Asia tech stocks slide tracking Wall St losses amid AI doubts, govt. uncertainty

Introduction & Market Context

Kuehne + Nagel International AG (SWX:KNIN) presented its half-year 2025 results on July 24, revealing a mixed performance characterized by strong market share gains in key segments but declining profitability due to significant currency headwinds. The logistics giant has revised its full-year EBIT guidance downward, primarily reflecting these currency impacts rather than operational challenges.

The company’s results come amid increasing uncertainty in global trade, with particular volatility in sea freight markets and ongoing tensions affecting US-China trade relations. Despite these challenges, Kuehne + Nagel demonstrated resilience in maintaining volumes and stabilizing yields in its core Sea and Air Logistics segments.

Financial Performance Highlights

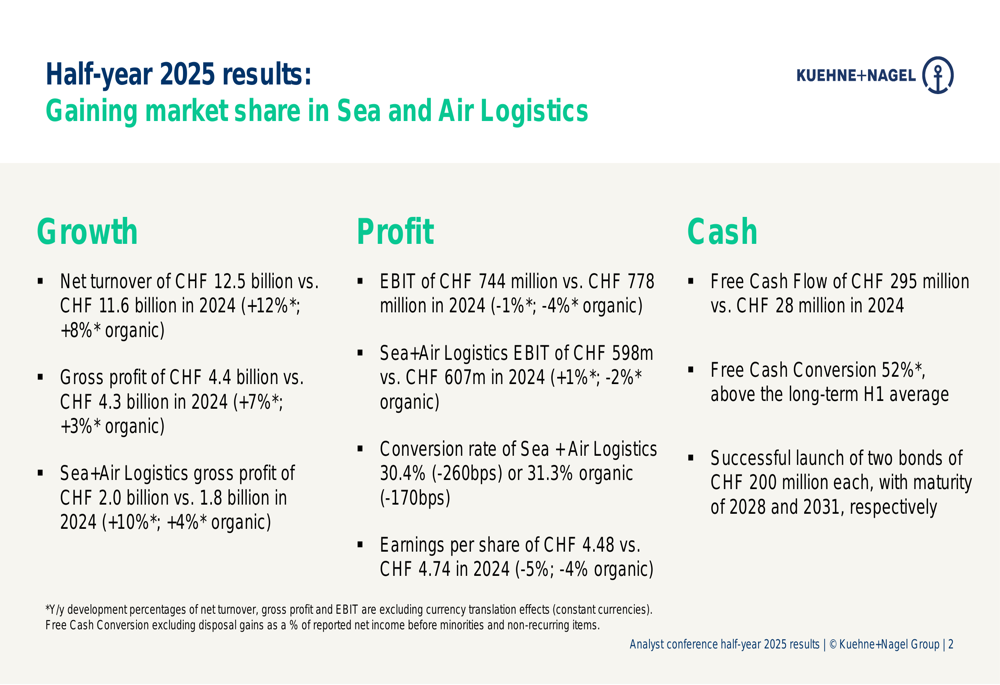

For the first half of 2025, Kuehne + Nagel reported net turnover of CHF 12.5 billion, representing a 12% increase (8% organic) compared to the same period in 2024. Gross profit rose to CHF 4.4 billion, up 7% (3% organic), while EBIT declined slightly to CHF 744 million, down 1% (-4% organic) from the previous year.

As shown in the following comprehensive financial overview:

The company’s earnings per share decreased by 5% to CHF 4.48, reflecting the pressure on profitability. However, free cash flow showed remarkable improvement, reaching CHF 295 million compared to just CHF 28 million in the first half of 2024. This resulted in a free cash conversion rate of 52%, well above the long-term H1 average.

