U.S. stocks edge higher; solid earnings season continues

Introduction & Market Context

Klaviyo Inc (NYSE:KVYO) released its Q2 2025 investor presentation on August 5, 2025, showcasing strong financial performance with 32% year-over-year revenue growth. The company, which positions itself as "the only CRM built for B2C," continues to expand its customer base, product offerings, and international presence while maintaining healthy profitability metrics.

Following the earnings release, Klaviyo’s stock rose 3.01% in aftermarket trading to $31.49, building on a 0.43% gain during regular trading hours. The company’s shares have traded between $22.16 and $49.55 over the past 52 weeks.

Quarterly Performance Highlights

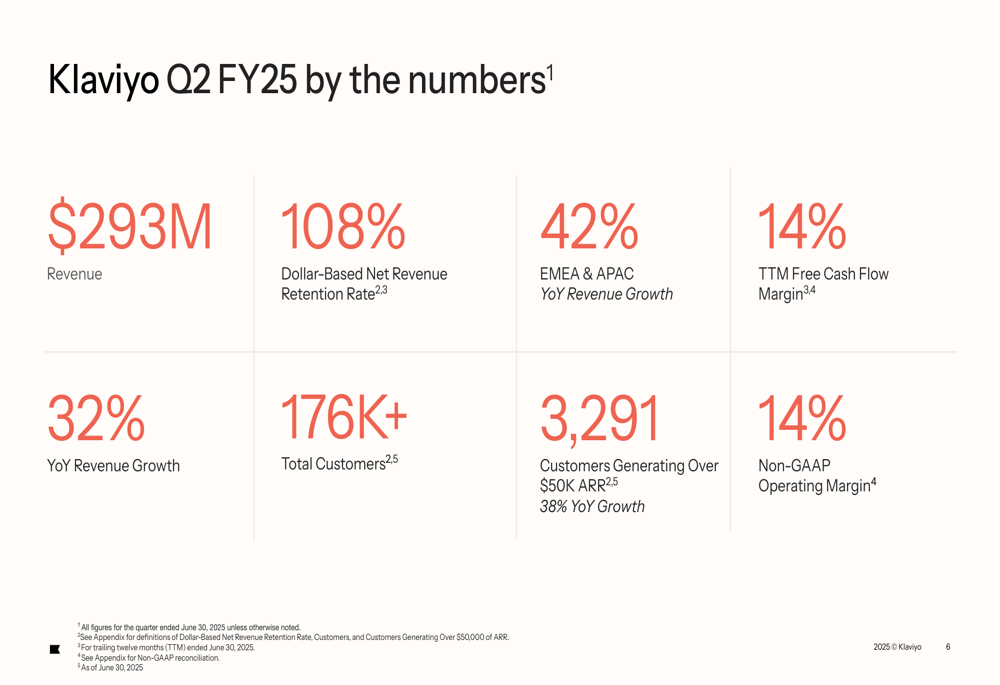

Klaviyo reported Q2 2025 revenue of $293 million, representing 32% year-over-year growth and exceeding the guidance provided in its Q1 earnings report, which projected Q2 revenue between $276-280 million.

As shown in the following summary of key performance metrics, the company maintained strong momentum across multiple dimensions:

