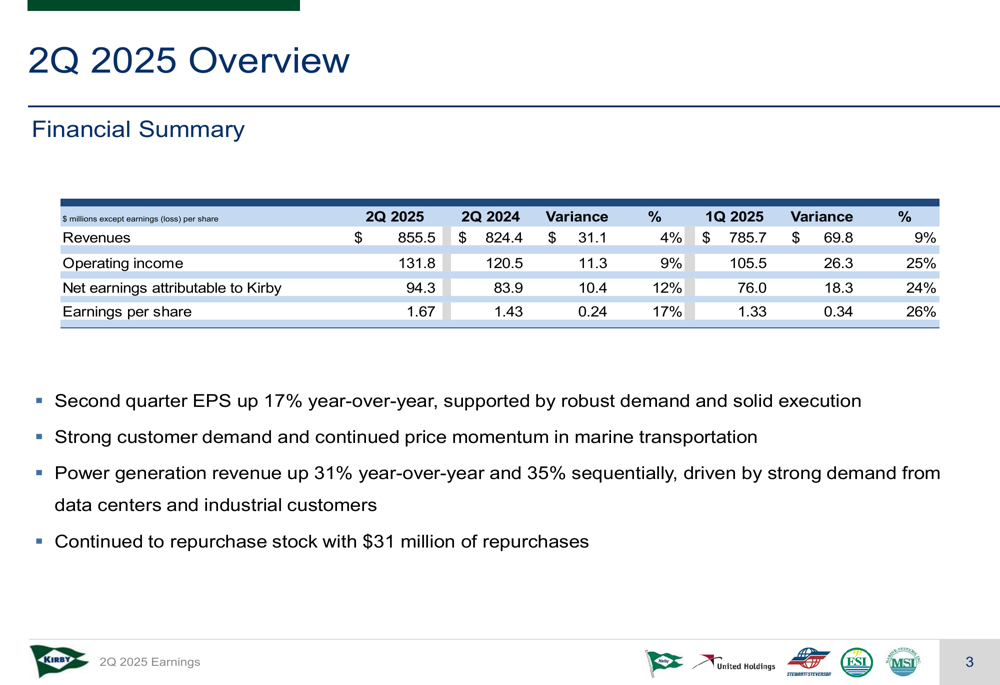

Kirby delivered solid financial results across most metrics in the second quarter. Earnings per share reached $1.67, up 17% from $1.43 in Q2 2024 and 26% higher than the $1.33 reported in Q1 2025. Total (EPA:TTEF) revenue increased to $855.5 million, representing 4% year-over-year and 9% sequential growth.

Operating income rose to $131.8 million, a 9% improvement from the same period last year and 25% higher than the previous quarter. Net earnings attributable to Kirby reached $94.3 million, up 12% year-over-year and 24% sequentially.

The company continued its share repurchase program, buying back 331,900 shares at an average price of $94.01 for a total of $31.2 million during the quarter.