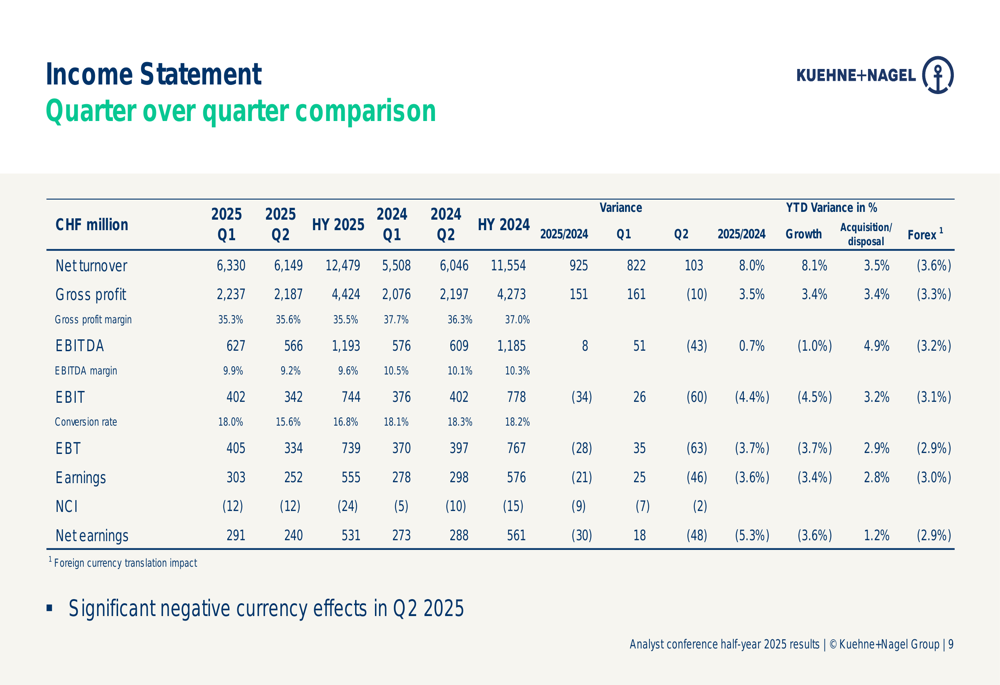

Quarter-over-quarter analysis reveals a significant slowdown in Q2 2025 compared to Q1, with net turnover declining from CHF 6,330 million to CHF 6,149 million and EBIT falling from CHF 402 million to CHF 342 million. This represents a 14.9% decline in EBIT compared to Q2 2024.