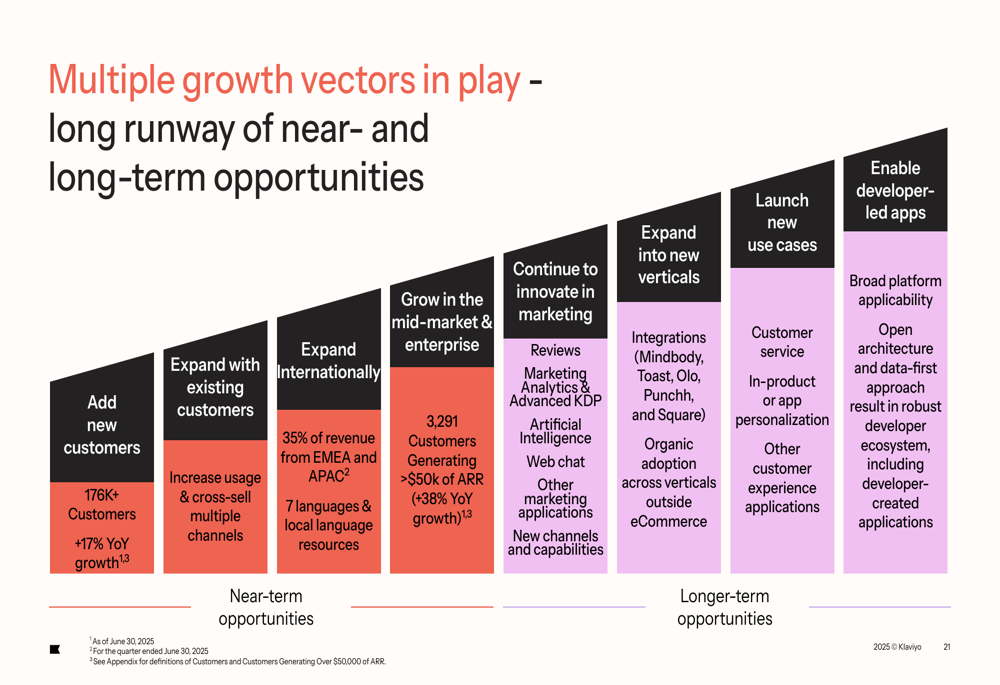

The company’s dollar-based net revenue retention rate of 108% indicates healthy expansion within its existing customer base. Particularly impressive was the 38% year-over-year growth in customers generating over $50,000 in annual recurring revenue (ARR), reaching 3,291 such customers. This demonstrates Klaviyo’s success in moving upmarket and increasing customer value.

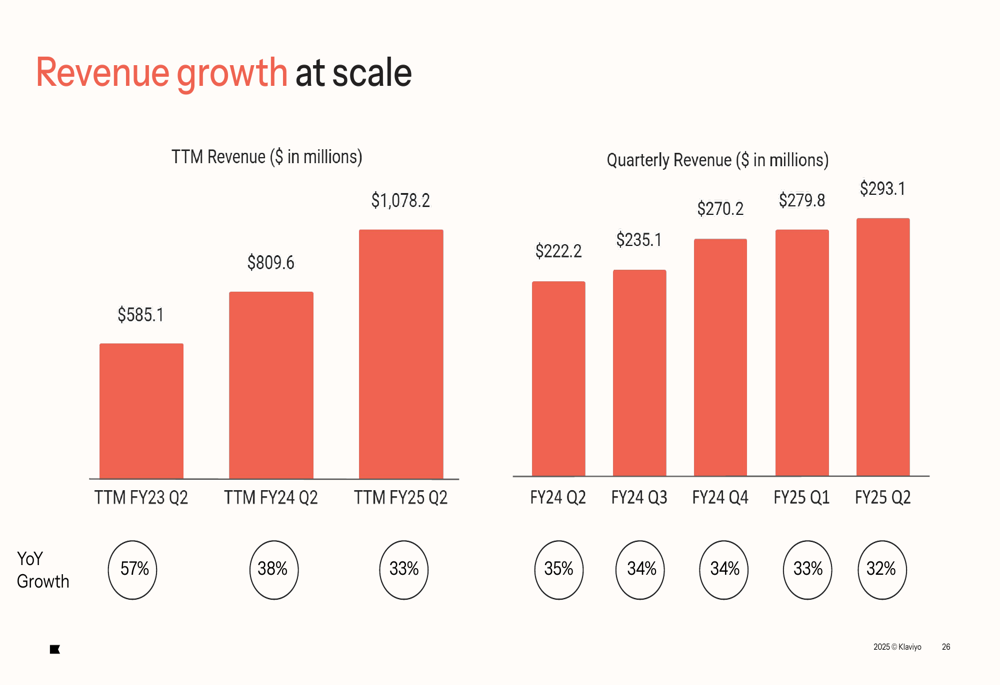

The revenue growth trajectory has remained consistent over recent quarters, as illustrated in the following chart:

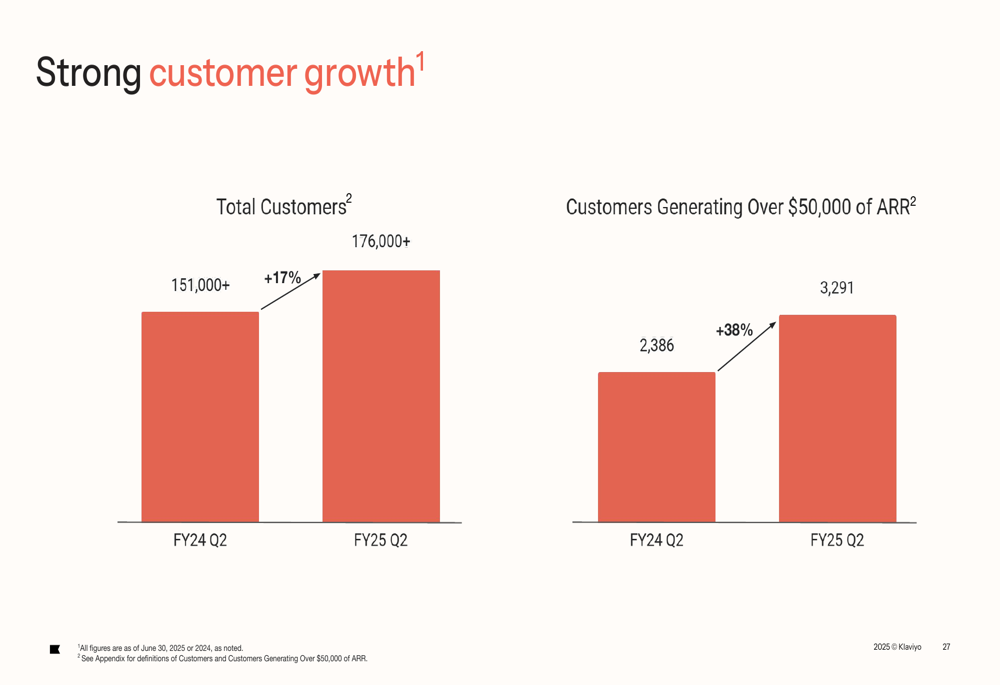

Customer growth has also been robust, with total customers increasing to over 176,000, up from approximately 151,000 in the same quarter last year:

Strategic Initiatives

Klaviyo highlighted several strategic initiatives driving its growth, including product innovation, international expansion, and AI integration.

