NVIDIA launches Jetson Thor robotics computers for physical AI systems

Lamb Weston Holdings Inc (NYSE:LW) shares rose over 4% in premarket trading after the company presented its fourth quarter and full fiscal year 2025 results on July 23, outlining a new strategic framework aimed at reversing profit declines through substantial cost-cutting measures.

Q4 and Full Year Performance Highlights

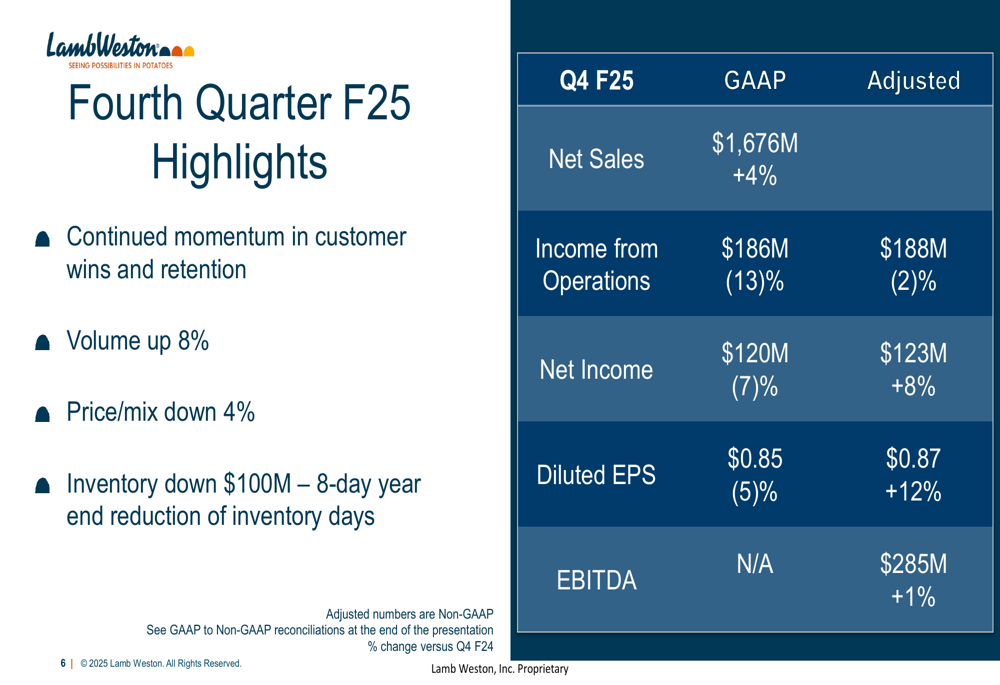

The french fry producer reported fourth-quarter net sales of $1.68 billion, representing a 4% increase year-over-year, driven by 8% volume growth that was partially offset by a 4% decline in price/mix. Despite the sales growth, profitability metrics showed continued pressure, with adjusted EBITDA reaching $285 million, up just 1% from the prior year.

As shown in the following chart of quarterly financial performance:

