Can anything shut down the Gold rally?

Introduction & Market Context

Lantheus Holdings Inc (NASDAQ:LNTH) presented its second quarter 2025 results on August 6, revealing a 4.1% year-over-year revenue decline and significantly reduced full-year guidance. The diagnostic imaging company’s stock plummeted 24.27% in premarket trading to $55, reflecting investor concerns about the company’s near-term growth prospects.

The presentation, delivered by CEO Brian Markison and other executives, highlighted both challenges in the company’s core PYLARIFY business and strategic initiatives aimed at diversifying revenue streams through acquisitions and pipeline development.

This marked the second consecutive quarter of disappointing results for Lantheus, following Q1 2025’s earnings miss that previously drove the stock down 12.25%.

Quarterly Performance Highlights

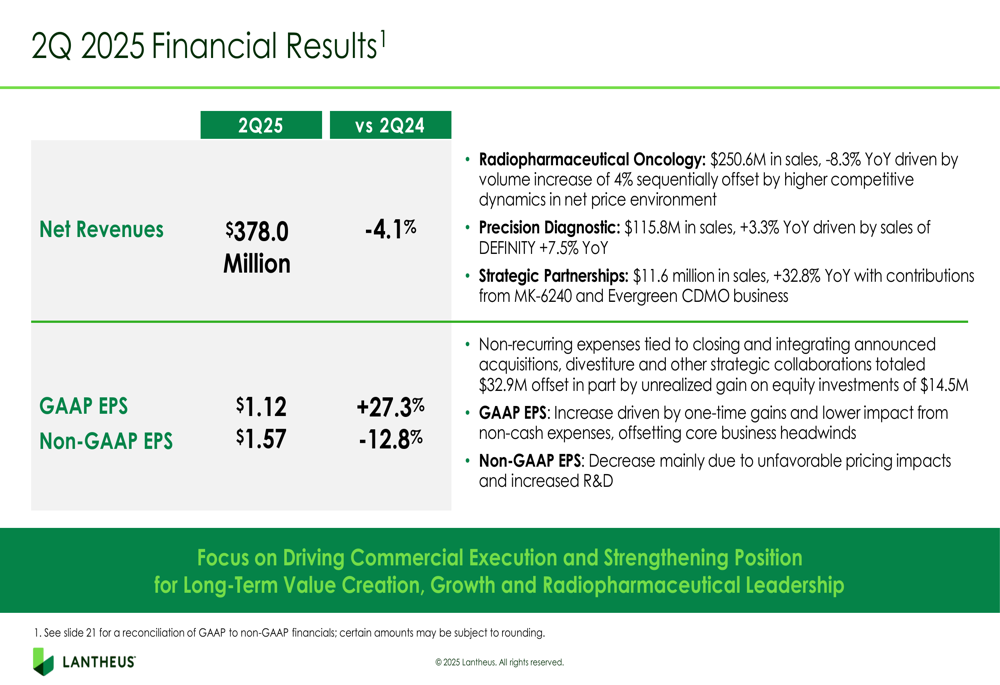

