Procore stock price target raised to $90 from Goldman Sachs on stabilizing growth

Introduction & Market Context

Kraft Heinz Co (NASDAQ:KHC) presented its third-quarter 2025 business update on October 29, revealing signs of modest recovery in volume trends despite continued year-over-year declines in sales and profitability. The food giant’s stock dropped 4.6% to $24.34 following the presentation, approaching its 52-week low of $24.19, as investors reacted to mixed results.

The company reported an adjusted EPS of $0.61, which beat analyst expectations of $0.58, but still represented an 18.7% decline from the previous year. Revenue came in at $6.24 billion, slightly below the anticipated $6.26 billion, with organic net sales declining 2.5% year-over-year.

Quarterly Performance Highlights

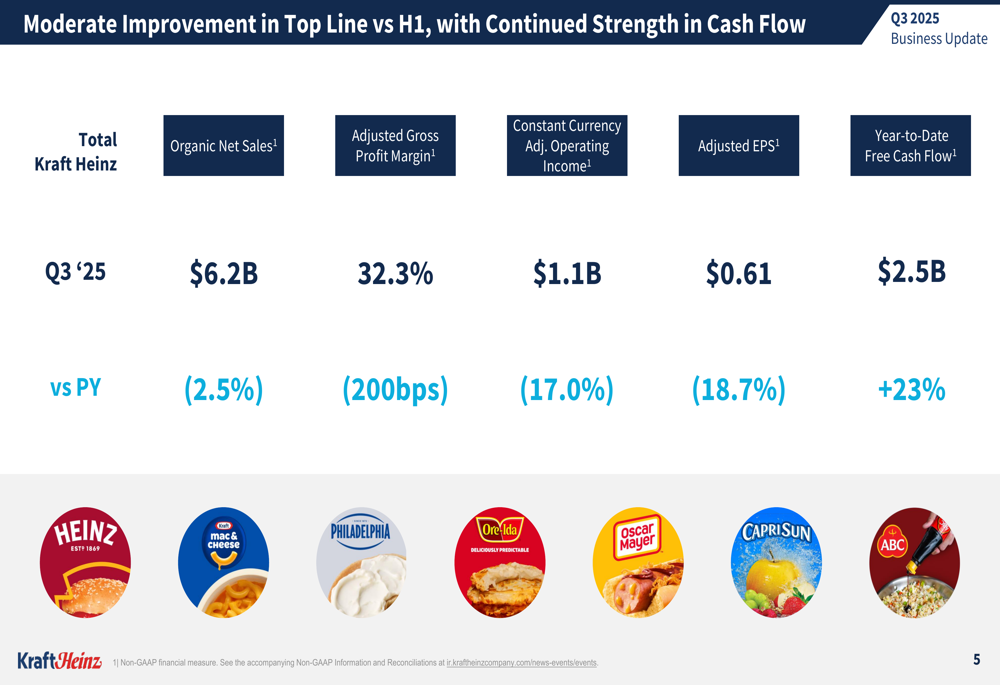

Kraft Heinz’s Q3 2025 results showed a mixed financial picture with continued pressure on top-line metrics but improving volume trends compared to the first half of the year.

As shown in the following financial summary from the presentation:

The company reported organic net sales of $6.2 billion, representing a 2.5% decline versus the prior year. Adjusted gross profit margin contracted by 200 basis points to 32.3%, while constant currency adjusted operating income fell 17.0% to $1.1 billion. Adjusted EPS declined 18.7% to $0.61.

A bright spot in the results was the company’s year-to-date free cash flow, which increased 23% to $2.5 billion, demonstrating Kraft Heinz’s ability to generate cash despite operational challenges.

