Lisa Cook sues Trump over firing attempt, emergency hearing set

Introduction & Market Context

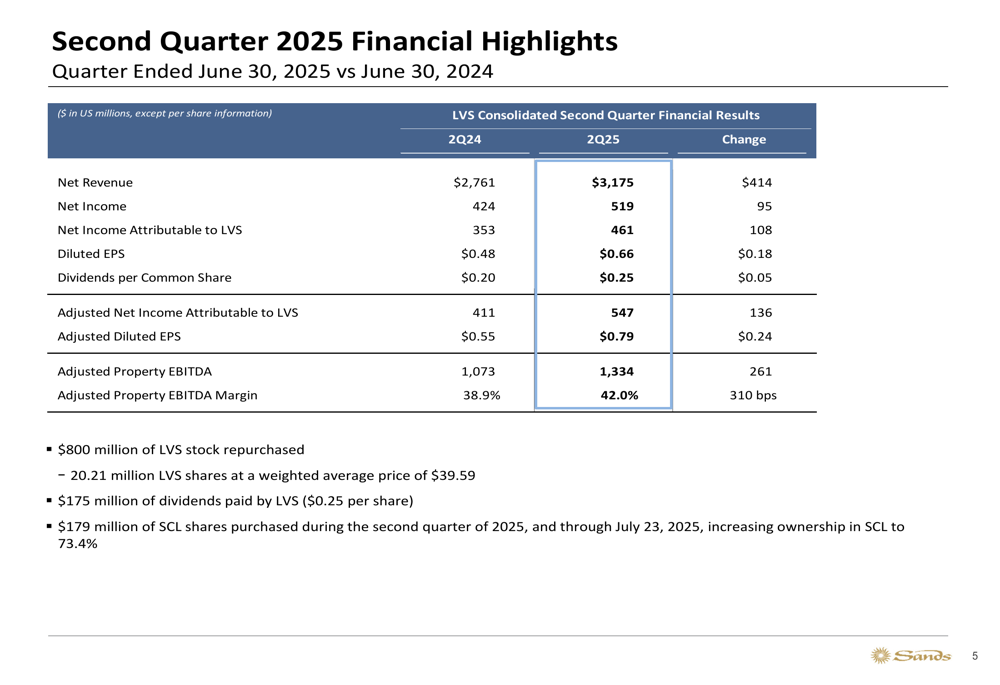

Las Vegas Sands Corp. (NYSE:LVS) released its second-quarter 2025 earnings presentation on July 23, showing strong financial performance driven primarily by exceptional results at its Marina Bay Sands property in Singapore. The company reported significant year-over-year growth across key metrics, with total adjusted property EBITDA reaching $1.33 billion, up 24.3% from the same period last year.

The results mark a notable improvement from the first quarter of 2025, when LVS missed analyst expectations on both earnings per share and revenue. The stock closed at $48.52 on July 23, showing a modest gain of 0.33% for the day, with limited movement in after-hours trading.

Quarterly Performance Highlights

Las Vegas Sands delivered substantial year-over-year growth across all key financial metrics in the second quarter of 2025. Net revenue increased to $3.18 billion, up 15% from $2.76 billion in Q2 2024. Net income attributable to LVS rose to $461 million, a 30.6% increase from $353 million in the prior-year period, while adjusted property EBITDA grew 24.3% to $1.33 billion.

As shown in the following comprehensive financial summary, the company’s profitability metrics also improved significantly:

Diluted earnings per share reached $0.66, up 37.5% from $0.48 in Q2 2024, while adjusted diluted EPS increased to $0.79 from $0.55. The company’s adjusted property EBITDA margin expanded to 42.0%, a 310 basis point improvement from 38.9% in the prior-year period.

Regional Performance Analysis

The company’s performance showed a stark contrast between its two main operating regions. Marina Bay Sands in Singapore delivered exceptional results, while Macao operations showed more modest growth.

