PepsiCo shares jump as Elliott reveals $4 billion stake and turnaround plan

Introduction & Market Context

Kiwetinohk Energy Corp (TSX:KEC) released its Q1 2025 corporate presentation on May 8, 2025, highlighting the company’s operational achievements and growth strategy against a backdrop of recent financial underperformance. The Canadian energy producer, which focuses on upstream oil and gas production in Alberta’s Duvernay and Montney formations, has seen its stock trade at $14.83 as of May 7, 2025, down 0.87% on the day and well below its 52-week high of $17.48.

The presentation comes after disappointing Q4 2024 financial results, where Kiwetinohk reported earnings per share of -$0.37, significantly below the forecasted $0.60, and revenue of $97.4 million against an anticipated $128.4 million. Despite these financial challenges, the company continues to emphasize its operational strengths and long-term growth potential.

Executive Summary

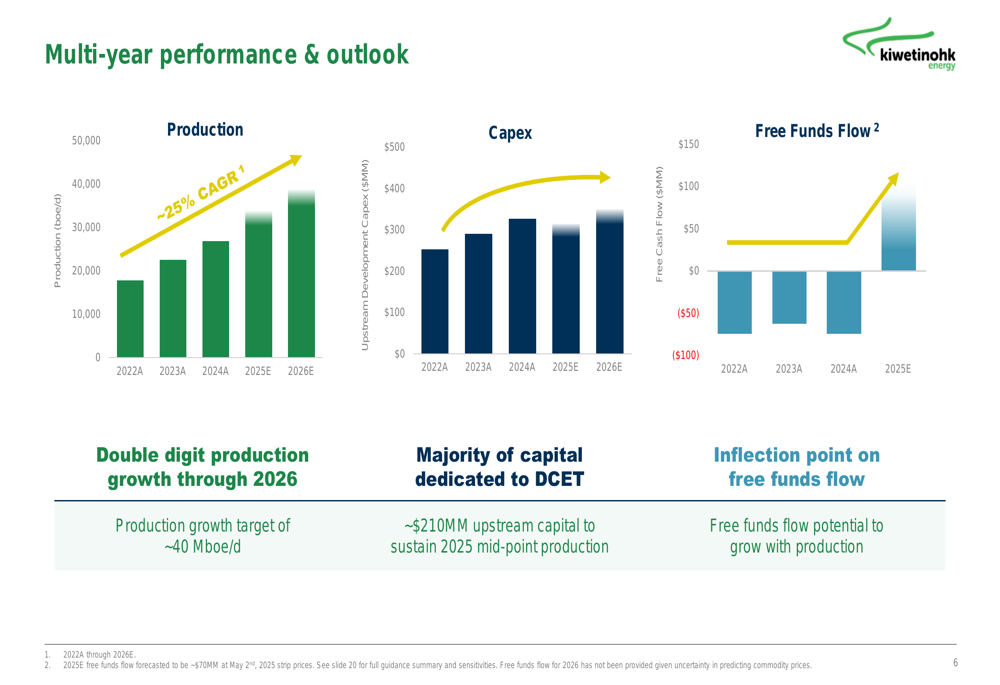

Kiwetinohk’s presentation outlines an ambitious growth strategy centered on its Duvernay and Montney assets, projecting approximately 25% compound annual growth rate (CAGR) in production from 2022 to 2026. The company highlights its infrastructure advantages, particularly its Alliance Pipeline capacity providing access to premium U.S. gas markets, which has enabled it to realize prices approximately 175% above AECO benchmark in Q1 2025.