Volume Trends & Category Performance

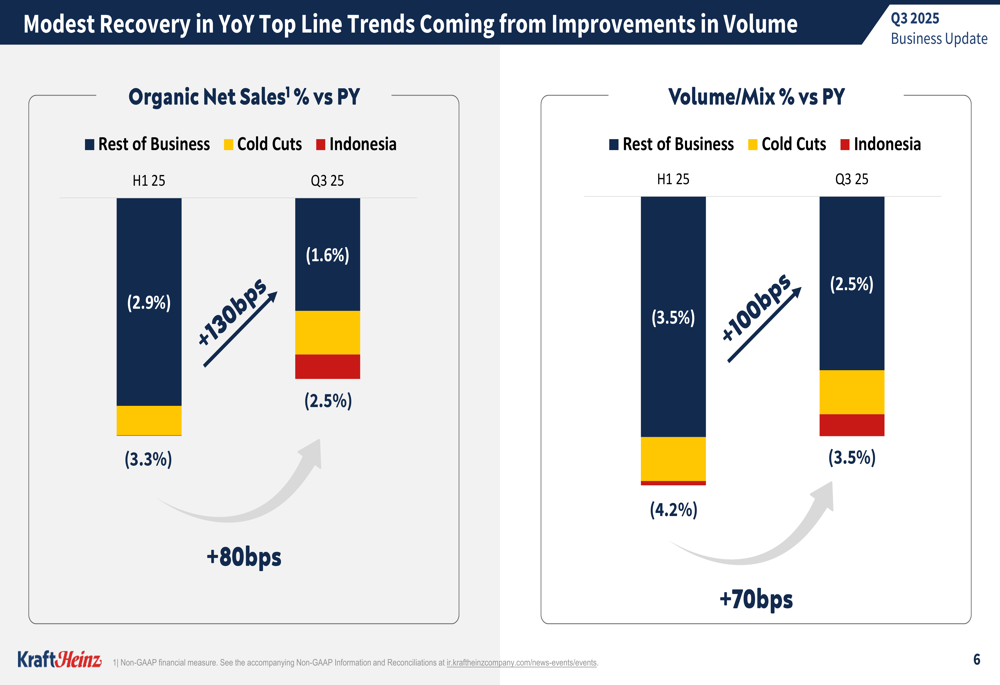

The presentation highlighted improving volume trends in Q3 compared to the first half of 2025, suggesting early signs of recovery in consumer demand.

As illustrated in the following chart showing volume improvement:

Volume/mix trends showed sequential improvement, with the rest of the business (excluding cold cuts) improving from -3.5% in H1 to -2.5% in Q3. Similarly, the cold cuts segment improved from -4.2% to -3.5%. While still negative, these trends indicate a modest recovery in volume performance.

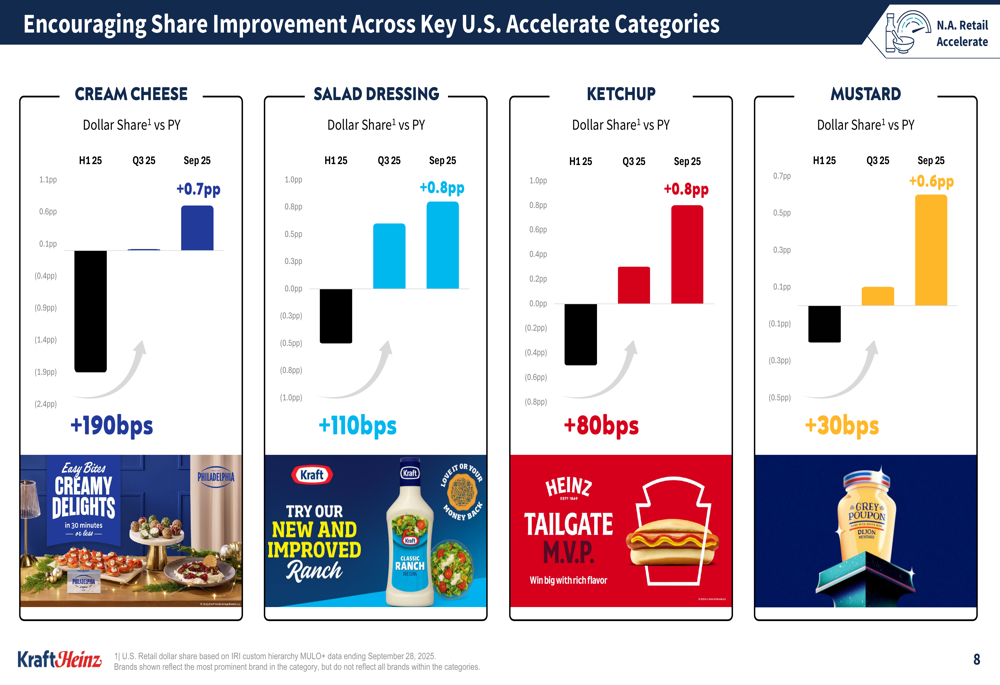

Kraft Heinz also reported encouraging market share gains across key U.S. categories, providing evidence that its brand investments are yielding results despite overall market challenges.

The following slide showcases these market share improvements:

The company gained market share in cream cheese (+0.7 percentage points), salad dressing (+0.8 percentage points), ketchup (+0.8 percentage points), and mustard (+0.6 percentage points), demonstrating strength in its core condiment and dairy categories.

