Gold bars to be exempt from tariffs, White House clarifies

Introduction & Market Context

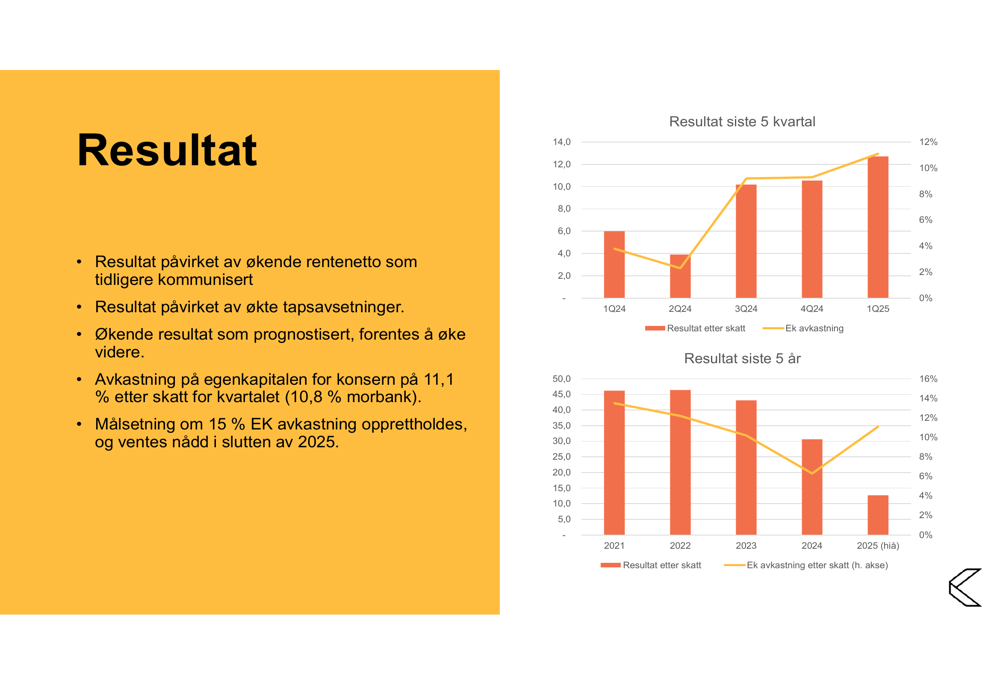

Kraft Bank ASA (OB:KRAB) presented its first quarter 2025 results on May 12, showcasing a remarkable 203% increase in profit after tax compared to the same period last year. The Norwegian specialized mortgage bank, which focuses on helping customers with financial difficulties, reported a profit of 12.7 million Norwegian kroner (MNOK), up from 4.2 MNOK in Q1 2024.

The bank’s business model centers on providing refinancing solutions to individuals facing economic challenges, with the goal of eventually transitioning them back to regular banking relationships. This approach has proven increasingly effective as Norway’s high cost of living continues to impact household finances.