Marine Transportation Analysis

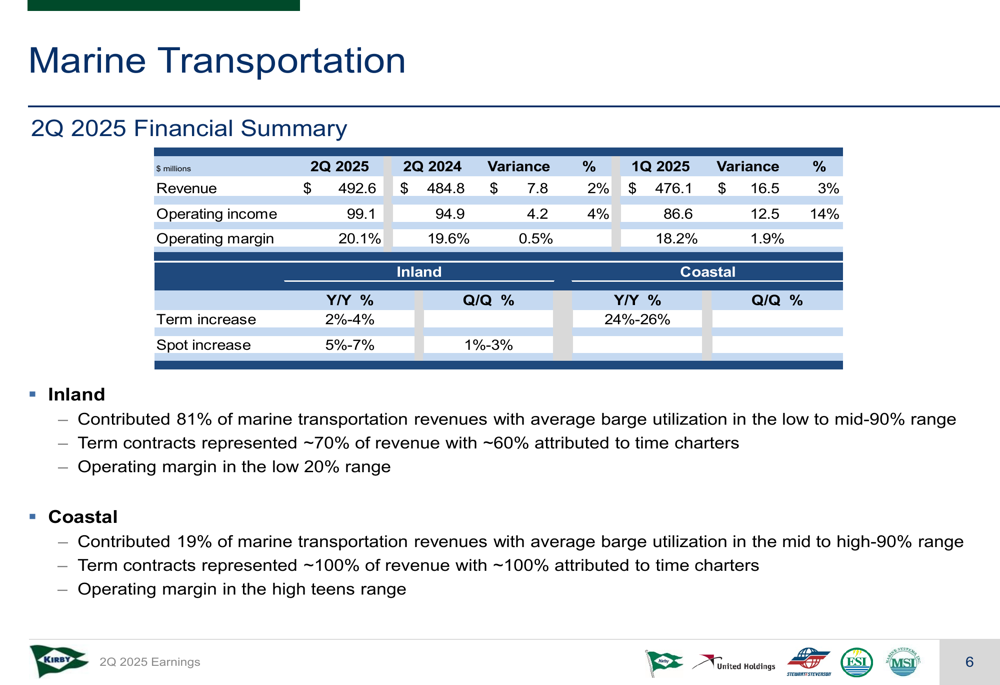

Kirby’s Marine Transportation segment, which contributed approximately 58% of total revenue, showed steady improvement despite moderate impacts from navigational and lock delays. The segment generated $492.6 million in revenue, up 2% year-over-year and 3% sequentially, while operating income increased to $99.1 million, representing 4% year-over-year and 14% sequential growth.

Operating margins in the Marine Transportation segment expanded to 20.1%, compared to 19.6% in Q2 2024 and 18.2% in Q1 2025. This improvement was driven by disciplined execution and sustained pricing growth.

In the inland market, which represented 81% of marine transportation revenues, spot prices increased in the mid-single digits year-over-year, while term contracts were renewed higher in the low to mid-single digit range. Barge utilization remained strong in the low to mid-90% range.

The coastal market showed even stronger performance with term contracts renewed higher in the mid-20% range year-over-year. Barge utilization in this segment reached the mid to high-90% range, reflecting strong customer demand combined with limited availability of large capacity vessels.

