Cardiff Oncology shares plunge after Q2 earnings miss

Introduction & Market Context

Krystal Biotech Inc. (NASDAQ:KRYS) shares tumbled 12.36% to $142.23 on May 6, 2025, after the company’s first-quarter earnings release missed analyst expectations. The gene therapy developer reported diluted earnings per share of $1.20, falling short of the forecasted $1.46, while revenue of $88.2 million missed the anticipated $99.12 million. Despite these misses, the company’s corporate presentation highlighted significant year-over-year growth and global expansion plans for its flagship product VYJUVEK.

Quarterly Performance Highlights

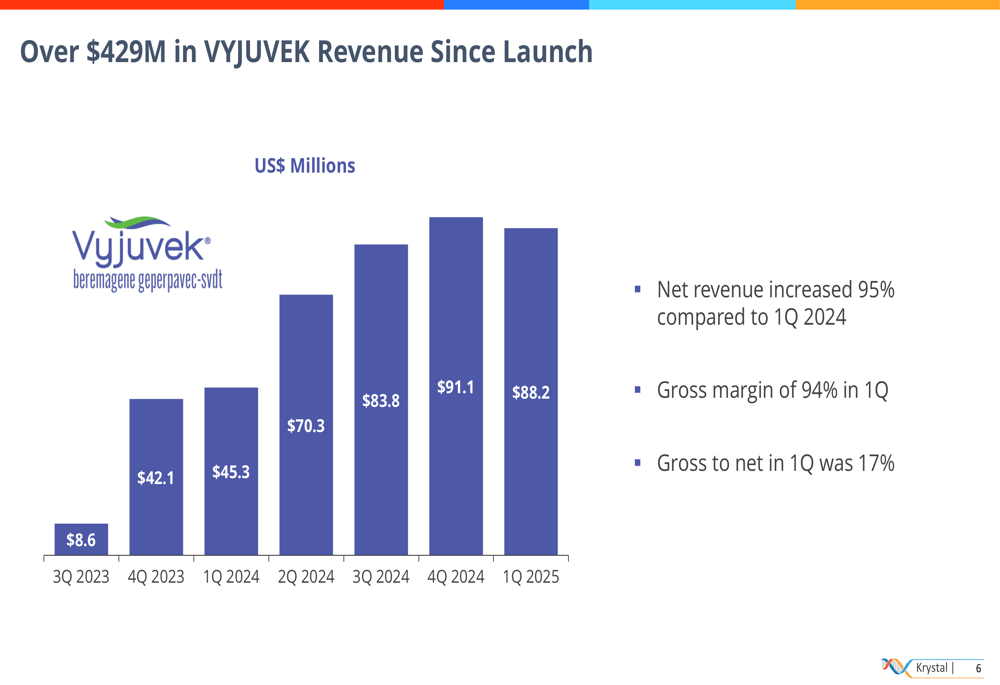

Krystal Biotech reported net product revenue of $88.2 million for VYJUVEK in Q1 2025, representing a 95% increase compared to Q1 2024, but a sequential decline from $91.1 million in Q4 2024. The company maintained a strong gross margin of 94% in the first quarter, with gross-to-net at 17%.

As shown in the following chart of quarterly revenue growth:

