Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

Lakeland Industries Inc (NASDAQ:LAKE) presented its fiscal second quarter 2026 financial results on September 9, 2025, highlighting record revenue growth despite facing margin pressures and tariff challenges. The protective equipment manufacturer’s stock closed at $15, down 3.73% in aftermarket trading following the release, reflecting investor concerns about the earnings miss despite strong top-line growth.

The company’s presentation showcased a 36% year-over-year revenue increase, though this fell short of analyst expectations. Lakeland continues to navigate a complex operating environment with facility consolidations, inventory management challenges, and strategic shifts toward fire services products.

Quarterly Performance Highlights

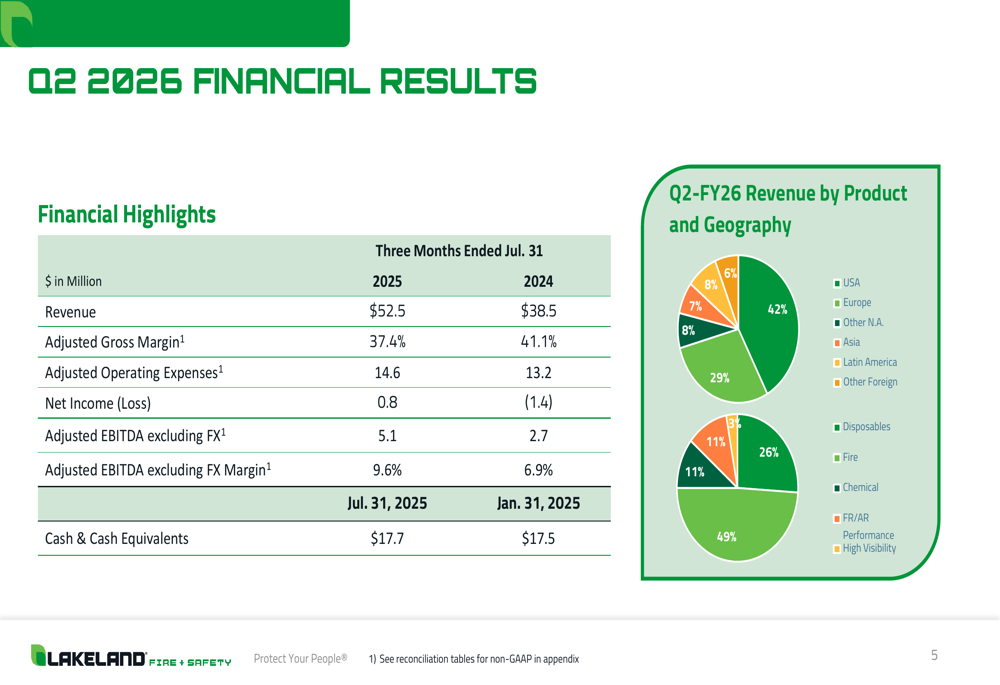

Lakeland reported record Q2 net sales of $52.5 million, representing a 36% increase from the prior year, driven primarily by a 113% surge in Fire Services products. Geographic performance was notably strong in key markets, with U.S. sales increasing 78% to $22.1 million and European sales more than doubling with a 113% increase to $15.1 million.

As shown in the following quarterly financial results:

Despite the impressive revenue growth, Lakeland’s adjusted gross margin declined to 37.4% from 41.1% in the comparable period. The company’s adjusted EBITDA excluding foreign exchange effects reached $5.1 million, an 89% increase from the prior year, with adjusted EBITDA margin expanding to 9.6% from 6.9%.

