Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Knorr-Bremse AG (ETR:KBX) released its Q2 2025 financial results on July 31, showing improved profitability despite challenging conditions in the commercial vehicle market. The company reported a 60 basis point improvement in operating EBIT margin to 13.1%, driven primarily by strong performance in its Rail Vehicle Systems (RVS) segment, which offset headwinds in the Commercial Vehicle Systems (CVS) division.

The company’s stock has shown resilience, trading at €86.80 as of July 30, 2025, down slightly by 0.34% but maintaining its strong year-to-date performance. According to previous earnings reports, Knorr-Bremse has delivered impressive YTD returns of 28.82%, significantly outperforming broader market indices.

Quarterly Performance Highlights

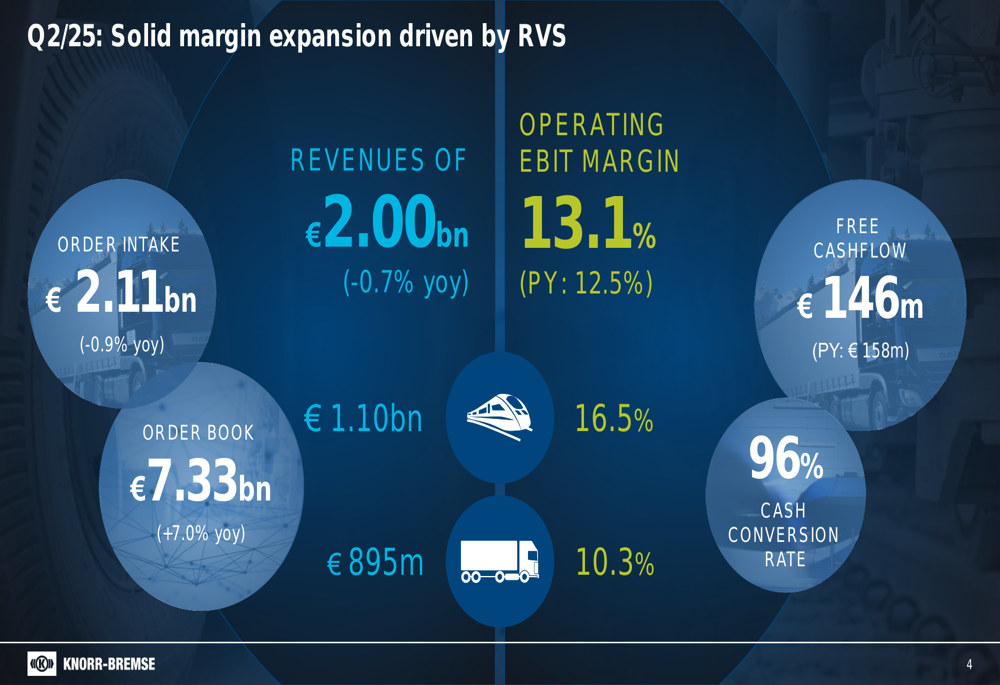

Knorr-Bremse reported Q2 2025 revenue of €2.00 billion, representing a slight decrease of 0.7% year-over-year. Despite this modest revenue decline, the company achieved an operating EBIT margin of 13.1%, up from 12.5% in the prior-year period. Order intake stood at €2.11 billion, down 0.9% year-over-year, while the order book increased by 7.0% to €7.33 billion.

As shown in the following chart of key financial metrics, the company maintained solid performance across major indicators:

Free cash flow reached €146 million, slightly below the prior year’s €158 million, but with a strong cash conversion rate of 96%. The company’s annualized ROCE improved to 21.3%, up from 20.2% in Q2 2024, demonstrating enhanced capital efficiency.

