How are energy investors positioned?

Introduction & Market Context

L3Harris Technologies (NYSE:LHX) reported strong second-quarter 2025 results on July 24, with record orders driving significant backlog growth and continued margin expansion. The aerospace and defense company’s shares rose 2% in premarket trading to $275, extending their 52-week high as investors responded positively to the results and raised guidance.

The company’s performance comes amid increased global defense spending and growing demand for advanced technology solutions in space, missile defense, and communications systems. L3Harris continues to benefit from its strategic positioning in these high-growth areas, leveraging its "Trusted Disruptor" approach to capture market share.

Quarterly Performance Highlights

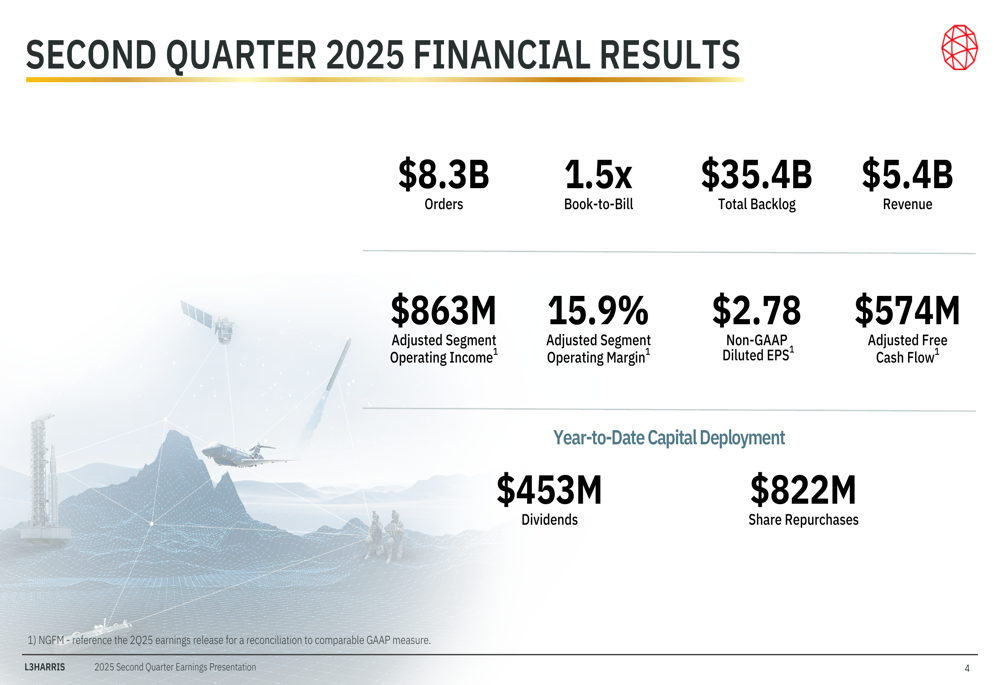

L3Harris reported second-quarter orders of $8 billion, resulting in a book-to-bill ratio of 1.5x—the highest since the company’s merger. This strong order activity pushed total backlog to a record $35.4 billion, providing substantial visibility for future revenue growth.

Revenue for the quarter reached $5.4 billion, representing 6% organic growth compared to the same period last year. The company achieved a segment operating margin of 15.9%, marking the seventh consecutive quarter of margin expansion.

As shown in the following financial results summary:

Non-GAAP diluted earnings per share grew 16% year-over-year to $2.78, or 22% on a pension-adjusted basis. The company generated $574 million in adjusted free cash flow during the quarter and returned significant capital to shareholders, with year-to-date capital deployment including $453 million in dividends and $822 million in share repurchases.

Segment Performance

All four of L3Harris’ business segments contributed to the company’s strong performance, with particularly notable results in the Aerojet Rocketdyne division.

