Apple announces iPhone 17 with 48MP cameras and 6.3-inch display

Introduction & Market Context

Korn Ferry (NYSE:KFY) released its fourth quarter fiscal year 2025 earnings presentation on June 18, showing a 4% year-over-year revenue increase at constant currency despite mixed performance across business segments. The global organizational consulting firm’s stock rose 3.36% in premarket trading to $69.00, reflecting positive investor sentiment following the results.

The company continues to position itself as a comprehensive talent solutions provider addressing a $450 billion market opportunity, with a strategic focus on integrating its various service offerings to drive sustainable growth. This quarter’s results demonstrate Korn Ferry’s ability to navigate variable market conditions while maintaining margin improvement.

Quarterly Performance Highlights

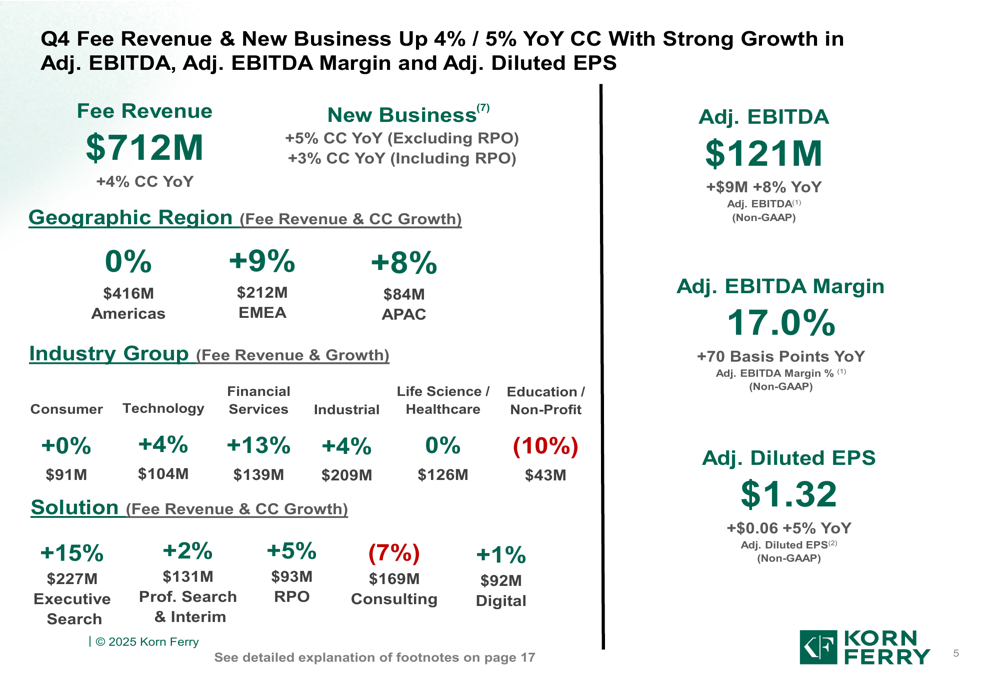

Korn Ferry reported Q4 FY’25 fee revenue of $712 million, representing a 4% year-over-year increase at constant currency. The company’s adjusted EBITDA reached $121 million, up 8% from the prior year, while adjusted EBITDA margin expanded by 70 basis points to 17.0%. Adjusted diluted earnings per share came in at $1.32, a 5% improvement year-over-year.

As shown in the following comprehensive overview of key metrics:

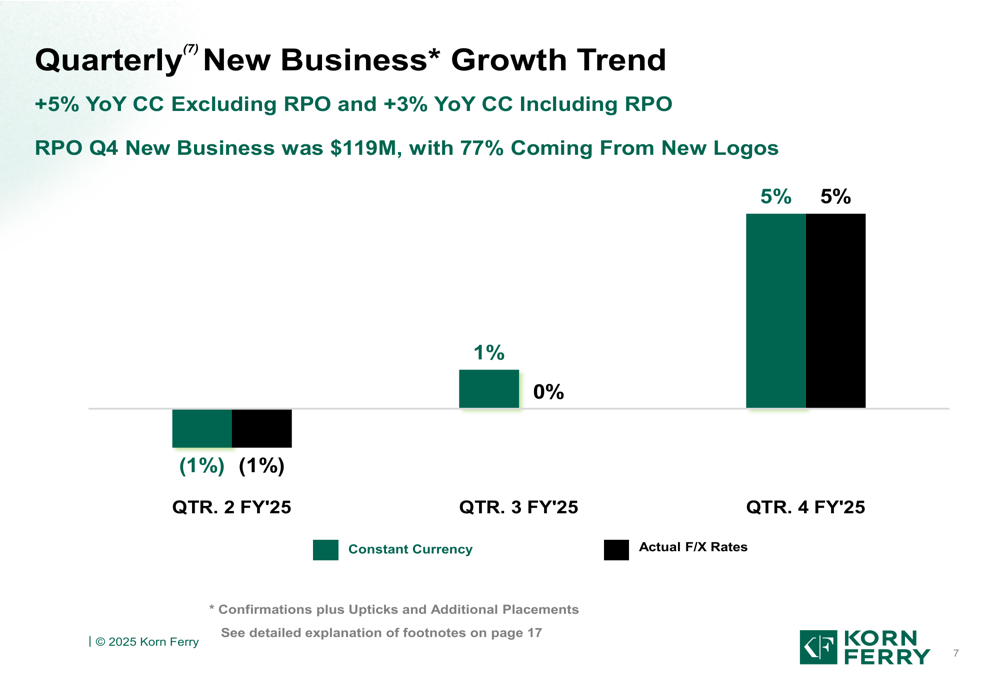

New business growth showed positive momentum at 5% year-over-year (excluding RPO) and 3% (including RPO), indicating continued demand for Korn Ferry’s services despite macroeconomic uncertainties. The company’s performance varied significantly across segments and regions, with Executive Search and international markets driving much of the growth.

Segment Performance Analysis

Executive Search emerged as the standout performer in Q4, with fee revenue increasing by 15% year-over-year at constant currency. This segment, which represents 32% of total fee revenue and 35% of adjusted EBITDA, saw a 10% increase in new assignments to 1,738. Adjusted EBITDA for Executive Search rose 19% with margins expanding by 100 basis points year-over-year.

The following chart illustrates the quarterly new business growth trend across segments:

In contrast, Consulting services experienced a 7% decline in fee revenue, despite a 4% increase in bill rates. The company attributed this to a shift toward longer engagements. Consulting represents 24% of fee revenue and 19% of adjusted EBITDA, with both metrics declining compared to the previous year.

Digital services, contributing 13% of fee revenue, showed modest growth of 1% year-over-year. Subscription and license revenue remained a key focus, accounting for 40% of the segment’s new business in Q4. Professional Search & Interim grew by 2%, while Recruitment Process Outsourcing (RPO) increased by 5%.