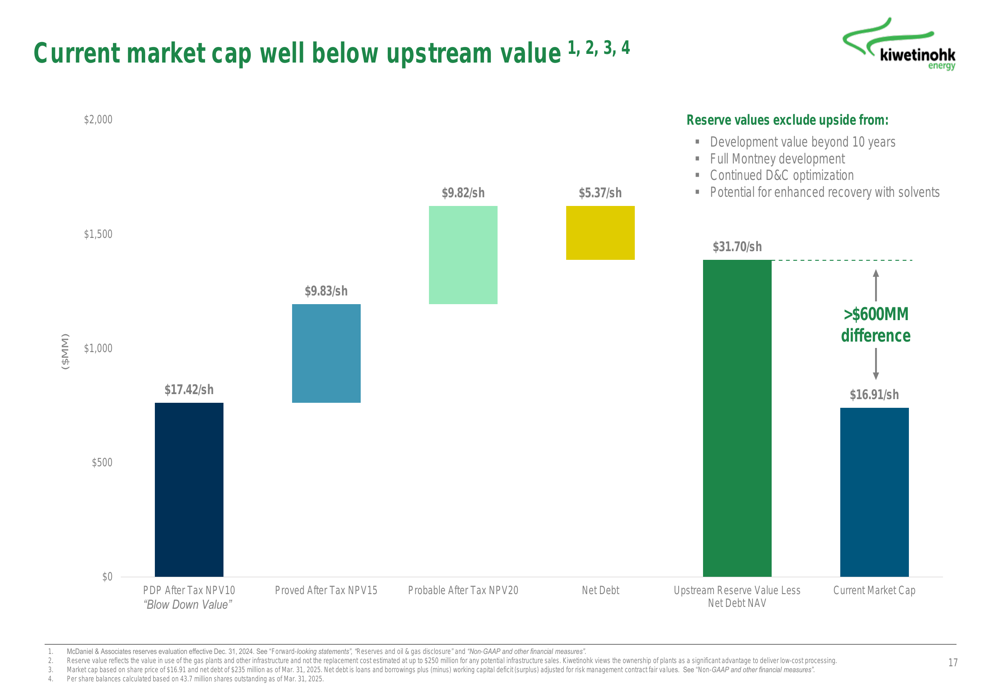

Management projects free funds flow of approximately $70 million for 2025 based on May 2nd strip prices, representing an inflection point as the company balances growth with cash generation. Notably, Kiwetinohk claims its current market capitalization of $740 million sits below the value of its upstream assets alone, suggesting potential undervaluation.

Quarterly Performance & Growth Strategy

Kiwetinohk reports production of approximately 32.5 Mboe/d expected in 2025, with a target of tripling production and capacity to reach 40 Mboe/d. The company’s growth strategy is supported by an extensive inventory of 429 drilling locations across the Duvernay (182) and Montney (247) formations, providing approximately 24 years of drilling programs.

As shown in the following multi-year performance outlook, Kiwetinohk projects continued production growth through 2026, with increasing free funds flow as operations scale:

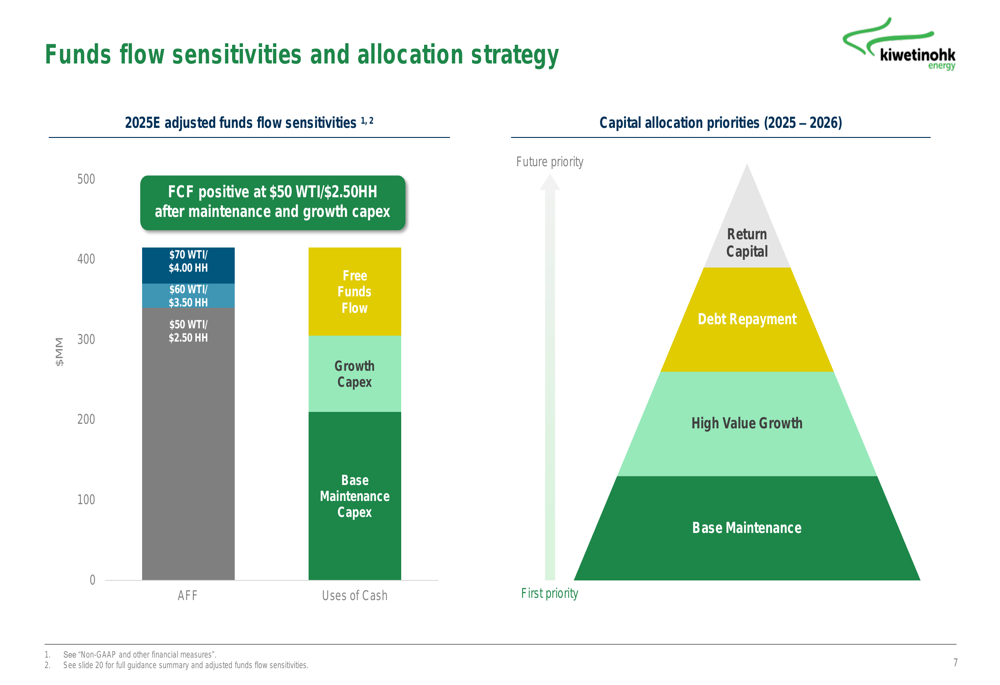

The company’s capital allocation strategy prioritizes base maintenance first, followed by high-value growth opportunities, debt repayment, and eventually returning capital to shareholders. Management indicates that Kiwetinohk remains free cash flow positive even at $50 WTI and $2.50 Henry Hub prices after accounting for maintenance and growth capital expenditures.

For 2025, Kiwetinohk has provided guidance of 31.0-34.0 Mboe/d in average sales volumes, with oil and liquids comprising 45-49% of production. The company expects operating expenses of $6.75-7.25 per boe and transportation expenses of $5.75-6.00 per boe, with upstream capital expenditures projected at $290-315 million.

Infrastructure & Competitive Advantages

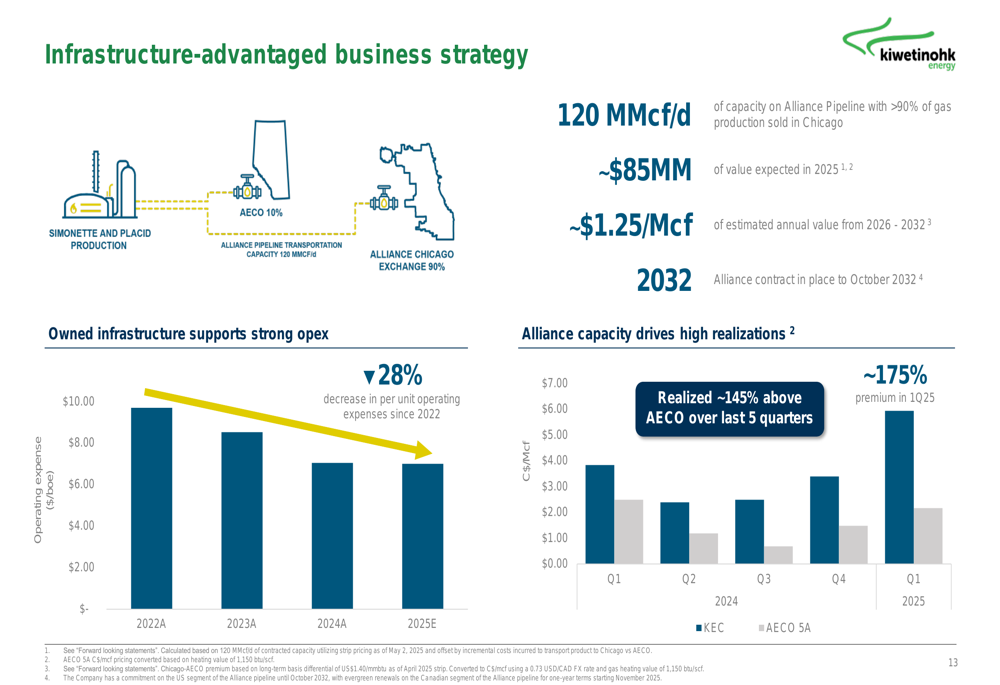

A cornerstone of Kiwetinohk’s strategy is its infrastructure advantage, particularly its 120 MMcf/d of capacity on the Alliance Pipeline, which allows the company to sell over 90% of its gas production in the premium Chicago market. This infrastructure advantage is expected to generate approximately $85 million of value in 2025 and approximately $1.25/Mcf of estimated annual value from 2026-2032.

