Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

Lakeland Financial Corporation (NASDAQ:LKFN), the parent company of Lake City Bank, presented its first quarter 2025 results highlighting the company’s long-term growth trajectory, strong capital position, and strategic focus on commercial banking. The Indiana-based financial institution, which operates 54 branch offices and manages $6.9 billion in banking assets, continues to emphasize its organic growth strategy amid a changing interest rate environment.

The bank’s stock closed at $54.59 on April 24, 2025, up 0.18% for the day, though it was trading down 2% in premarket activity on April 25. The shares have traded between $50.74 and $78.61 over the past 52 weeks, reflecting some volatility in the regional banking sector.

Quarterly Performance Highlights

Lakeland Financial reported net income of $20.1 million for Q1 2025, with earnings per share of $0.78, representing a 14% decrease compared to the same period last year. Despite this earnings pressure, the company highlighted several positive developments, including revenue growth of 6% and expanding net interest margin.

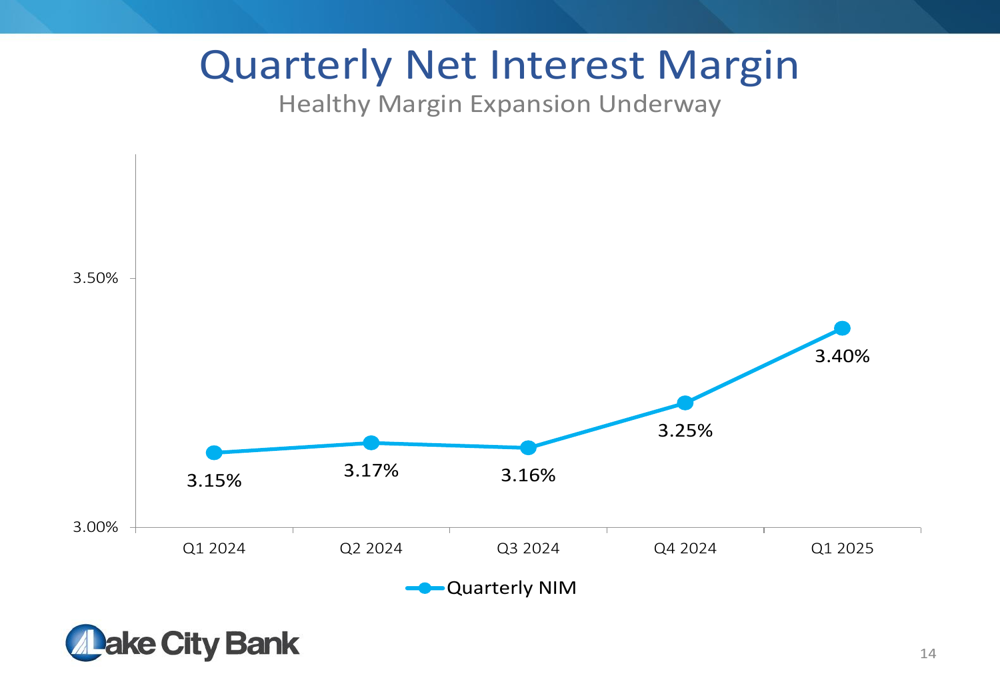

As shown in the following chart, the company’s net interest margin expanded by 15 basis points quarter-over-quarter, reaching 3.40% in Q1 2025 compared to 3.25% in Q4 2024:

This margin expansion was driven by deposit costs coming down more rapidly than loan repricing in the current easing cycle. Management noted that noninterest-bearing deposits remained stable at 22% of total deposits, while the cumulative deposit beta for the easing cycle stands at 55%, compared to a loan beta of 37%.