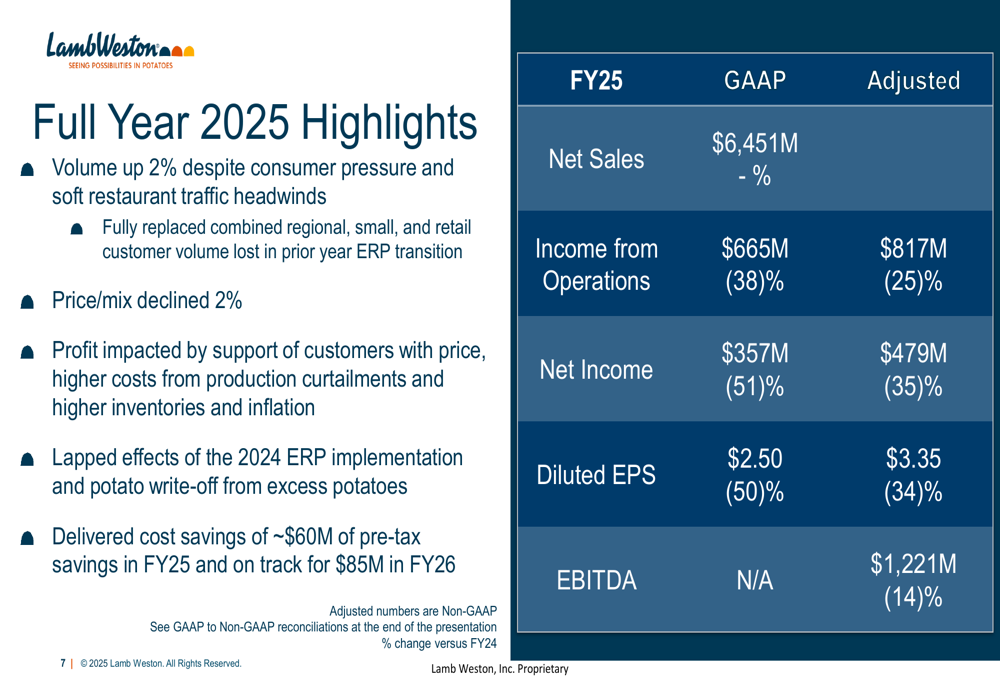

For the full fiscal year 2025, Lamb Weston’s results reflected significant profitability challenges despite modest volume growth. The company reported annual net sales of $6.45 billion, with volume up 2% but price/mix down 2%. Adjusted EBITDA declined 14% to $1.22 billion, while adjusted diluted EPS fell 34% to $3.35.

The full year financial summary reveals the extent of the profit pressure:

"FY25 was a year of substantial change for Lamb Weston," said Mike Smith, President and CEO. "We’re acting with urgency to capitalize on opportunities and seeing results from our efforts to build momentum with customers."

Strategic Initiatives: "Focus to Win" Framework

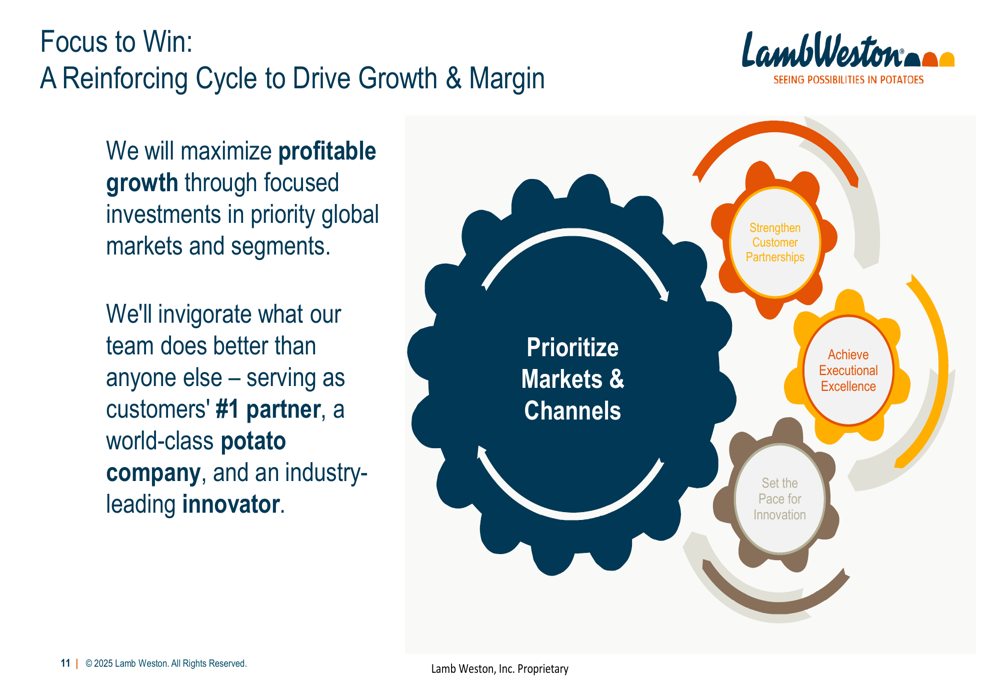

Lamb Weston unveiled its new strategic framework called "Focus to Win," which aims to concentrate resources on the most attractive growth opportunities while building capabilities to strengthen customer relationships and operational excellence.