Segment Analysis

Sea Logistics

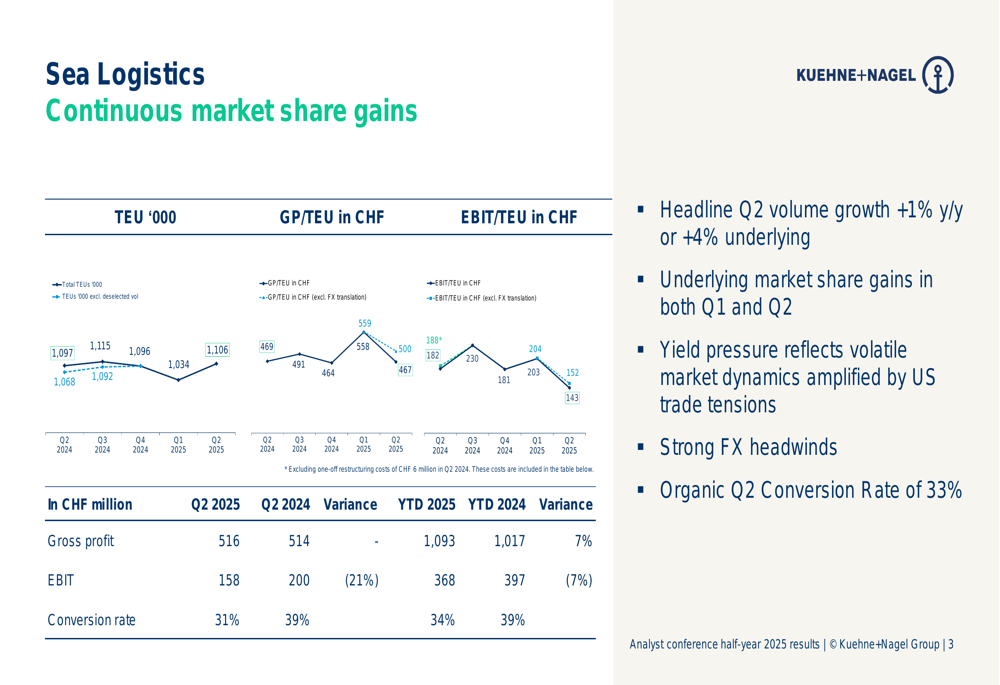

The Sea Logistics segment showed volume growth of 1% year-over-year in Q2 2025, or 4% excluding deselected volumes, indicating continued market share gains. However, EBIT declined by 21% to CHF 158 million, with the conversion rate dropping from 39% to 31%. This reflects significant yield pressure due to volatile market dynamics and strong FX headwinds.

The following chart illustrates the performance trends in Sea Logistics:

Air Logistics

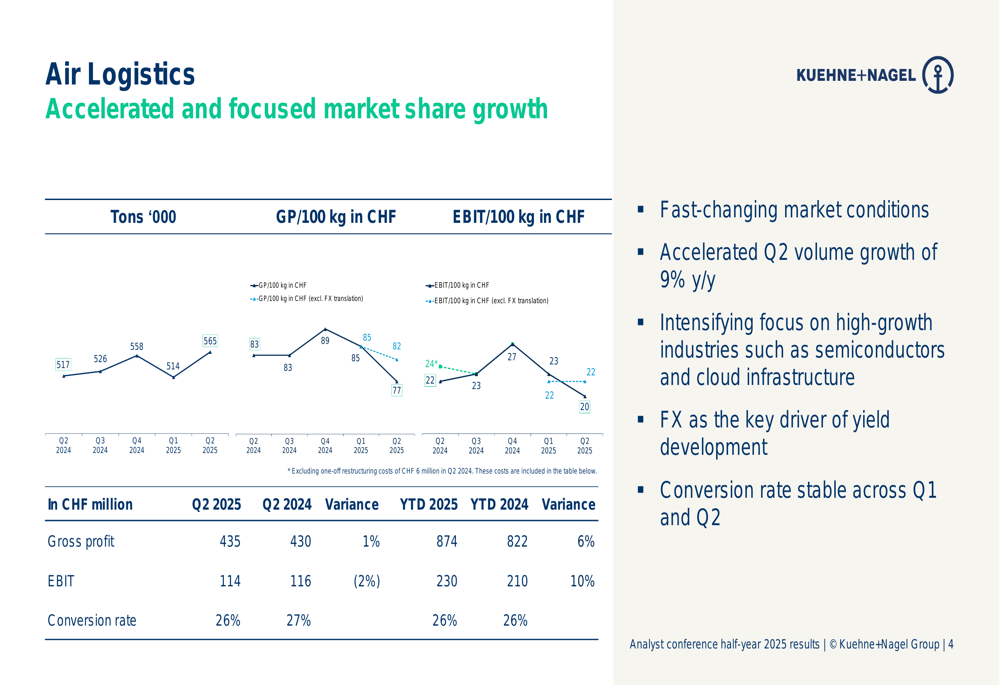

Air Logistics demonstrated stronger resilience, with accelerated volume growth of 9% year-over-year in Q2 2025. Gross profit increased slightly by 1% to CHF 435 million, while EBIT declined marginally by 2% to CHF 114 million. The conversion rate remained relatively stable at 26% compared to 27% in Q2 2024.

The company highlighted its intensifying focus on high-growth industries such as semiconductors and cloud infrastructure, as shown in the following performance metrics:

Road Logistics

Road Logistics faced significant challenges, with Q2 2025 EBIT declining by 22% to CHF 28 million compared to Q2 2024. Net turnover decreased by 3% to CHF 881 million, reflecting broad-based demand weakness across sectors and geographies. The segment did benefit from the first-time consolidation of TDN Group in Spain in June 2025.