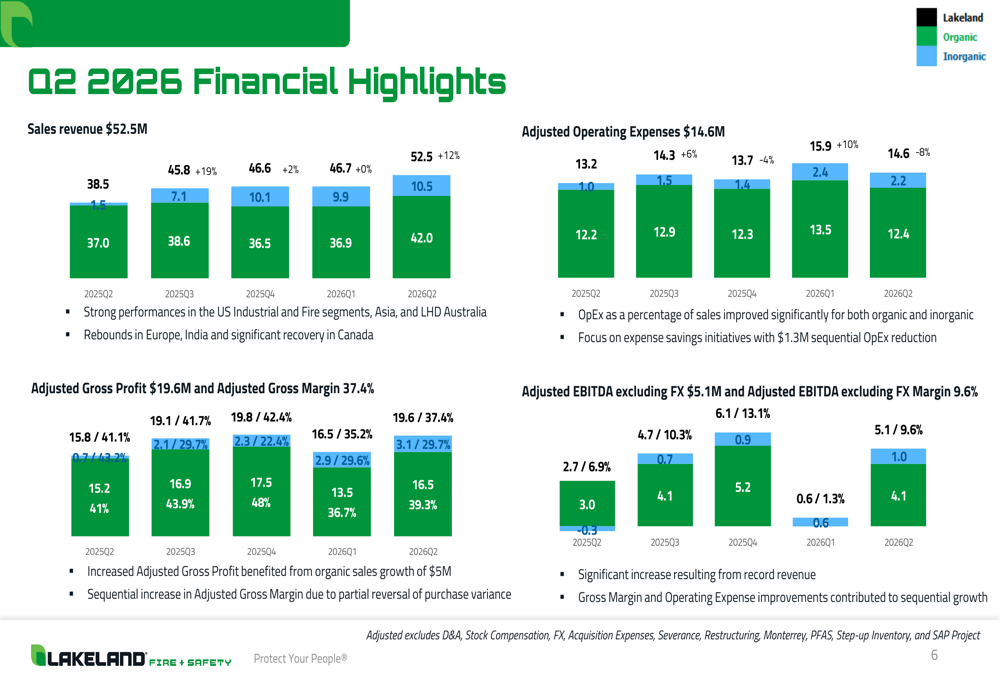

The company’s revenue trends over recent quarters demonstrate consistent growth, with both organic and inorganic contributions:

Detailed Financial Analysis

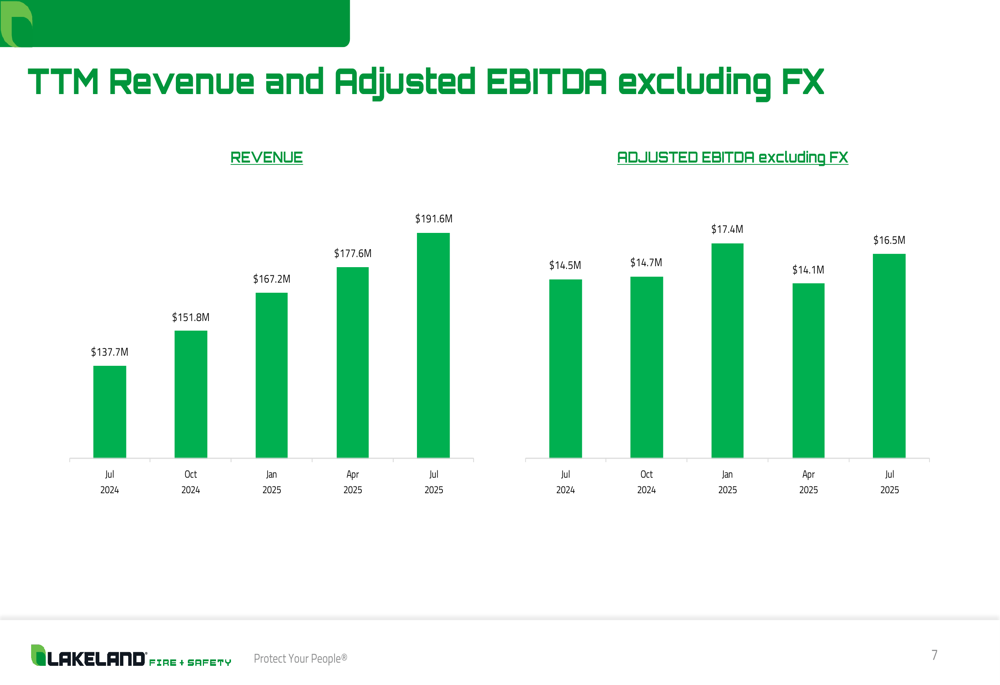

Lakeland’s trailing twelve-month (TTM) performance shows sustained growth, with revenue increasing from $137.7 million in July 2024 to $191.6 million in July 2025. Similarly, adjusted EBITDA excluding FX effects grew from $14.5 million to $16.5 million over the same period.