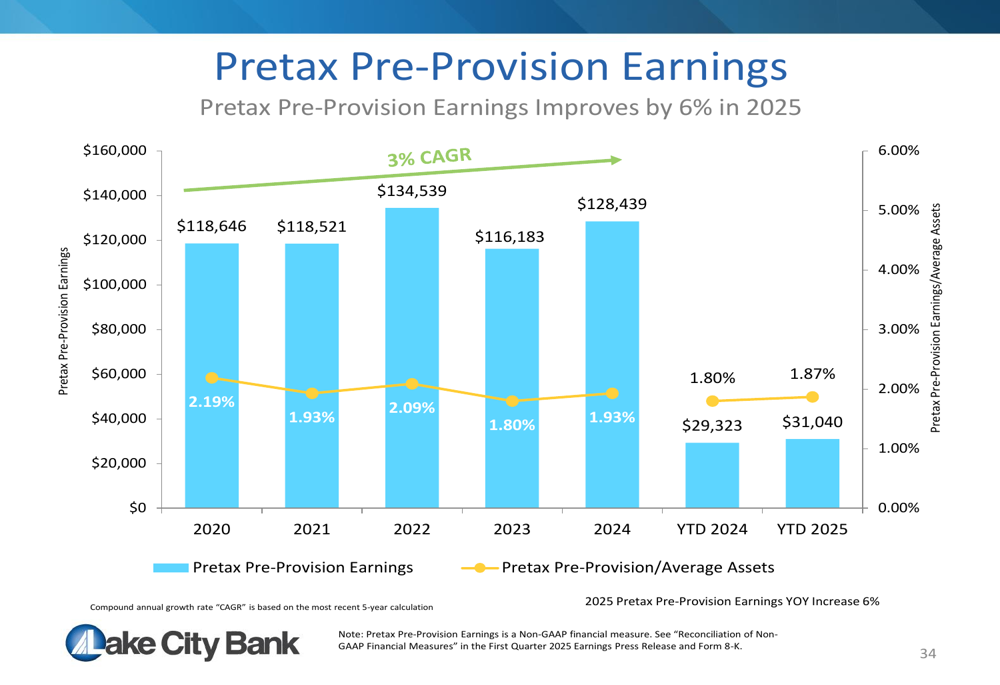

The company’s pretax pre-provision earnings improved by 6% year-over-year, reaching $31.0 million in Q1 2025 compared to $29.3 million in Q1 2024:

Balance Sheet Strength & Loan Growth

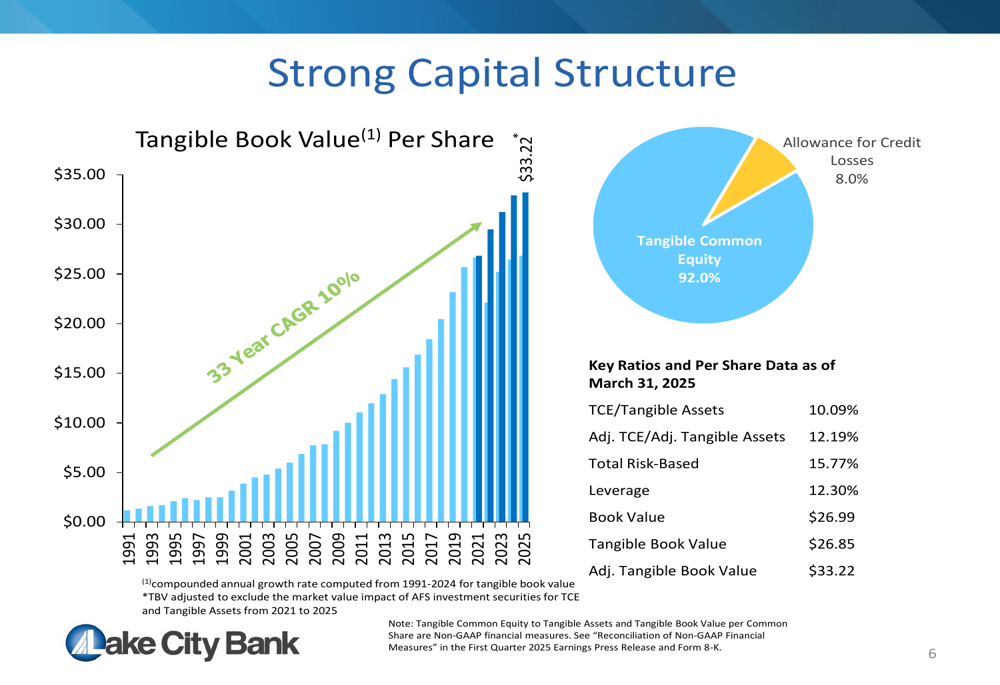

Lakeland Financial emphasized its strong capital position, with tangible common equity to tangible assets at 10.09% as of March 31, 2025. The company’s risk-based capital ratio of 15.77% significantly exceeds the well-capitalized threshold of 10.0%.