The company’s infrastructure advantages are illustrated in the following slide:

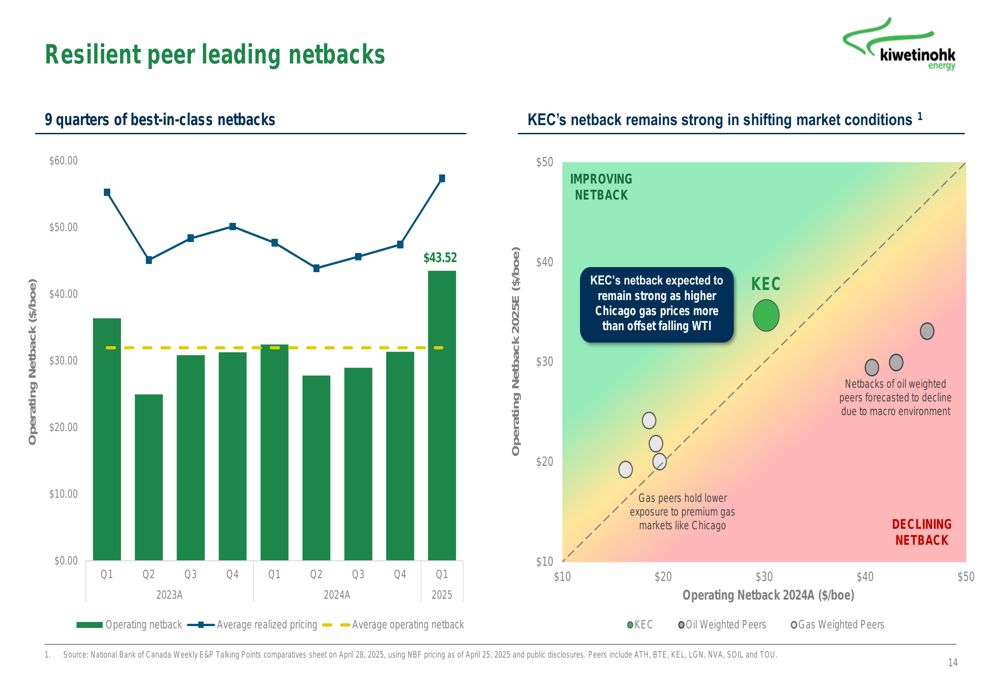

This infrastructure positioning has enabled Kiwetinohk to achieve what it describes as "nine quarters of best-in-class netbacks," with realized prices significantly above AECO benchmark. The company expects its netback to remain strong as higher Chicago gas prices more than offset falling WTI oil prices.