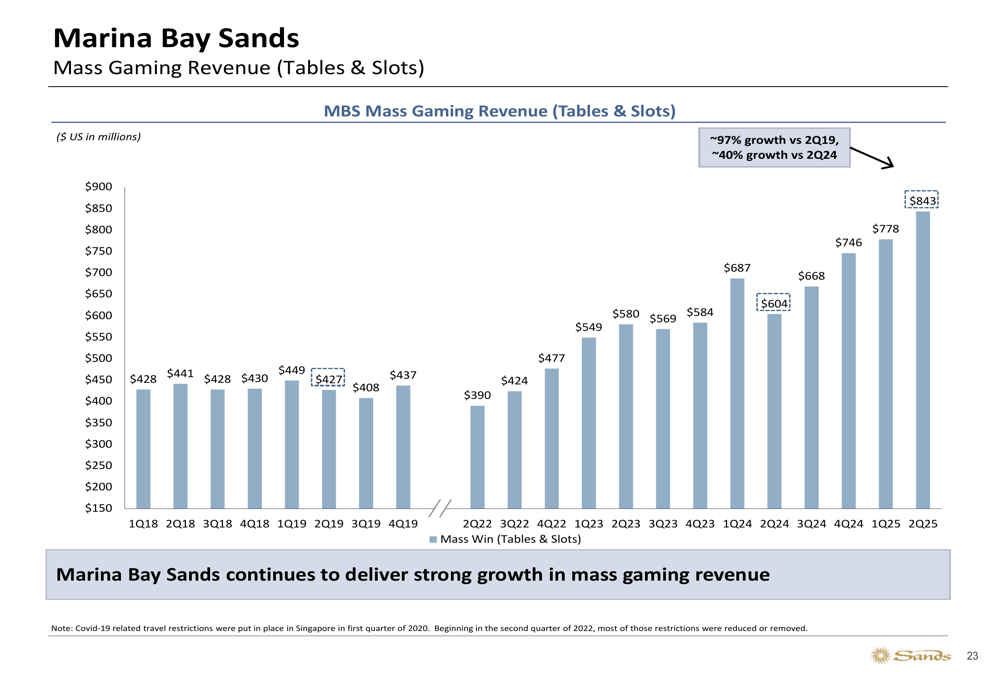

Marina Bay Sands generated adjusted property EBITDA of $768 million, a remarkable 50% increase from $512 million in Q2 2024. The property’s EBITDA margin expanded by 490 basis points to 55.3%. This performance was boosted by favorable hold in rolling play, which positively impacted adjusted property EBITDA by $107 million.

As illustrated in the following chart, Marina Bay Sands achieved record mass gaming revenue:

Mass gaming revenue at Marina Bay Sands reached $843 million in Q2 2025, representing approximately 97% growth from Q2 2019 and 40% growth compared to Q2 2024. The property’s strong performance follows the completion of its suite renovation and refurbishment program, which has enhanced its appeal to premium customers.

