Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Finnish wood products manufacturer Koskisen Ltd (HEL:KOSKI) reported strong revenue growth in its half-year 2025 results despite facing challenging market conditions. The company, currently trading near its 52-week high at €8.92, has maintained solid profitability while executing strategic investments and completing a significant acquisition.

CEO Jukka Pahta noted that the operating environment remains unstable, particularly regarding consumer-driven demand, while the situation in the Middle East continues to affect market conditions for softwood sawn timber. Meanwhile, weak economic conditions in Central Europe have impacted demand for birch plywood and chipboard products.

Quarterly Performance Highlights

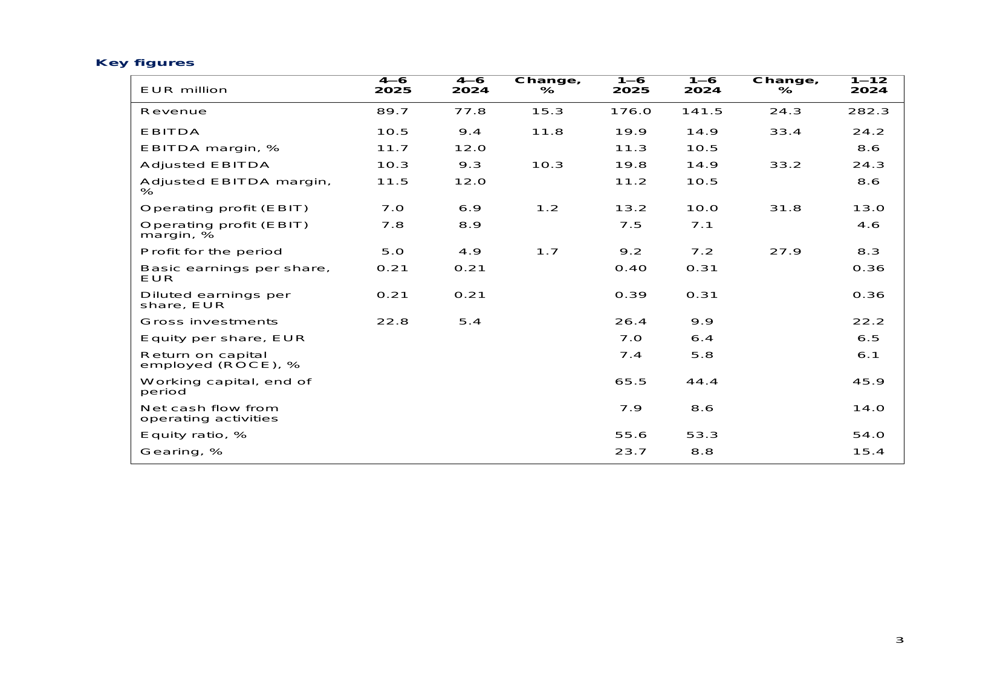

Koskisen reported consolidated revenue of €89.7 million for Q2 2025, representing a 15.3% increase from €77.8 million in the comparable period. For the first half of 2025, revenue jumped 24.3% to €176.0 million from €141.5 million in H1 2024.

As shown in the following comprehensive financial table, the company’s adjusted EBITDA for Q2 2025 increased to €10.3 million from €9.3 million in Q2 2024, though the margin slightly decreased to 11.5% from 12.0%:

Operating profit for Q2 2025 rose marginally to €7.0 million from €6.9 million in the prior year, with the operating profit margin declining to 7.8% from 8.9%. For H1 2025, operating profit increased significantly to €13.2 million from €10.0 million, improving the margin to 7.5% from 7.1%.

Basic earnings per share remained flat at €0.21 for Q2 2025, while H1 2025 EPS improved to €0.40 from €0.31 in the comparable period.