Contract Logistics

Contract Logistics reported stable underlying performance, with net turnover and gross profit growth of 5% year-over-year in Q2 2025 excluding FX effects. However, reported EBIT declined by 16% to CHF 42 million, impacted by a one-off legal provision of CHF 16 million. Excluding this provision, underlying EBIT growth was 12% (17% excluding FX effects).

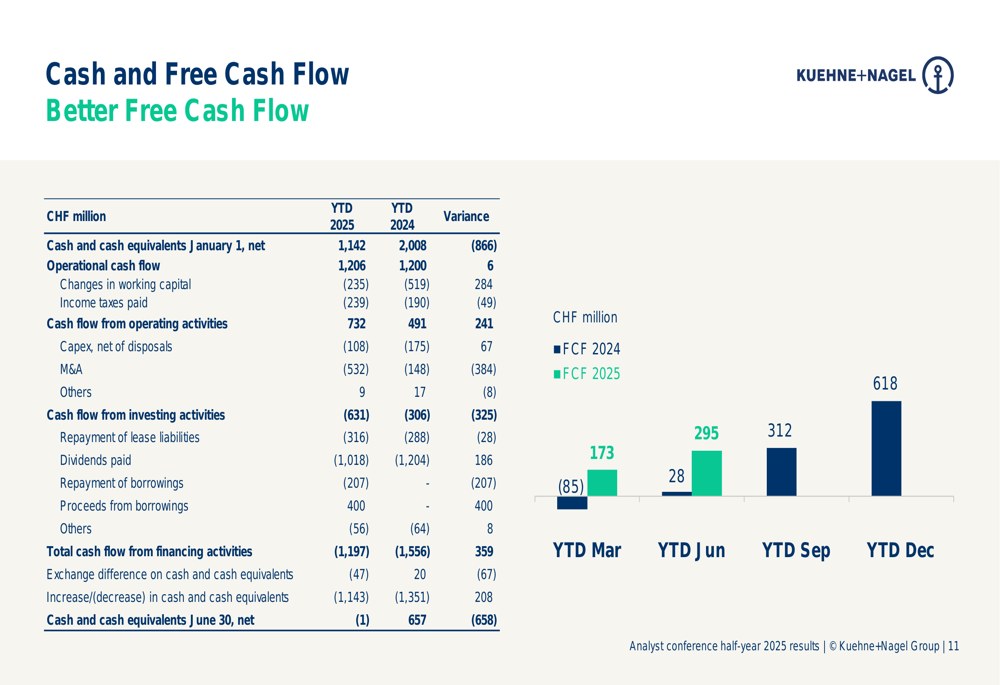

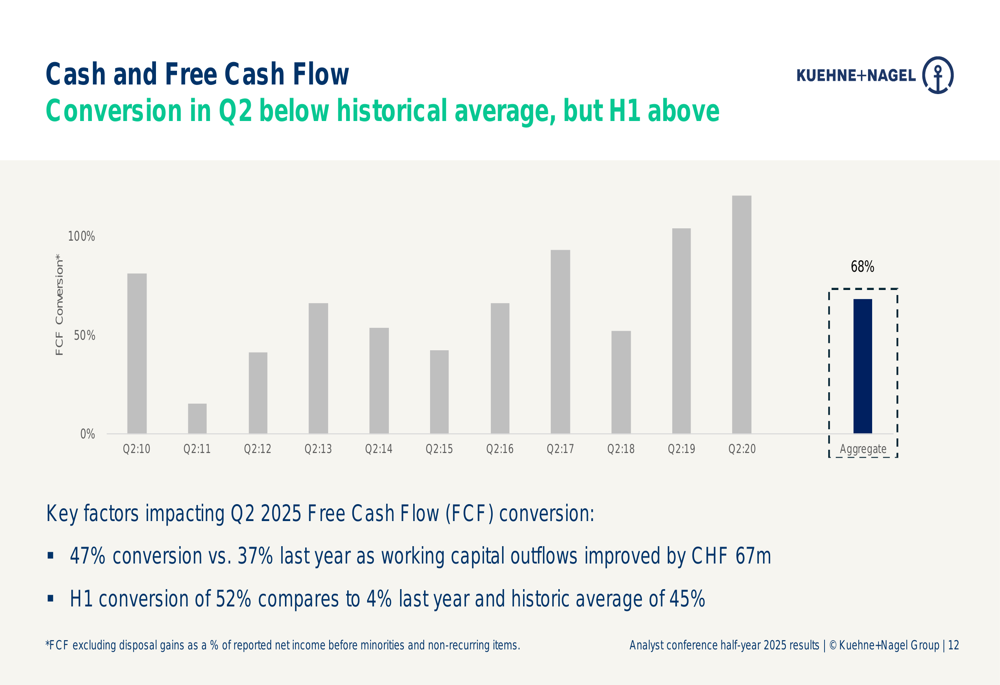

Cash Flow and Working Capital

A standout aspect of Kuehne + Nagel’s H1 2025 results was the significant improvement in cash flow generation. Free cash flow reached CHF 295 million, compared to just CHF 28 million in H1 2024, with a conversion rate of 52% versus 4% last year.

The following chart illustrates the company’s cash flow development:

The free cash flow conversion rate showed substantial improvement, as demonstrated in this historical comparison:

Working capital intensity stood at 4.8% as of June 30, 2025, at the higher end of the company’s target corridor but showing sequential improvement from 5.1% at the end of Q1 2025. The DSO/DPO spread narrowed significantly to 3.2 days from 9.0 days a year earlier, indicating less favorable payment terms.

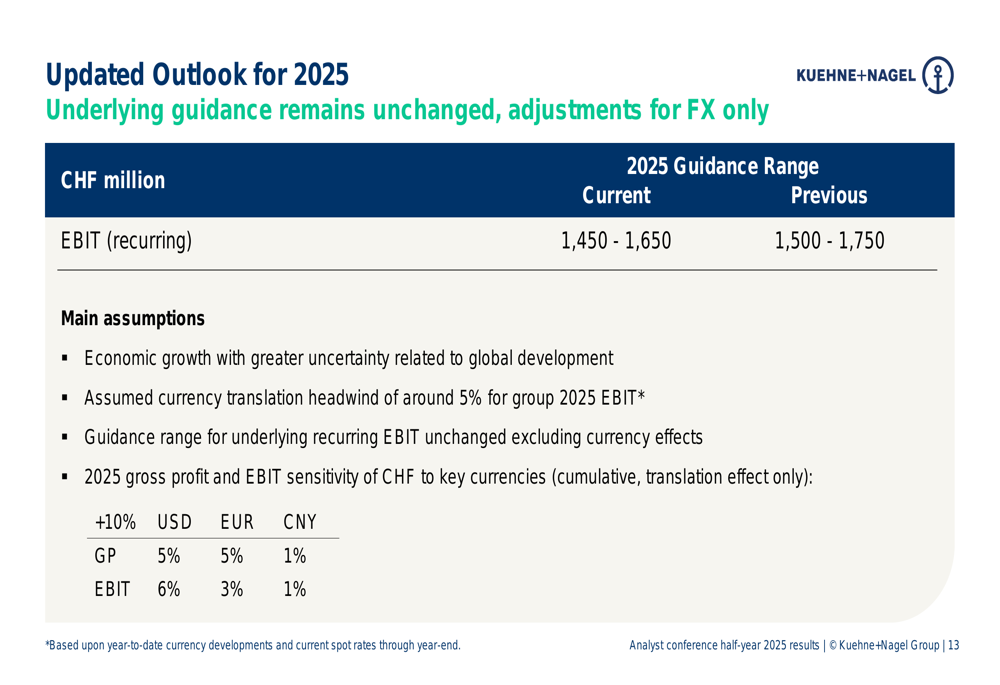

Outlook and Guidance

Based on the first-half performance and anticipated currency headwinds, Kuehne + Nagel has revised its full-year 2025 EBIT guidance to CHF 1,450-1,650 million, down from the previous range of CHF 1,500-1,750 million. The company emphasized that the underlying guidance range remains unchanged excluding currency effects, which are expected to create a headwind of around 5% for group 2025 EBIT.