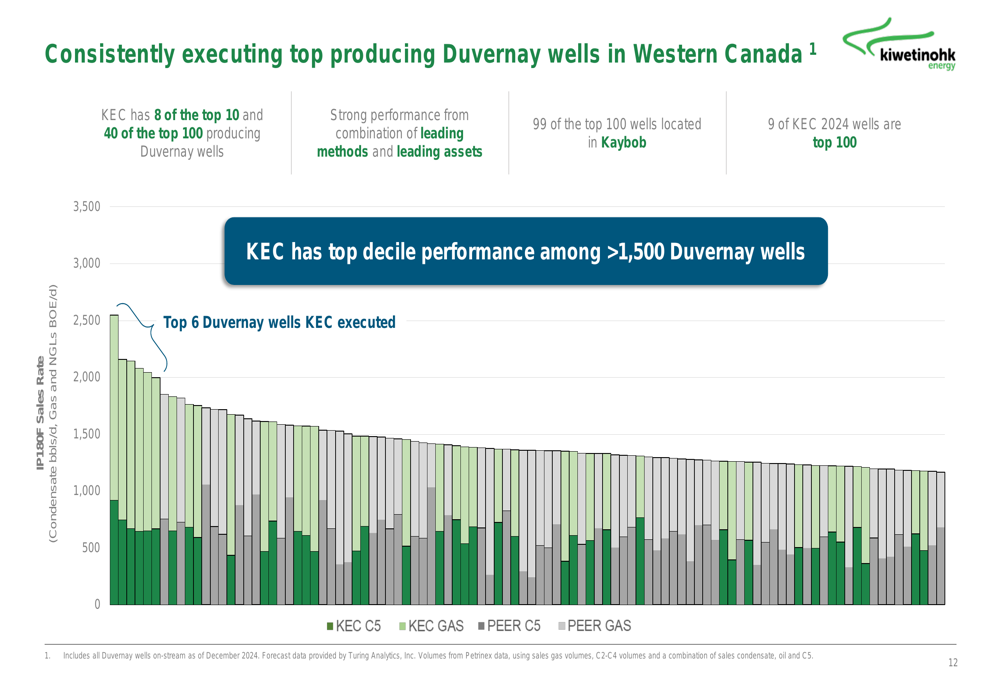

Another key competitive advantage highlighted is Kiwetinohk’s well performance in the Duvernay formation. The company claims to have 8 of the top 10 and 40 of the top 100 producing Duvernay wells, demonstrating top decile performance among over 1,500 Duvernay wells.

Valuation Analysis

Kiwetinohk’s presentation makes a case for the company being undervalued, noting that its current market capitalization of $740 million is below the value of its upstream assets alone. This valuation gap is illustrated in the following slide:

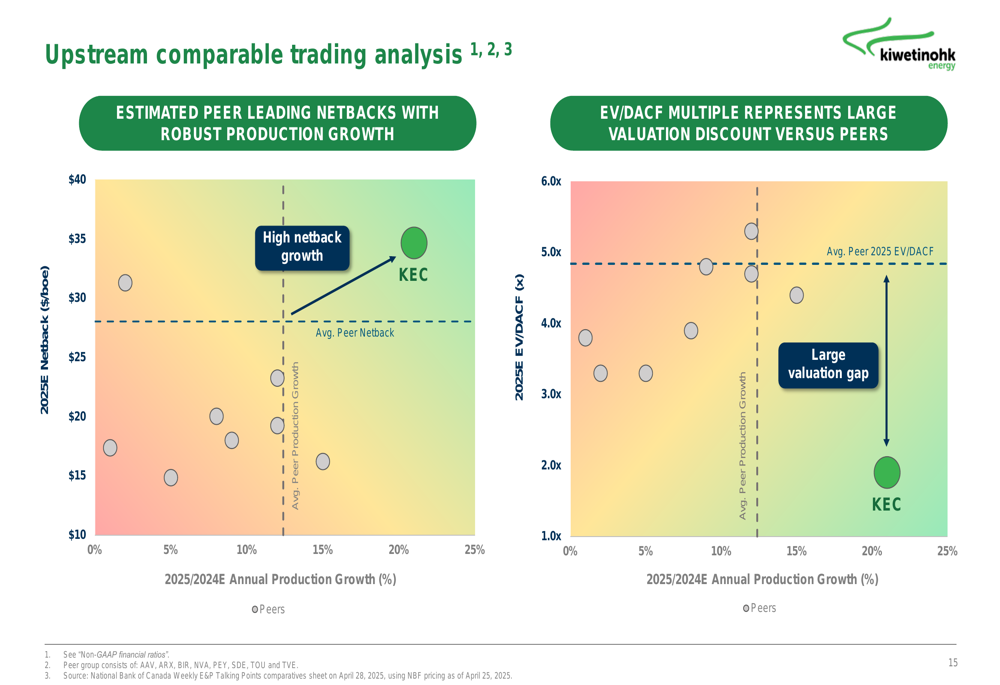

The company also highlights its valuation discount compared to peers on an EV/DACF (Enterprise Value to Debt-Adjusted Cash Flow) multiple basis, despite what it describes as "estimated peer leading netbacks with robust production growth."