The Communication Systems segment reported revenue of $1.376 billion, up from $1.346 billion in the prior year period. The segment maintained a robust operating margin of 24.4%, driven by increased international demand for resilient communication equipment and related waveforms.

Integrated Mission Systems delivered revenue of $1.622 billion, with organic growth of 6% when adjusting for divestitures. Operating margin improved significantly to 13.2% from 12.0% in the prior year, benefiting from monetization of legacy end-of-life assets.

Space & Airborne Systems saw revenue increase to $1.787 billion, representing 7% organic growth. This segment’s performance was supported by increased FAA volume, though operating margin slightly decreased to 12.3% from 12.6% a year earlier.

The Aerojet Rocketdyne segment showed the strongest growth, with revenue increasing to $698 million—up 12% organically. Operating margin improved to 13.3% from 12.8%, driven by cost savings from the L3Harris NeXt initiative.

Strategic Initiatives

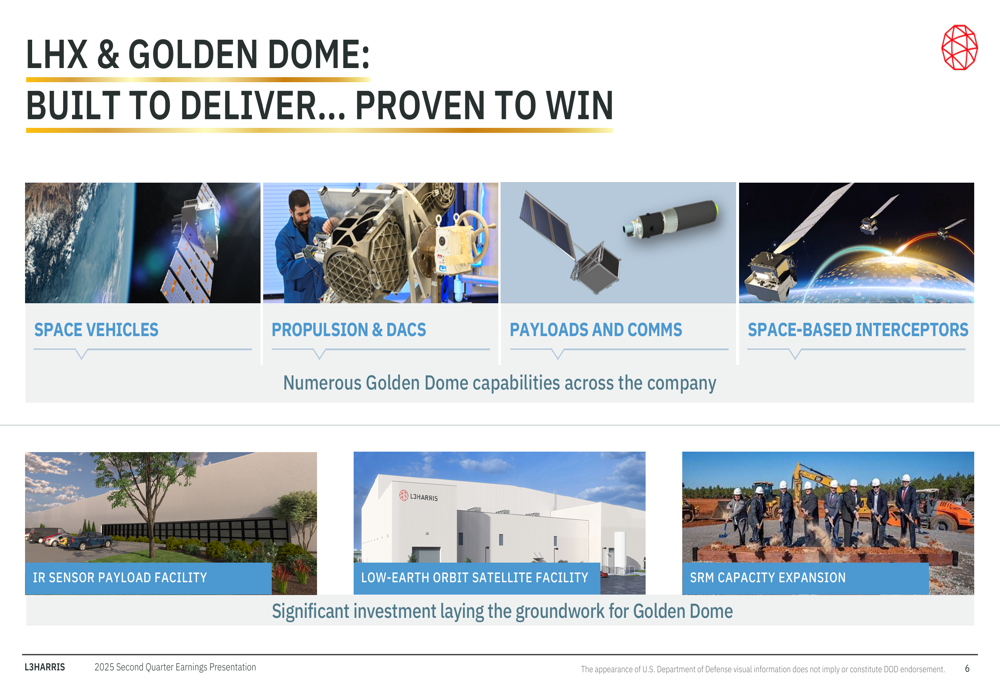

L3Harris continues to execute on its "Trusted Disruptor" strategy, which aims to position the company as both a reliable defense contractor and an innovative technology provider. The strategy is yielding results across multiple business areas, as illustrated in the following slide:

A key strategic focus is the Golden Dome initiative, which leverages L3Harris’ capabilities across space vehicles, propulsion systems, payloads, communications, and missile defense. The company is making significant investments in this area, as shown in the following overview:

These investments include expansion of facilities in Fort Wayne, Indiana, and Palm Bay, Florida, as well as the development of "factories of the future" that leverage robotics and automation for solid rocket motor production.