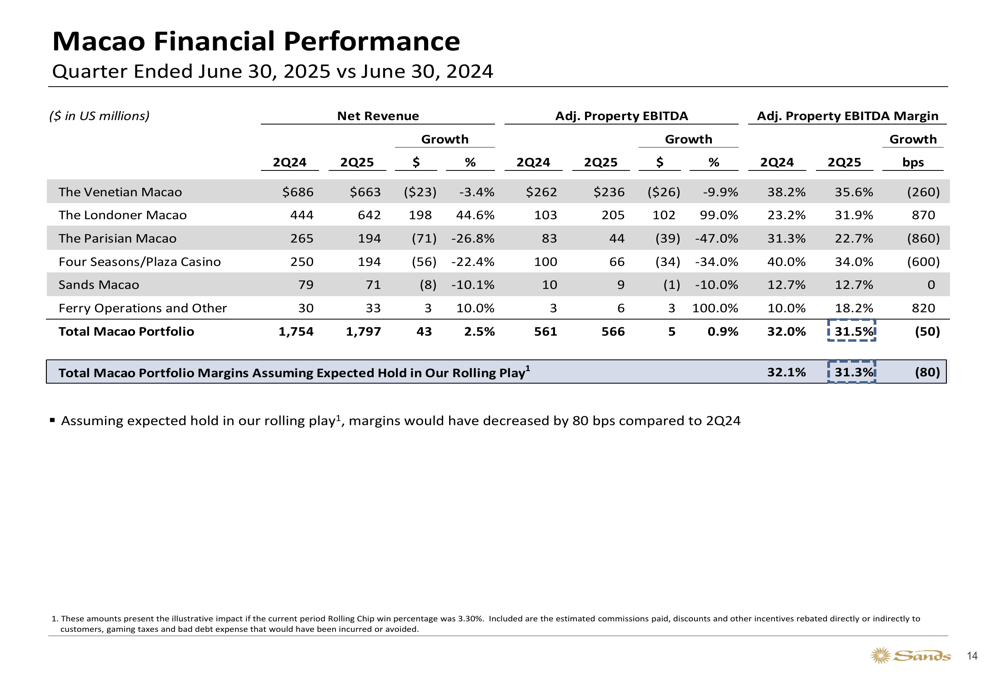

In contrast, Macao operations delivered more modest results, with adjusted property EBITDA of $566 million, just slightly above the $561 million reported in Q2 2024. The adjusted property EBITDA margin for Macao operations declined by 50 basis points to 31.5%.

The following breakdown shows the performance of individual properties within the Macao portfolio:

The Londoner Macao stood out with 44.6% revenue growth and a 99% increase in EBITDA compared to Q2 2024, reflecting the positive impact of recently completed renovations. However, this was offset by declines at other properties, particularly The Parisian Macao, which saw revenue decrease by 26.8% and EBITDA fall by 47%.

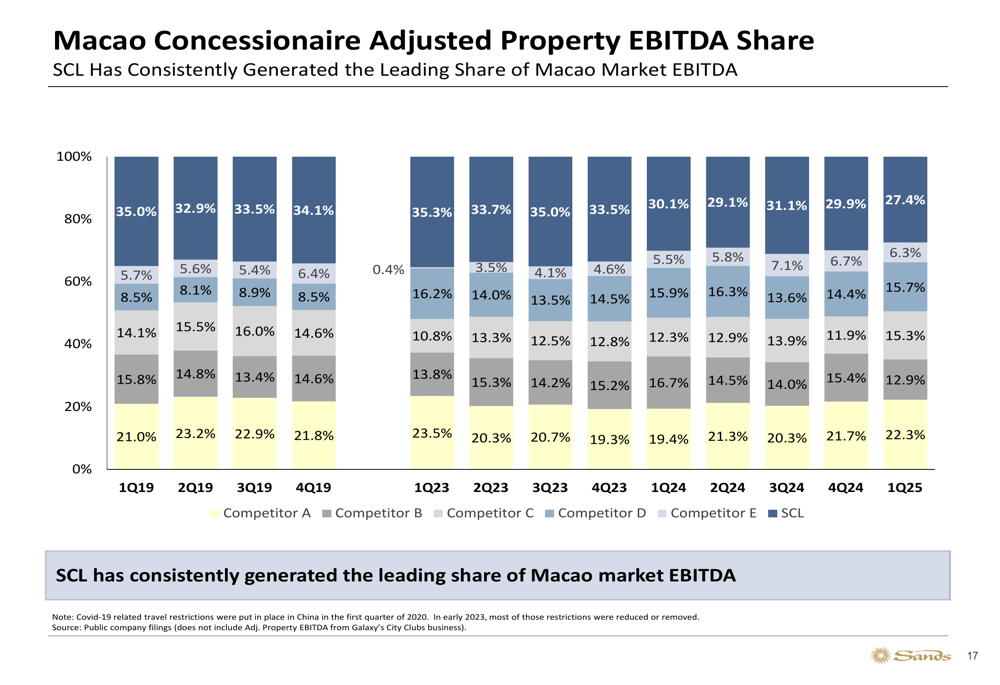

Despite these mixed results, Sands China Ltd (HK:1928). (SCL) continues to maintain its leading position in the Macao market, as shown in the following chart of concessionaire market share:

Strategic Initiatives and Capital Investments

Las Vegas Sands has completed its capital investment programs to increase suite capacity in both Macao and Singapore. The Marina Bay Sands property now features 1,844 keys, including 775 suites, following the completion of its renovation program.

