Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

KORU Medical (TASE:BLWV) Systems (NASDAQ:KRMD) presented its first quarter 2025 earnings results on May 7, 2025, showcasing continued momentum in its core business and strategic expansion initiatives. The company, which specializes in subcutaneous drug delivery systems, reported strong revenue growth and improved profitability metrics while raising its full-year guidance.

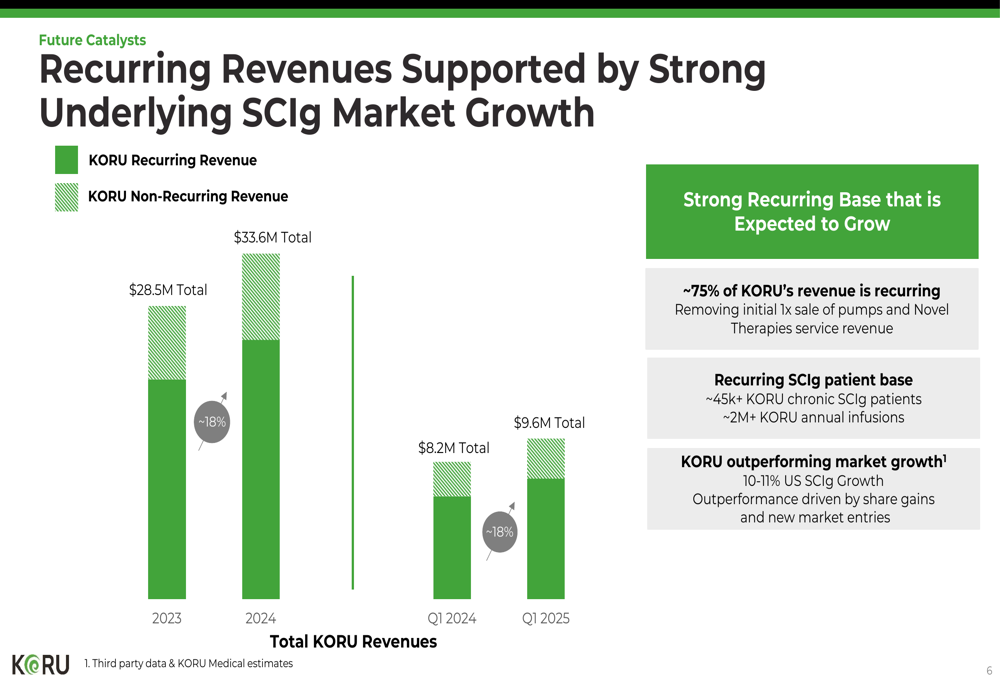

KORU’s Freedom Infusion System continues to benefit from the ongoing shift from intravenous (IV) hospital settings to subcutaneous (SC) therapy in home and infusion clinic settings. The system is currently used by approximately 45,000 chronic patients receiving subcutaneous immunoglobulin (SCIg) therapy, generating over 2 million annual infusions.

The stock closed at $2.72 on the day of the earnings presentation, with a modest 1.1% gain in after-hours trading. This performance comes after the stock experienced a 4.57% decline following its Q4 2024 earnings release, despite beating expectations at that time.