Updated Guidance and Outlook

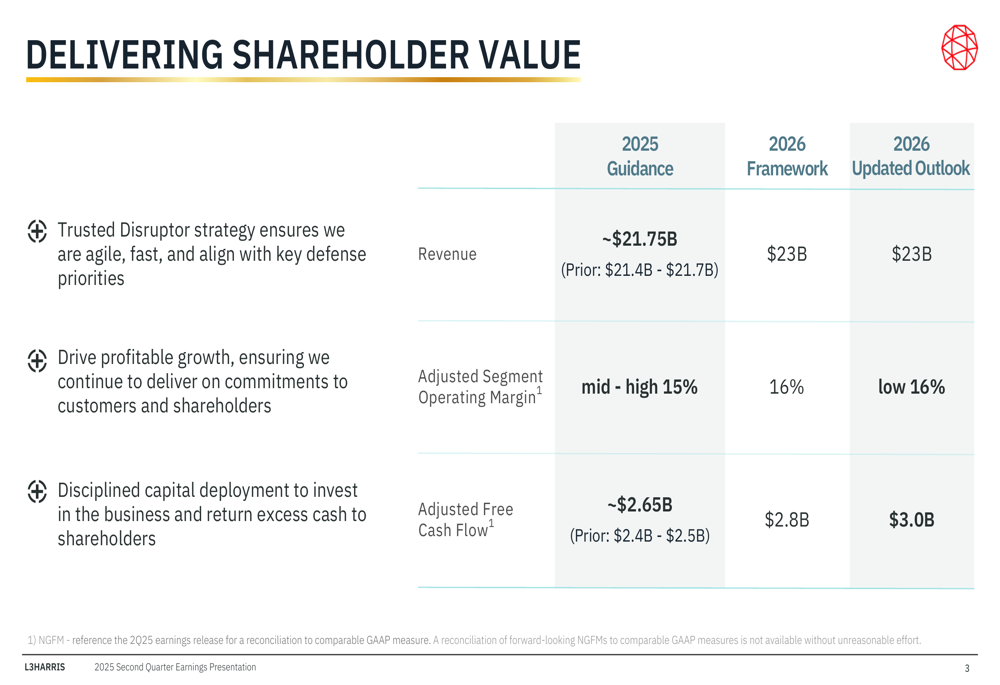

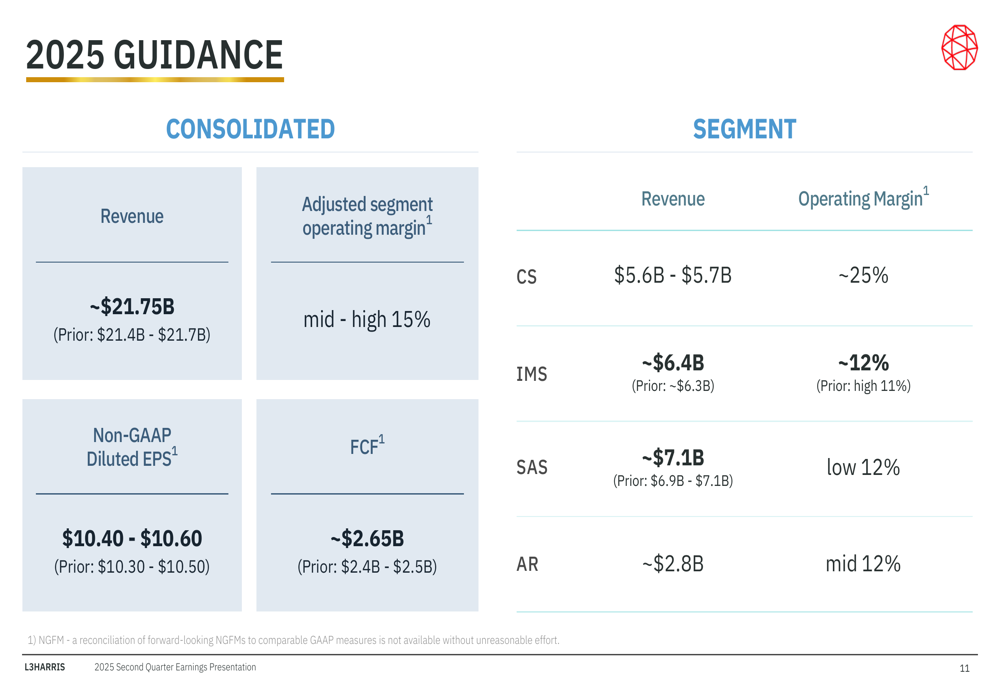

Based on strong first-half performance, L3Harris has raised its full-year 2025 guidance. The company now expects revenue of approximately $21.75 billion, up from the previous range of $21.4-$21.7 billion. Adjusted free cash flow guidance has been increased to approximately $2.65 billion from the prior range of $2.4-$2.5 billion.

The company’s updated guidance and long-term framework are detailed in the following slide:

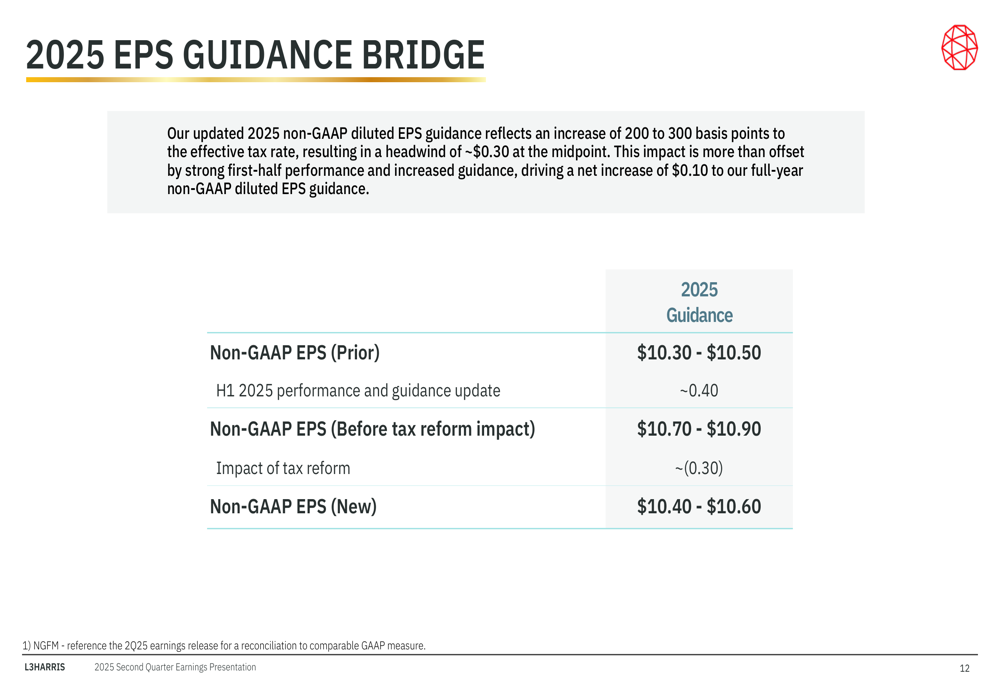

Non-GAAP EPS guidance has been updated to $10.40-$10.60, reflecting both strong operational performance and the impact of tax reform. The following bridge explains the changes to the EPS guidance:

Looking further ahead, L3Harris has maintained its 2026 revenue target of $23 billion, with adjusted segment operating margin expected to reach the low 16% range and adjusted free cash flow projected at $3.0 billion.

The company’s segment-specific guidance for 2025 provides additional detail on expected performance:

With record backlog, expanding margins, and strategic investments in high-growth areas, L3Harris appears well-positioned to deliver on both its near-term guidance and longer-term financial framework. The company’s focus on innovation and operational efficiency continues to drive shareholder value in an increasingly complex global defense environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.