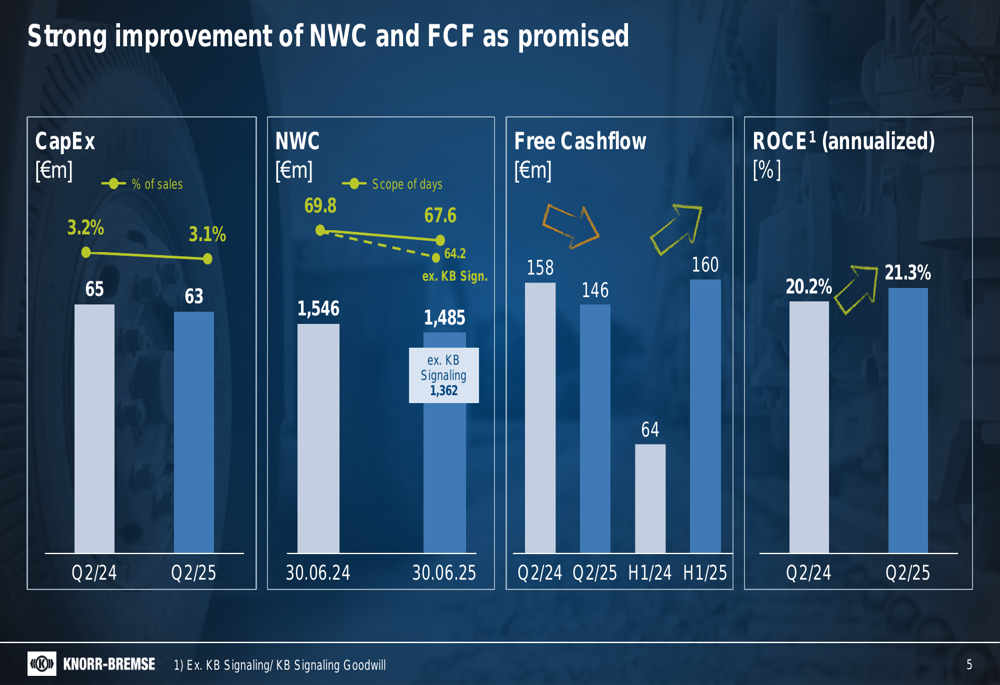

The company’s working capital management showed significant improvement, as illustrated in this chart:

Segment Analysis

Rail Vehicle Systems (RVS)

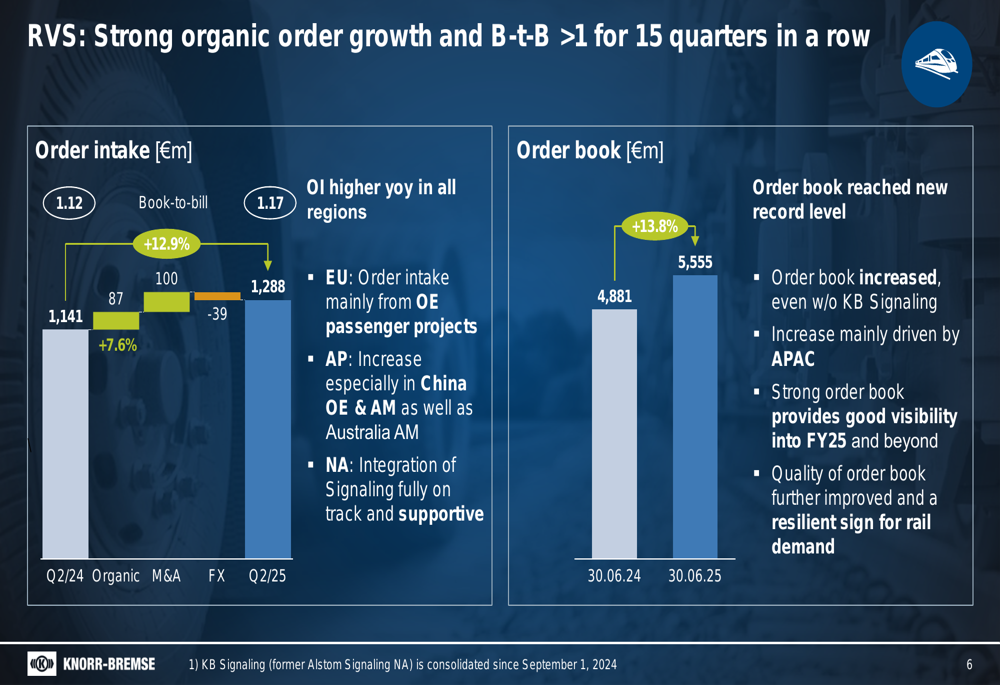

The RVS segment was the standout performer, with revenue increasing to €1.10 billion and operating EBIT margin reaching 16.5%, compared to 15.6% in the prior-year period. This segment benefited from strong organic order growth of 7.6% and a healthy book-to-bill ratio of 1.12.

