Lisa Cook sues Trump over firing attempt, emergency hearing set

Introduction & Market Context

Knight-Swift Transportation (NYSE:KNX) reported a significant turnaround in its first quarter 2025 financial results, returning to profitability after posting losses in the same period last year. The transportation giant presented its Q1 2025 earnings on April 23, 2025, showcasing substantial year-over-year improvements across key financial metrics despite mixed segment performance.

The company’s results appear to validate management’s cautious optimism expressed during the Q3 2024 earnings call, when executives suggested that "the worst of this truckload cycle may be behind us" and predicted a gradual market recovery in 2025. Knight-Swift shares closed at $39.03 on the day of the earnings release but declined 2.8% to $38.50 in after-hours trading, remaining well below their 52-week high of $61.51.

Quarterly Performance Highlights

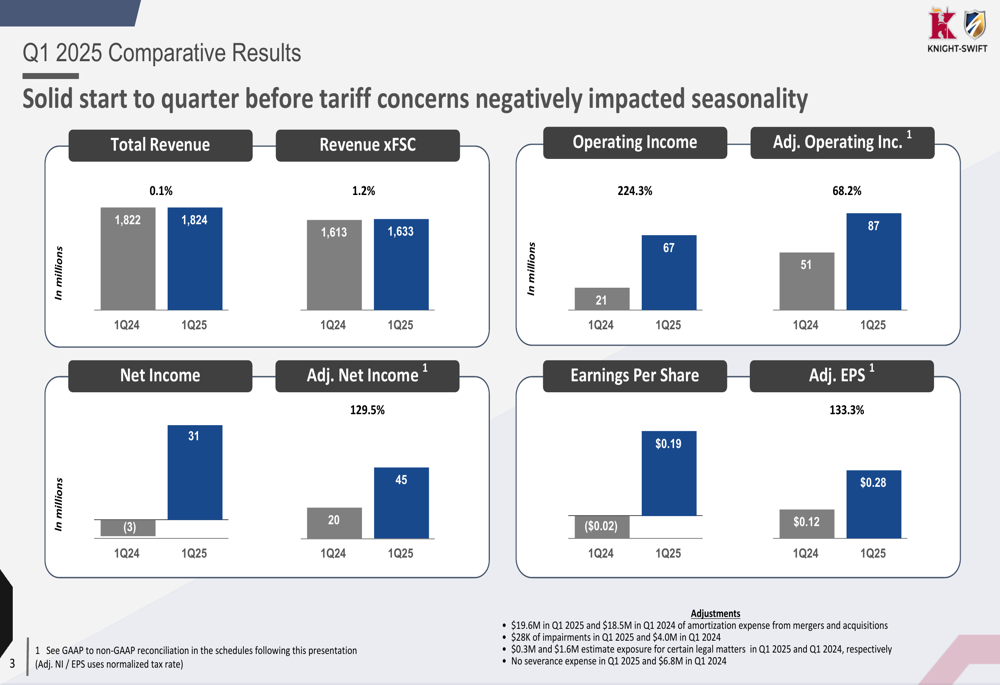

Knight-Swift reported total revenue of $1.82 billion for Q1 2025, essentially flat with a 0.1% increase from Q1 2024. However, revenue excluding fuel surcharges grew 1.2% to $1.63 billion. The company’s profitability metrics showed dramatic improvement, with operating income surging 224.3% to $67 million and adjusted operating income increasing 68.2% to $87 million.

The company returned to profitability with net income of $31 million compared to a $3 million loss in Q1 2024. Adjusted net income more than doubled, rising 129.5% to $45 million. Similarly, earnings per share improved to $0.19 from a loss of $0.02 per share in the prior-year period, while adjusted EPS jumped 133.3% to $0.28.