Distribution & Services Analysis

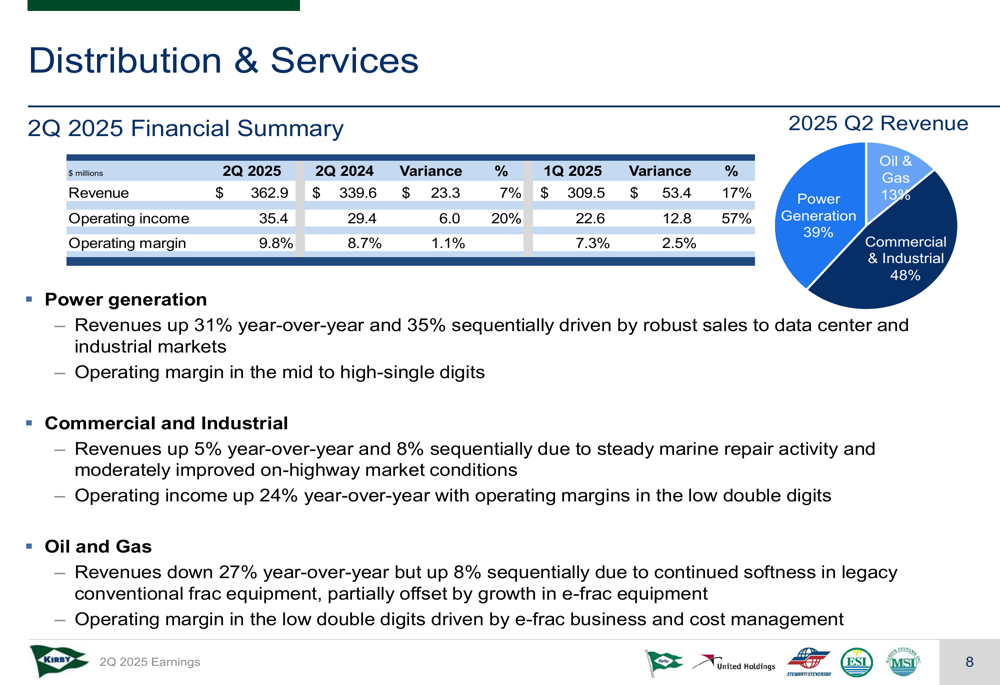

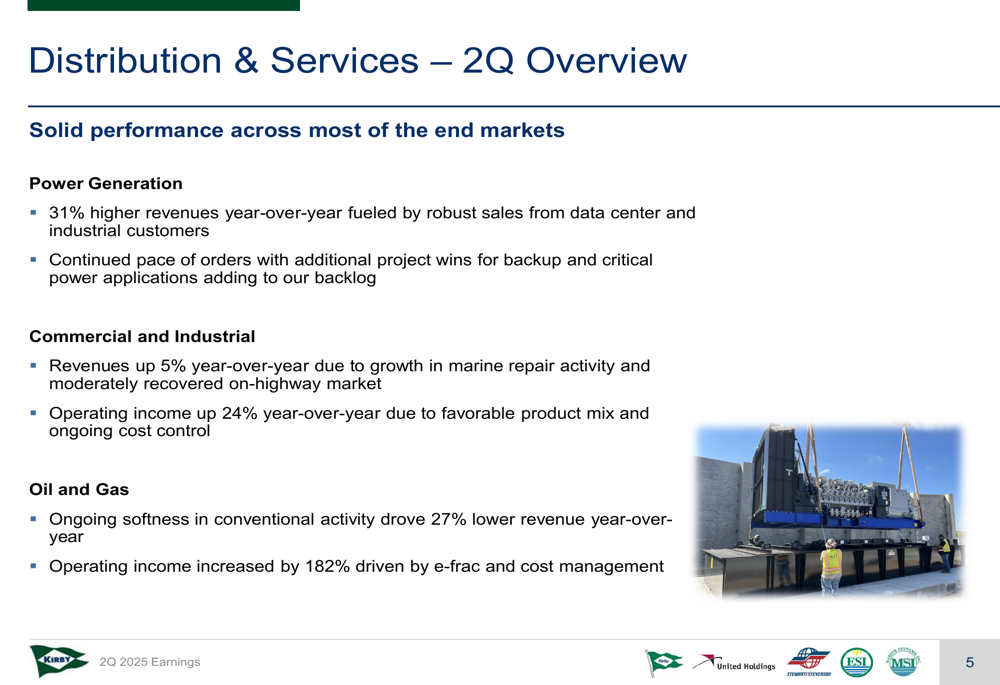

The Distribution & Services segment delivered impressive results, with revenue increasing to $362.9 million, up 7% year-over-year and 17% sequentially. Operating income surged to $35.4 million, representing a 20% year-over-year and 57% sequential increase. Operating margins expanded to 9.8%, compared to 8.7% in Q2 2024 and 7.3% in Q1 2025.

The standout performer within this segment was Power Generation (HM:PGV), which saw revenues jump 31% year-over-year and 35% sequentially, driven by robust sales from data center and industrial customers. This subsegment now represents 39% of Distribution & Services revenue and is expected to grow to approximately 40% for the full year.

The Commercial and Industrial subsegment, which contributes 48% of segment revenue, reported a 5% year-over-year increase due to growth in marine repair activity and a moderately recovered on-highway market. Operating income in this area improved by 24% year-over-year.

In contrast, the Oil and Gas subsegment continued to face challenges, with revenues declining 27% year-over-year due to ongoing softness in conventional activity. However, operating income increased by 182% driven by the e-frac business and effective cost management. This subsegment now represents only 13% of Distribution & Services revenue.