The following chart illustrates this growth trajectory:

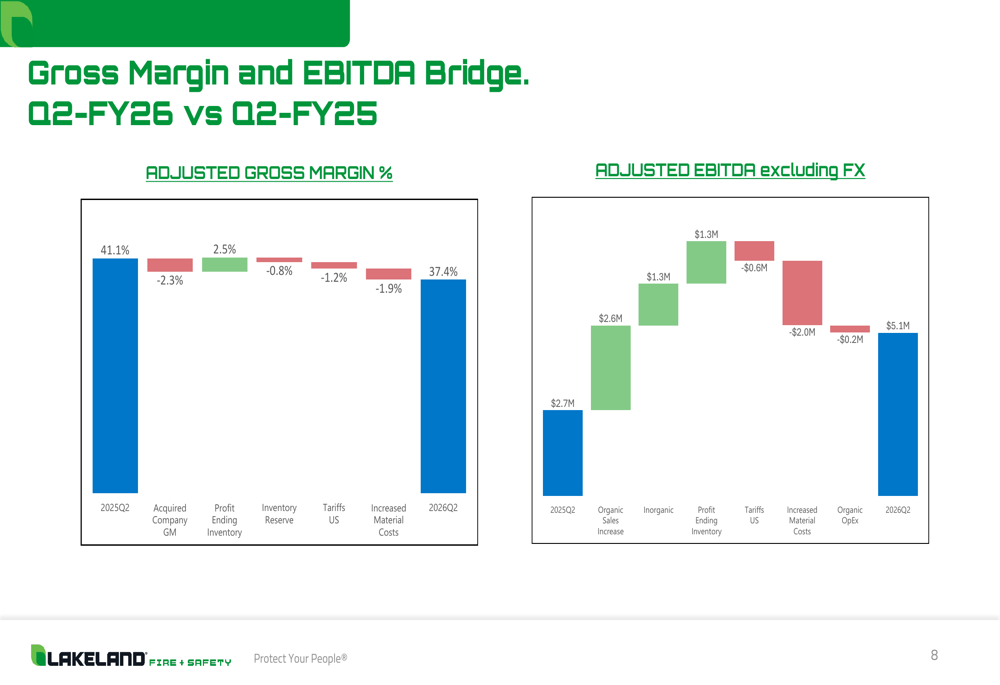

The company’s presentation provided a detailed breakdown of factors affecting gross margin and EBITDA performance. The adjusted gross margin decline from 41.1% to 37.4% was attributed to several factors, including the acquired company impact (2.5%), profit reserve ending inventory (-2.3%), inventory reserves (-0.8%), U.S. tariffs (-1.2%), and increased material costs (-1.9%).

This bridge analysis helps visualize the various positive and negative factors affecting performance:

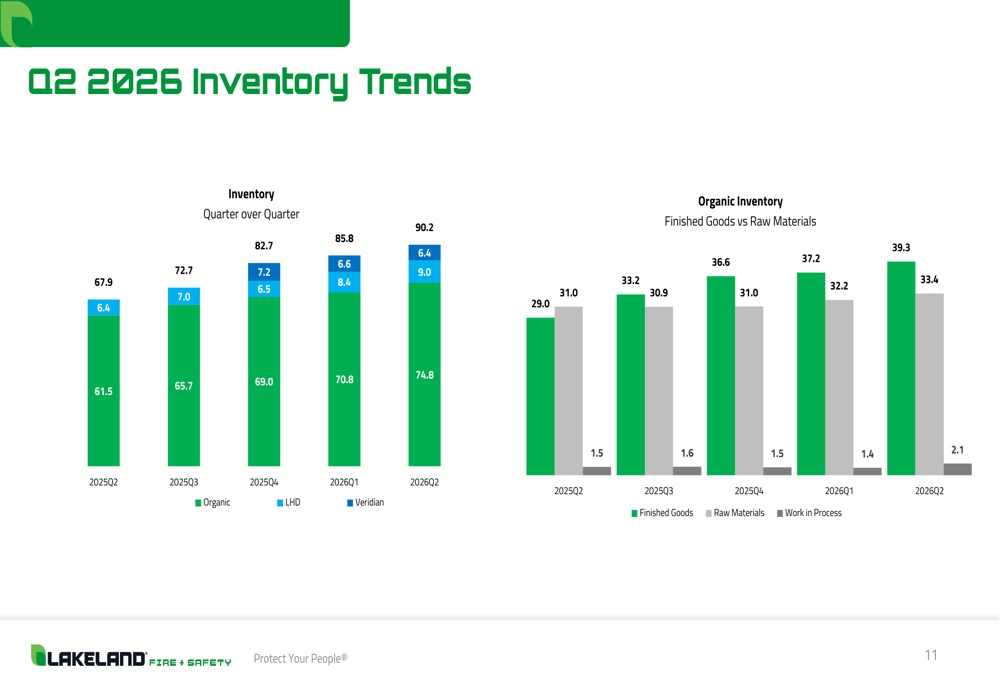

Lakeland’s balance sheet as of July 31, 2025, showed cash and cash equivalents of $17.7 million, slightly up from $17.5 million on January 31, 2025. Total assets increased to $226.3 million from $212.5 million, while inventories grew to $90.2 million from $82.7 million. The company’s cash flow statement revealed net cash used in operating activities of $9.7 million compared to $4.1 million in the prior year, suggesting increased working capital requirements.

Strategic Initiatives & Operational Changes

Lakeland highlighted several strategic initiatives during the quarter, including the shipment of a $3.1 million order for fire intervention boots to the Italian Ministry of the Interior, demonstrating the company’s growing presence in international fire services markets.

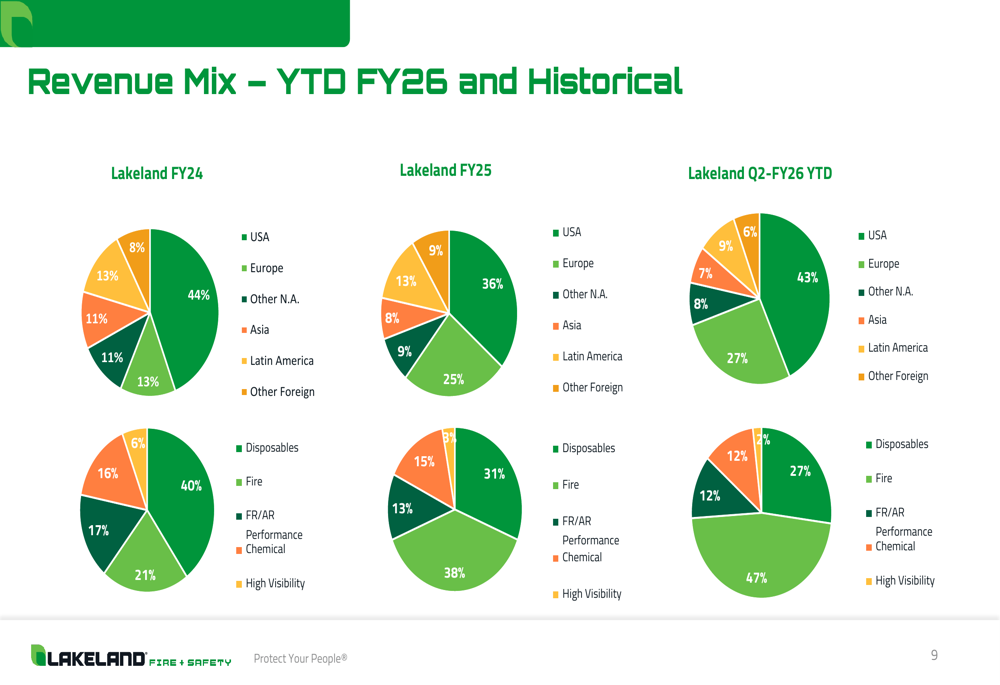

The company’s revenue mix has shifted significantly over recent years, with Performance products growing from 21% of revenue in FY24 to 47% in Q2-FY26 YTD. Geographically, the U.S. market represented 43% of revenue in Q2-FY26 YTD, down slightly from 44% in FY24 but up from 36% in FY25.