As shown in the following comparative results chart:

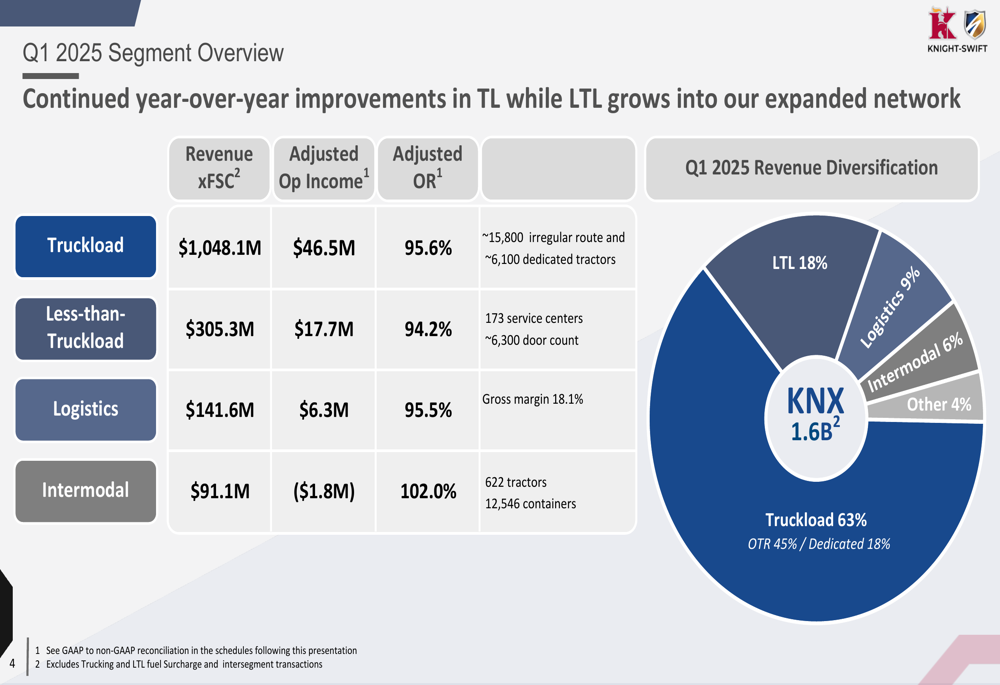

The company’s segment revenue diversification shows the truckload segment remains dominant at 63% of total revenue, with less-than-truckload (LTL) accounting for 18%, logistics 9%, intermodal 6%, and other segments 4%. Knight-Swift operates approximately 15,800 irregular route tractors and 6,100 dedicated tractors in its truckload segment, while its LTL network encompasses 173 service centers with about 6,300 door count.

The following segment overview illustrates the company’s diverse transportation operations:

Segment Analysis

Truckload Segment

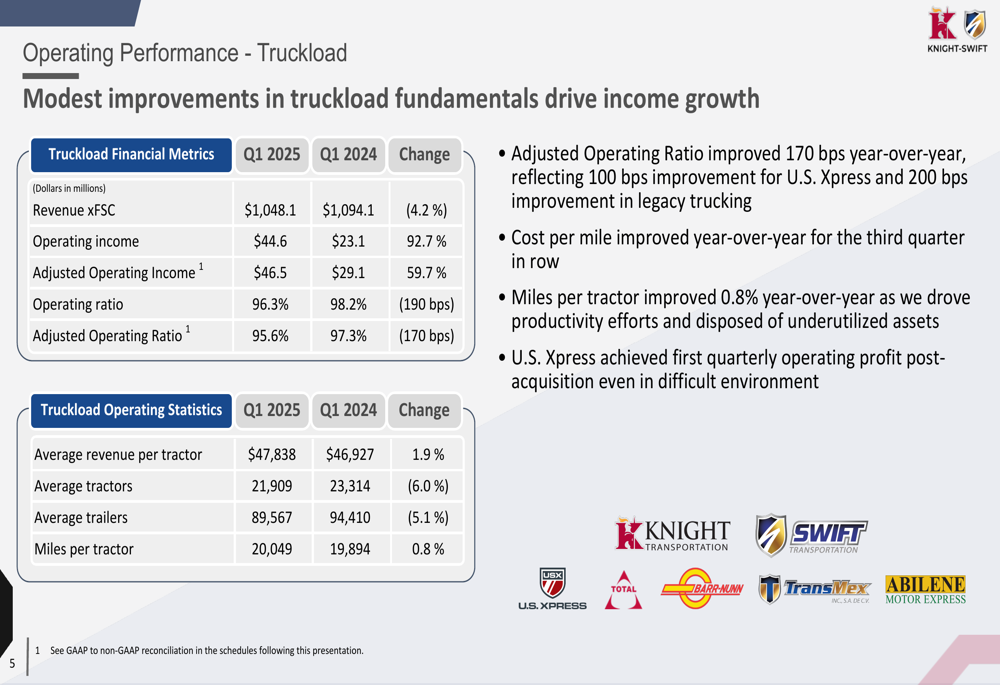

The truckload segment, Knight-Swift’s largest business unit, experienced a 4.2% decline in revenue excluding fuel surcharges to $1.05 billion. Despite this revenue decrease, the segment’s profitability improved substantially, with operating income nearly doubling (92.7%) to $44.6 million and adjusted operating income increasing 59.7% to $46.5 million. The adjusted operating ratio improved 170 basis points to 95.6%.