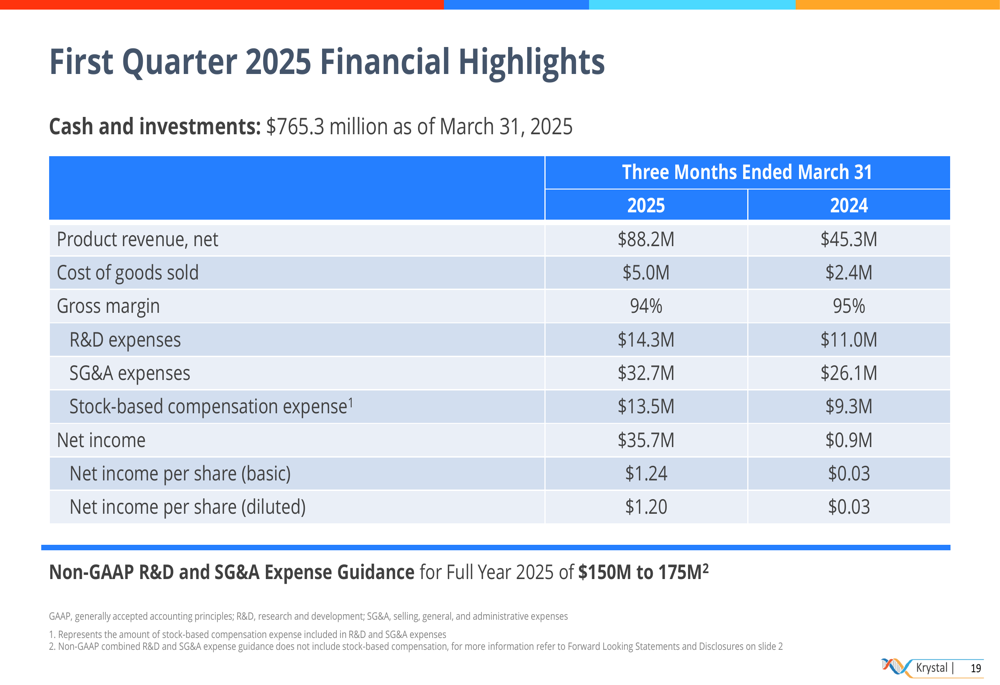

The financial results revealed net income of $35.7 million, translating to $1.24 per basic share and $1.20 per diluted share. R&D expenses reached $14.3 million, while SG&A expenses totaled $32.7 million, including $13.5 million in stock-based compensation.

The company’s detailed financial performance is illustrated in this summary:

Global Expansion Strategy

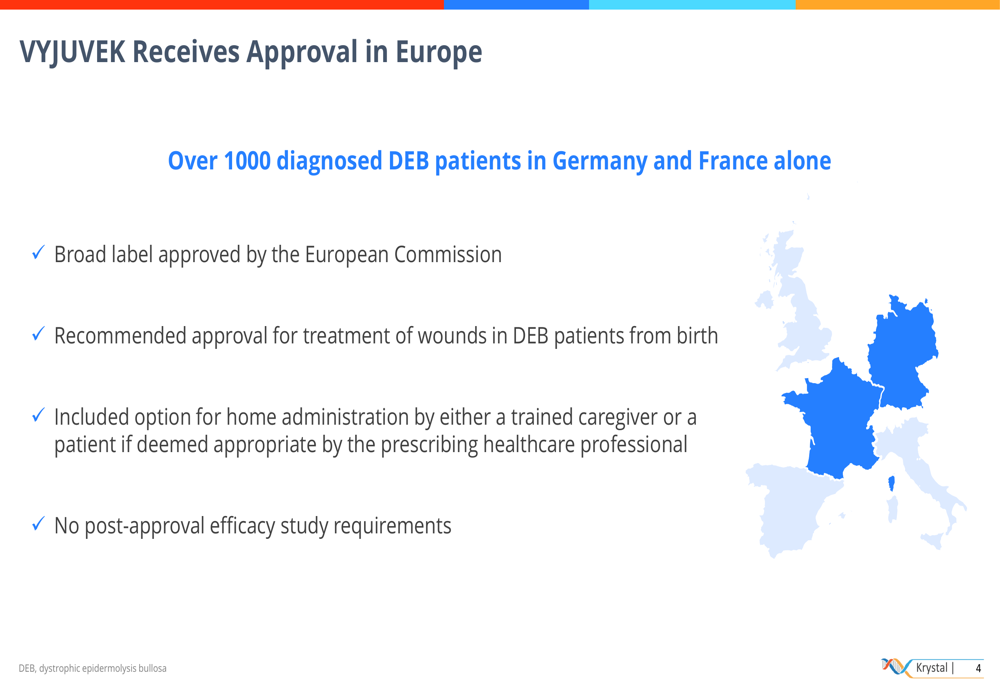

A key focus of Krystal’s presentation was its global expansion strategy for VYJUVEK. The company recently received European Commission approval with a broad label for treating dystrophic epidermolysis bullosa (DEB) patients from birth, including an option for home administration.

