Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

Kulicke and Soffa Industries Inc (NASDAQ:KLIC) presented its third quarter fiscal 2025 earnings results on August 6, 2025, highlighting a period of continued challenges but with emerging signs of recovery. The semiconductor equipment manufacturer reported that trade-related uncertainty contributed to order hesitation early in the quarter, particularly affecting demand in the automotive and industrial segments.

The presentation comes after a disappointing second quarter that saw the company post significant losses while undergoing restructuring of its Electronics Assembly business. With shares down over 34% in the six months prior to Q2 results, investors have been closely watching for signs of stabilization.

Quarterly Performance Highlights

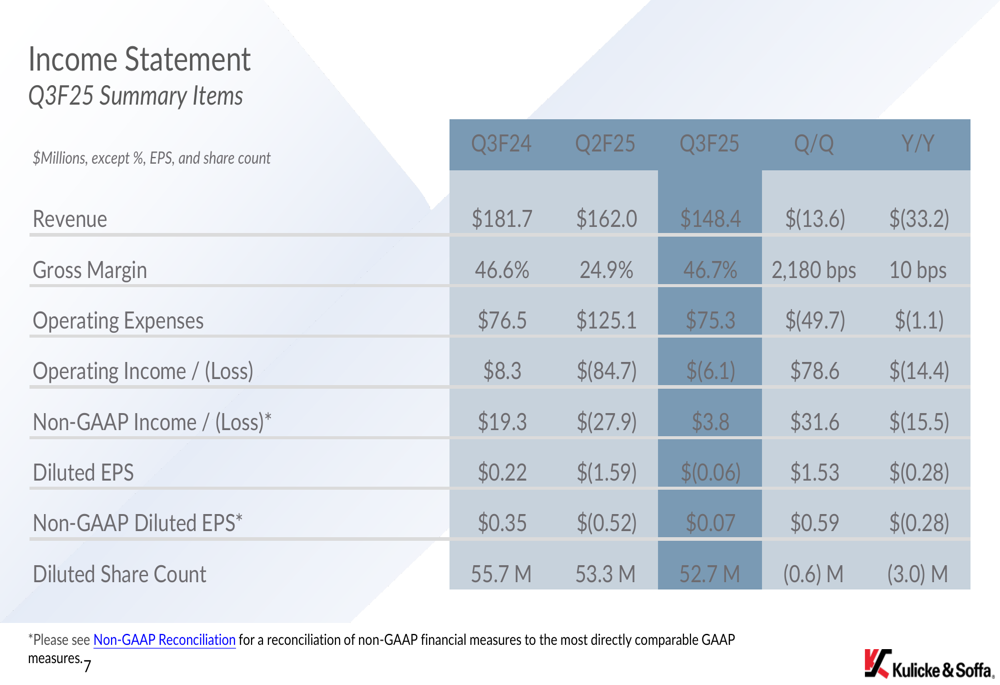

Kulicke & Soffa reported Q3F25 revenue of $148.4 million, representing an 8.4% sequential decline from the previous quarter’s $162 million. The company posted a GAAP net loss of $3.3 million or $(0.06) per share, while non-GAAP net income came in at $3.8 million or $0.07 per share.

As shown in the following comprehensive income statement, the company demonstrated significant improvement in gross margin, which rose to 46.7% from 24.9% in the previous quarter:

This margin improvement reflects the company’s progress in completing its restructuring efforts. Operating expenses decreased substantially to $75.3 million from $125.1 million in Q2F25, contributing to a much smaller operating loss of $6.1 million compared to the previous quarter’s $84.7 million loss.