Segment Performance Analysis

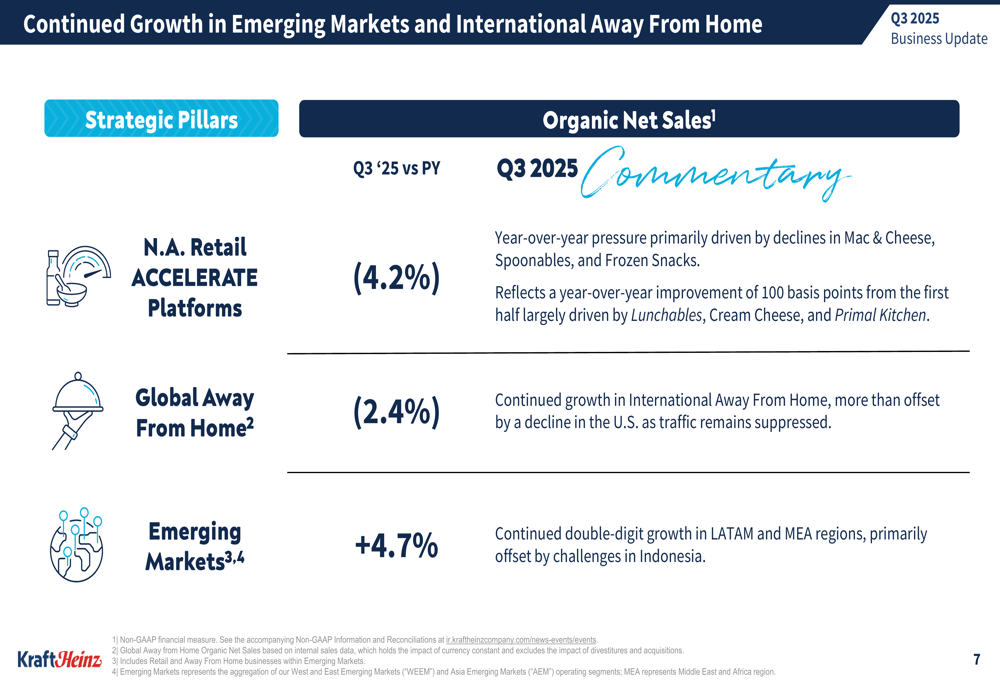

Kraft Heinz’s presentation revealed significant performance variations across its business segments, with emerging markets showing strength while North American retail faced continued pressure.

As shown in this segment breakdown:

Emerging markets delivered 4.7% growth compared to the prior year, driven by "continued double-digit growth in LATAM and MEA regions," though partially offset by challenges in Indonesia. Global Away From Home declined 2.4%, with growth in international markets more than offset by U.S. weakness where "traffic remains suppressed."

North American Retail ACCELERATE Platforms experienced a 4.2% decline, though this represented a 100 basis point improvement from the first half, primarily driven by better performance in Lunchables, Cream Cheese, and Primal Kitchen brands.