Business Model & Social Impact

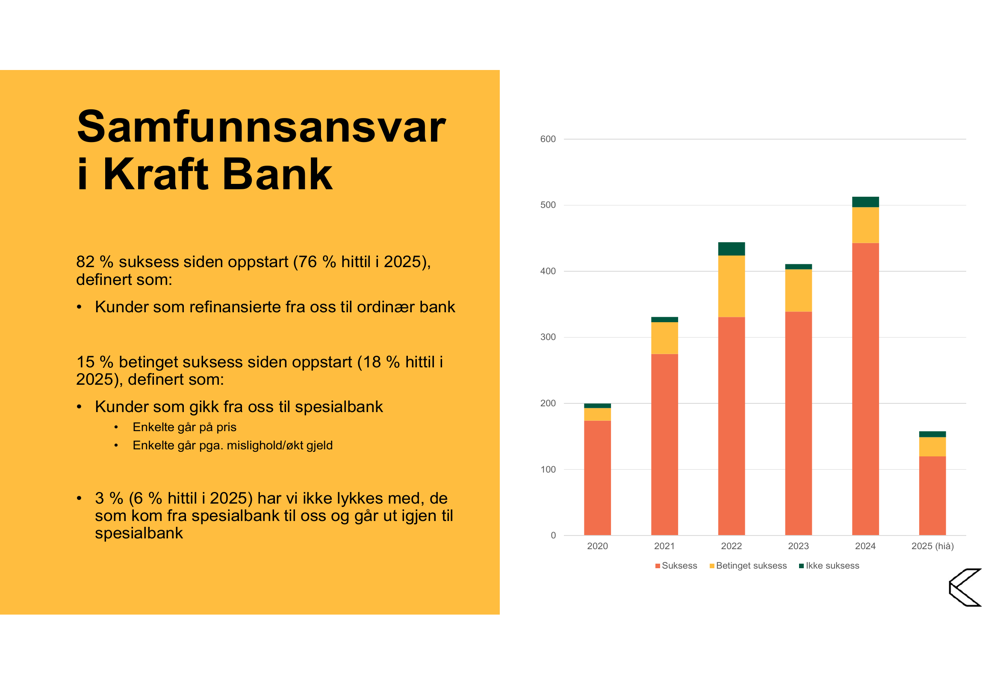

Kraft Bank’s core mission revolves around helping customers overcome financial difficulties through responsible refinancing. Since its inception in 2018, the bank has successfully "cleared" 2,093 customers, including 162 in the most recent quarter. The bank defines success as customers who refinance from Kraft Bank to a regular bank, which has occurred at an 82% rate since the company’s founding.

As shown in the following chart of customer success rates:

The bank maintains a strong social responsibility focus, noting that when it helps customers avoid forced home sales, "a family keeps their home and gets the chance to start over." This approach benefits both individuals and local communities, according to the presentation.

Quarterly Performance Highlights

Kraft Bank reported significant financial improvements in Q1 2025:

- Profit after tax reached 12.7 MNOK (vs. 4.2 MNOK in Q1 2024)

- Return on equity after tax improved to 11.1% (vs. 3.8% in Q1 2024)

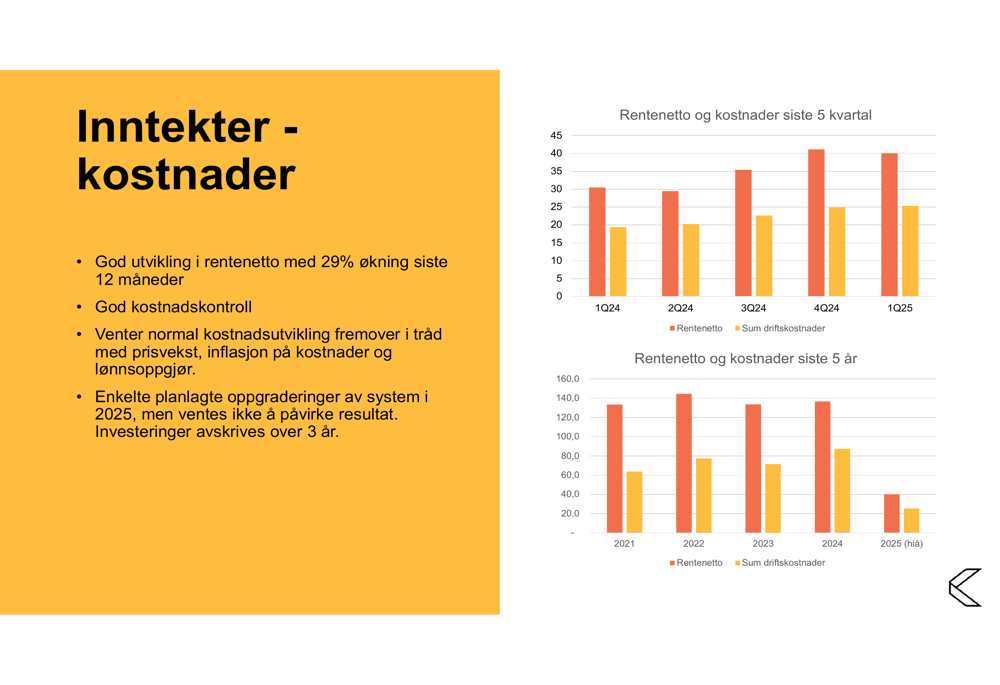

- Net interest income grew 29% year-over-year

- Book equity per share stood at 11.19 kroner at quarter-end

- Dividend for 2024 was paid on April 14, 2025

The bank’s subsidiary, Varde Finans, is now operating with positive results, contributing to the overall performance improvement. The following chart illustrates the steady improvement in financial results:

Detailed Financial Analysis

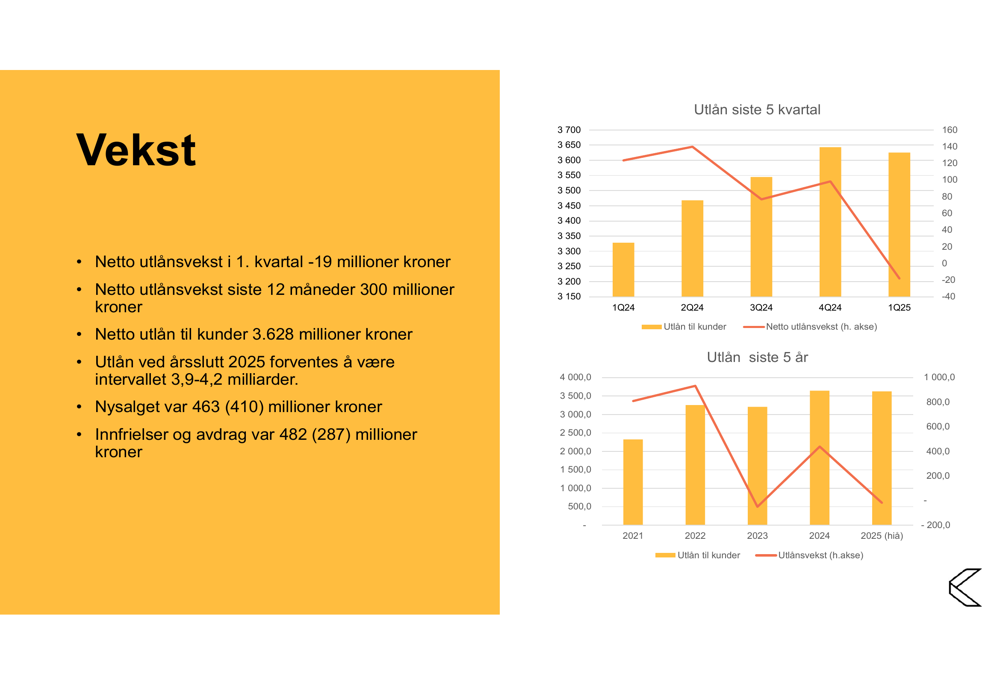

Kraft Bank’s loan portfolio remained relatively stable in Q1, with net loans to customers at 3,628 million kroner. The bank reported a slight contraction in net lending during the quarter (-19 million kroner) but maintained 300 million kroner growth over the trailing twelve months.

New sales reached 463 million kroner (compared to 410 million previously), while redemptions and installments totaled 482 million kroner (up from 287 million). The bank expects total loans at year-end 2025 to reach between 3.9-4.2 billion kroner.

The following chart details the bank’s loan growth trends:

Cost control remains a priority, with the bank expecting normal cost development going forward in line with inflation and wage settlements. Some planned system upgrades are scheduled for 2025 but are not expected to materially impact results as investments will be depreciated over three years.