The company’s strategic approach is illustrated in this reinforcing cycle:

The strategy addresses evolving market dynamics, including changing consumer behavior with the rise of food delivery apps, growth in QSR through chicken, Mexican, and Asian concepts, and continued air fryer penetration enabling retail fry sales. The company also noted high growth in lower margin markets and evolving supply/demand dynamics with new capacity announced in Europe and Asia.

"We will maximize profitable growth through focused investments in priority global markets and segments," Smith emphasized during the presentation.

Cost Reduction and Efficiency Plans

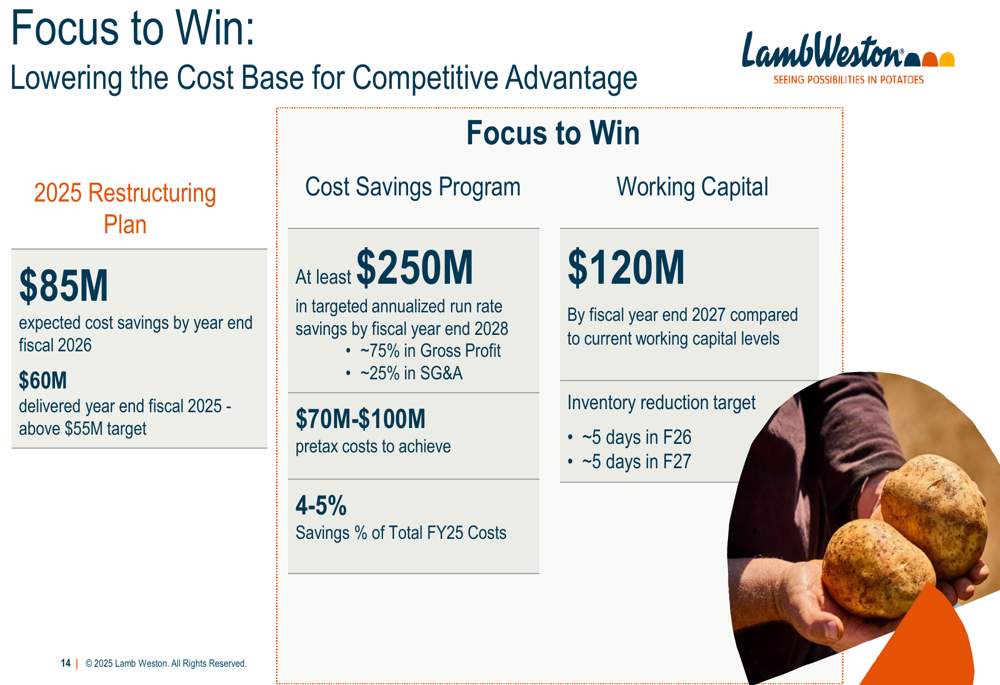

Central to Lamb Weston’s turnaround strategy is an ambitious cost savings program targeting at least $250 million in annualized run-rate savings by fiscal year end 2028. The company plans to achieve these savings through a combination of gross profit improvements (75%) and SG&A reductions (25%).

The details of the cost reduction plan are outlined in this chart:

The company has already delivered $60 million in cost savings in fiscal 2025, exceeding its $55 million target. For fiscal 2026, Lamb Weston expects to achieve $85 million in cost savings.

Additionally, the company is targeting $120 million in working capital improvements by fiscal year end 2027, including inventory reduction of approximately 5 days in both fiscal 2026 and 2027.