Segment Performance

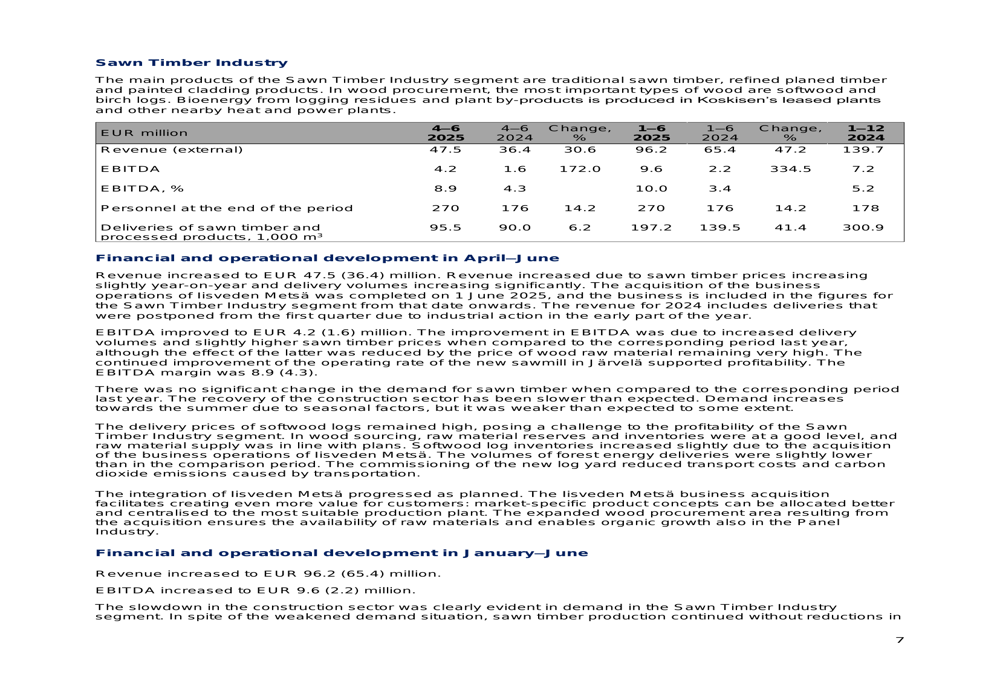

The Sawn Timber Industry segment delivered exceptional results, as illustrated in the following segment breakdown:

External revenue for the Sawn Timber segment increased by 30.6% to €47.5 million in Q2 2025, while EBITDA surged by 172.0% to €4.2 million. The segment’s EBITDA margin improved significantly to 8.9% from 4.3% in Q2 2024. For H1 2025, the segment’s external revenue grew by 47.2% to €96.2 million, with EBITDA increasing by 334.5% to €9.6 million.