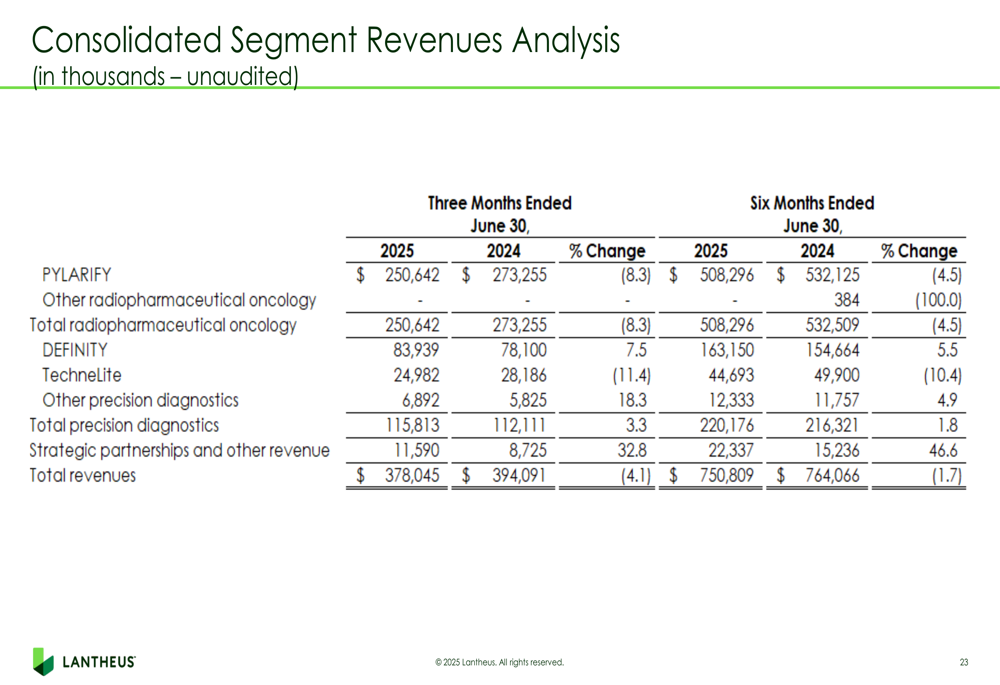

Lantheus reported Q2 2025 revenues of $378 million, representing a 4.1% decrease compared to the same period last year. Non-GAAP adjusted earnings per share came in at $1.57, down 12.8% year-over-year.

The company’s performance varied significantly across product lines:

- PYLARIFY, Lantheus’ radiopharmaceutical oncology product, generated $251 million in sales, declining 8.3% compared to Q2 2024

- DEFINITY, the company’s ultrasound enhancing agent, delivered $83.9 million in revenue, growing 7.5% year-over-year

- Strategic partnerships revenue reached $11.6 million, showing strong growth of 32.8%

As shown in the following comprehensive financial breakdown:

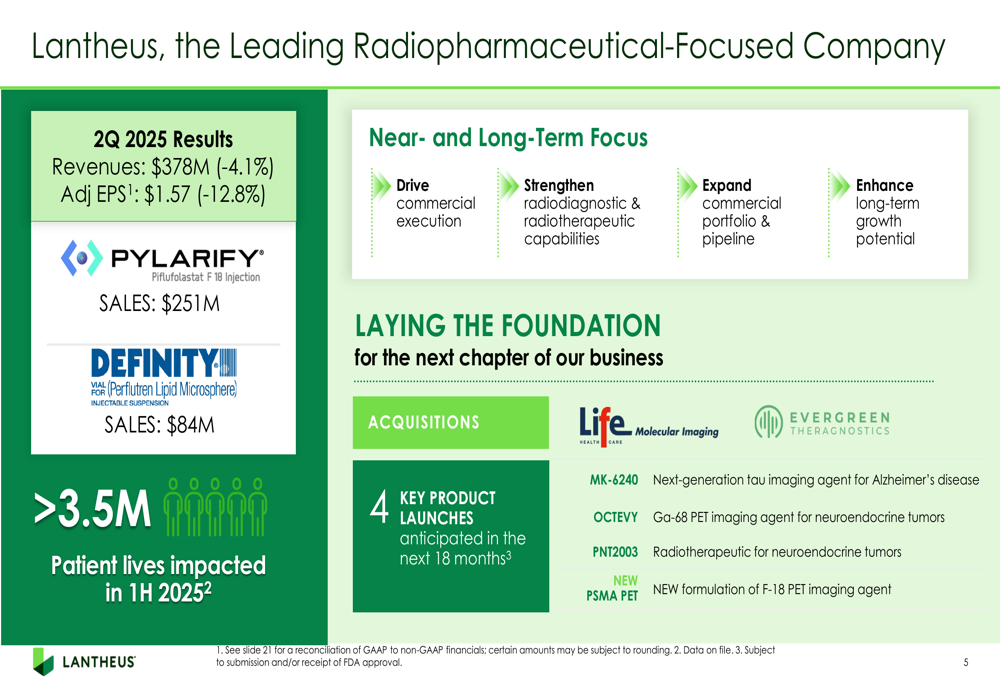

The company highlighted that over 3.5 million patient lives were impacted in the first half of 2025, underscoring the clinical importance of its products despite financial challenges.