Capital Allocation and Shareholder Returns

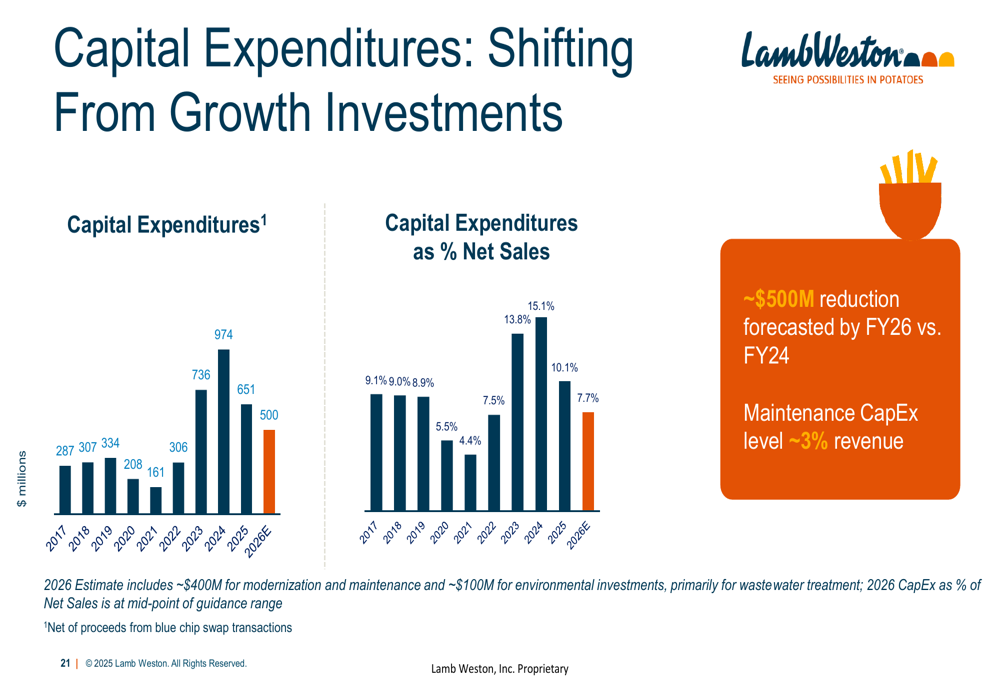

Lamb Weston is shifting its capital expenditure focus from growth investments to modernization and maintenance. The company expects capital expenditures of approximately $500 million in fiscal 2026, with about $400 million allocated to modernization and maintenance and $100 million for environmental investments, primarily wastewater treatment.

This chart illustrates the company’s capital expenditure trend:

In fiscal 2025, Lamb Weston returned $489 million to shareholders through dividends and share repurchases, with $358 million still remaining available under its current repurchase authorization. The company’s board declared a quarterly dividend of $0.37 per share.