The following chart illustrates these shifts in revenue composition:

Operationally, Lakeland completed a $6.1 million sale and partial leaseback of its Decatur, Alabama warehouse property, enhancing liquidity. The company also announced the closures of facilities in Hull, England, and Quitman, Arkansas, as part of its ongoing operational restructuring efforts.

Inventory management remains a challenge, with inventories increasing quarter over quarter. Raw materials account for a growing portion of organic inventory:

Forward-Looking Statements

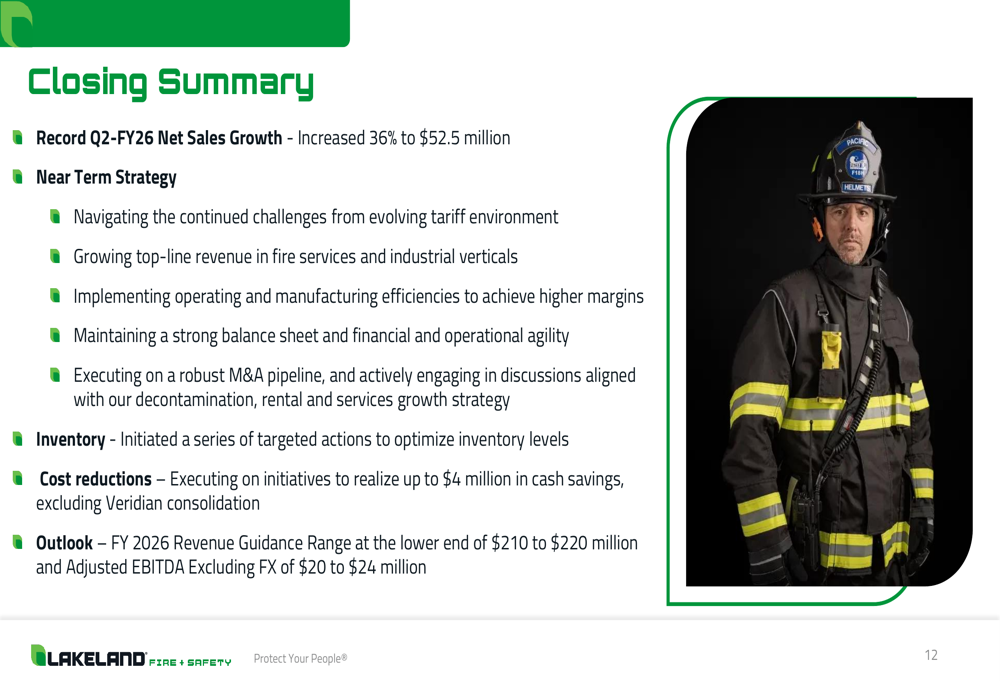

Looking ahead, Lakeland adjusted its fiscal 2026 guidance, now expecting revenue to be at the lower end of its previously announced $210 to $220 million range. The company maintained its adjusted EBITDA excluding FX guidance of $20 to $24 million.

Management outlined its near-term strategy focusing on navigating tariff challenges, growing fire services revenue, improving efficiencies, maintaining a strong balance sheet, and executing its M&A pipeline. The company is also implementing cost reduction initiatives expected to realize up to $4 million in cash savings, excluding Veridian consolidation.

As summarized in the company’s closing slide:

While Lakeland’s presentation emphasized strong revenue growth and strategic positioning, the actual financial results revealed challenges in meeting market expectations. The earnings per share of $0.08 fell significantly short of the forecasted $0.2925, and the reported revenue of $52.5 million missed analyst expectations of $54.59 million. These misses, combined with margin pressures and operational restructuring costs, likely contributed to the stock’s negative performance following the announcement.

As Lakeland continues its strategic shift toward fire services and performance products, investors will be watching closely to see if the company can translate its impressive revenue growth into improved profitability and shareholder returns in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.