Detailed Financial Analysis

Lantheus’ Q2 2025 financial results revealed mixed signals. While GAAP EPS increased 27.3% to $1.12, non-GAAP EPS declined 12.8% to $1.57. The company noted that non-GAAP EPS was negatively impacted by unfavorable pricing and increased R&D expenses.

Free cash flow improved to $79.1 million (including $7.5 million in non-recurring expenses), compared to $73.5 million in Q2 2024. The company maintained a strong balance sheet with $695.6 million in cash and $750 million in available revolving credit.

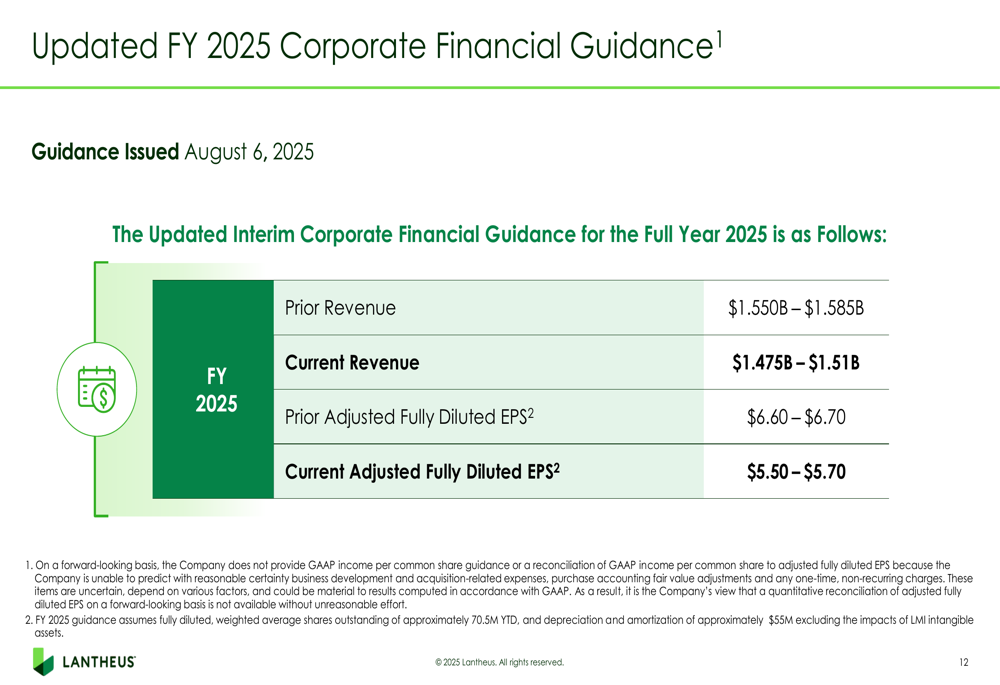

The most significant development was Lantheus’ substantial reduction in full-year guidance, as illustrated in this slide:

The company now projects full-year 2025 revenue between $1.475 billion and $1.51 billion, down from its previous guidance of $1.55 billion to $1.585 billion. Similarly, adjusted EPS guidance was slashed to $5.50-$5.70 from the prior $6.60-$6.70 range, representing a reduction of approximately 17%.

This guidance reduction follows a Q1 earnings miss and suggests ongoing challenges in the company’s core business, particularly with PYLARIFY, which is facing pricing pressures.