The following chart illustrates the robust order growth in the RVS segment:

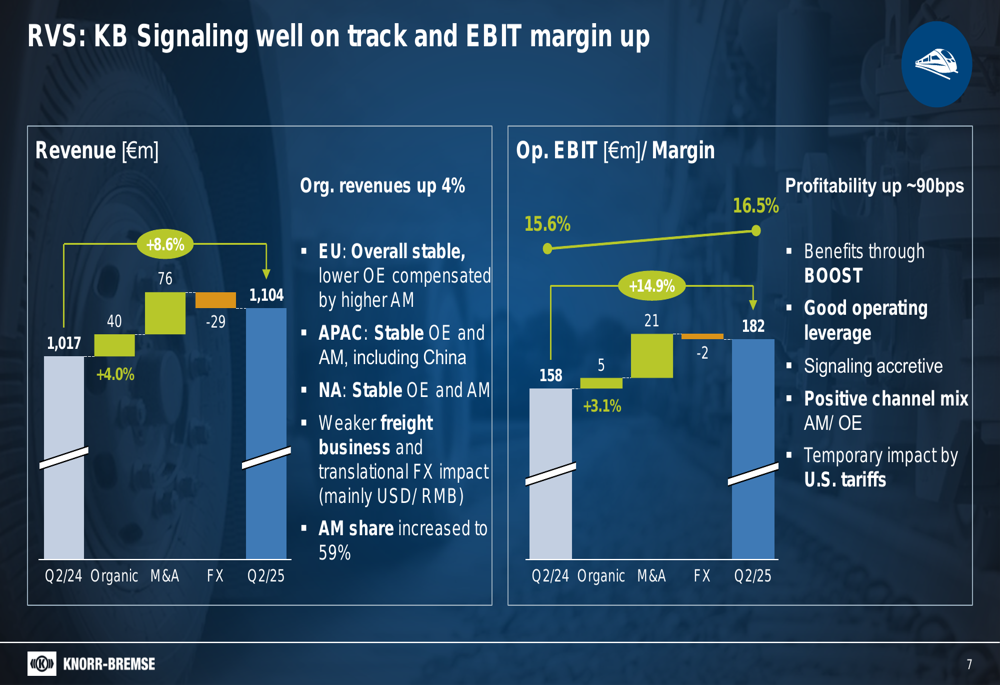

The integration of KB Signaling is progressing well and contributing positively to the segment’s performance. Organic revenue growth of 4% was complemented by M&A contribution of 8.6%, while FX impacts partially offset these gains.

As shown in the revenue and margin bridge below, the RVS segment’s profitability improvement was driven by multiple factors including BOOST program benefits, good operating leverage, and positive channel mix:

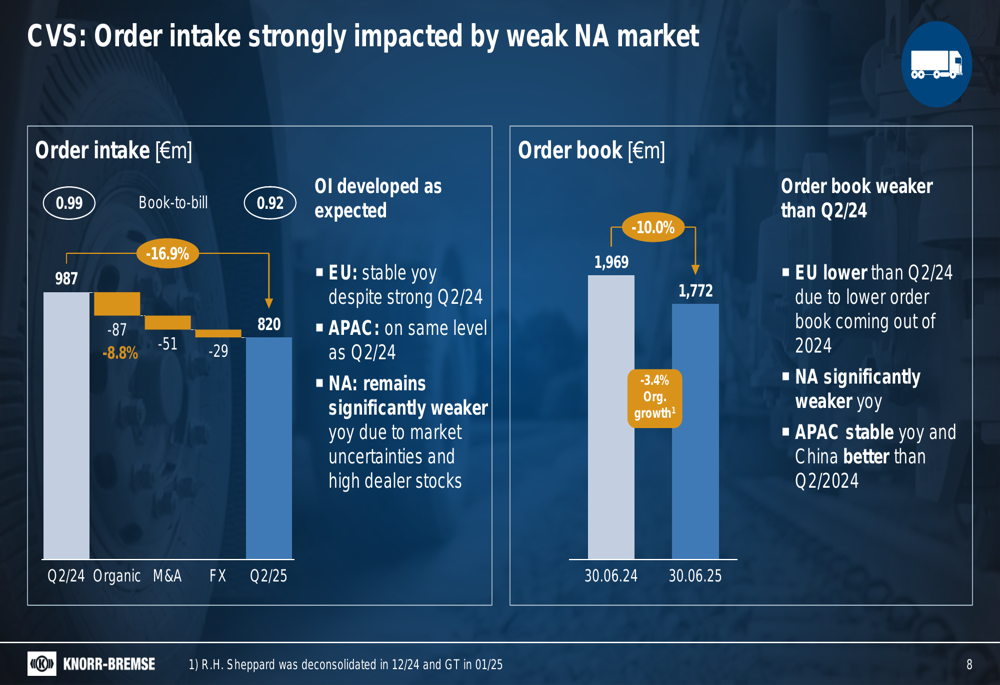

Commercial Vehicle Systems (CVS)