The updated outlook and assumptions are detailed in the following slide:

Management highlighted increased uncertainty related to global economic development, particularly in trade relations. The company remains focused on market share gains in attractive sectors and maintaining agility in response to global trade uncertainties.

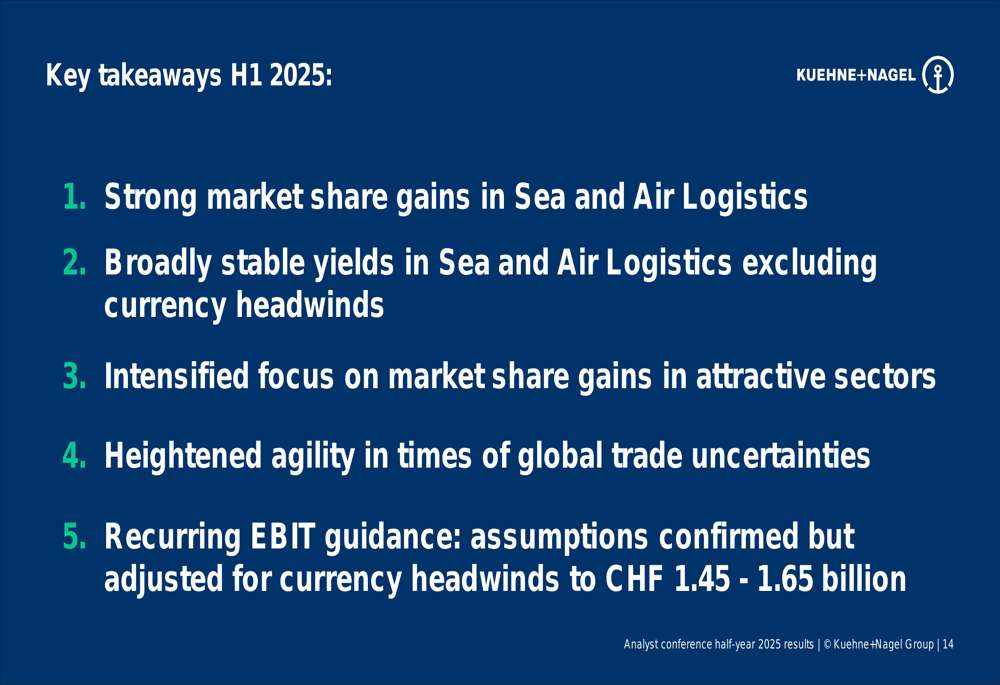

Strategic Initiatives

Kuehne + Nagel continues to execute its strategic roadmap focused on four key pillars: Kuehne+Nagel Experience, Market Potential, Digital Ecosystem, and Living ESG. The company is particularly emphasizing sales excellence and differentiated higher-margin service offerings to drive growth in challenging market conditions.

The key takeaways from the H1 2025 results underscore this strategic focus:

Comparing these results with Q1 2025, which showed strong growth with an 8% increase in gross profit and 7% increase in EBIT, the second quarter demonstrates a clear slowdown in momentum. However, the company’s ability to maintain market share gains while generating strong cash flow indicates underlying operational resilience despite the challenging environment.

In conclusion, Kuehne + Nagel’s H1 2025 results reflect a company navigating a complex global trade environment with a strategic focus on market share gains and cash generation, while managing the impact of significant currency headwinds on profitability. The revised guidance suggests cautious optimism for the remainder of the year, contingent on stabilization in currency markets and continued execution of strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.