Strategic Initiatives

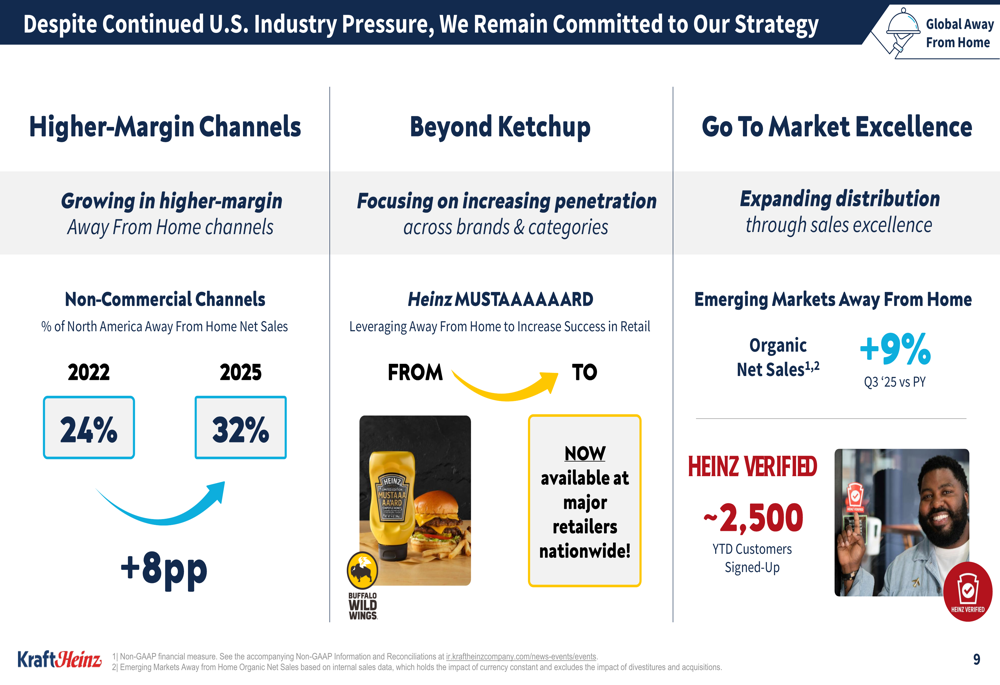

Despite ongoing industry pressures, Kraft Heinz emphasized its commitment to strategic investments and channel expansion initiatives.

The company’s strategy focuses on three key areas as outlined in the presentation:

Kraft Heinz is prioritizing growth in higher-margin channels, particularly in non-commercial Away From Home segments, which have increased from 24% of North American Away From Home net sales in 2022 to 32% in 2025. The company is also expanding beyond its core ketchup business with products like Heinz Mustard, while leveraging its Away From Home success to drive retail performance.

Additionally, the presentation highlighted the company’s distribution expansion through sales excellence, noting 9% organic net sales growth in emerging markets’ away-from-home segment.

Forward-Looking Statements

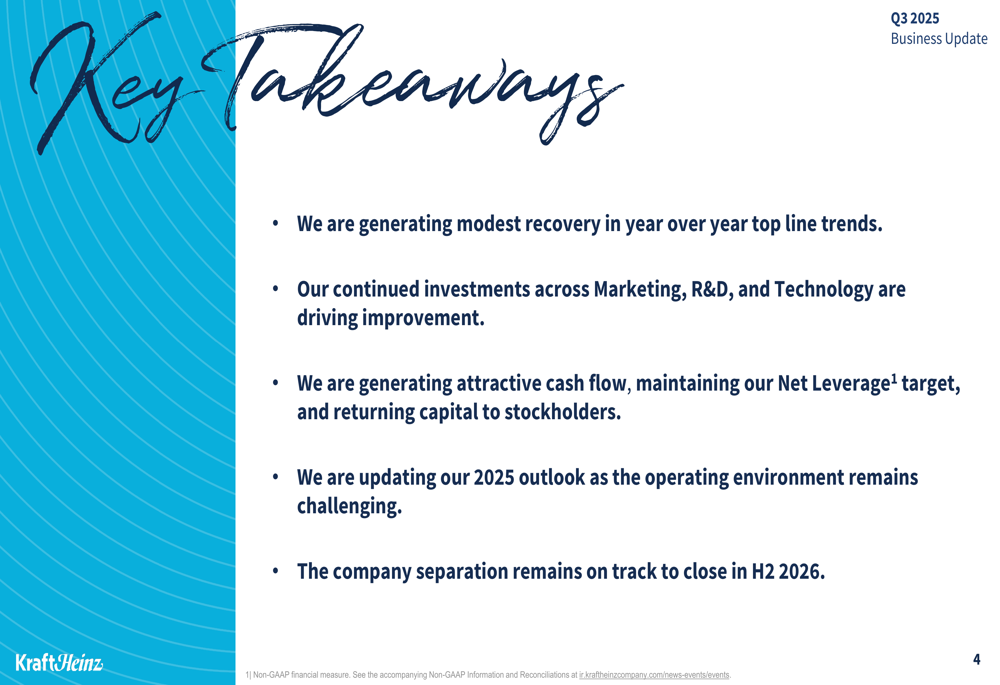

The presentation outlined several key forward-looking elements, including the company’s updated 2025 outlook and progress toward its planned separation.

As summarized in the key takeaways slide:

Kraft Heinz is maintaining its net leverage target while updating its 2025 outlook. According to the earnings report, the company now projects adjusted EPS in the range of $2.50 to $2.57 for the full year, with expectations of a 3% to 3.5% decline in organic net sales.

The company also confirmed that its previously announced separation plan remains on track to close in the second half of 2026, representing a significant upcoming structural change for the business.

CEO Carlos Abrams-Rivera emphasized the company’s commitment to continued investments in Marketing, R&D, and Technology, stating in the earnings call that these investments are "fueling the recovery" in the business.

While Kraft Heinz faces persistent challenges in its core North American business, the presentation highlighted the company’s focus on cash generation, market share improvements in key categories, and strategic investments aimed at positioning the business for future growth as it prepares for its planned separation in 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.