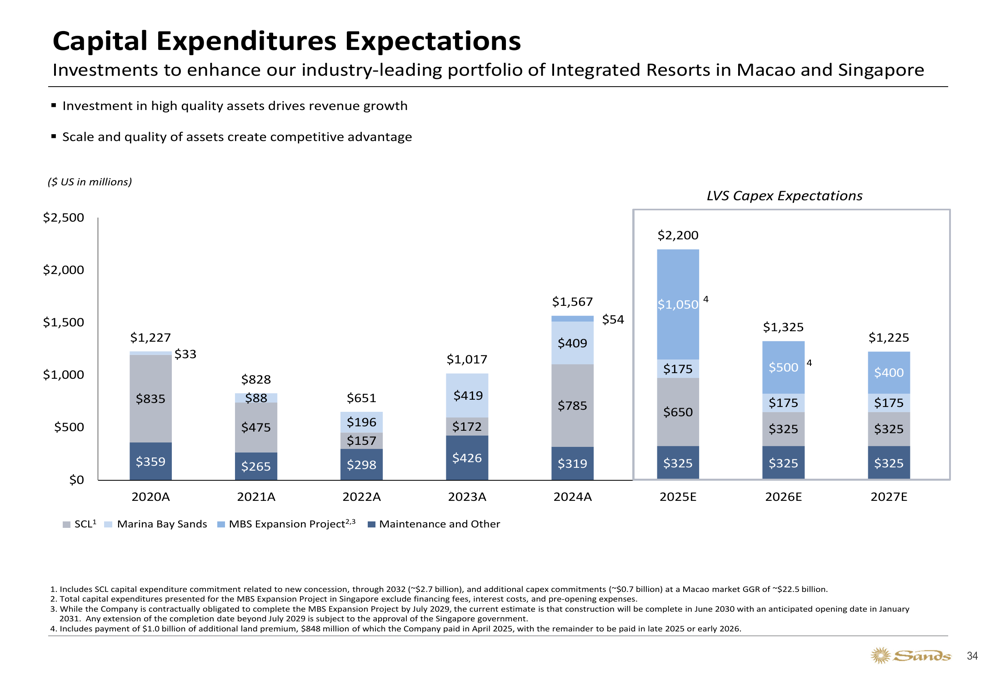

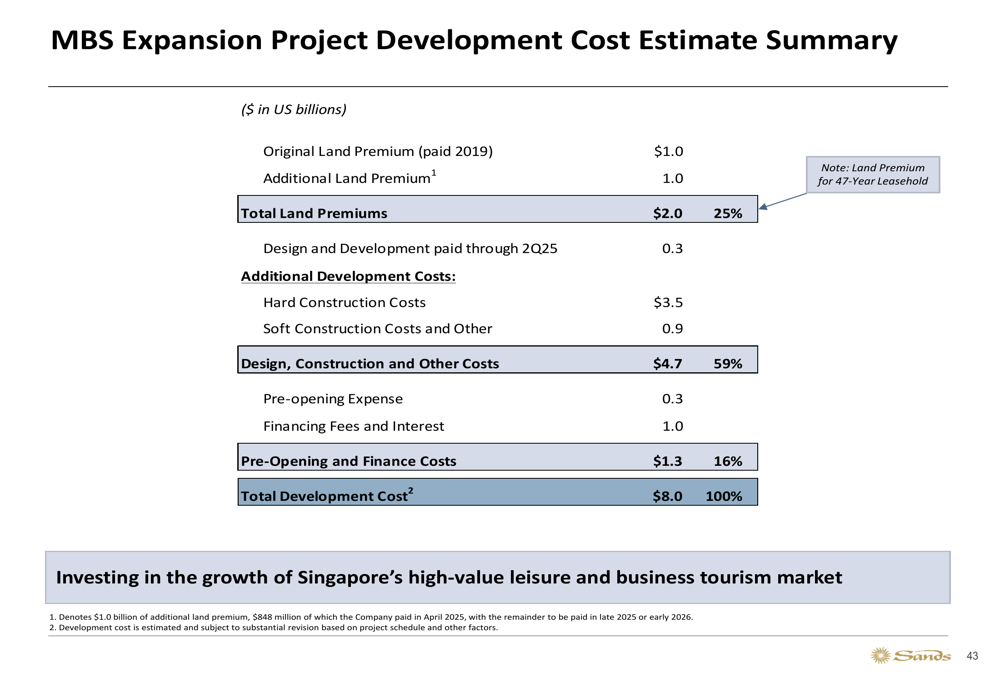

The company is now focusing on its ambitious Marina Bay Sands expansion project, with an estimated total development cost of $8 billion. The project is expected to open in January 2031 and includes an all-suite ultra-luxury hotel and other amenities designed to enhance Singapore’s tourism appeal.