As illustrated in the following chart, the company has maintained a strong tangible book value growth trajectory with a 33-year CAGR of 10%:

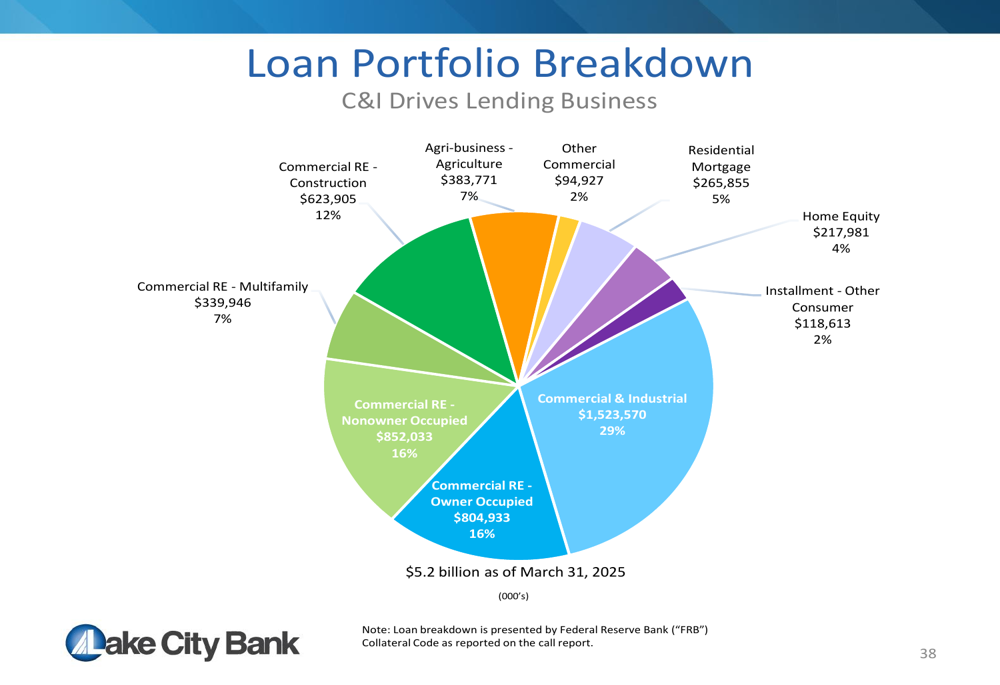

Average loans increased by $215 million or 4% year-over-year, primarily driven by growth in the commercial portfolio. The company’s loan composition remains heavily weighted toward commercial lending, which represents 89% of the total loan portfolio:

The bank’s commercial real estate exposure is diversified, with owner-occupied properties representing 16% of the portfolio, while construction loans account for 12%. Notably, the company emphasized its minimal exposure to office properties, which represent only 2% of the total loan portfolio.