Quarterly Performance Highlights

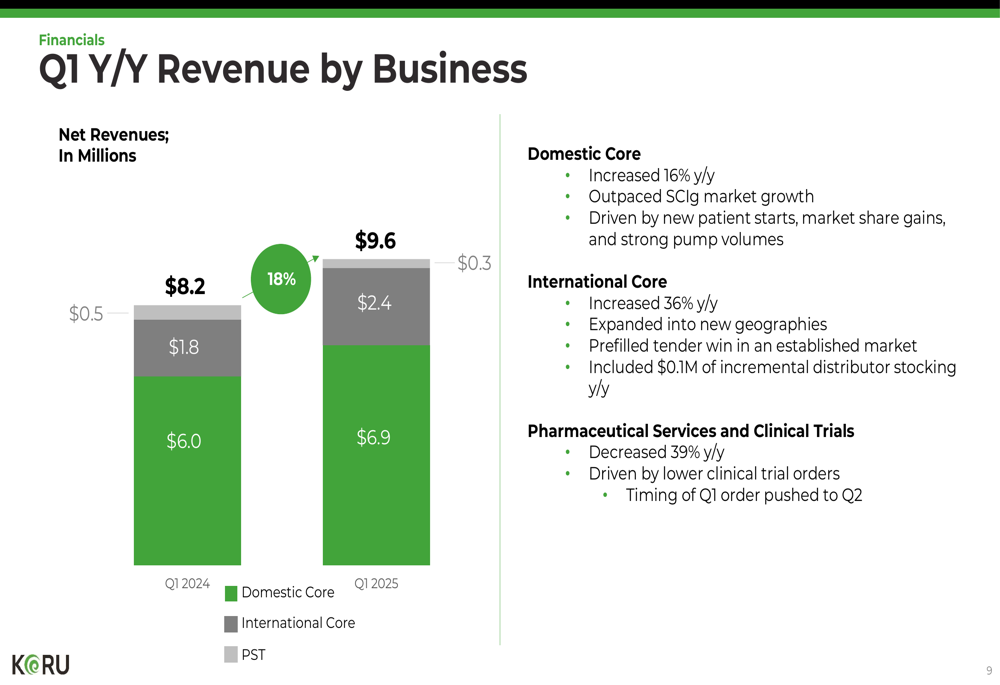

KORU Medical reported Q1 2025 revenues of $9.6 million, representing an 18% increase compared to the same period last year. The company’s core business, which includes both domestic and international segments, grew by an impressive 21%, driven by recurring revenues, new patient starts, market share expansion, and geographic growth.

As shown in the following breakdown of revenue by business segment:

Domestic core revenue increased by 16% year-over-year to $6.9 million, outpacing the underlying SCIg market growth. This performance was driven by new patient starts, market share gains, and strong pump volumes. International core revenue showed even stronger growth, jumping 36% year-over-year to $2.4 million as the company expanded into new geographies and secured a prefilled tender win in an established market.

The Pharmaceutical (TADAWUL:2070) Services and Clinical Trials (PST) segment, however, experienced a 39% year-over-year decline to $0.3 million, which the company attributed to lower clinical trial orders and timing issues, with a Q1 order pushed to Q2.

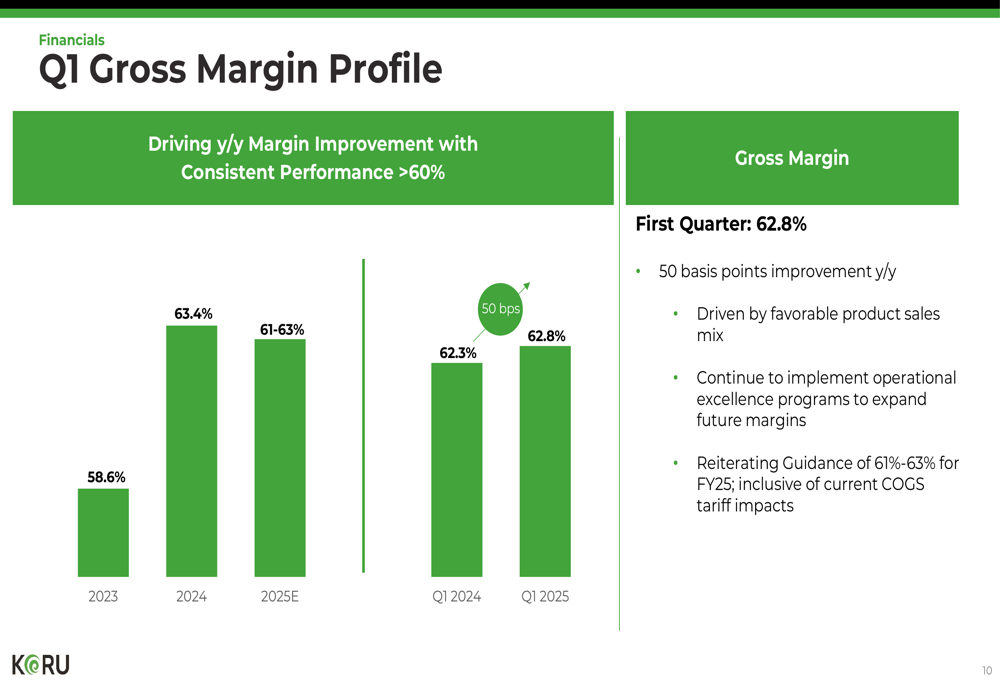

Gross margin improved to 62.8%, a 50 basis points increase compared to Q1 2024, driven by a favorable product sales mix. The company continues to implement operational excellence programs aimed at expanding future margins.