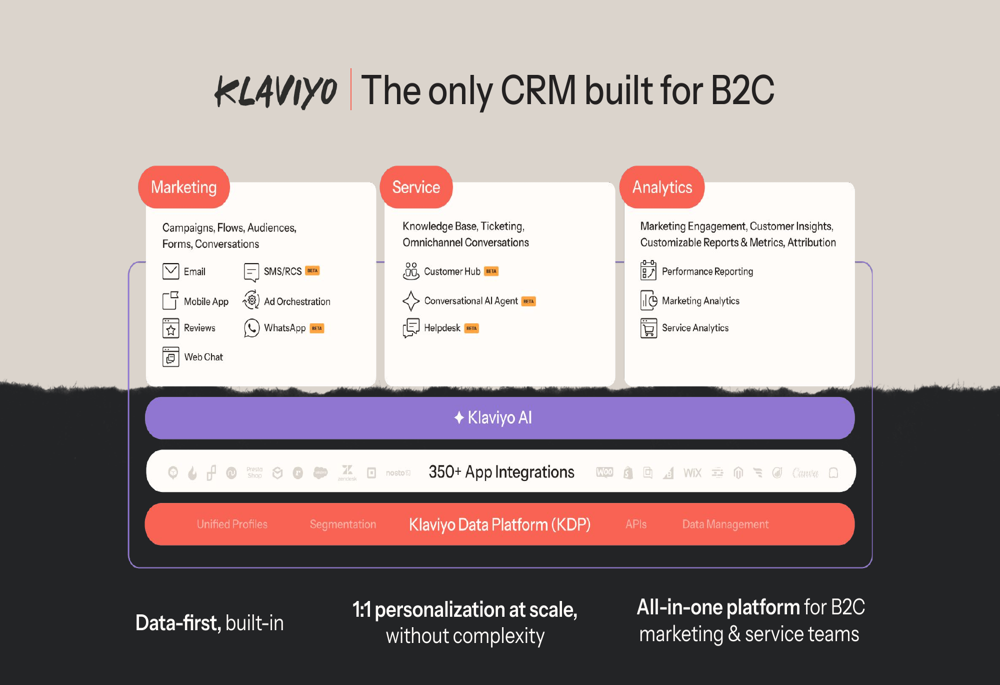

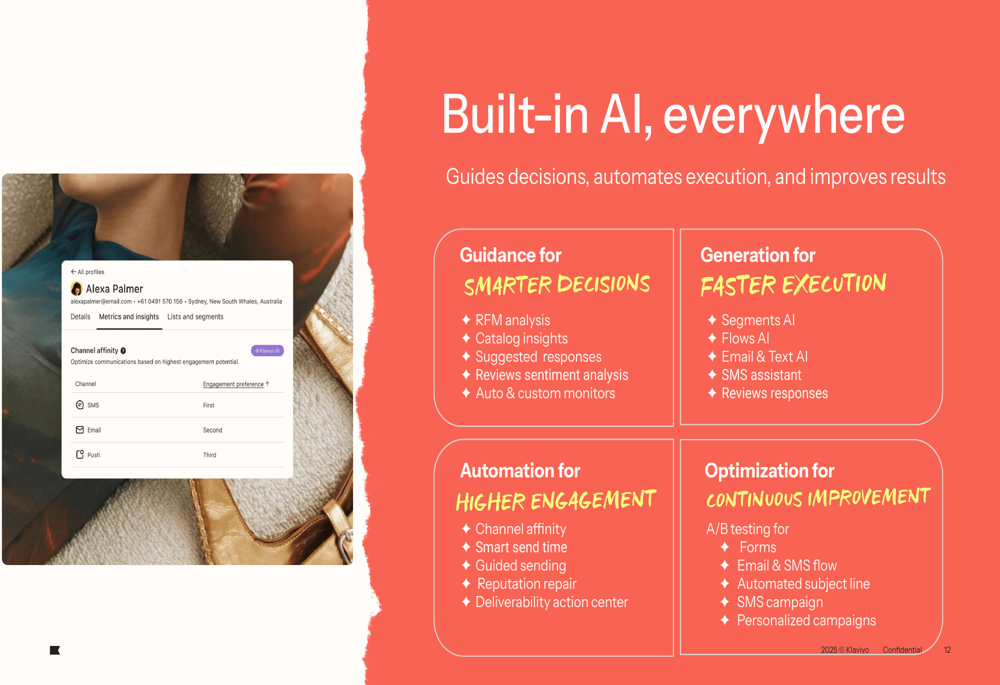

The company is positioning itself as a comprehensive B2C CRM platform that combines marketing automation, analytics, and customer service capabilities. This integrated approach is illustrated in their platform overview:

A key focus area is the integration of AI throughout the platform, which Klaviyo believes provides a competitive advantage by enabling smarter decision-making, faster execution, and improved customer engagement:

Klaviyo is also expanding its product offerings with new capabilities like WhatsApp integration and an omnichannel campaign builder, which should help drive further growth and customer adoption.