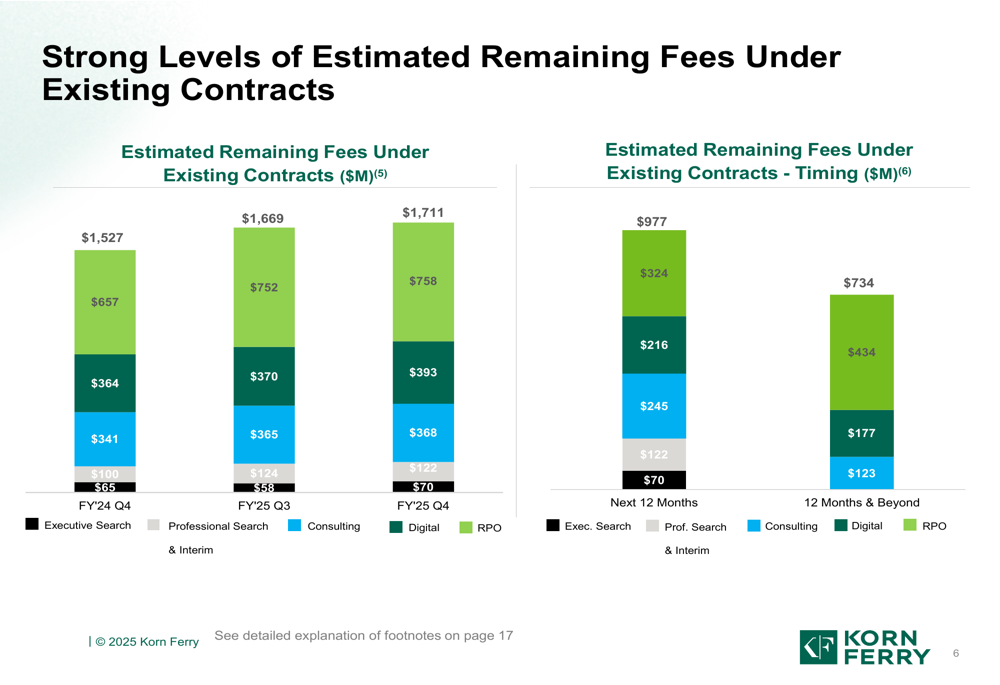

The company’s backlog of remaining fees under existing contracts provides visibility into future revenue streams, with Consulting showing the largest backlog at approximately $758 million:

Regional Performance Analysis

Geographic performance revealed significant disparities, with international markets driving growth while the Americas remained flat. EMEA (Europe, Middle East, and Africa) led with 9% year-over-year growth at constant currency, representing 30% of total fee revenue. Similarly, APAC (Asia-Pacific) grew by 8%, though it constitutes a smaller portion of the business at 12% of fee revenue.

The Americas region, which accounts for 58% of Korn Ferry’s fee revenue, showed no growth compared to the previous year. This regional disparity highlights the importance of the company’s global diversification strategy in maintaining overall growth.

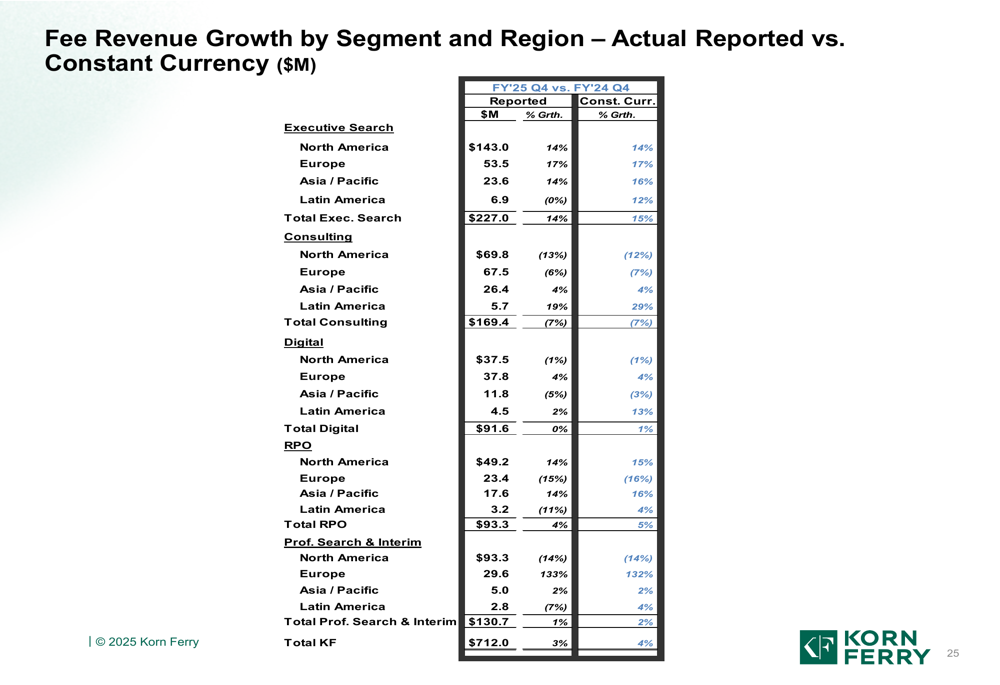

The following detailed breakdown illustrates fee revenue growth by segment and region:

Capital Allocation & Financial Position

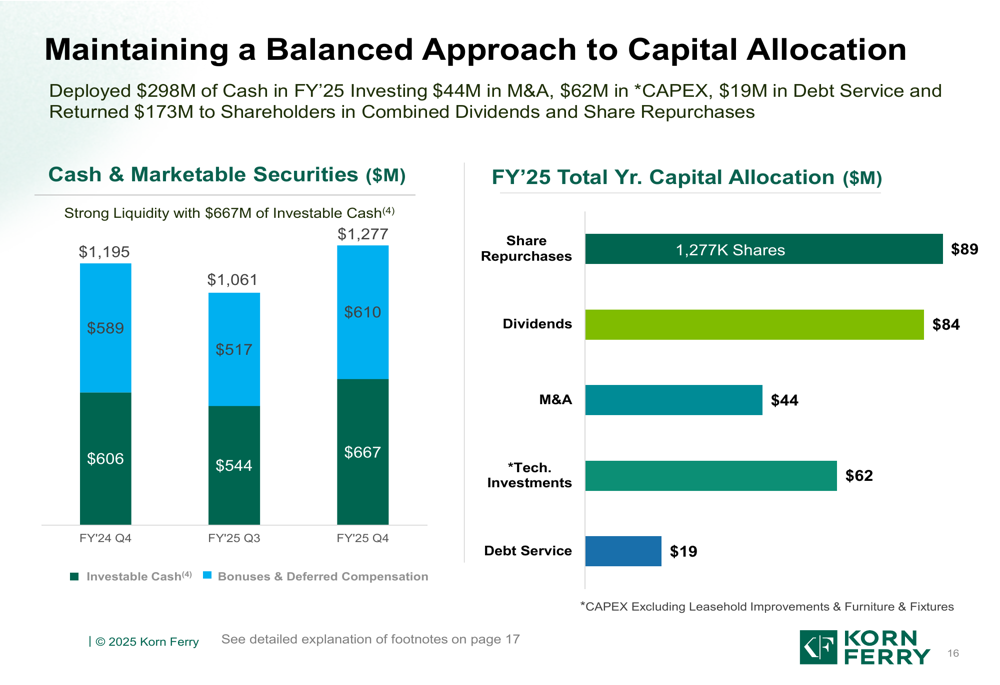

Korn Ferry maintained a balanced approach to capital allocation in FY’25, returning $173 million to shareholders through dividends and share repurchases while investing $44 million in M&A and $62 million in capital expenditures. The company reported strong liquidity with $667 million in investable cash.

This strategic allocation of capital reflects Korn Ferry’s commitment to shareholder returns while continuing to invest in growth opportunities:

The company’s financial position remains solid, with sufficient cash to fund operations and strategic initiatives. Korn Ferry’s approach to capital management aligns with its long-term growth strategy, which includes both organic expansion and selective acquisitions.

Strategic Positioning & Future Outlook

Korn Ferry continues to emphasize its unique positioning as a global organizational consulting firm with integrated talent solutions. The company highlighted that its "Marquee & Diamond Accounts" generate approximately 40% of fee revenues, with 77% of clients purchasing two or more solutions. Cross-solution referrals account for 25% of fee revenue, demonstrating the effectiveness of the company’s integrated approach.

The company’s strategy leverages proprietary intellectual property, including data from over 10 billion data points covering assessments, compensation information for more than 28 million individuals across 31,000 companies, and employee engagement data for over 38 million colleagues.

As illustrated in the following overview of Korn Ferry’s strategic positioning:

Looking ahead, Korn Ferry’s diverse service offerings and global presence position it to navigate varying market conditions. The strong performance in Executive Search and international markets provides momentum, while the company continues to address challenges in the Consulting segment. With a robust backlog of existing contracts and continued focus on margin improvement, Korn Ferry appears well-positioned for sustained growth despite segment variability.

The market’s positive reaction to the results, with the stock trading up 3.36% in premarket to $69.00, suggests investor confidence in the company’s strategy and execution. This represents a continued recovery toward the stock’s 52-week high of $80.64, reflecting optimism about Korn Ferry’s future prospects in the global talent management market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.