This improved profitability came despite a 6.0% reduction in average tractors to 21,909 units, as the company achieved a 1.9% increase in average revenue per tractor to $47,838 and a 0.8% improvement in miles per tractor to 20,049.

The following chart details the truckload segment’s performance metrics:

Less-Than-Truckload Segment

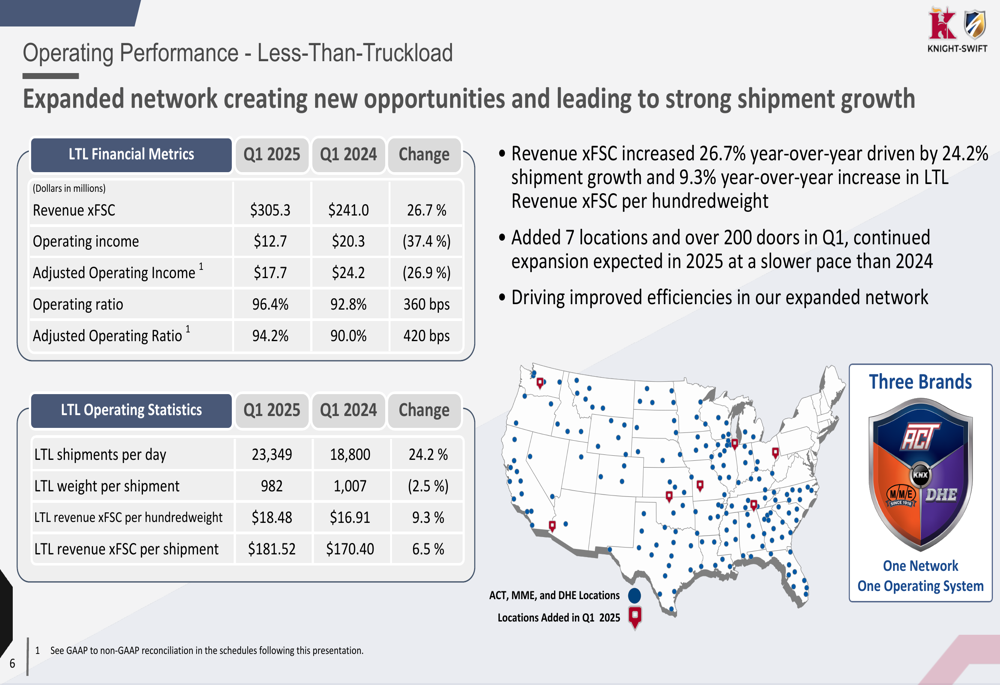

Knight-Swift’s LTL segment showed robust revenue growth of 26.7% to $305.3 million (excluding fuel surcharges), driven by a 24.2% increase in shipments per day to 23,349. However, profitability declined, with operating income falling 37.4% to $12.7 million and adjusted operating income decreasing 26.9% to $17.7 million. The adjusted operating ratio deteriorated by 420 basis points to 94.2%.

The segment benefited from pricing improvements, with revenue per hundredweight increasing 9.3% to $18.48 and revenue per shipment rising 6.5% to $181.52, partially offsetting a 2.5% decrease in weight per shipment.

The LTL segment’s performance metrics are illustrated in the following chart:

Logistics Segment

The logistics segment delivered strong results, with revenue excluding intersegment transactions growing 11.8% to $141.6 million. Operating income more than doubled to $5.1 million, representing a 108.0% increase, while adjusted operating income rose 73.4% to $6.3 million. The adjusted operating ratio improved by 160 basis points to 95.5%.

This performance was driven by an 11.7% increase in revenue per load to $1,956 and a 130 basis point improvement in gross margin to 18.1%, reflecting the company’s disciplined pricing strategy in this segment.