The following chart outlines the company’s capital expenditure expectations through 2027:

For 2025, LVS expects total capital expenditures of $1.94 billion, with $785 million allocated to Sands China (OTC:SCHYY), $650 million to Marina Bay Sands, $175 million to the MBS expansion project, and $325 million to maintenance and other investments.

The breakdown of the Marina Bay Sands expansion project costs is detailed in the following chart:

Return of Capital to Shareholders

Las Vegas Sands continued its significant return of capital to shareholders in Q2 2025. The company repurchased approximately $800 million of LVS stock during the quarter, representing 20.21 million shares at an average price of $39.59. Additionally, LVS paid $175 million in dividends ($0.25 per share) and purchased $179 million of SCL shares, increasing its ownership to 73.4%.

Since the third quarter of 2023, LVS has focused primarily on share repurchases, which have accounted for approximately 74% of its capital return, with dividends making up the remaining 26%. Over the last seven quarters, the company has repurchased 10.3% of its outstanding shares.

Forward-Looking Statements

Looking ahead, Las Vegas Sands remains optimistic about its growth prospects, particularly in Singapore where the operating environment remains strong. The company expects its recent investments to contribute to growth in 2025 and beyond.

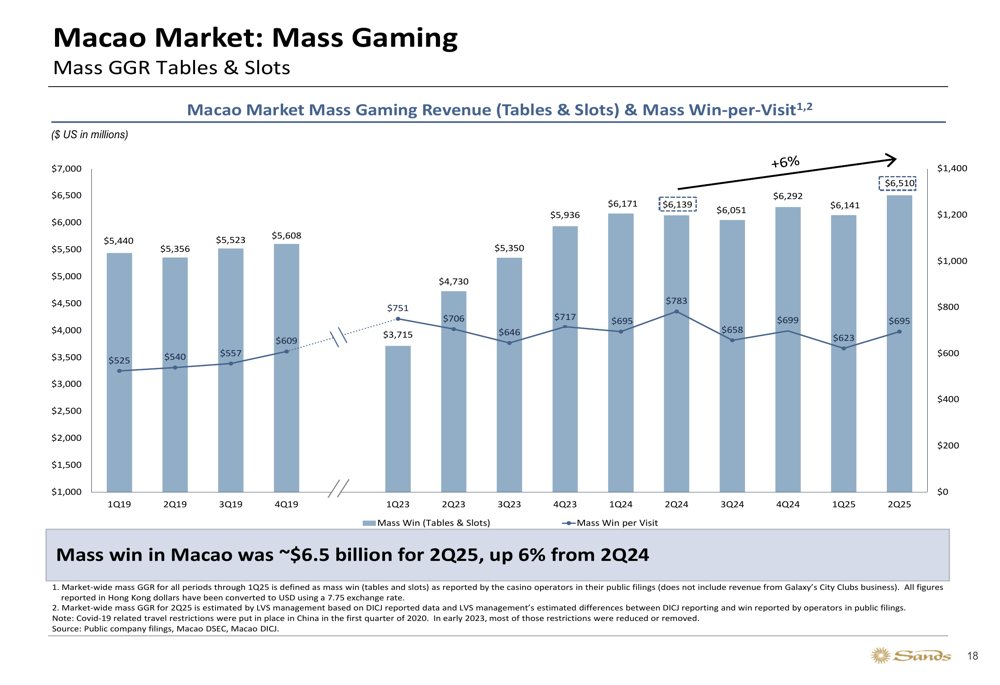

In Macao, the market recovery continues to be led by the premium mass segment, while the base mass segment remains below 2019 levels. The company noted that the growth rate of the Macao market improved in the second quarter of 2025, with total gaming revenue reaching approximately $7.6 billion, an 8% increase year-over-year.

The following chart illustrates the trend in Macao’s mass gaming revenue:

However, visitation to Macao remains below 2019 levels, with approximately one million fewer visitors from China excluding Guangdong Province. This suggests potential for further recovery as travel patterns normalize.

Las Vegas Sands’ strategic priorities include returning excess capital to shareholders through its share repurchase program and pursuing development opportunities in new jurisdictions, while maintaining its strong balance sheet and liquidity position.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.