Net interest income and cost trends are illustrated in this chart:

Loan Portfolio & Credit Quality

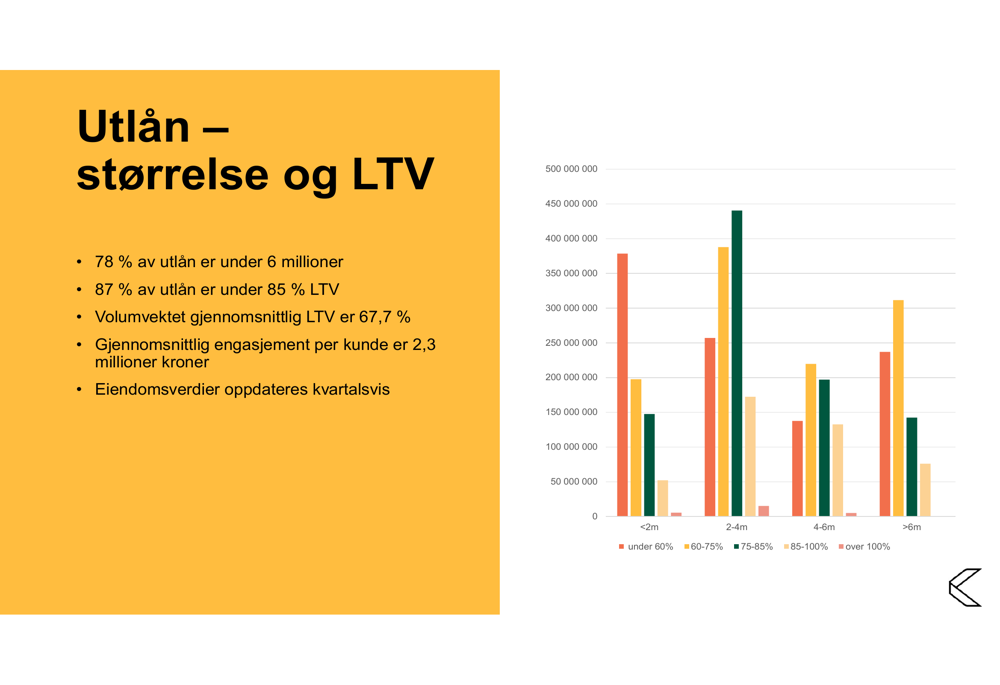

Kraft Bank maintains a well-secured loan portfolio with 99.2% of loan volume secured by property mortgages. The volume-weighted average loan-to-value (LTV) ratio stands at 67.7%, with 87% of loans having an LTV under 85%.

The portfolio is diversified with an average commitment per customer of 2.3 million kroner, and 78% of loans are under 6 million kroner. The bank updates property values quarterly to maintain accurate risk assessments.

The distribution of loans by size and LTV is shown in the following chart:

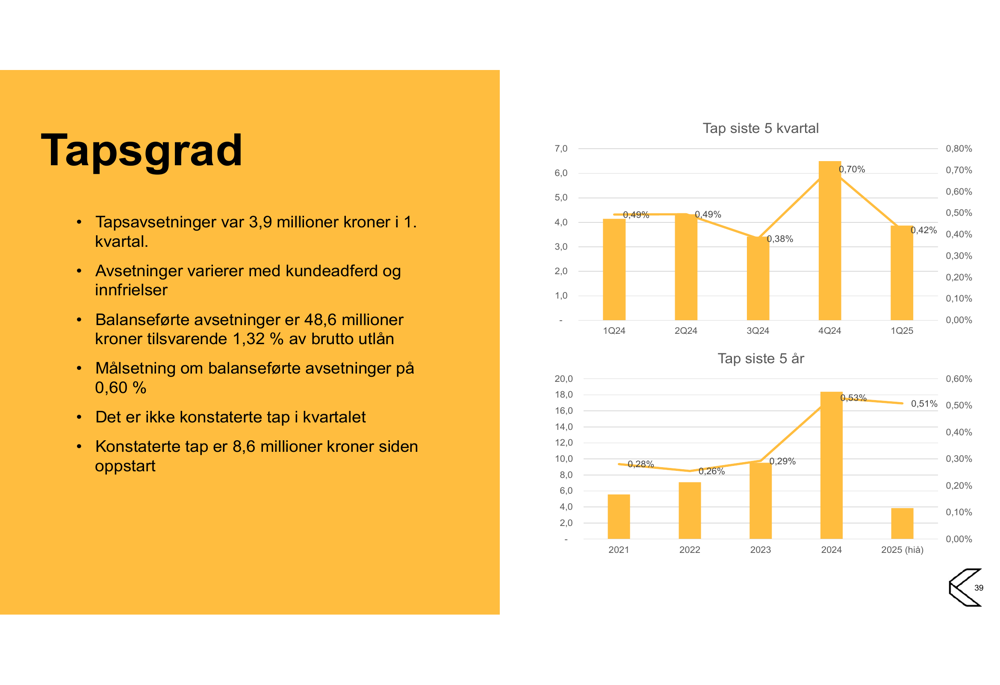

Loss provisions were 3.9 million kroner in Q1, with balance sheet provisions totaling 48.6 million kroner, equivalent to 1.32% of gross loans. The bank aims to eventually reduce provisions to 0.60% of gross loans. Since inception, Kraft Bank has recognized only 8.6 million kroner in confirmed losses against 9.3 billion kroner in total lending.

The impairment ratio trend is illustrated here:

Capital Position & Outlook

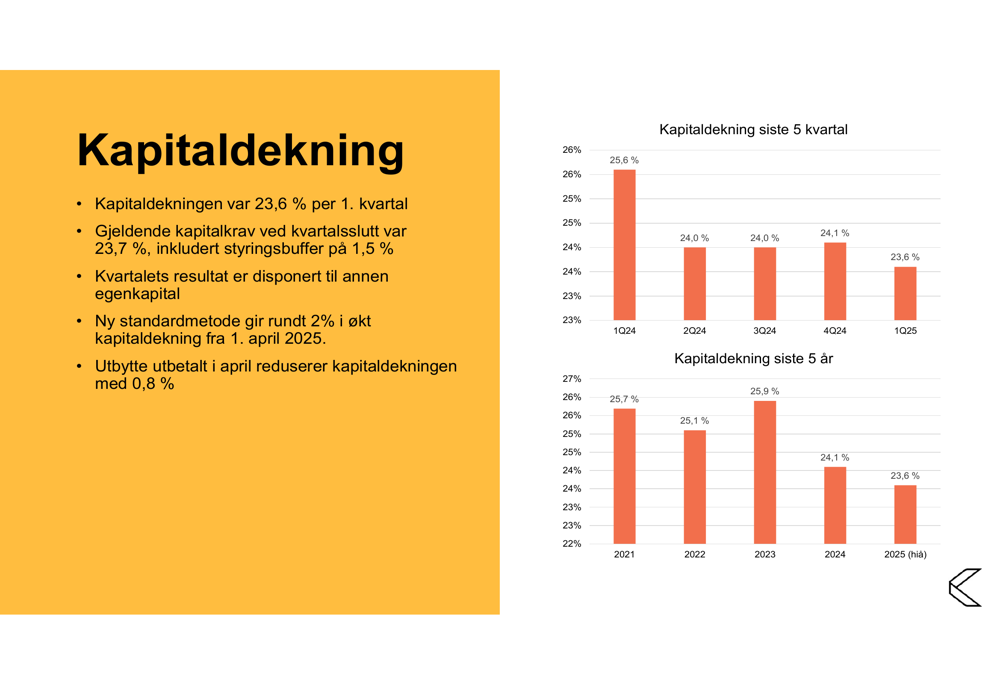

Kraft Bank reported a capital coverage ratio of 23.6% at the end of Q1 2025, slightly below its management target of 23.7% (which includes a 1.5% buffer). The bank expects a boost of approximately 2% to its capital coverage from April 1, 2025, due to the implementation of a new standard method.

The bank’s capital position over time is shown in this chart:

Looking ahead, Kraft Bank maintains its target of achieving a 15% return on equity by the end of 2025, up from the current 11.1%. The bank expects continued improvement in earnings as loans with interest rate guarantees gradually roll out of its books.

Management anticipates steady increasing earnings throughout 2025, with loan growth expected to bring the total portfolio to between 3.9-4.2 billion kroner by year-end. The bank’s capital plan includes issuing fund bonds, revising interim results, retaining surplus, reducing growth if necessary, and potentially raising additional equity.

As Norway’s economic conditions continue to create challenges for households, Kraft Bank’s specialized refinancing model appears well-positioned to serve its target market while delivering improving financial results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.