Deposit Strategy & Funding

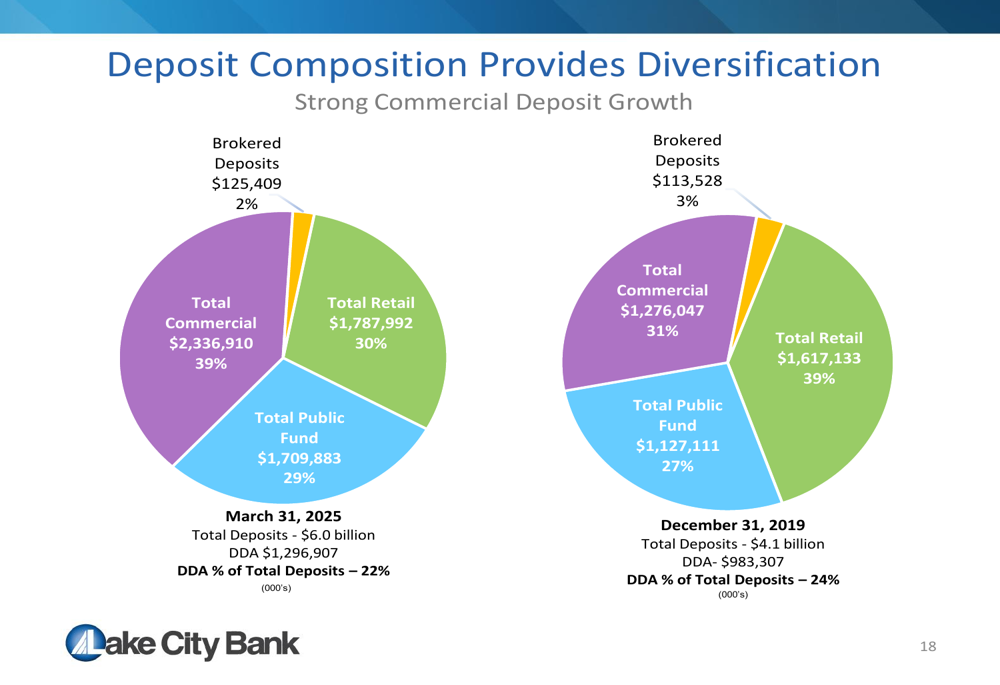

Lakeland Financial’s deposit base remains diversified across commercial, retail, and public fund segments. The presentation highlighted that commercial deposits have increased as a percentage of total deposits, now representing 39% compared to 31% at the end of 2019:

The company emphasized that 98% of deposit accounts are less than $250,000, providing stability to the funding base. Additionally, public funds in Indiana are covered by the Public Deposit Insurance Fund (PDIF), offering additional security for this segment which represents 29% of total deposits.

Management highlighted the bank’s strong position in attracting and retaining deposits in its mature markets, noting that Lake City Bank has grown deposits by 93% over the last ten-year period, outperforming several larger competitors in the region.

Digital Transformation & Customer Engagement

The presentation emphasized Lakeland Financial’s ongoing investment in technology and digital banking capabilities. The company implemented a new digital platform in 2021 through a fintech partnership, which has driven increased adoption across all customer generations.

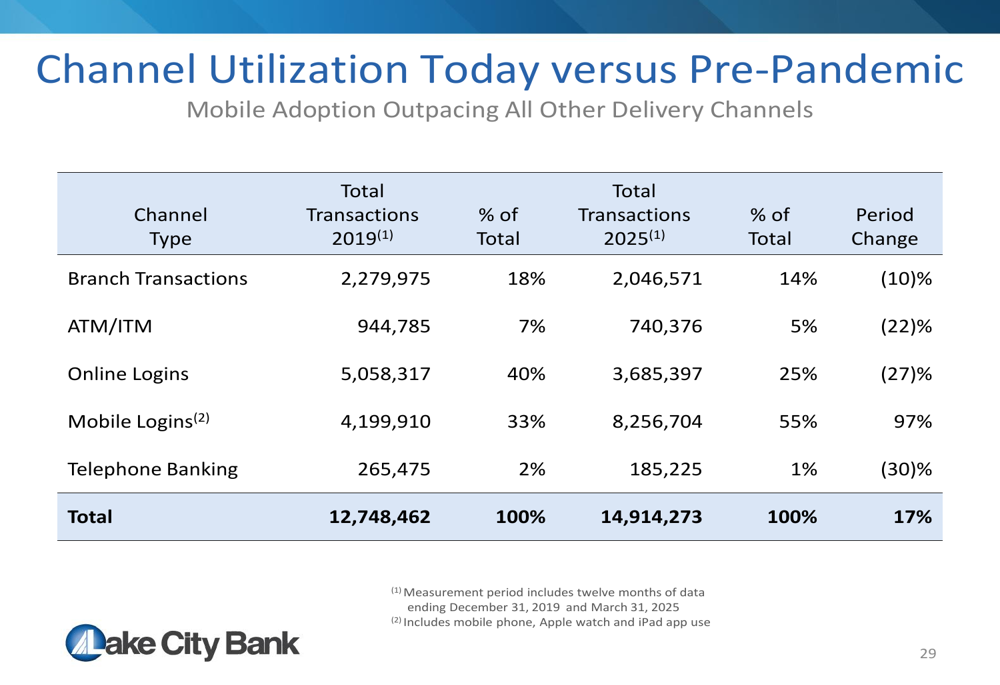

As shown in the following chart, mobile banking adoption has significantly outpaced all other delivery channels when comparing current usage to pre-pandemic levels:

Digital adoption has increased to 52% as of March 31, 2025, up from 50% a year earlier and 49% two years ago. The company noted that this trend spans across all customer generations, including baby boomers and mature customers.