Balance Sheet and Capital Allocation

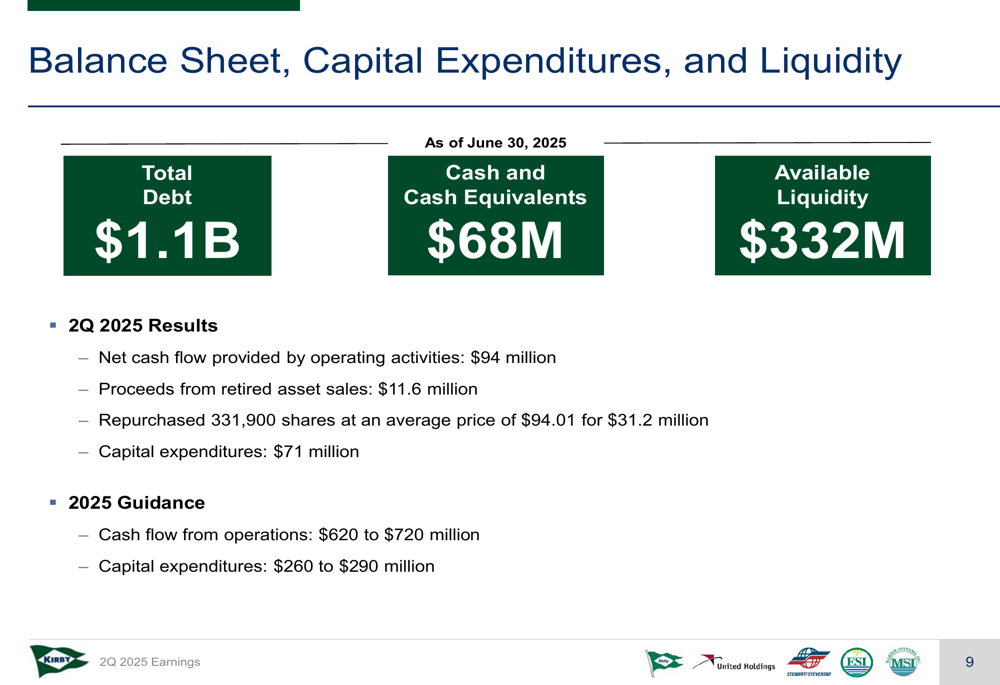

As of June 30, 2025, Kirby maintained a solid financial position with total debt of $1.1 billion and cash and cash equivalents of $68 million. Available liquidity stood at $332 million. Net cash flow provided by operating activities was $94 million for the quarter, while capital expenditures totaled $71 million.

For the full year 2025, Kirby expects cash flow from operations to range between $620 million and $720 million, with capital expenditures projected between $260 million and $290 million.