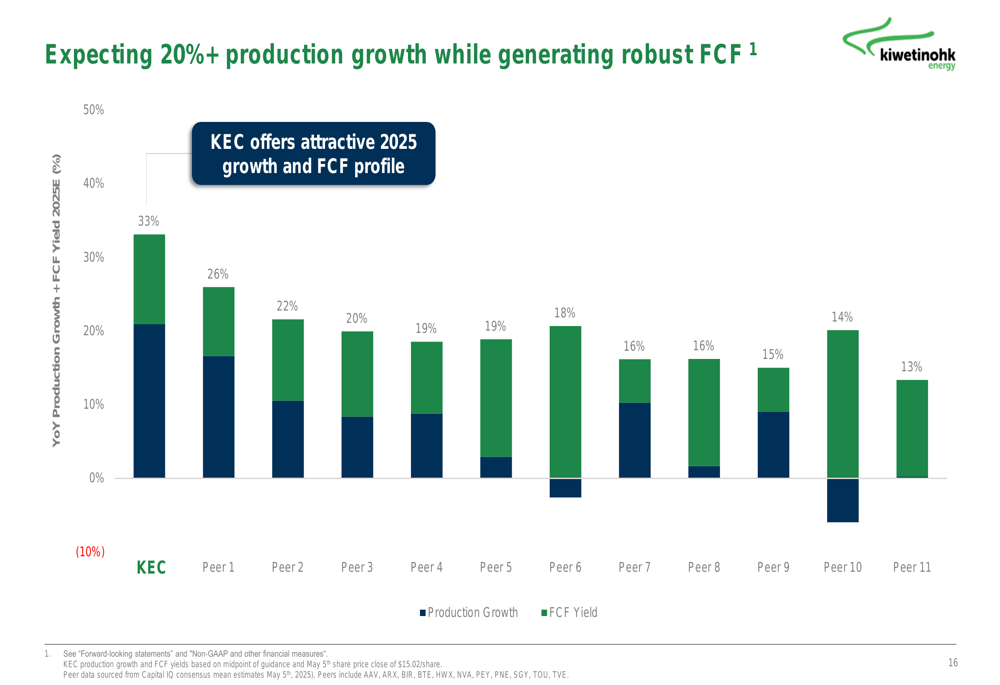

Kiwetinohk further emphasizes its attractive growth and free cash flow profile for 2025 compared to peers, projecting over 20% year-over-year production growth while generating robust free cash flow:

Forward Outlook & Challenges

Looking ahead, Kiwetinohk’s 2025 budget focuses on high-value growth across its Tony Creek (Duvernay), South Simonette (Duvernay), and Placid (Montney) assets. The company plans to drill approximately 18 new wells in 2025, including 13 Duvernay and 5 Montney wells.

Despite the optimistic outlook presented, investors should consider several challenges. The recent earnings miss in Q4 2024 raises questions about the company’s ability to meet financial projections. Additionally, potential U.S. import tariffs on Canadian oil and gas could impact profitability, and fluctuations in natural gas prices may affect revenue streams.

The company’s net debt position of $235 million as of Q1 2025 also warrants monitoring, though management indicates debt repayment is a priority in its capital allocation strategy once base maintenance and high-value growth opportunities are funded.

Conclusion

Kiwetinohk Energy’s Q1 2025 presentation paints a picture of a company with strong operational performance and growth potential, particularly through its infrastructure advantages and high-quality Duvernay and Montney assets. However, the recent financial underperformance in Q4 2024 suggests investors should approach the company’s projections with appropriate caution.

The apparent valuation gap between Kiwetinohk’s market capitalization and the value of its upstream assets may represent an opportunity for investors willing to bet on the company’s ability to translate its operational strengths into improved financial performance. As the company reaches what it describes as an "inflection point" in free funds flow, the coming quarters will be crucial in determining whether Kiwetinohk can deliver on its ambitious growth strategy while generating the cash flow needed to reduce debt and eventually return capital to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.