Strategic Initiatives

Lantheus emphasized its strategic focus on diversification and long-term growth potential through several key initiatives:

1. Recent acquisitions of Life Molecular Imaging and Evergreen Theragnostics to strengthen radiodiagnostic and radiotherapeutic capabilities

2. Four key product launches anticipated in the next 18 months:

- MK-6240: Next-generation tau imaging agent for Alzheimer’s disease

- OCTEVY: Ga-68 PET imaging agent for neuroendocrine tumors

- PNT2003: Radiotherapeutic for neuroendocrine tumors

- NEW PSMA PET: New formulation of F-18 PET imaging agent

The company’s near and long-term strategic focus is illustrated in this comprehensive slide:

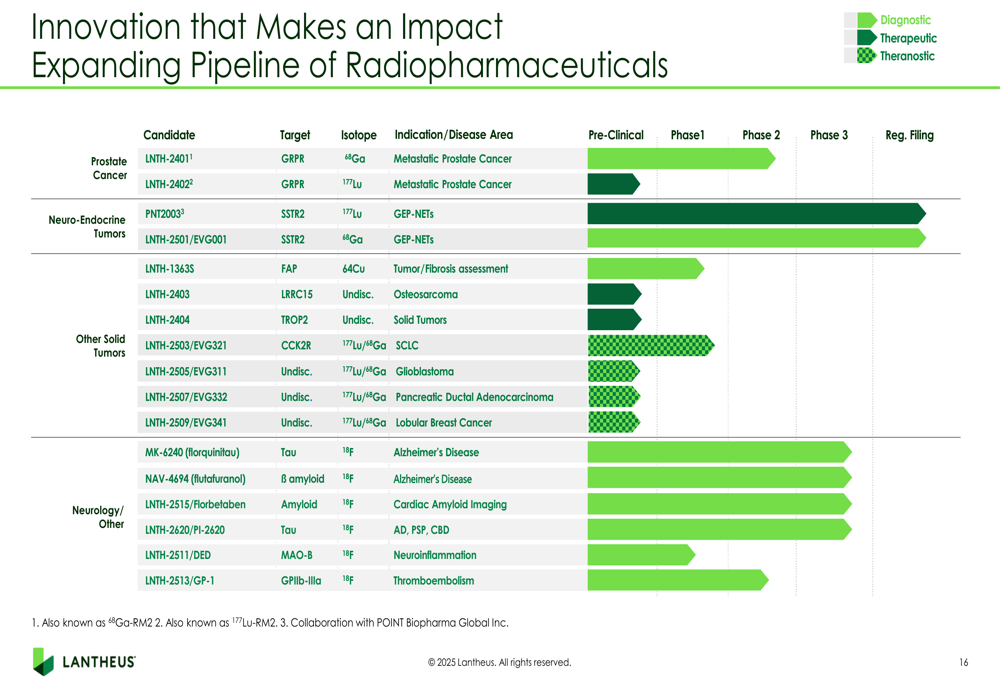

Lantheus also highlighted its expanding innovation pipeline across diagnostic, therapeutic, and theranostic applications, demonstrating the company’s commitment to diversifying beyond its current product portfolio:

Management emphasized maintaining market leadership through "clear and compelling clinical differentiation" and "disciplined pricing strategy," particularly for PYLARIFY despite its sales decline.

Forward-Looking Statements

Despite near-term challenges, Lantheus remains focused on its long-term growth strategy centered around its corporate purpose: "FIND, FIGHT and FOLLOW Disease to Deliver Better Patient Outcomes."

The company announced a new $400 million stock repurchase program, signaling management’s confidence in Lantheus’ long-term value proposition despite current headwinds. This financial flexibility is supported by the company’s strong cash position and free cash flow generation.

CEO Brian Markison emphasized the company’s commitment to "laying the foundation for future growth" through strategic acquisitions and pipeline development. The company’s segment revenue analysis provides insight into the current business mix and areas of growth potential:

While PYLARIFY’s decline presents a significant challenge, the growth in DEFINITY and strategic partnerships demonstrates the value of Lantheus’ diversification strategy. The company’s expanded pipeline, particularly in Alzheimer’s imaging and neuroendocrine tumors, represents potential future growth drivers that could offset current challenges.

However, investors appear skeptical about the near-term outlook, as evidenced by the sharp stock decline following the presentation. The significant guidance reduction suggests that Lantheus faces more substantial headwinds than previously anticipated, and the market will likely require concrete evidence of successful diversification before regaining confidence in the company’s growth trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.