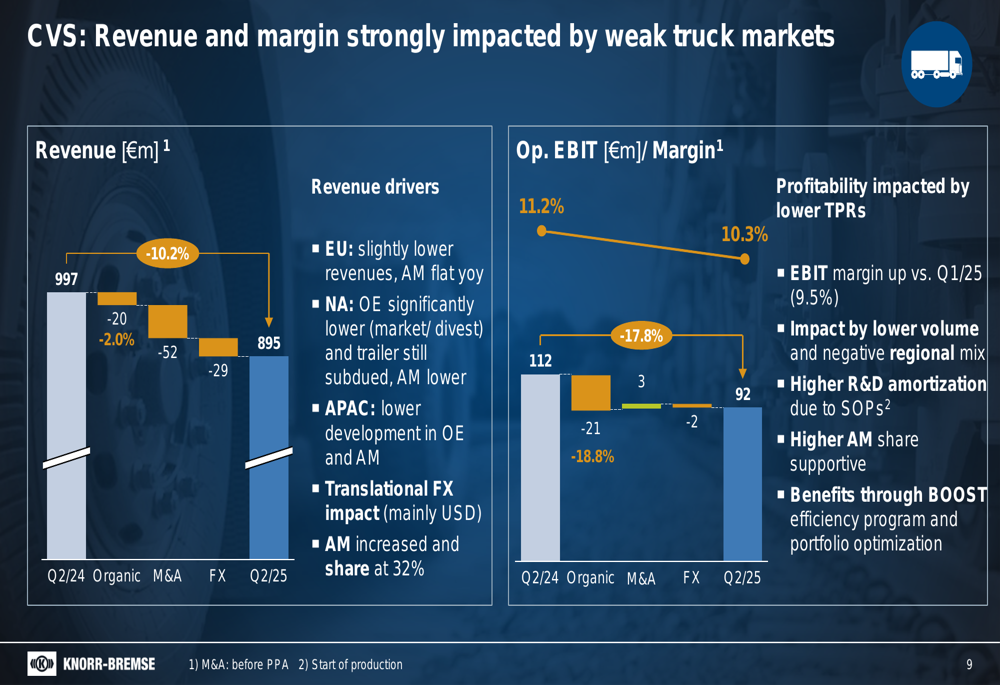

The CVS segment faced more challenging conditions, with revenue declining to €895 million from €997 million in the prior-year period. Operating EBIT margin decreased to 10.3% from 11.2%, primarily impacted by lower truck production rates, especially in North America.

The following chart shows the impact of the weak North American market on order intake:

Despite these challenges, the CVS segment showed sequential improvement, with the Q2 2025 margin of 10.3% higher than the Q1 2025 margin of 9.5%. The segment benefited from a higher aftermarket share (32%) and the BOOST efficiency program, which helped mitigate volume declines.

The revenue and margin performance of the CVS segment is illustrated in this chart:

Financial Position & Outlook

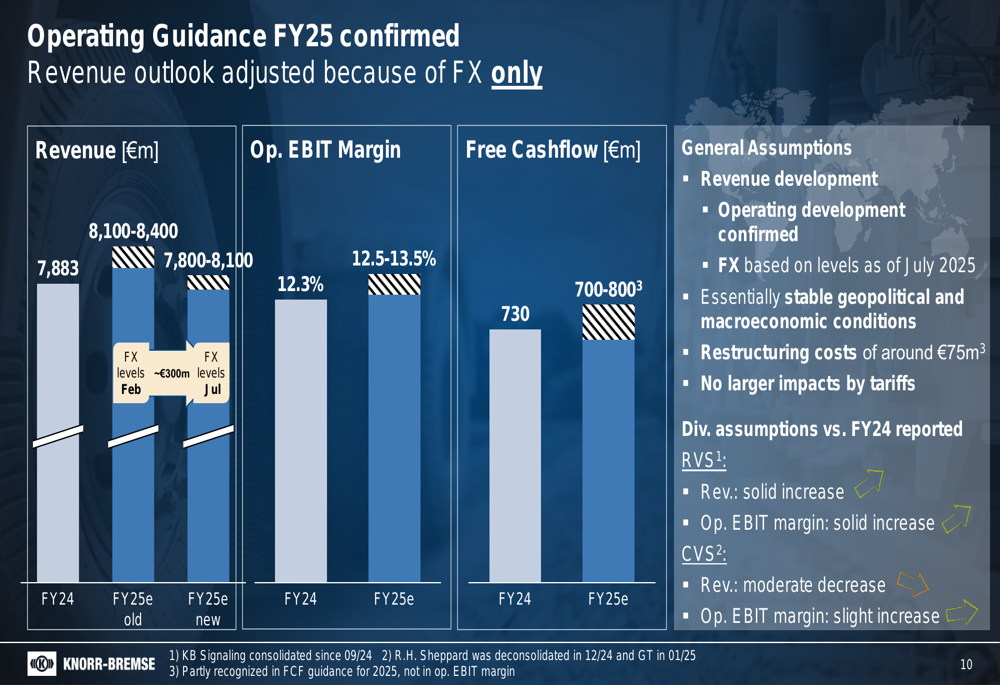

Knorr-Bremse confirmed its operating guidance for FY25, though it adjusted its revenue outlook from €8,100-8,400 million to €7,800-8,100 million, attributing the change solely to FX translation effects. The company maintained its operating EBIT margin guidance of 12.5-13.5% and free cash flow target of €700-800 million.

The following chart details the company’s guidance for FY25:

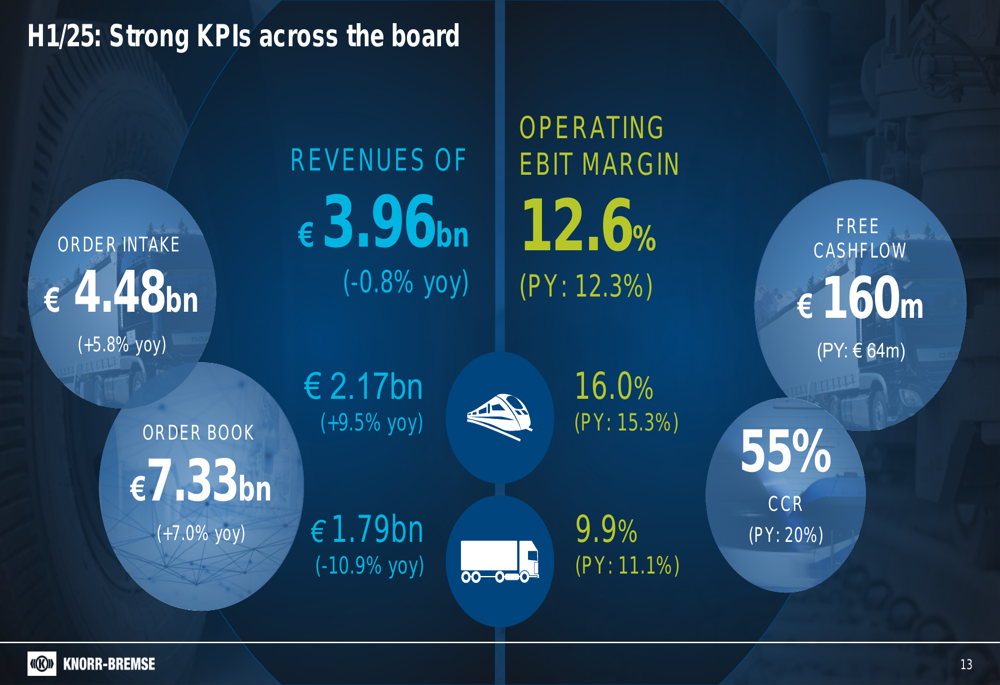

For the first half of 2025, Knorr-Bremse reported strong KPIs across the board, with an operating EBIT margin of 12.6% (up from 12.3% in H1 2024) and free cash flow of €160 million (up from €64 million). The cash conversion rate improved dramatically to 55% from 20% in the prior-year period.

As shown in this comprehensive H1 2025 performance overview:

Strategic Initiatives

The company’s BOOST efficiency program continues to deliver results, contributing to margin improvements in both segments. Management highlighted that the RVS segment has reached its mid-term target margin ahead of schedule, while the CVS segment is implementing strong measures to support profitability, particularly in North America.

Knorr-Bremse also noted potential mid-term benefits from German stimulus and European Defense Budget increases, with first orders expected in 2026/2027 for the RVS segment. The company continues to optimize its portfolio, as evidenced by its strategic approach to M&A activities.

Forward-Looking Statements

Looking ahead, Knorr-Bremse expects book-to-bill ratios to remain above 1 for the rail segment globally, with stable demand in Europe, good development in China, and positive momentum in India. For the truck segment, the company anticipates aftermarket development to outperform OE development, with truck production rates stabilizing in the second half of 2025 across all regions.

The company’s financial calendar for the remainder of 2025 includes several investor conferences in September and the Q3 2025 financial results release scheduled for October 30, 2025.

While the company faces challenges from potential U.S. tariff impacts and ongoing restructuring efforts (with costs estimated at around €75 million), management remains confident in its ability to navigate these headwinds through operational improvements and strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.