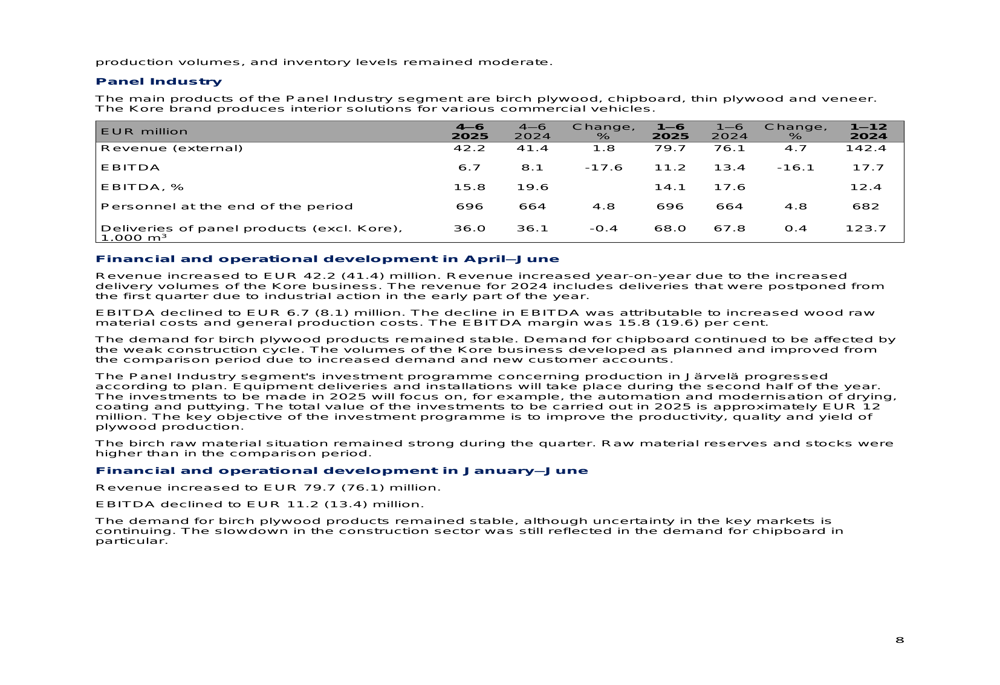

In contrast, the Panel Industry segment showed more modest growth with some profitability challenges, as shown in this detailed breakdown:

The Panel Industry segment’s external revenue increased by just 1.8% to €42.2 million in Q2 2025, while EBITDA decreased by 17.6% to €6.7 million. The segment’s EBITDA margin declined to 15.8% from 19.6% in Q2 2024. For H1 2025, external revenue grew by 4.7% to €79.7 million, but EBITDA decreased by 16.1% to €11.2 million.

CEO Pahta attributed the decline in Panel Industry profitability to higher wood raw material and production costs, while noting that the segment’s investment program in Järvelä is progressing according to plan.

Strategic Initiatives

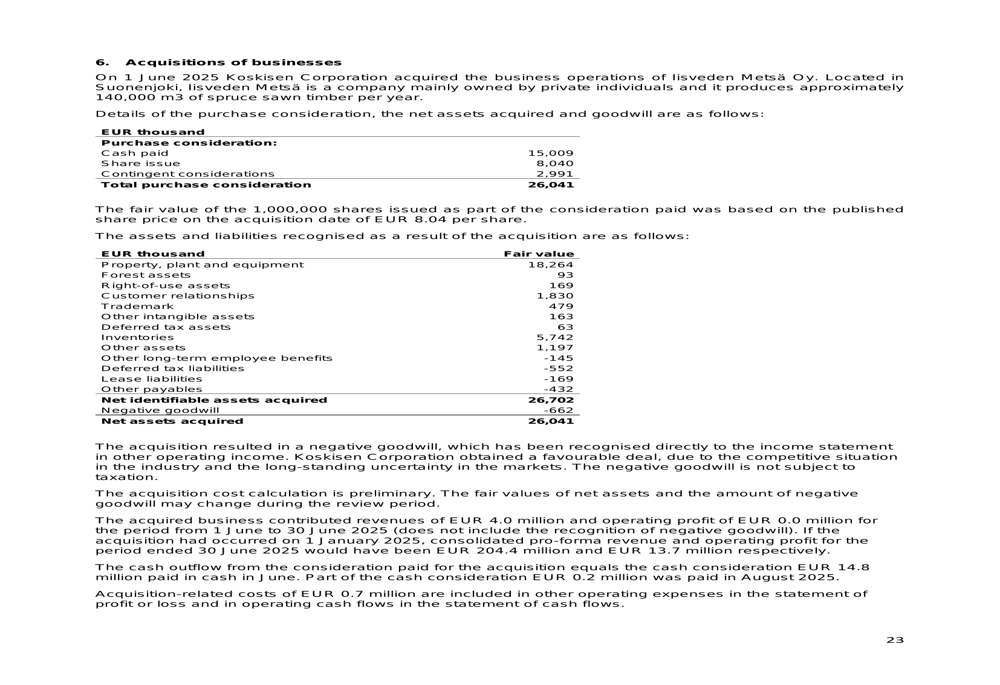

A significant milestone during the quarter was the completion of the Lisveden Metsä acquisition on June 1, 2025. The following details highlight the financial aspects of this strategic acquisition:

The acquisition, valued at €26.0 million, strengthens Koskisen’s position in the sawn timber market. The purchase consideration included property, plant and equipment valued at €18.3 million and inventories worth €5.7 million. The company reported that the integration of Lisveden Metsä is progressing according to plan.