2025 Outlook

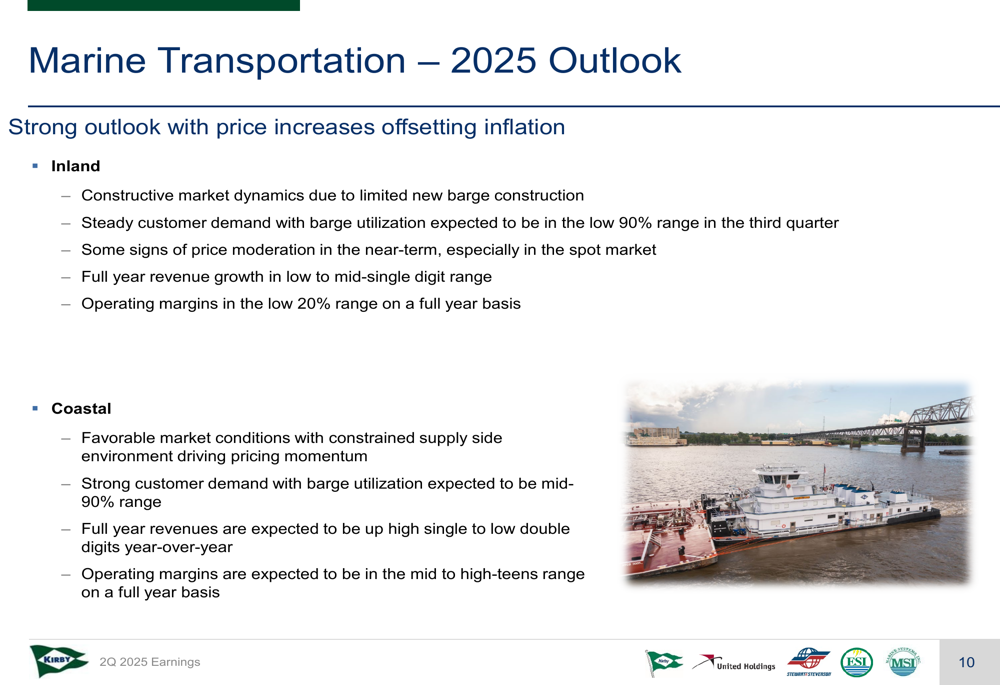

For the Marine Transportation segment, Kirby anticipates a strong outlook with price increases offsetting inflation. In the inland market, the company expects steady customer demand with barge utilization in the low 90% range for the third quarter, though it noted some signs of price moderation in the spot market. Full-year revenue growth is projected in the low to mid-single digit range with operating margins in the low 20% range.

The coastal market outlook remains favorable with strong customer demand and barge utilization expected in the mid-90% range. Full-year coastal revenues are projected to increase in the high single to low double digits year-over-year, with operating margins in the mid to high-teens range.

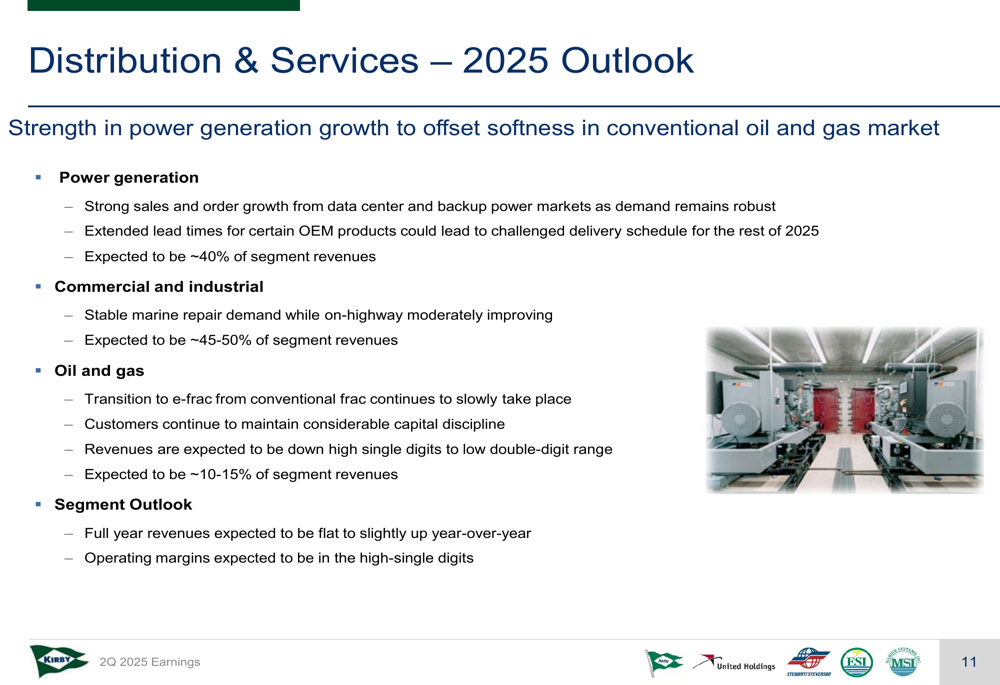

For the Distribution & Services segment, Kirby expects strength in power generation to offset softness in the conventional oil and gas market. Power generation should continue to benefit from strong sales and order growth from data center and backup power markets, though extended lead times for certain OEM products could challenge delivery schedules for the rest of 2025.

Overall, Kirby projects full-year Distribution & Services revenues to be flat to slightly up year-over-year, with operating margins in the high-single digits. The company’s focus on data center power generation and strategic cost management appears positioned to help offset challenges in conventional oil and gas markets as the industry slowly transitions to e-frac technology.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.