Strategic Growth Pillars

KORU Medical’s growth strategy is built on three pillars: defending and growing its leadership position in domestic SCIg, expanding internationally, and adding new drugs to its label through pharmaceutical services and clinical trials.

The company’s execution across these strategic areas has been strong, as illustrated in this summary:

In its domestic SCIg core business, KORU reported 16% year-over-year revenue growth in Q1, marking six consecutive quarters of sequential growth. The company is benefiting from double-digit SCIg market growth of approximately 10% year-over-year, while also expanding its market share.

The international segment showed remarkable 36% year-over-year growth in Q1, driven by strong SCIg adoption, entry into new geographic markets including the Middle East and North Africa (MENA), and expanded prefilled syringe opportunities.

The company’s recurring revenue model provides stability and predictability, with approximately 75% of total revenue coming from recurring sources. This model is supported by the growing SCIg patient base, which generates more than 2 million annual infusions.

Pipeline and Future Opportunities

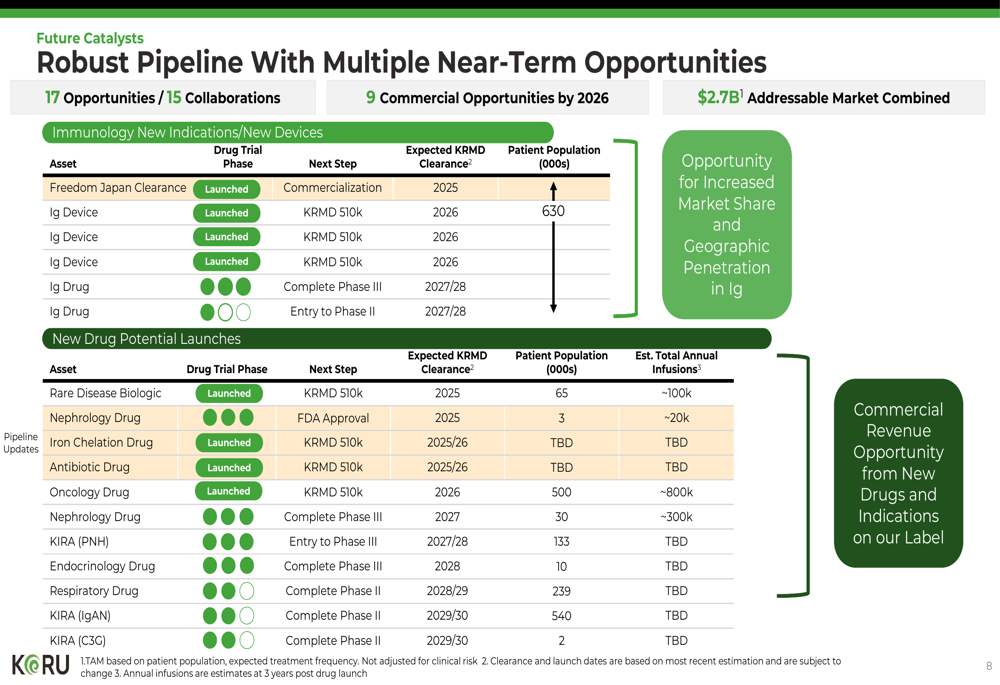

KORU Medical is actively expanding beyond its core SCIg market through collaborations with pharmaceutical companies. The company currently has 15 pharmaceutical collaborations in progress, with plans to submit for FDA 510(k) clearance with two commercialized drugs on the Freedom Infusion System in 2025.