Koskisen also continues to invest in sustainable operations, with construction work started on a district heating connection pipe between production plants in Järvelä. The company’s investment program in the Panel Industry segment is also advancing as planned.

Financial Position & Cash Flow

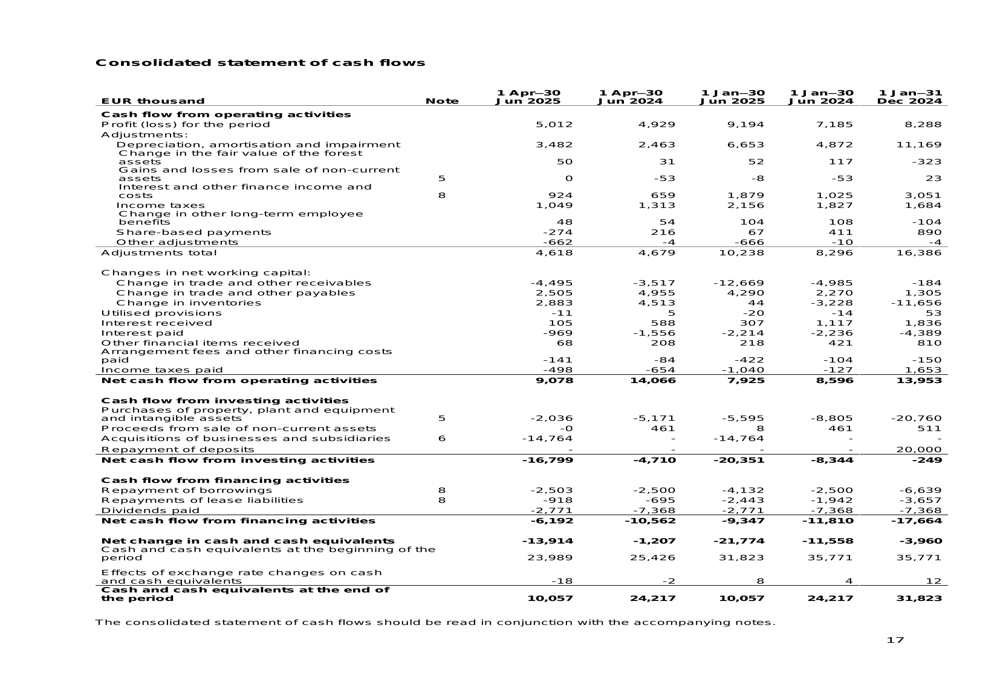

The company’s financial position remains solid despite increased investments and the recent acquisition. The consolidated statement of cash flows reveals important trends in the company’s financial activities:

Net cash flow from operating activities decreased slightly to €7.9 million in H1 2025 from €8.6 million in H1 2024. Cash flow from investing activities increased significantly to -€20.4 million from -€8.3 million, reflecting the company’s acquisition and investment activities. Cash flow from financing activities was -€9.3 million compared to -€11.8 million in H1 2024.

The equity ratio strengthened to 55.6% from 53.3% in the comparable period, while gearing increased to 23.7% from 8.8%, primarily due to the acquisition and investments. Interest-bearing net liabilities increased to €38.8 million from €13.0 million in H1 2024.

Forward-Looking Statements

Koskisen maintained its profit guidance for 2025, expecting revenue to grow and the adjusted EBITDA margin to be between 7-11%. The company has set ambitious strategic goals to be achieved by the end of 2027, including:

- Revenue target of €500 million, including both organic and inorganic growth

- Adjusted EBITDA margin averaging 15% over the cycle

- Maintaining a strong balance sheet

- Attractive dividend policy of at least one-third of net profit each year

The company expects global demand for softwood sawn timber to grow by an average of 1.9% per year, while demand in the birch plywood market is projected to grow globally by 2.3% per year.

CEO Pahta emphasized that despite the unstable operating environment, the company is well-positioned to continue its growth trajectory, particularly with the improved performance of the Sawn Timber Industry segment and the strategic acquisition of Lisveden Metsä.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.