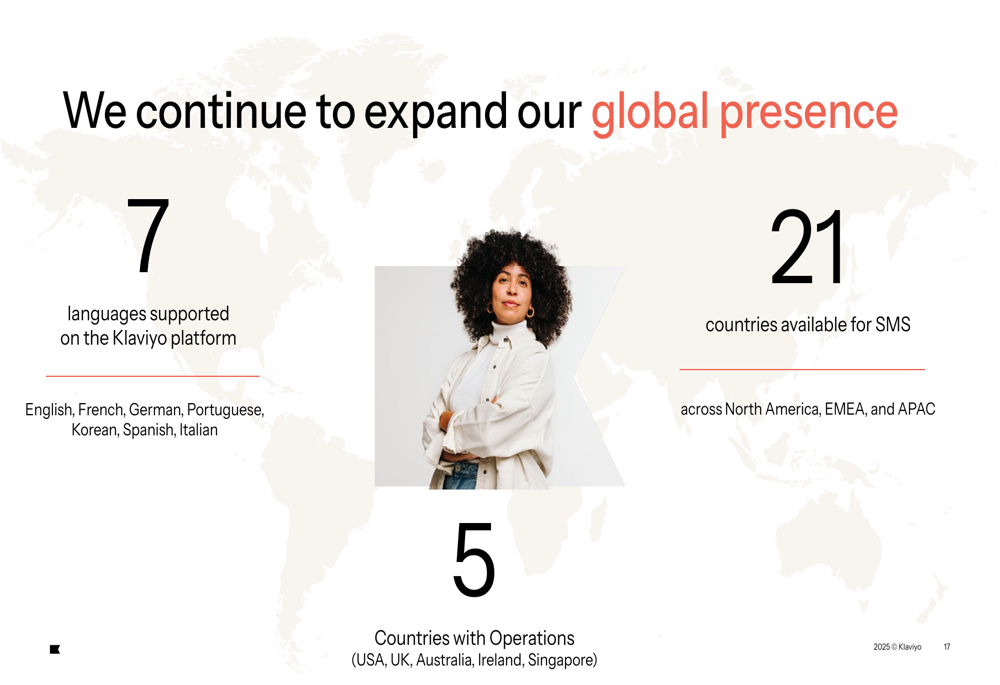

The company continues to invest in international expansion, with operations now in five countries and support for seven languages. International markets are growing faster than the overall business, with EMEA and APAC regions showing 42% year-over-year revenue growth:

Detailed Financial Analysis

Klaviyo’s financial performance demonstrates the company’s ability to balance growth with profitability. The company reported a non-GAAP operating margin of 14% for Q2 2025, slightly down from 15% in Q2 2024, reflecting continued investments in sales and marketing to drive growth.

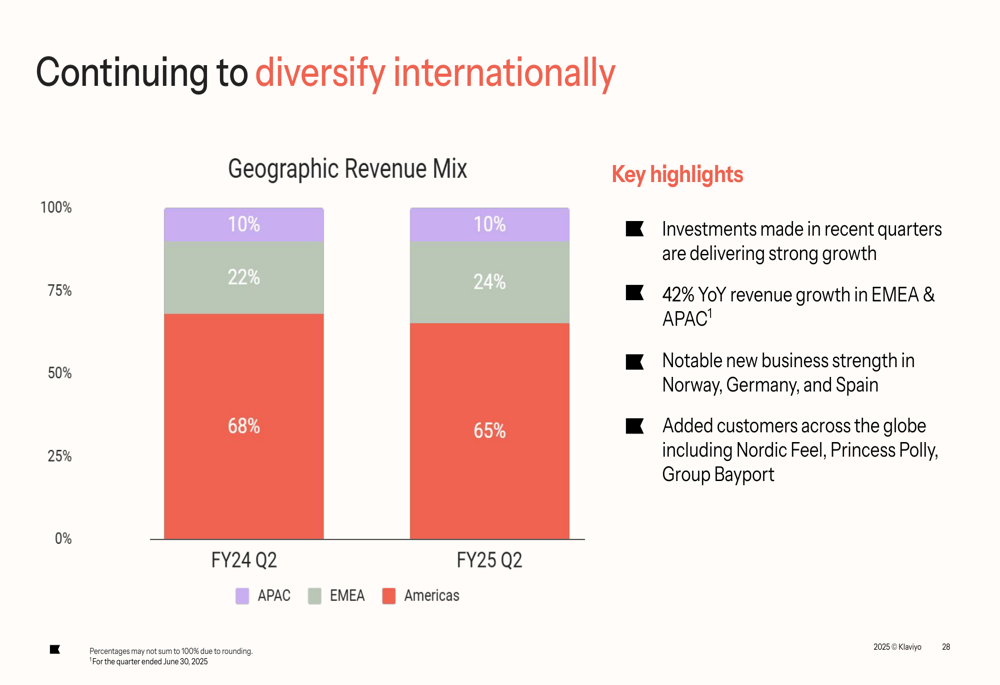

Geographic revenue diversification continues to improve, with the Americas now representing 65% of revenue (down from 68% a year ago), while EMEA has increased to 24% (up from 22%):

The company’s free cash flow generation remains strong, with a trailing twelve-month free cash flow margin of 14%. Q2 2025 free cash flow was $59.3 million, representing a 20.2% margin for the quarter.