The company’s robust pipeline includes multiple near-term opportunities across various therapeutic areas:

KORU expects to have 9 commercial opportunities by 2026, representing a combined addressable market of $2.7 billion. These opportunities span immunology, rare diseases, nephrology, oncology, and other therapeutic areas, with expected clearance dates ranging from 2025 to 2029/30.

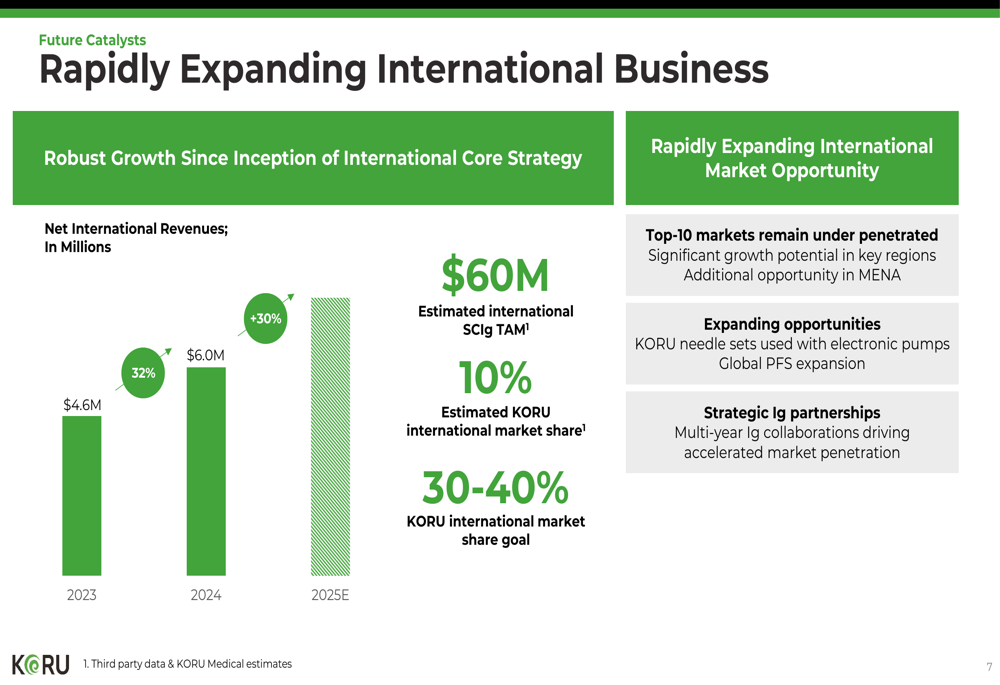

The company’s international expansion is also progressing rapidly, with net international revenues projected to grow by approximately 30% in 2025. KORU currently has an estimated 10% share of the $60 million international SCIg total addressable market (TAM) and is targeting 30-40% market share in the future.

Financial Outlook and Guidance

Based on its strong Q1 performance, KORU Medical has raised its 2025 revenue guidance to $38.5-$39.5 million, representing 15-17% growth compared to 2024. This is an increase from the previous guidance of $38-39 million (13-16% growth) provided during the Q4 2024 earnings call.

The company reiterated its gross margin guidance of 61-63% for the full year 2025, inclusive of current COGS tariff impacts. KORU also expects to generate positive cash flow from operations for the full year 2025.

As of March 31, 2025, the company had a cash balance of $8.7 million, with Q1 cash usage of $0.8 million. The net loss for the quarter was approximately $1.2 million, representing a 36% improvement compared to the same period last year.

Looking beyond 2025, KORU Medical has outlined a pathway to sustained growth of over 20% annually, driven by:

Key milestones for 2025 include three new pharmaceutical collaborations (two of which are already complete), multiple 510(k) submissions for new drugs on its label, commercial sales in Japan in the first half of 2025, and the launch of a Phase 1 flow controller in Q3 2025.

With its strong recurring revenue base, expanding international presence, and robust pipeline of new drug opportunities, KORU Medical appears well-positioned to capitalize on the growing trend toward subcutaneous drug delivery and achieve its ambitious growth targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.