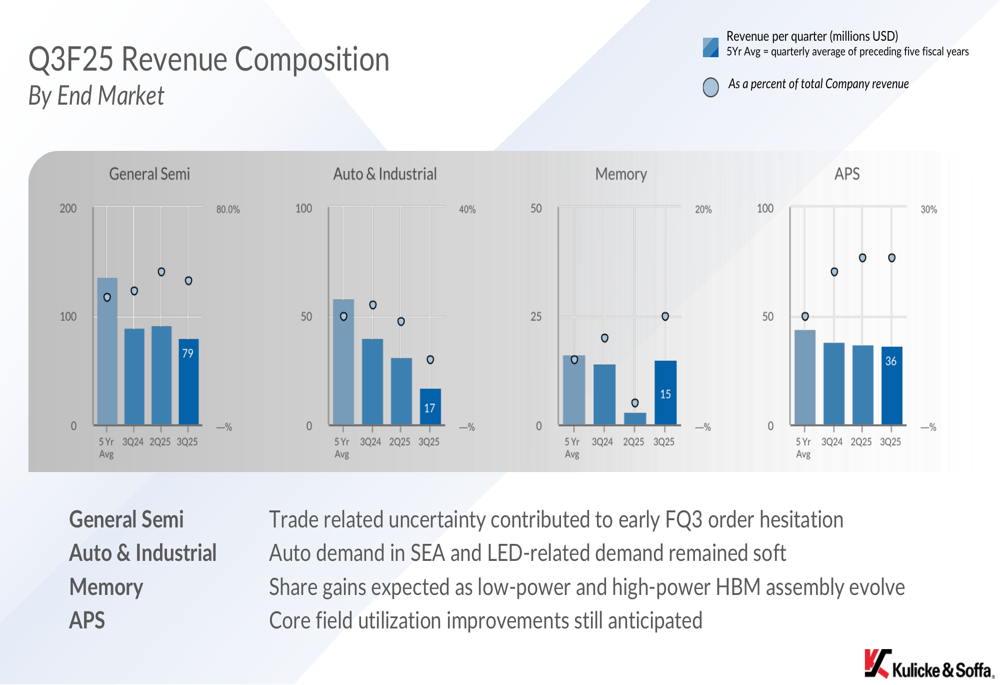

The revenue breakdown by end market reveals that General Semiconductor remains the company’s largest segment, while Auto & Industrial demand faced particular challenges:

Detailed Financial Analysis

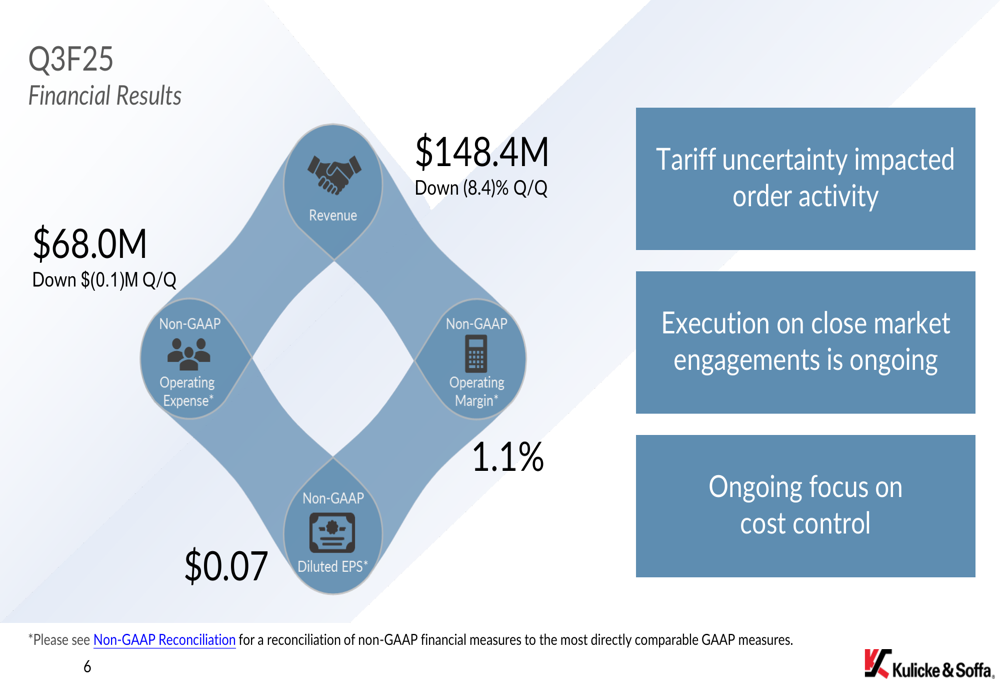

Despite the sequential revenue decline, Kulicke & Soffa maintained a strong financial position with $368 million in net cash. The company continued its capital return program, repurchasing $21.6 million in shares and paying $10.8 million in dividends during the quarter.

The company’s financial results circular diagram highlights the key metrics for the quarter:

Operating margin on a non-GAAP basis was positive at 1.1%, showing improvement from the previous quarter’s losses. The company attributed the sequential revenue decline primarily to macro order hesitation, which particularly affected Auto/Industrial demand. However, management noted that technology and capacity-related order activity is driving recovery in the General Semiconductor and Memory segments.