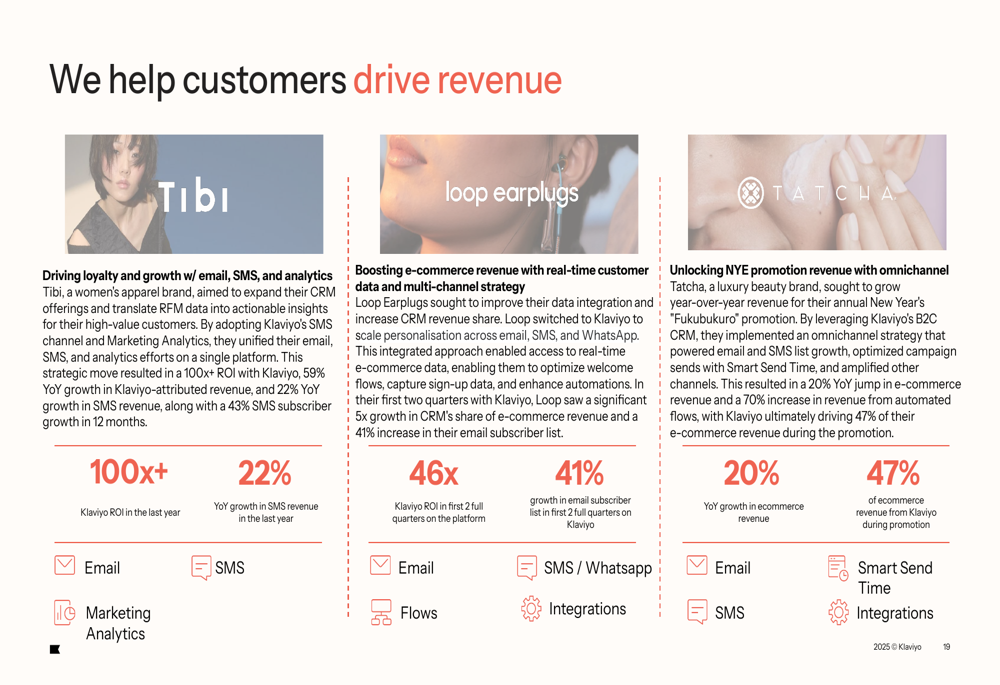

Klaviyo’s success with customers is demonstrated through several case studies, showing significant return on investment across different industry segments:

Forward-Looking Statements

Klaviyo provided guidance for Q3 FY25 and updated its full-year outlook, projecting continued strong growth:

For Q3 FY25:

- Revenue of $297-301 million (26-28% YoY growth)

- Non-GAAP operating income of $32.5-35.5 million (11-12% margin)

For full-year FY25:

- Revenue of $1,195-1,203 million (27-28% YoY growth)

- Non-GAAP operating income of $144-150 million (12% margin)

This guidance represents an increase from the company’s previous full-year outlook provided in Q1, which projected revenue of $1,171-1,179 million.

Klaviyo sees significant growth potential ahead, with a global total addressable market (TAM) of $68 billion, of which the company has penetrated only about 2% so far. The company’s growth strategy focuses on multiple vectors:

Competitive Industry Position

Klaviyo emphasizes its unique position as the only CRM built specifically for B2C companies. The company’s data-first approach and vertically integrated technology stack are presented as key competitive advantages:

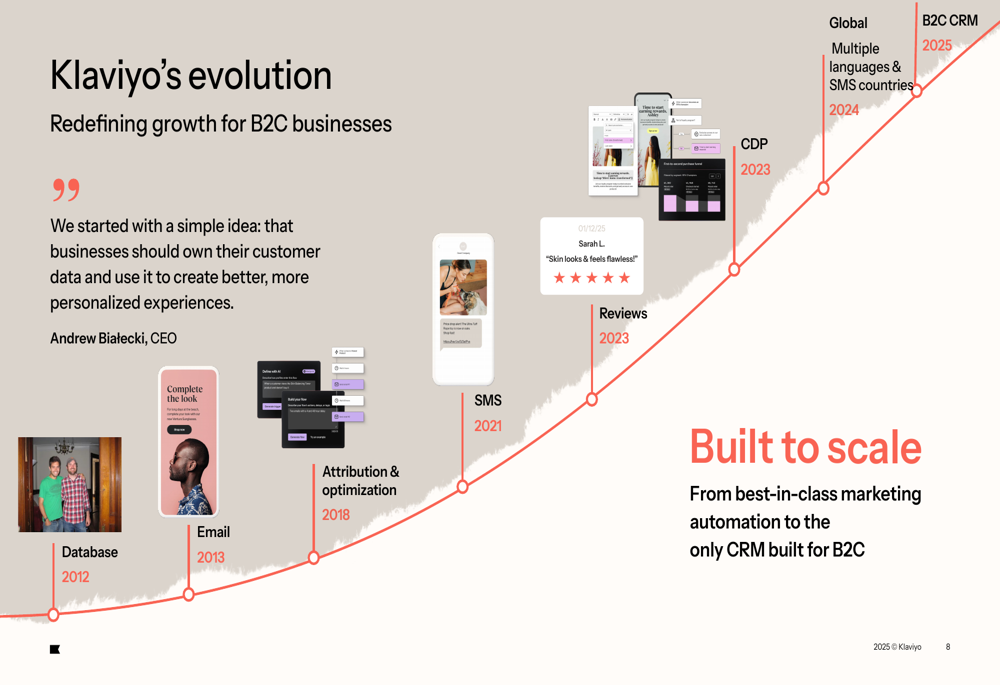

The company has evolved from its origins as an email marketing platform to become a comprehensive CRM solution for consumer brands. This evolution has been driven by continuous product innovation and expansion into new capabilities:

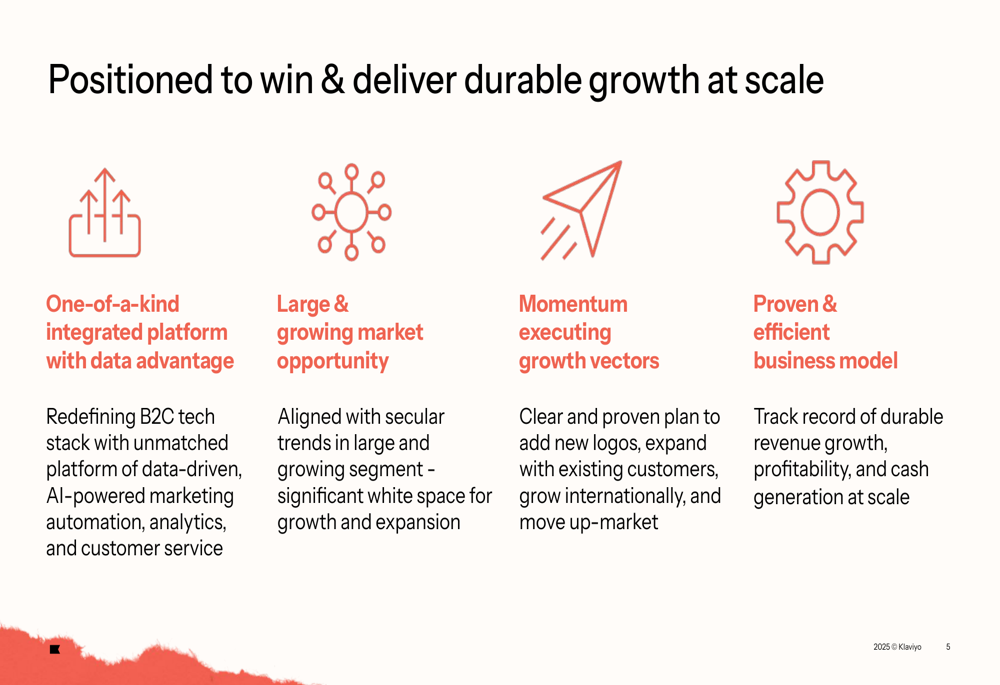

With its strong financial performance, expanding product capabilities, and large market opportunity, Klaviyo appears well-positioned to continue its growth trajectory. The company’s focus on AI integration, international expansion, and moving upmarket should provide multiple avenues for sustained growth in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.