Intermodal Segment

Knight-Swift’s intermodal segment remained challenging but showed signs of improvement. Revenue excluding intersegment transactions increased 3.5% to $91.1 million, while the operating loss narrowed by 63.1% to $1.8 million. The operating ratio improved by 360 basis points to 102.0%, though the segment continues to operate at a loss.

The improvement was driven by a 4.6% increase in load count to 35,211, offsetting a 1.1% decrease in average revenue per load to $2,587. The company operated 622 tractors and 12,546 containers in this segment during Q1 2025.

Forward Guidance

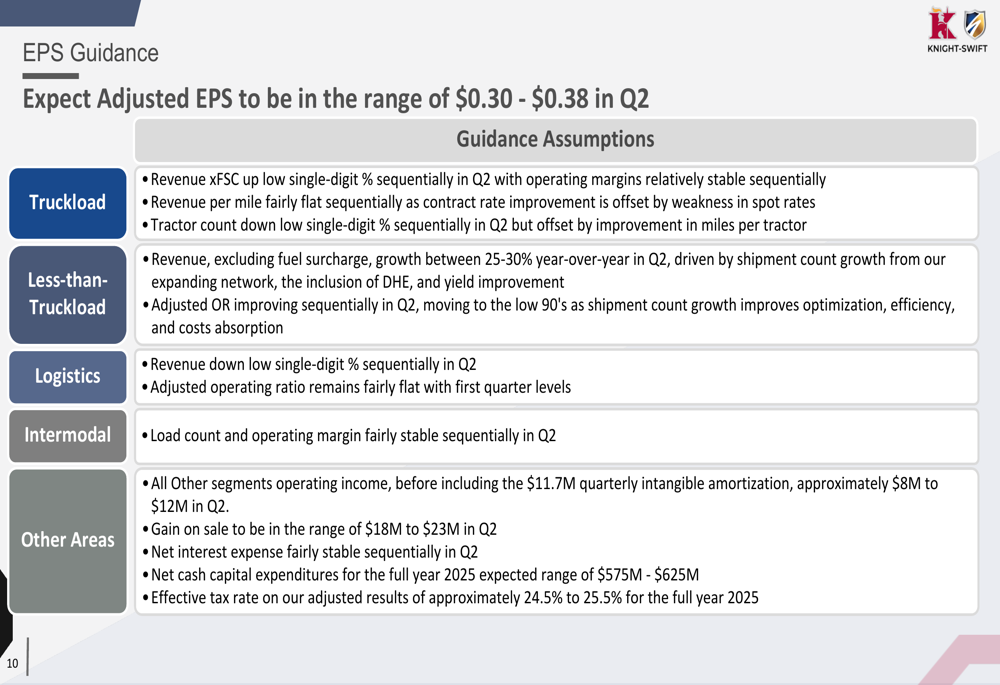

Knight-Swift provided guidance for Q2 2025, projecting adjusted earnings per share in the range of $0.30 to $0.38. The company outlined several assumptions supporting this guidance, including:

- Truckload revenue excluding fuel surcharges is expected to increase by a low single-digit percentage sequentially

- LTL revenue excluding fuel surcharges is projected to grow between 25-30% year-over-year

- Logistics revenue is anticipated to decrease by a low single-digit percentage sequentially

- Intermodal load count and operating margin are expected to remain relatively stable

- Gain on sale is forecasted to be in the range of $18 million to $23 million in Q2

The following slide details the company’s guidance for the upcoming quarter:

Market Reaction and Outlook

Despite the significant year-over-year improvement in profitability, Knight-Swift’s stock declined in after-hours trading following the earnings release. This reaction may reflect investor concerns about the mixed segment performance, particularly the profitability challenges in the LTL segment despite strong revenue growth.

The company’s return to profitability and improved adjusted operating ratios across most segments suggest that the market recovery anticipated by management is materializing. However, the continued operating loss in the intermodal segment and deteriorating operating ratio in the LTL business highlight ongoing challenges that may temper investor enthusiasm.

Knight-Swift’s guidance for Q2 2025 indicates management’s confidence in continued improvement, particularly in the truckload segment, which appears to be benefiting from more favorable market conditions after a challenging cycle. The projected strong growth in the LTL segment also suggests that the company’s strategic investments in this area are gaining traction, though profitability improvements remain a work in progress.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.