Strategic Initiatives

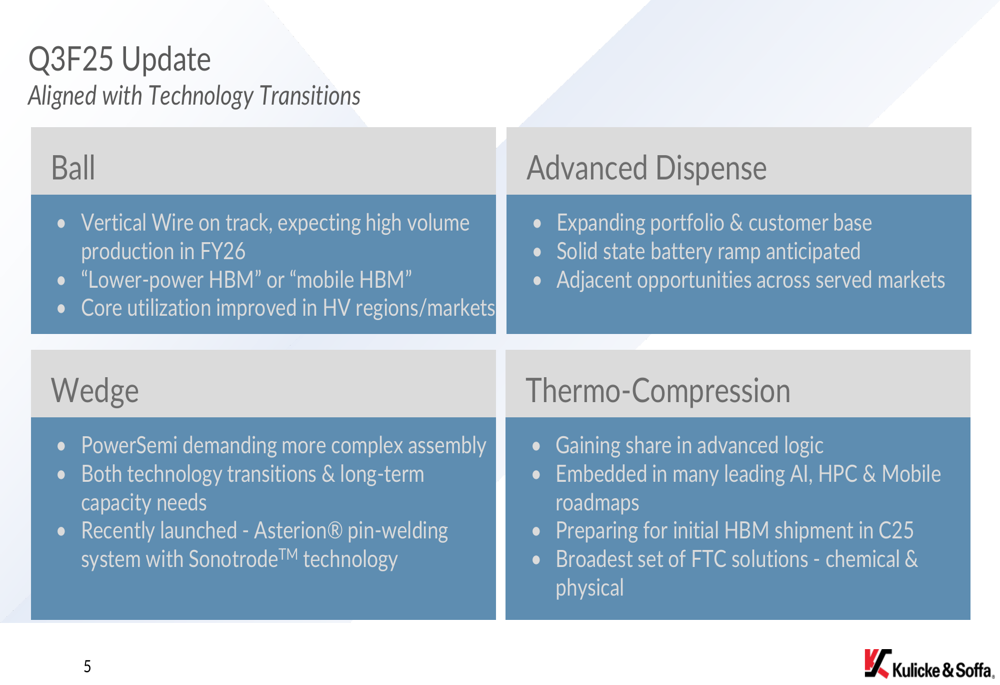

Kulicke & Soffa emphasized its focus on several key technology transitions that are expected to drive long-term growth. The company is making progress with its Vertical Wire technology, which is positioned for mobile High Bandwidth (NASDAQ:BAND) Memory (HBM) applications, with high volume production expected in FY26.

The company’s presentation outlined progress across four key technology areas:

In the Wedge segment, the company recently launched the Asterion® pin-welding system with Sonotrode™ technology to address increasingly complex power semiconductor assembly requirements. The Advanced Dispense business is expanding its portfolio and customer base, with solid-state battery production ramps anticipated.

Perhaps most significantly, the company’s Thermo-Compression technology is gaining share in advanced logic applications and is embedded in many leading AI, high-performance computing, and mobile roadmaps. The company is preparing for initial HBM shipments in calendar year 2025.

Forward-Looking Statements

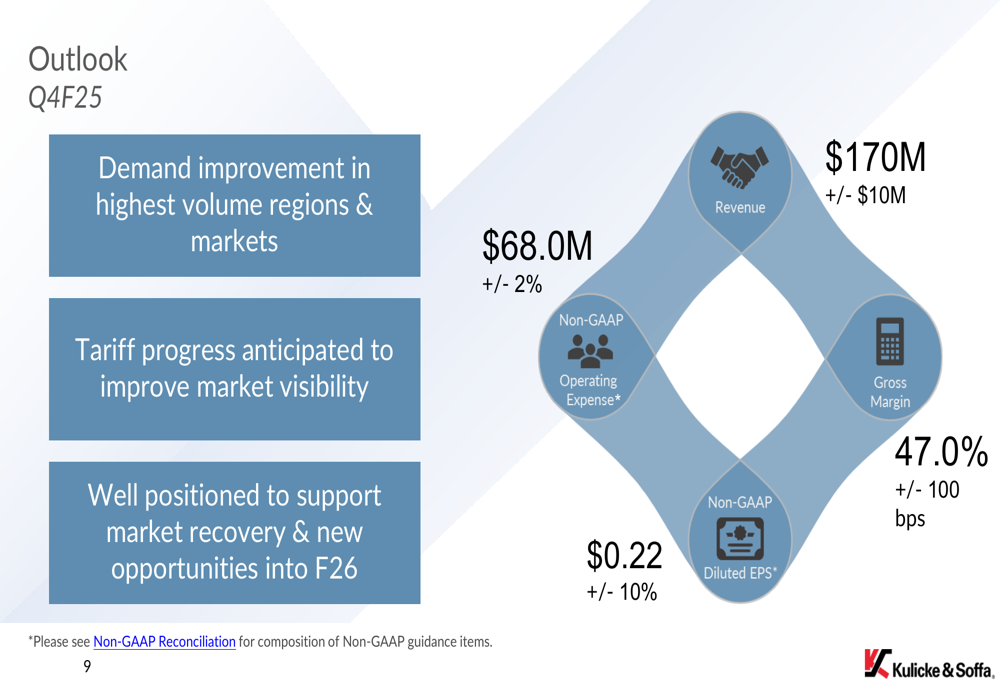

Looking ahead to Q4F25, Kulicke & Soffa provided an optimistic outlook, projecting revenue of $170 million (plus or minus $10 million) and non-GAAP EPS of $0.22 (plus or minus 10%). This represents a significant sequential improvement in both revenue and profitability.

The company’s outlook for the coming quarter is summarized in this forward-looking guidance:

Management expects demand improvement in the highest volume regions and markets, with tariff progress anticipated to improve market visibility. The company believes it is well-positioned to support market recovery and new opportunities as it moves into fiscal year 2026.

The guidance suggests gross margin will remain strong at 47.0% (plus or minus 100 basis points), while operating expenses are expected to hold steady at $68.0 million (plus or minus 2%).

As Kulicke & Soffa works through its transition period, the company appears to be making progress toward sustainable growth, with its technology roadmap and improving financial metrics providing some encouragement for investors after several challenging quarters. However, the company still faces headwinds from trade uncertainties and uneven demand across its end markets as it works to return to consistent profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.