Regional Economic Outlook

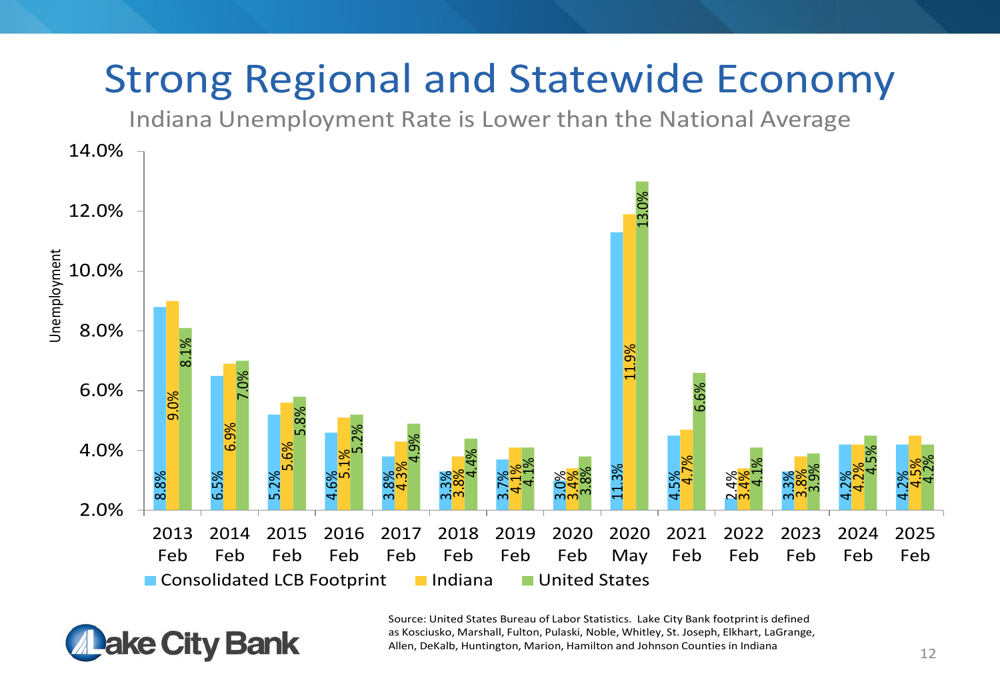

Lakeland Financial emphasized the strong economic fundamentals in its Indiana markets, noting that 67% of the counties in its footprint are classified as growth or high-growth counties based on population projections.

The unemployment rate in the bank’s consolidated footprint stands at 4.2%, equal to the national average and below Indiana’s state average of 4.5%, as illustrated in the following chart:

The presentation highlighted Indiana’s position as the top manufacturing state in the country, with recent tech hub designations in microelectronics, hydrogen energy, and biotechnology. Management noted significant economic development initiatives, including Eli Lilly (NYSE:LLY)’s $13 billion investment in Indiana’s LEAP Research and Innovation District.

Forward-Looking Statements

Looking ahead, Lakeland Financial remains focused on its commercial banking strategy, emphasizing relationship-driven lending and deposit gathering. The company expects continued margin expansion as deposit costs decline more rapidly than loan yields in the current interest rate environment.

Management highlighted the bank’s asset-sensitive balance sheet, which is positioned to maintain relatively neutral performance in various interest rate scenarios. The company’s interest rate risk modeling suggests minimal impact on net interest income under both rising and falling rate scenarios.

The presentation emphasized Lakeland Financial’s long-term track record of shareholder value creation, noting that it is one of only four institutions with assets between $1 billion and $10 billion that has maintained an LTM ROE above 13% and a 20-year tangible book value per share CAGR exceeding 8%.

Despite the year-over-year decline in earnings for Q1 2025, management expressed confidence in the company’s strategic positioning and growth prospects, supported by Indiana’s favorable economic outlook and the bank’s established market presence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.