FY26 Outlook and Guidance

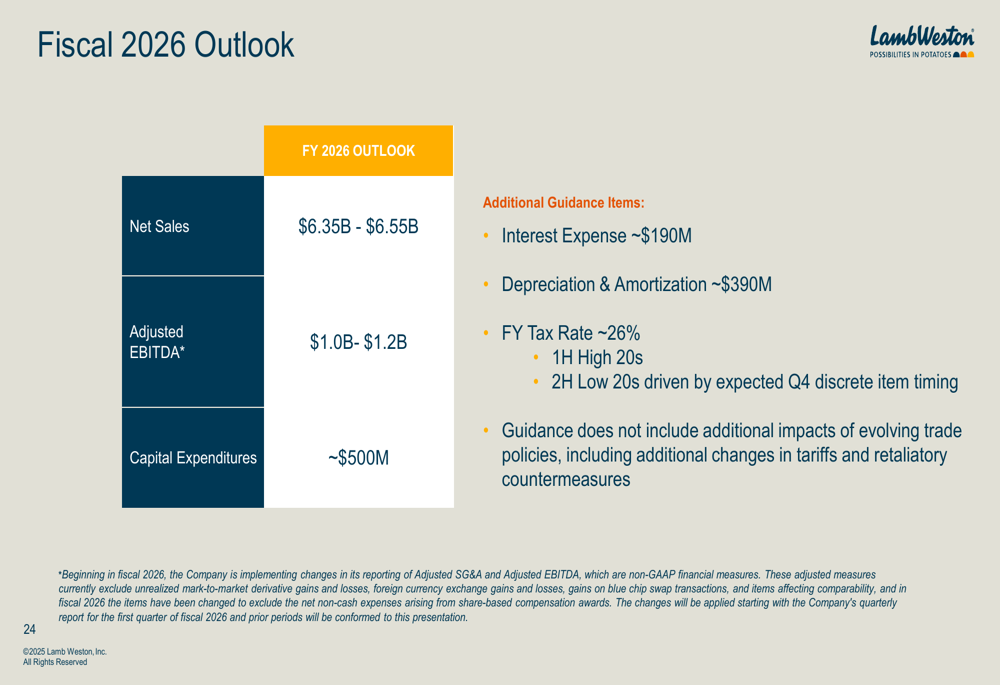

Looking ahead to fiscal 2026, Lamb Weston provided guidance that reflects continued challenges but anticipates benefits from its cost-saving initiatives. The company expects net sales between $6.35 billion and $6.55 billion, with adjusted EBITDA between $1.0 billion and $1.2 billion.

The fiscal 2026 outlook is summarized in this chart:

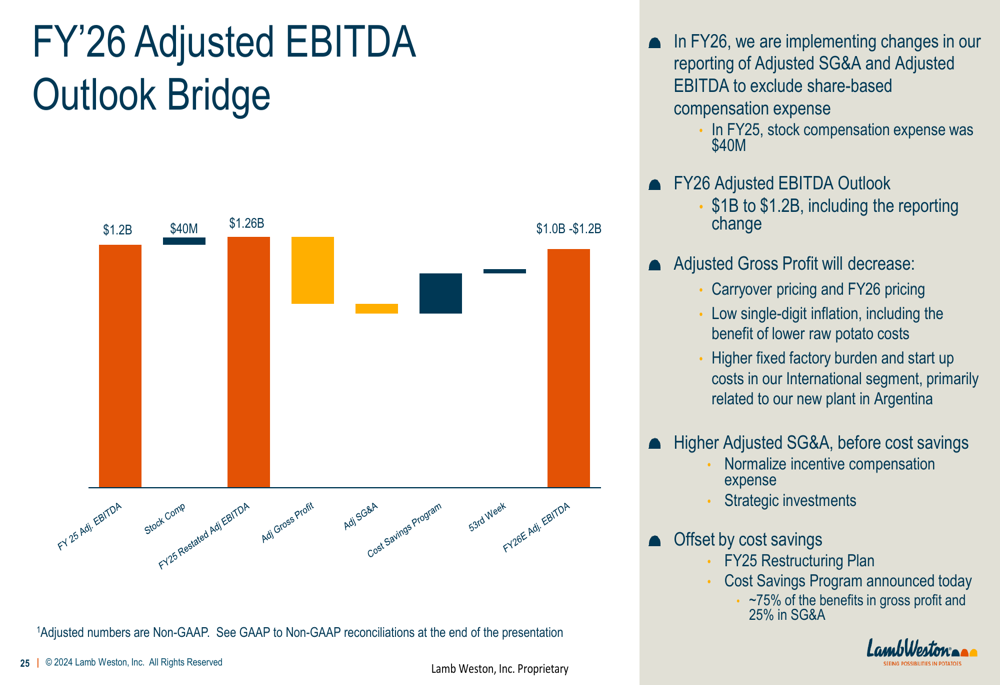

The company’s adjusted EBITDA outlook bridge shows the expected impacts of various factors on fiscal 2026 performance:

On the raw materials front, Lamb Weston reported that contract negotiations for the 2025 potato crop are complete, with a mid-single digit percentage decline in raw potato prices expected in North America. In Europe, the company anticipates an average crop with potato costs expected to be flat to slightly down year-over-year.

Market Context

Lamb Weston’s Q4 results and strategic shift come after a challenging period for the company. The stock has struggled, trading near its 52-week low of $47.87, despite showing some signs of stabilization in the fourth quarter. The premarket gain of 4.33% to $51.30 suggests investors are cautiously optimistic about the company’s restructuring plans.

The results follow a stronger third quarter when the company beat expectations with an EPS of $1.10 against a forecast of $0.89, which had driven a 6.86% stock price increase at that time.

As Lamb Weston implements its "Focus to Win" strategy and cost-cutting measures, investors will be watching closely to see if the company can successfully reverse the profit decline trend while maintaining its market position in an evolving competitive landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.