The European approval represents a significant market opportunity, as illustrated in this slide:

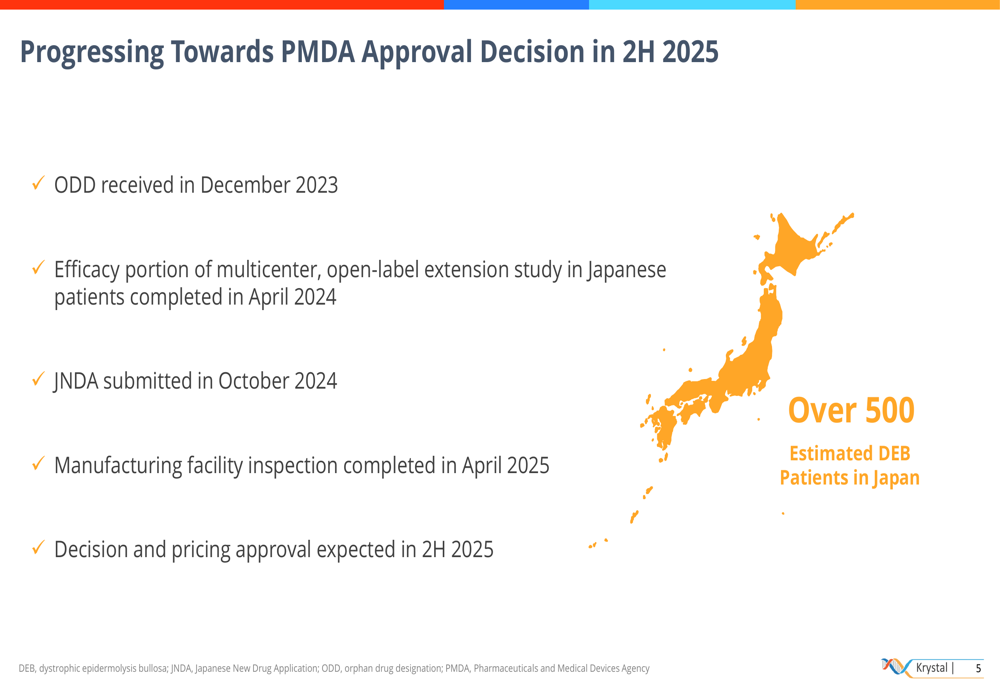

In Japan, Krystal is progressing toward a potential approval decision in the second half of 2025. The company completed the efficacy portion of its Japanese patient study in April 2024, submitted its application in October 2024, and completed a manufacturing facility inspection in April 2025.

The Japanese market represents another substantial opportunity with over 500 estimated DEB patients:

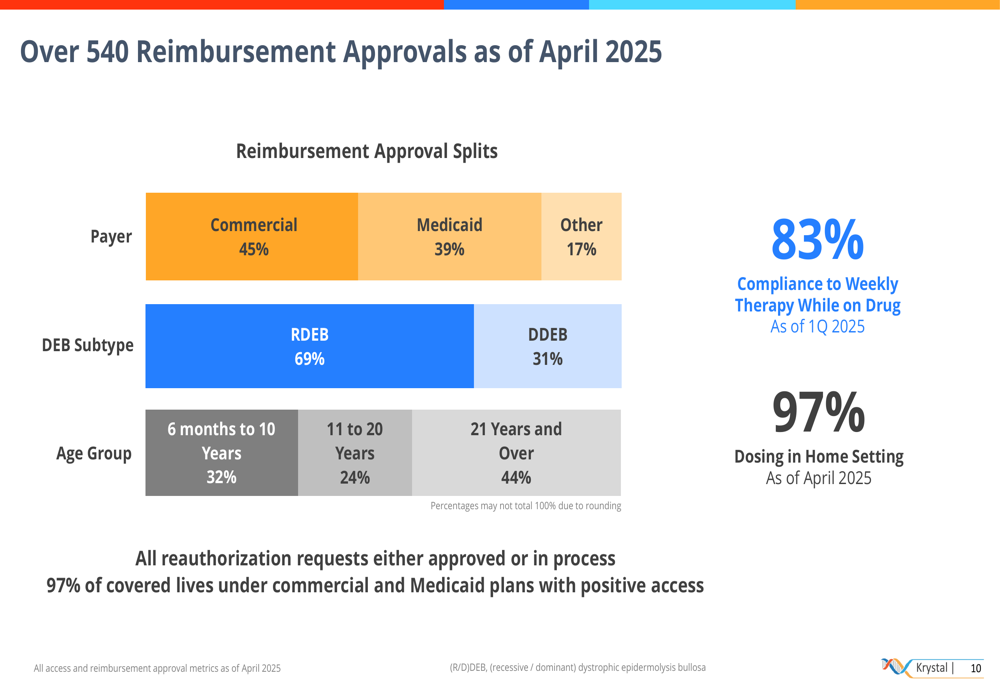

Patient Access and Reimbursement

Krystal’s presentation highlighted strong patient access metrics in the U.S. market. The company reported that 97% of covered lives under commercial and Medicaid plans have positive access to VYJUVEK. Additionally, 83% of patients are compliant with weekly therapy, and 97% of dosing occurs in the home setting as of April 2025.

The patient demographics and reimbursement breakdown are detailed in this slide:

The company emphasized that all reauthorization requests have been either approved or are in process, suggesting strong ongoing insurance coverage for patients.

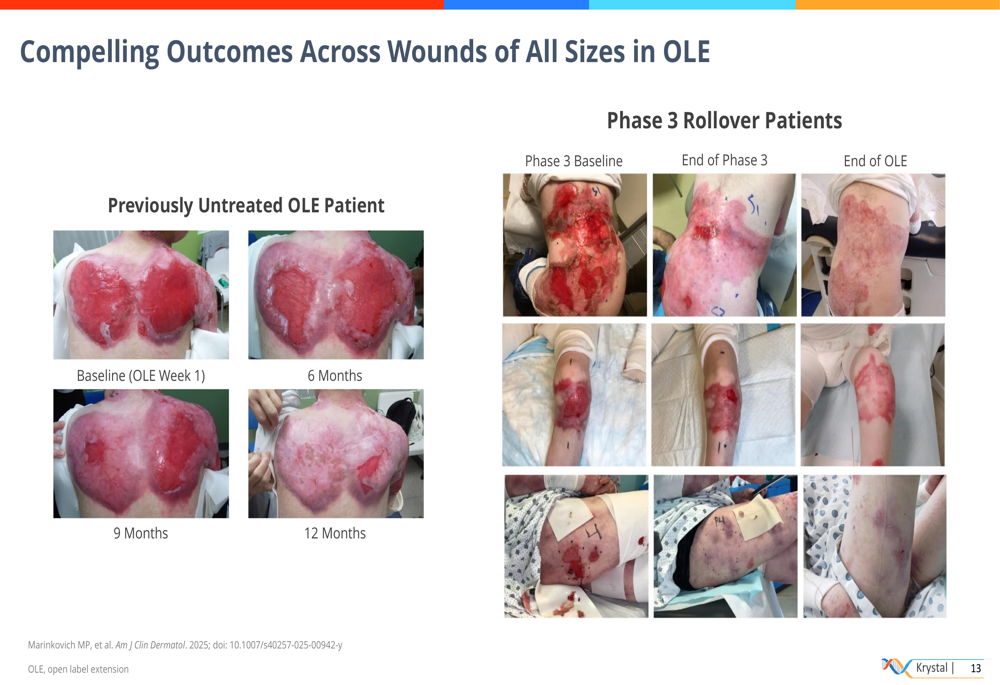

Clinical Efficacy and Pipeline Updates

Krystal showcased compelling clinical outcomes from its open-label extension study, demonstrating VYJUVEK’s efficacy across wounds of various sizes:

Looking ahead to the remainder of 2025, the company highlighted four expected clinical readouts:

1. KB407 for cystic fibrosis (mid-summer)

2. KB408 for alpha-1 antitrypsin deficiency lung disease (2H 2025)

3. KB304 for aesthetic skin conditions (2H 2025)

4. KB803 for ocular DEB lesions (2H 2025)

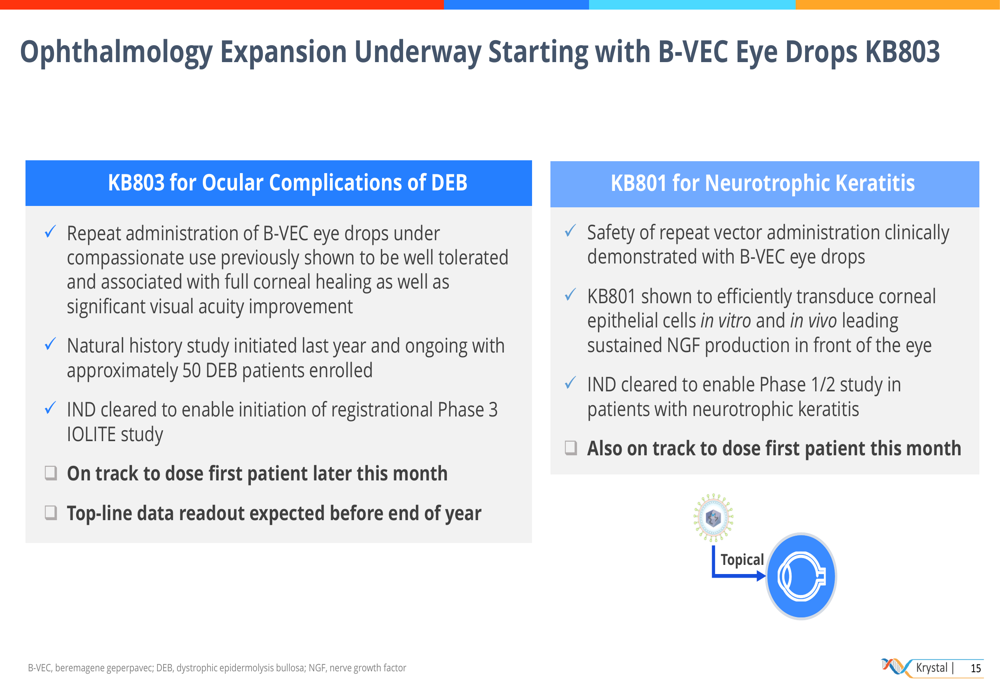

Ophthalmology Expansion

A significant portion of the presentation focused on Krystal’s expansion into ophthalmology with two advancing programs:

The KB803 program (B-VEC eye drops) has shown promising results under compassionate use, with patients experiencing full corneal healing and significant visual acuity improvement. The company has initiated a registrational Phase 3 study with top-line data expected before year-end.

The KB801 program for neurotrophic keratitis (NK) represents Krystal’s second ophthalmology indication. The company designed KB801 to drive sustained, local nerve growth factor expression to maximize efficacy while minimizing dosing frequency compared to the current standard of care, which requires six daily doses for eight weeks.

Forward-Looking Statements

Despite the Q1 earnings miss, Krystal maintained its non-GAAP R&D and SG&A expense guidance for full-year 2025 at $150-175 million. The company emphasized its financial stability as a key strength, noting seven consecutive quarters of profitable EPS since VYJUVEK’s launch.

The company’s 2025 outlook focuses on three key value drivers:

1. European launch to bolster the VYJUVEK franchise

2. Four clinical readouts across its pipeline

3. Financial stability providing optionality to maximize shareholder value

Analyst Perspectives

While the Q1 results fell short of expectations, analysts remain generally positive on Krystal’s long-term prospects. According to available data, the consensus suggests a potential upside of approximately 32% from current levels, despite the stock trading near its 52-week low of $137.01.

The earnings miss and subsequent stock decline highlight the challenges Krystal faces in meeting heightened market expectations as it transitions from early commercial success to sustained global growth. Investors will likely focus on the upcoming European launch execution and pipeline readouts as key catalysts for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.